OD6 announces ultra high grade fluorspar in USA - high enough for direct shipping ore?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 10,650,000 OD6 Shares at the time of publishing this article. The Company has been engaged by OD6 to share our commentary on the progress of our Investment in OD6 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

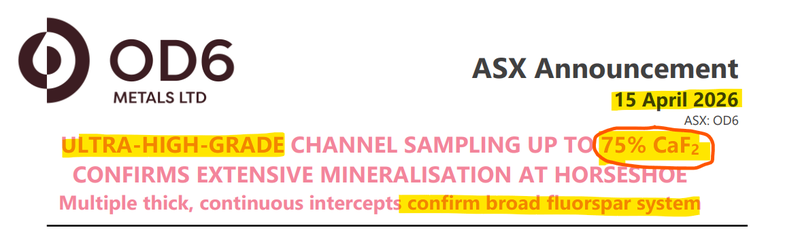

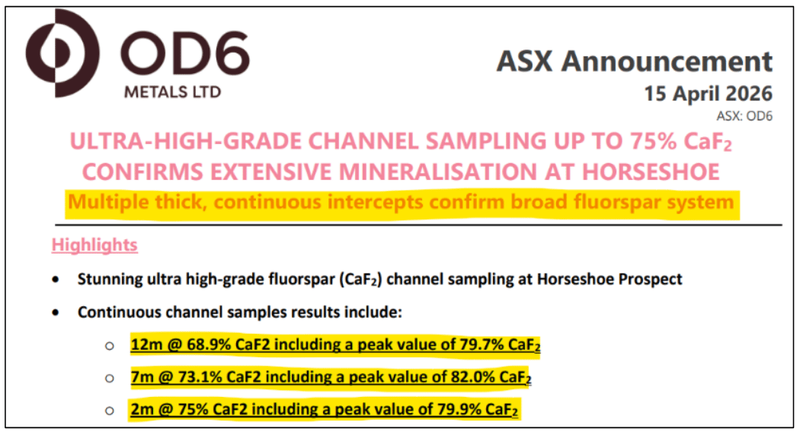

This morning our USA fluorspar Investment OD6 Metals (ASX:OD6) announced ultra high grades of fluorspar that could “support potential for Direct Shipping Ore (DSO)”...

... from surface, in and around the old open-pits that OD6’s historic mine was producing fluorspar from back in the 1950s in Nevada, USA.

Fluorspar is used in the production of missile systems, military electronics and jet fuel.

(not to mention an essential role in AI semiconductor chip production, batteries, nuclear power and aerospace)

The USA currently has no domestic supply.

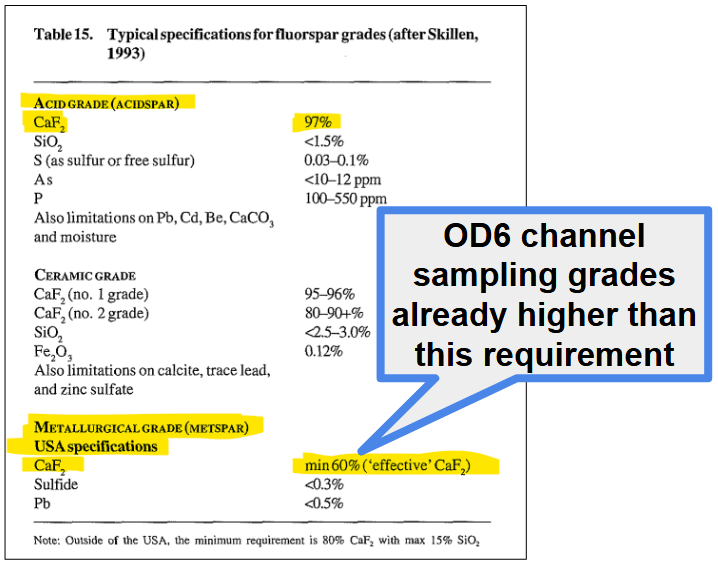

For us, the key takeaway from today’s announcement is that, based on the 60%+ grades, OD6’s project COULD be at a spec high enough to sell directly into the metallurgical fluorspar market.

