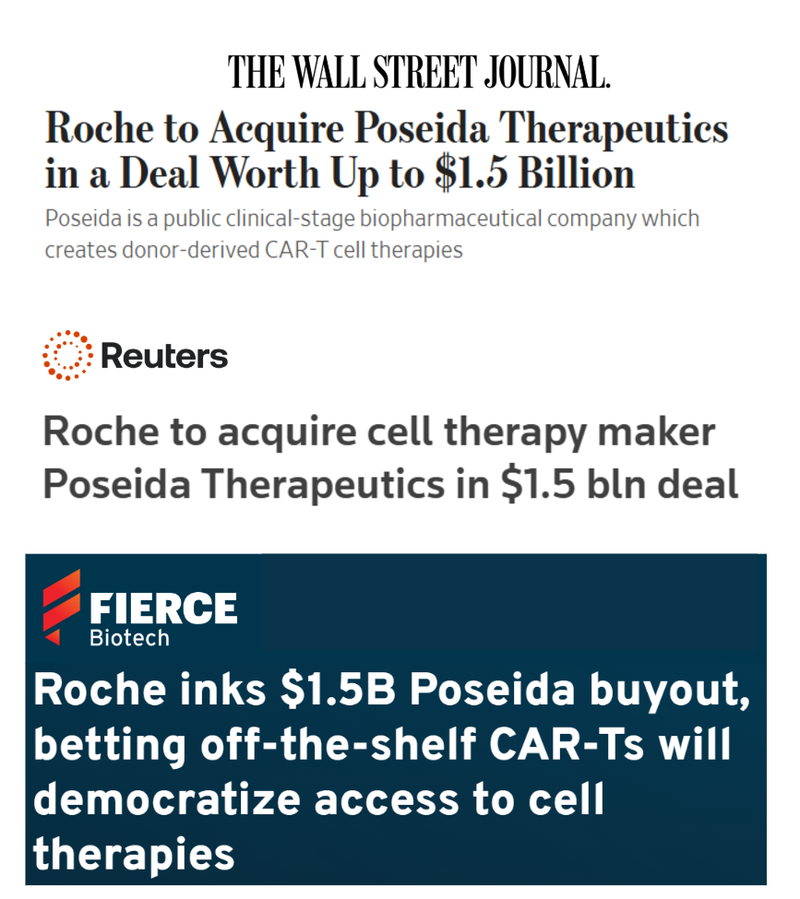

Cell therapy company just acquired by Roche for US$1.5BN. ALA looks similar…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,410,000 ALA shares and 480,000 ALA options at the time of publishing this article. The Company has been engaged by ALA to share our commentary on the progress of our Investment in ALA over time.

60 hours ago news broke that global pharma giant, the US$410BN Roche, is acquiring a small Phase 1 “cell therapy for cancer” company called Poseida Therapeutics...

... for US$1.5BN.

Our biotech Investment, the AUD $200M capped Arovella Therapeutics (ASX:ALA) is also a “cell therapy for cancer” company.

ALA is starting its Phase 1 trial in 2025...

Poseida had been waiting for its Phase 1 trial results - but now it has been acquired by Roche.

Phase 1 trials is the point where we typically start to see M&A activity by Big Pharma in this space.

Like Roche’s acquisition this week and AstraZeneca’s US$1.2BN move on Graacell in December 2023.

(there’s many more - we share a full list further down the page).

This week we also noticed that a prominent researcher who helped get a cell therapy through the FDA approval process for Kite Pharma, has recently popped up on ALA’s clinical advisory board.

Kite Pharma was acquired by Gilead Life Sciences for US$11.9BN in 2017.

More on this in a minute...

But back to the Roche ‘deal of the week’.

Roche plans to acquire a company called Poseida Therapeutics for US $1.5BN - comprising US$1BN in cash and then another $500M in additional performance related payments.