(called “metspar” - used in steel making).

That’s what OD6 means when it's saying “potential for direct shipping ore (DSO)”.

Meaning the material could be mined and shipped directly to a buyer.

So the grades today (from surface) are literally high enough that the ore could be dug out and shipped directly as an end product for steel making with minimal processing required.

Some quick back-of-the-napkin calcs - even just 100,000 tonnes of steel making fluorspar would be worth ~US$40M+ (more on these numbers in a second - and note these numbers are based on a bunch of assumptions we made, things can change so don’t treat as gospel).

And the CAPEX wouldn’t be high because there is no processing (ie: no processing plant build costs).

OD6 Managing Director Brett Hazelden reckons this new development might enable OD6 to apply for a White House FAST41 application:

(source - today’s OD6 announcement)

A great potential nearer term cash flow source for OD6 while it works to fill the USA’s domestic supply gap of fluorspar for more “nationally strategic” use cases.

(military, AI, nuclear, aerospace and all that kind of stuff)

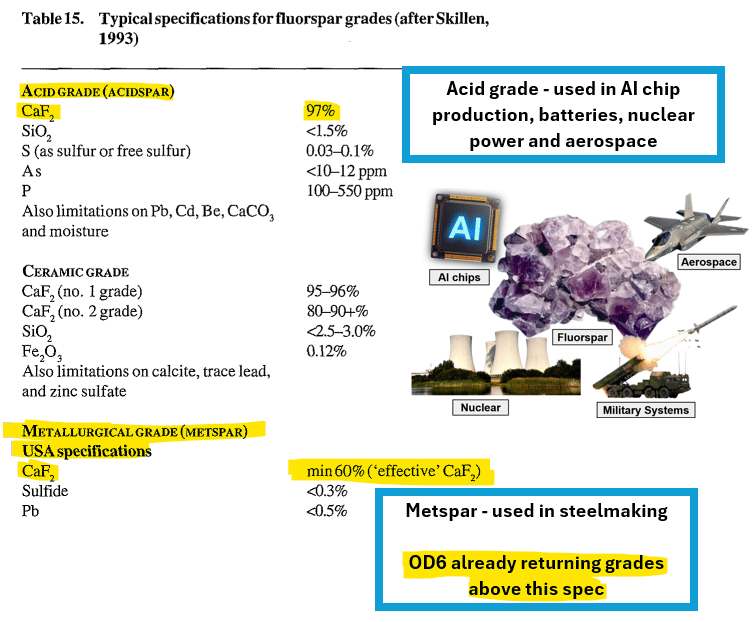

Fluorspar 101: Over 97% grade is known as ‘acidspar’. 60-96% grade is known as ‘metspar’.

(source)

OD6 is announcing today’s news into a market where the US government is actively looking for domestic fluorspar production to fill up its critical mineral stockpile.

That US critical mineral stockpile just happens to sit 300km from OD6’s project.

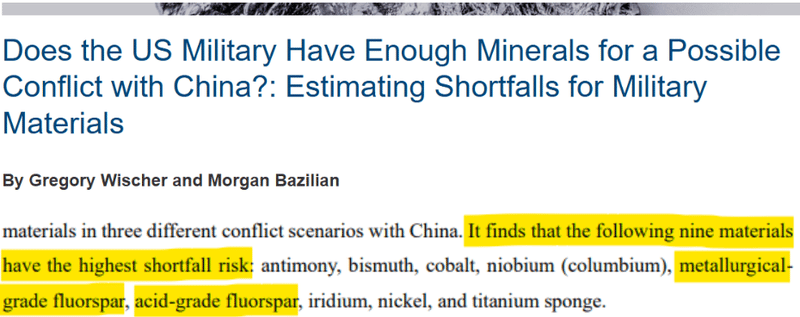

Fluorspar is one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario. (source)

(a major conflict like we are seeing in the Middle East right now...)

Over the last ~4 months, US government agencies (mostly military related) have:

- Issued a US$250M contract to purchase fluorspar from a pre-revenue micro cap (issued by the US Pentagon) (20th of January 2026), AND;

- the US Defence Logistics Agency (DLA) included fluorspar on its list of critical minerals that are a priority for sourcing (30th of January 2026).

Two signals within the last 4 months from the US government trying to incentivise domestic production.

One of our key reasons for Investing in OD6 was because it is the only ASX listed company with a fluorspar asset in the USA (in Nevada).

We think OD6’s asset could realistically become a potential supply source for the US - the same way the project was mined back in the 1950s.

(only this time, into a market where the US government is an active buyer).

OD6’s asset produced fluorspar from a small scale mining operation in the 1950s and based on historic sampling data alone, the project already has a non-JORC resource estimate.

And now, OD6 has sampled parts of the project that were mined in the past - returning grades that OD6 says “support potential for Direct Shipping Ore (DSO)”.

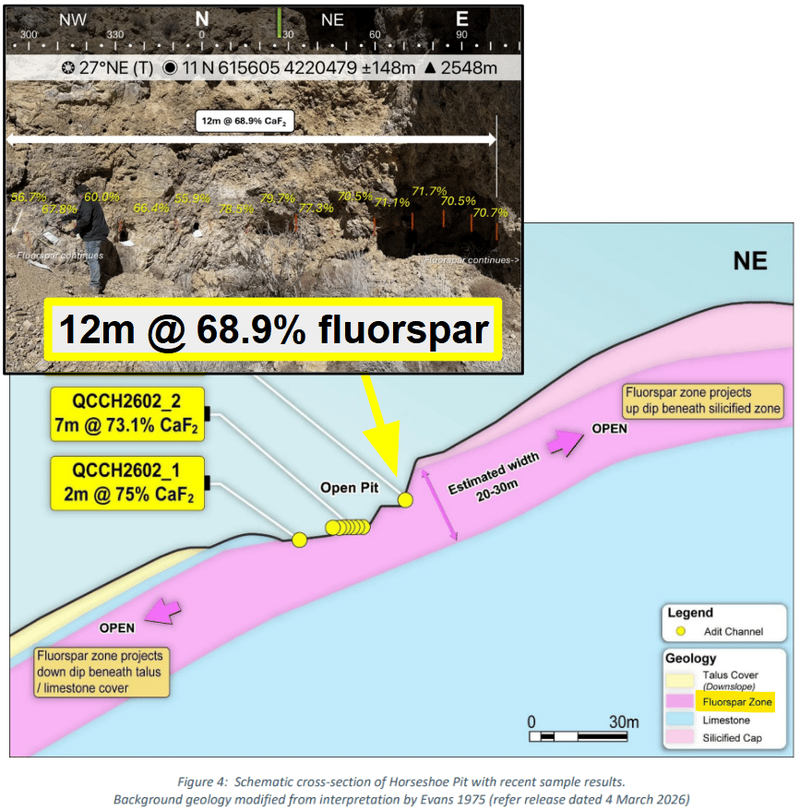

The old production from the project produced ~26,000 tonnes of material at an estimated grade of 44.9% fluorite. (source)

Today’s channel samples returned 12m at 68.9% and peak values of 82% - grades that could be mined and sold directly without any processing.

(source)

OD6’s project has never been drilled before - all of the previous mining was limited to near surface material from the side of a hill.

So we don't really know how big the project is in terms of tonnage.

But IF those 60-70%+ grades are consistent across the project AND OD6 can deliver a few drill holes that hit 10-20m+ intercepts with similar grades...

THEN, the concept of a small scale mining operation being spun up again for minimal costs means producing a DSO product becomes an option.

(remembering that OD6 already has a non-JORC resource estimate - which can't be announced because it is from 1956 and has not been verified under current JORC guidelines. source)

We did a bit of digging (...get it?) on what a small scale mining operation might look like.