We think Poseida and the A$200M capped ALA are similar in a lot of ways:

- Both are targeting blood cancer

- Both are focused on off-the-shelf (allogenic) cell therapy - ALA is iNKT, Poseida is CAR-T.

- Both also have a solid tumour therapy (Poseida is recruiting for Phase 1, ALA is preclinical)

- Both are developing platform technologies, meaning once the tech works, it can be used across multiple diseases.

- Poseida is at Phase 1 trials, ALA is looking to enter Phase 1 in 2025.

Poseida was taken over by Roche for up to US$1.5BN, ALA is capped at A$200M.

(Source 1, Source 2, Source 3)

An interesting takeaway for us was that the acquisition was made BEFORE the readout of Poseida’s phase 1 trial results.

ALA expects to complete its Investigational New Drug (IND) submission with the FDA in Q1 2025 and get into the clinic next year.

Even though it can be a risky bet for the big pharma company, we have seen that there is a willingness to do these type commercial deals at inflection points for the smaller companies.

Sometimes, they happen before a company enters the clinic (pre-clinical) and sometimes before the readout of phase 1 trial results.

(probably because this is when the big pharma company and the smaller target are able to agree on a deal that makes sense considering the risks/costs of trials).

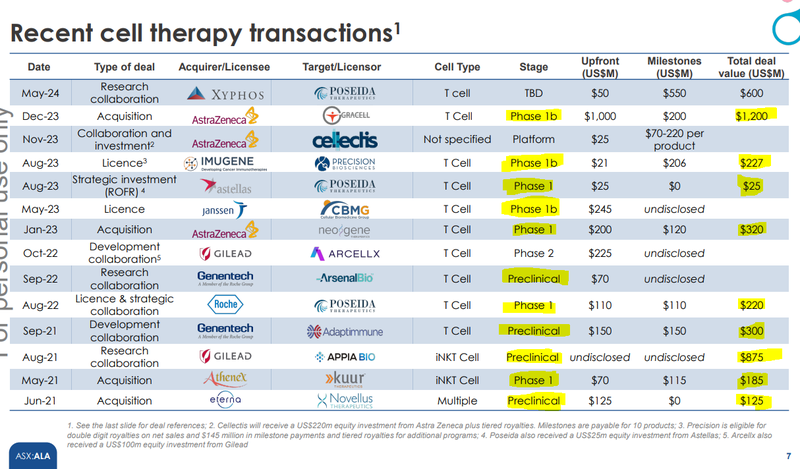

The right column in the chart below shows the deal sizes in US$M - so we are talking about multiple multi hundred million dollar deals and the odd billion dollar plus deal thrown in the mix.

(Source)

We see this week’s US$1.5BN deal as indicative of the continued intense interest that big pharma companies have in the cell therapy space.

... and we think there is a clear reason.

Beyond saving lives - the financial prize is very big.

The cancer therapeutics market is valued at ~US$200BN in 2024 and is set to grow rapidly.

One example of a cancer therapeutic is Merck’s Keytruda drug, which is a prescription immunotherapy drug that treats various types of cancers.

In 2023, this drug generated US$25BN in sales, making it the company's top-selling drug and one of the best-selling drugs in the world.

Keytruda's sales accounted for ~41.6% of the US$250BN Merck's revenue in 2023.

In 2028 the patent is set to expire and we expect there to be an “arms race” to find cell therapy platforms that can work like Keytruda to target and kill cancer.

We think the pressure to find the next cancer therapy blockbuster is part of why Roche paid US$1.5BN for this cancer cell therapy platform BEFORE the Phase 1 read out.

And it is also why we think that our Investment ALA is in a very strong position as it targets commencement of its Phase 1 trial in the first half of 2025.

OK, but how does it all work?

“Cell therapies” use genetically engineered cells to target and kill cancer cells, while minimising collateral damage to the other healthy cells in the body.

The most common form of cell therapy is “T cell therapy”, which is currently used today to treat patients with cancer.