Here are the typical grades needed for the different fluorspar markets:

(source)

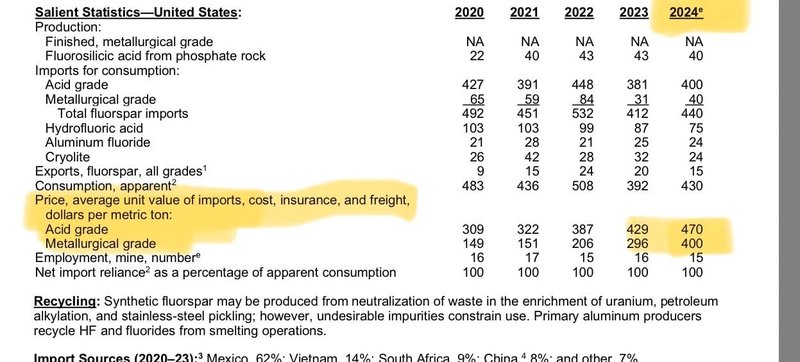

And according to the US Geological Survey (USGS), 60%+ metallurgical grade fluorspar was selling for US$470 per tonne in 2024:

(source)

So without any processing, literally just digging up the dirt, OD6 could have a US$400 per tonne product.

Even just 100,000 tonnes of that product would be >US$40M in revenues for $48M capped OD6.

All done with little to no processing (that’s what OD6 means when it says its project is returning Fluorspar grades that could “support potential for Direct Shipping Ore (DSO)”.

We are only talking 100,000 tonnes too, IF a few drillholes come in and OD6 can show there is size/scale to its project then OD6’s optionality changes in a big way.

OD6’s project could also be a lot bigger than we first thought

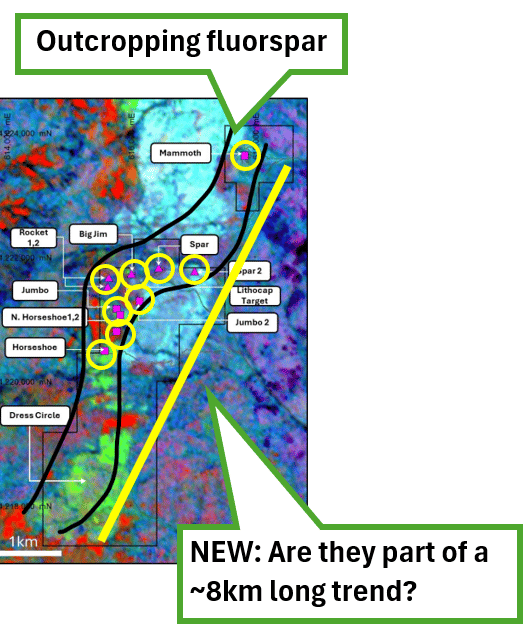

A few weeks ago, OD6 announced they had defined a ~8km long trend “linking multiple historic fluorspar occurrences across the project”.

(source)

Think of it like at first seeing a bunch of individual icebergs floating along in the water:

But then it turns out they are all actually part of one big iceberg underneath:

What this means is that potentially all of the OD6’s original, smaller fluorspar occurrences could actually be part of one bigger, underground system (that has never been drill tested before):

Ultimately, we will need to see OD6 drill its project and test that theory...

(all the icebergs tips above the water illustrate historically mined pits from surface, nobody has ever drilled this project to see if they are connected, that’s what OD6 will be doing)