The only problem is that this therapy needs to be made specifically for each cancer patient, rendering it expensive, insufficient and unreliable for scale.

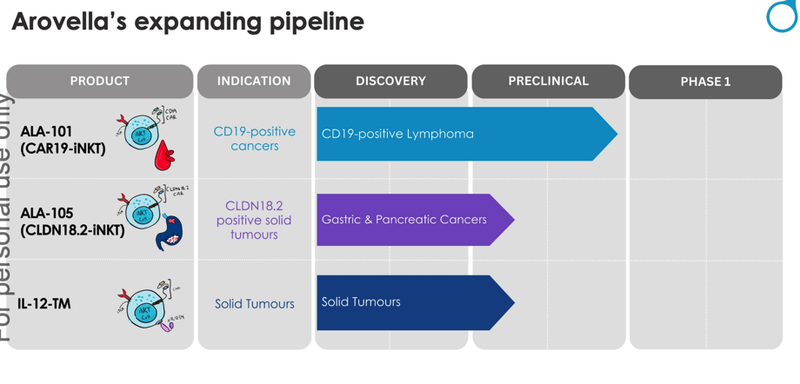

ALA aims to reduce these limitations of cell therapy by developing an ‘off-the-shelf’ solution. It has three programs:

- ALA-101 its invariant Natural Killer T (iNKT) Cell Therapy Platform, to kill blood cancers that produce the CD19 antigen

- ALA-105 (CLDN18.2) - another invariant Natural Killer T (iNKT) cell therapy targeting pancreatic cancer, gastric cancer, gastroesophageal junction cancers and potentially even lung cancer

- A preclinical solid tumour therapy that has been shown to kill solid tumour cancer cells in an in vivo (test tube) study.

ALA’s strategy is to develop into ‘off-the-shelf’ cell therapies that can treat thousands of patients with cancer, without the need for an individualised treatment.

Most of the money being poured into the cell therapy space (and there is a lot) is around fixing these two key problems:

- Individualised treatments and

- Targeting solid tumors (~90% of all cancers).

In time, ALA’s technology may be able to do both (noting that its solid tumour therapy is preclinical).

Perhaps that's why the ALA share price continues its steady upwards trajectory - from 3.8c when we first Invested, all the way up to circa 19c today.

At a $200M market cap, we think ALA continues to look undervalued compared to the billion dollar plus acquisitions being made in the space.

Of course this is speculative biotech investing, and anything can happen moving forward - past performance is not an indicator of future performance.

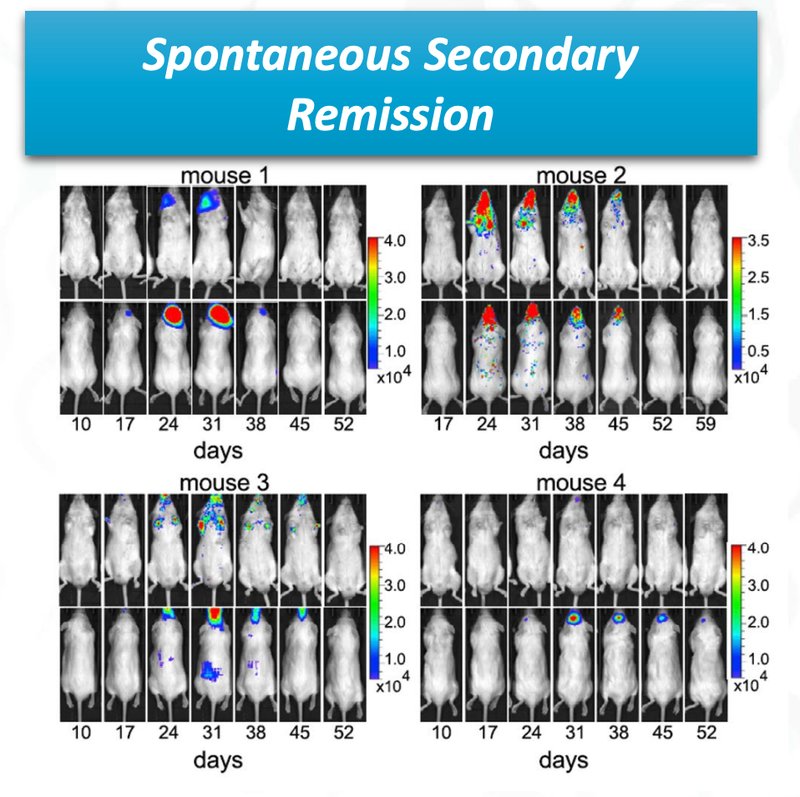

ALA’s early data looks promising

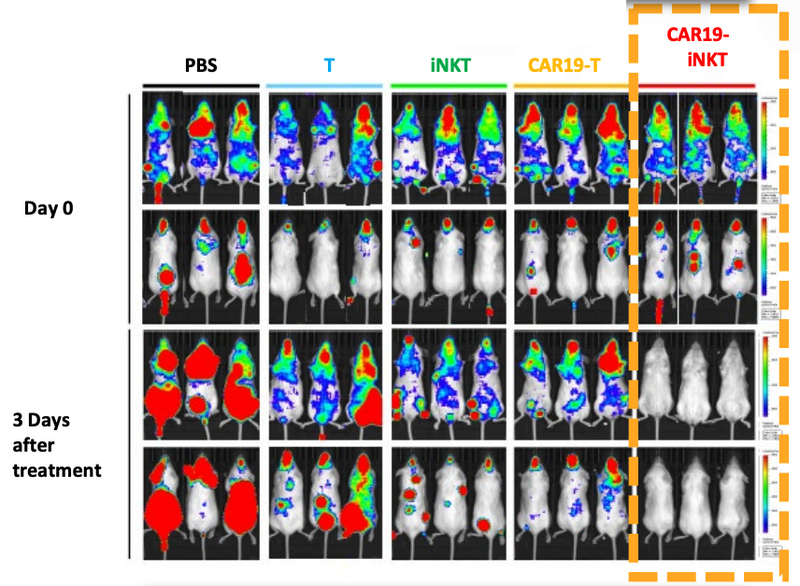

ALA has published some early data in mice that show its cell therapy completing removing cancer faster than current therapies:

ALA's preclinical mice trials showed spontaneous secondary remission - where cancer cells reappeared but were subsequently destroyed.

This phenomenon indicates that even if cancer returns after initial treatment, ALA's therapy demonstrates effectiveness in combating the secondary onset of cancer cells:

That’s a remarkable breakthrough - in mice.

However the proof will be in the pudding as ALA’s Phase 1 trial on humans approaches.

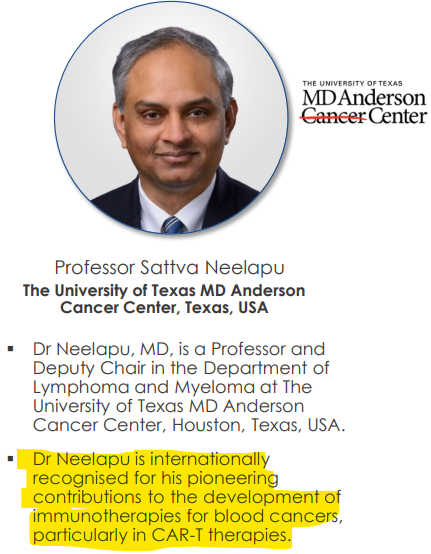

ALA has assembled an impressive clinical advisory board

As armchair biotech investors we tend to delegate to experts when it comes to evaluating the merits of a technology.

However, there is also a way to “externally validate” the technology based on who is involved in the company (and hopefully a validating deal from a big pharma company).

ALA recently appointed a clinical advisory board (CAB) with some serious heavy hitters on it.