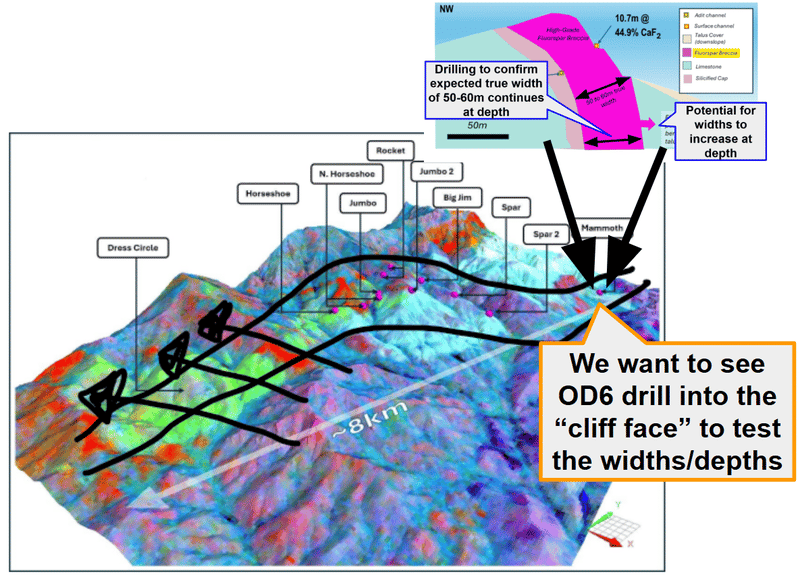

What we don't know YET is how big the “estimated widths” are - which will require OD6 to do some drilling to find out.

Next we want to see OD6 drill test the project and hopefully reveal thick fluorspar rich zones behind the wall faces (hopefully all across the ~8km long trend):

No guarantees there will be fluorspar deeper in the ground though - we’ve been burnt by a few ‘drilling into a hill face with surface mineralisation’ before - there’s always a chance OD6 drills dusters here.

Ultimately, drilling and attracting some sort of US government funding or strategic offtake/supply deal is central to our OD6 Big Bet which is as follows:

Our OD6 Big Bet:

"OD6 re-rates to a +$200M market cap by defining a significant fluorspar resource in Nevada, attracting US government funding or a strategic offtake/supply deal, and/or attracting a takeover bid at multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our OD6 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

OD6 Metals

11 reasons why we Invested in OD6

Here is our full initiation note for OD6 from back in March: Our Latest Investment: OD6 Metals (ASX: OD6)

Also, here are the 11 reasons why we Invested in OD6.

1. Low market cap with room to re-rate higher.

OD6 will have a market cap of ~$13.5M and an enterprise value closer to ~$8M (at 5c per share) following the completion of the capital raise announced today.

We think the company’s current valuation is at a level where it can re-rate to multiples of where it is now - especially IF the “US critical minerals playbook” is executed well and the market continues to reward the sector - and of course some successful drill results confirming the size and scale of the deposit.

No guarantees of course - this is small cap early stage resources investing - things can and do go wrong.

Update: OD6 is up 270% from our Initial Entry Price in 6 weeks and now has a market cap of $48M (at 18.5c per share).

Past performance is not an indicator of future performance.

2. OD6’s Fluorspar asset is in Nevada, USA. We have had past success in Nevada.

We like Nevada as a mining jurisdiction within the USA because it's home to some of the biggest, lowest cost mines in the country, and we have had some good success in Nevada before (SS1, BKB, VKA).

The past performance of these stocks is not an indicator of future performance of OD6.

3. OD6’s projects have produced fluorspar in the past but have never been drilled.

The project OD6 is acquiring has produced 26,000t from a small scale open pit before. The project has never been drilled before either. The mining was limited to carving out a hillside... we wonder what systematic exploration drilling could yield?

This project DOES have a historic resource - but can’t be announced because it is from 1956 and has not been verified under current JORC guidelines. (source)

4. OD6 is a ASX listed first mover into US fluorspar assets

As far as we know, right now, there are no other ASX listed companies with pure-play fluorspar assets in the US.

We have observed that the first movers in an emerging investment thematic often do the best.

Update: As far as we know, OD6 continues to be the only ASX-listed company with direct fluorspar exposure in the United States.

5. Fluorspar is listed as one of the 12 strategic defence critical minerals in the US -

The Pentagon explicitly mentioned fluorspar as one of the minerals it is looking to buy as part of its US$12BN critical minerals stockpile. (source)

Fluorspar has been identified as one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario.

6. The US Department of War awarded a US$169-250M supply contract to another US based fluorspar asset in January 2026 (source)

It’s clear the Department of War wants to secure its domestic fluorspar supply given the contract award of a few weeks ago.