This board will help ALA navigate the regulatory environment and advise on the clinical research program.

One of the clinical advisory board members really stood out to us though...

This is Professor Sattva Neelapu:

(Source)

Recently appointed to the ALA clinical advisory board, Professor Neelapu helped get a CAR-T therapy through the FDA approval process in his role at the prestigious MD Anderson Cancer Center.

Kite Pharma has been running trials at the MD Anderson Cancer Center on a CAR-T therapy called Yescarta (Kite Pharma was bought by Gilead Life Sciences for US$11.9BN in 2017).

(Yep, another multi-billion dollar acquisition in this space)

Yescarta got FDA approval in 2017 and is the most successful CAR-T therapy ever.

Sales from Yescarta delivered US$1.5BN in the full year 2023 for the US$114BN capped Gilead Life Sciences.

Yescarta is a CAR T-cell therapy for the treatment of large B-cell lymphoma (a blood cancer) where conventional treatment has failed.

So we’re pleased that from all of the different biotech companies chasing the key prize, Professor Sattva Neelapu has chosen to work with ALA as one of the best and most promising companies to get there.

(attaching his name and reputation to ALA and its technology)

Ultimately, we’re hoping Professor Sattva Neelapu’s expertise (along with the other highly qualified clinical advisory board members) can help ALA achieve our Big Bet:

Our ALA Big Bet

“ALA achieves a major breakthrough in cancer immunotherapy, and is acquired by a major pharmaceutical company for multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our ALA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

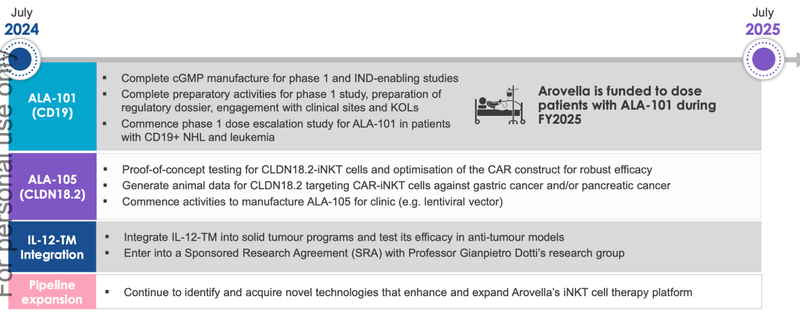

What’s next for ALA?

Check out this slide - but we agree it looks hard to read, so below the image we will cover off the key points.

🔲 Commence Phase 1 clinical trial for ALA-101

This is the big one.

ALA has confirmed that Phase 1 human trials will occur in the first half of next year.

ALA-101 is ALA’s most advanced treatment for blood cancers and ALA expects to complete its IND submissions with the FDA in Q1 2025.

These are the sub-milestones that ALA will likely need to achieve in anticipation of the Phase 1 clinical trial:

Milestones

✅ Complete process development and scale up - Completed this week

✅ Progressing to engineering and GMP batches to produce material for trial

🔲 IND application (expected Q1 2025)

🔲 Announce clinical trial plan

🔲 Secure ethics approval

🔲 Commence clinical trial and dose first patient

Risks

Early Stage Biotech Risk

As with many early stage biotechs, a lot can go wrong in developing technology. As ALA moves towards the clinical trial phase these risks will be more pronounced:

- The treatment is ineffective

- The treatment is not considered safe for human use

- Patient recruitment is delayed

- Ethics approval is delayed

Market risk

The market could sell off, or biotechs could sell off as a sector, impacting ALA’s share price regardless of its operational performance.

The market risks for ALA are linked directly to funding risk as capital markets for biotechs remain constrained.

Our ALA Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our ALA Investment Memo you can find the following:

- What does ALA do?

- The macro theme for ALA

- Our ALA Big Bet

- What we want to see ALA achieve

- Why we are Invested in ALA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.