We are backing OD6 to define a fluorspar resource of its own, fast-track it toward development and hopefully one day, receive similar funding deal/purchase contracts.

7. China controls 60% of Fluorspar supply

The US has zero domestic fluorspar production which we think makes projects like OD6 (inside US borders) valuable.

8. There is a listed Fluorspar success story on the ASX capped at $974M

We think that having a success story in the market is important. ASX listed Tivan has a fluorspar asset in WA and is capped at $974M.

Tivan’s project looks to be targeting supply into Asia. We are backing OD6 to achieve success by targeting supply into North America (mainly the US).

Update: Tivan’s market cap now sits at ~$816M.

9. Capital is flowing into US critical minerals macro thematic

We think OD6’s US fluorspar asset could attract increased capital flows both on the ASX and from North American investors/governments/institutions.

10. OD6 can follow the “US critical minerals playbook”

There is a playbook for ASX stocks to attract more attention and capital to projects that are based in the US (source) . OD6 isn’t yet listed in the US. We think that if its project gets any market traction it could go for a US listing that opens up the company to North American investors.

11. Free kick on “one of Australia’s largest and highest grade clay hosted rare earths deposits” (source)

OD6 also owns one of the largest and highest-grade clay-hosted rare earth deposits in Australia which in its own right could become a company maker.

We are mainly Invested in OD6 for the US fluorspar project, but the WA rare earths asset in the company is sort of a “free option” for us.

Why fluorspar?

For anyone who hasn’t heard of fluorspar before - here is why we think the US military is throwing cash at securing supply.

Fluorspar is critical for producing:

- Missile systems - fluorspar is required to produce hydrofluoric acid, which is used in missile guidance electronics

- AI semiconductor chips - used in the etching process for advanced chip manufacturing

- Military batteries - lithium-ion batteries require fluorine, and there's no fluorine without fluorspar

- Nuclear fuel - essential in uranium processing for nuclear power and weapons

- Aerospace and defence - used in jet fuel production and radar systems

Fluorspar has been identified as one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario:

(like the conflict that is happening right now...)

(source - from the full paper)

Fluorspar was one of the O.G. critical minerals - making it into the US critical minerals list way back in 2018 - it has maintained its status on that list ever since.

And fluorspar was one of the few minerals that was added to the tariff exemption list by the Trump administration in April 2025.

(source)

(meaning that supply was too important to the US to mess with by imposing import tariffs)

Those tariff exemptions end in July. So who knows what happens to fluorspar prices inside US borders at that point.

The US consumes ~400,000 metric tonnes of fluorspar per year and produces effectively zero domestically.

That gap - combined with China controlling ~60% of global supply - is why the Pentagon handed Ares Strategic Mining up to US$250M to develop domestic fluorspar production.

(source)

We also like that there is a fluorspar success story on the ASX already - $816M capped Tivan Ltd

One of the reasons we Invested in OD6 is because there's already a fluorspar success story on the ASX.

$816M capped Tivan has a fluorspar project in Western Australia that is currently in a Joint Venture with $61BN Japanese Conglomerate Sumitomo.

That JV tells us that the Japanese have a foot on the fluorspar that will come out of Tivan’s projects.

That means there's currently no real way to get US fluorspar exposure on the ASX - outside of OD6.

We also like that OD6’s asset is (so far) returning much higher grades than Tivan’s project too.

And OD6's grades are multiples higher than Tivan's.

Tivan’s resource is 43.2mt at 8.3% Fluorspar. (source)

Whilst OD6 does not have a defined resource estimate yet, OD6 is sampling grades up to 94% in rock chips and after today’s news ~60-82% across channel samples.

(source)

Remember OD6’s project produced fluorspar from a small scale mining operation in the 1950s - it produced ~26,000 tonnes of material at an estimated grade of 44.9% Fluorite. (source)

Even just using those old production grades - that’s ~7.5x the average grade of Tivan’s resource.

Tivan is capped at $816M.

OD6 - with an asset in the US - is capped at $48M.

Now, Tivan is a lot more advanced relative to OD6 with a defined resource estimate and a major partner involved backing its project. Market cap differences reflect these vastly different stages of development.

But so far we have some precedents set for:

- A pre-resource asset in the US gets a US$169M supply contract signed, and

- A company with a big resource brings in a multi billion dollar partner.

Validation for us that an asset with both (a resource AND inside US borders) could end up being a company maker for an ASX small cap.

What's next for OD6?

🔄Complete the acquisition of its US fluorspar project

We want to see OD6 complete acquisition of the US fluorspar project, this will give it full unencumbered access to help it progress the asset.

Milestones:

- 🔄 Due diligence process completed

- 🔲 Option to acquire exercised

- 🔲 Acquisition completed

🔄 Target generation for US fluorspar project

We want to see OD6 sample in and around the old workings on its project, run some geophysics and generate high priority drill targets ahead of its maiden drilling program.

Milestones:

- ✅ Rock chips

- ✅ Channel sampling

- 🔲 Soil sampling

- 🔲 Geophysics

- 🔲 Drill targets generated

Strategic / Government Engagement for fluorspar in the US

- 🔲 Engage with US Department of War, Department of Energy, or DLA regarding domestic fluorspar supply

- 🔲 Explore strategic partnerships or offtake discussions

What could go wrong?

With exploration set to get underway in the near term, the most obvious risk for OD6 in the short term will be “exploration risk” and “deal risk”.

OD6’s project has never been drilled, and there is no guarantee that drilling confirms a significant fluorspar resource from surface to depth.

Exploration risk

OD6 is at an early stage. The Quinn Fluorspar Project has never been drilled. There is no guarantee that drilling confirms the presence of a significant fluorspar resource at depth, even though historic mining, surface mapping, and satellite analysis are encouraging. Early-stage exploration is inherently risky and many projects fail to deliver economic mineralisation.

Source: "What could go wrong" - OD6 Investment Memo 4 March 2026

There is also a risk that the deal is not completed on OD6’s end.

At the moment, OD6 is still in the due diligence phase.

Acquisition completion risk

OD6 has secured an option over the Quinn assets but has not yet completed the full acquisition. The deal is structured with an upfront $275k IF the option gets exercised and then milestone-based deferred payments totalling plus A$3.8M. (source) There is a risk that OD6 does not proceed past the option stage if due diligence is unsatisfactory, or that later milestones prove difficult to fund.

Source: "What could go wrong" - OD6 Investment Memo 4 March 2026

Other risks

Like any early-stage exploration company, OD6 carries significant risk, here we aim to identify a few more risks.

With zero revenue, OD6 relies on capital markets to fund its progress. Capital raises can dilute existing investors and it's possible any capital raise is not on favourable terms for existing investors.

While OD6’s project has historical production, modern critical mineral supply chains require highly refined end products like acid-grade fluorspar.

There is no guarantee that the raw ore from the Quinn project can be economically processed and upgraded to meet the strict purity specifications required by US military or battery manufacturers.

The project also relies on exploring and potentially restarting a historic 1950s mine site in Nevada. While Nevada is a tier-1 mining jurisdiction, historic sites can sometimes carry legacy environmental liabilities.

Securing modern environmental approvals and drill permits for a site that hasn't operated in ~70 years could cause unforeseen delays or add unexpected compliance costs.

Additionally, OD6 is attempting to aggressively advance a brand-new US fluorspar project while also holding a massive clay-hosted rare earth deposit in Western Australia.

Managing two vastly different projects across two continents requires significant management bandwidth and capital.

There is a risk that company resources are stretched too thin, slowing overall progress or forcing the company to deprioritise one of the assets.

Finally, as a micro-cap company, OD6 shares may suffer from low trading liquidity. This means investors may find it difficult to buy or sell large volumes of shares on the ASX without significantly impacting the share price, leading to heightened volatility.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our OD6 Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our OD6 Investment Memo where you will find:

- What does OD6 do?

- The macro theme for OD6

- Our OD6 Big Bet

- What we want to see OD6 achieve

- Why we are Invested in OD6

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.