Why the US needs Uranium Enrichment

Published 20-FEB-2023 08:45 A.M.

|

15 minute read

We are announcing a new Investment on Monday morning.

One of our key Investment themes for 2023 is critical materials in the USA - specifically for energy and resource independence in a rapidly de-globalising world.

Our latest Investment is in uranium enrichment technology combined with JORC-stage USA based uranium assets.

Uranium “enrichment” is basically applying an advanced process to raw uranium (that is mined out of the ground) to enhance the concentration of its key element enough to be used as the fuel in nuclear reactors.

Uranium enrichment technologies and processes are closely guarded secrets.

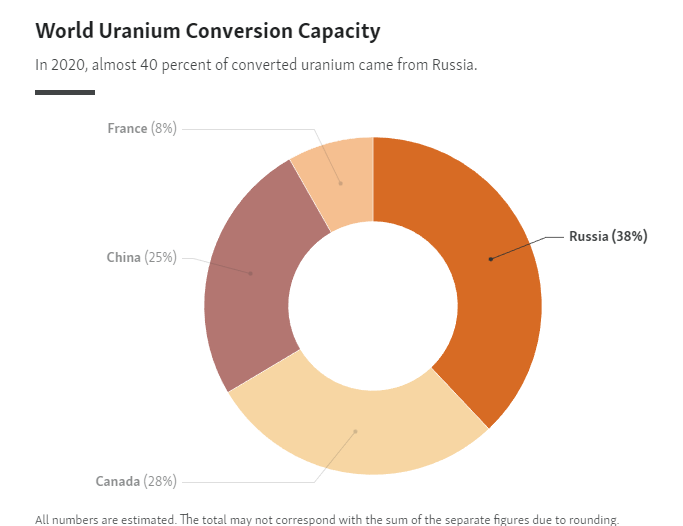

Russia controls ~38% of the world’s enrichment capacity. China controls ~25%.

According to Reuters: U.S. uranium enrichment capability has dwindled to nothing in recent decades as it leaned on other countries to supply the fuel.

The US is most vulnerable to supply chain shocks in the uranium industry because it has the world's largest nuclear reactor fleet - nuclear power accounts for ~20% of electricity production in the US.

In the last 72 hours the US has introduced the Nuclear Fuel Security Act (NFSA). This Act aims to establish domestic nuclear fuel production to protect against a disruption of Russian supplied “enriched” uranium.

At almost the same time, a US bill (H.R.1042) was proposed to ban imports of enriched uranium from Russia.

The new Investment we are announcing on Monday has just acquired a material stake in a rare uranium enrichment technology and has JORC stage uranium assets located in the USA.

This also fits with another of our 2023 Investment themes: adding exposure to more later stage companies to our Portfolio, which can begin production sooner in the current commodities supercycle.

This company aims to capitalise on more than $2 trillion in macroeconomic tailwinds.

That $2 trillion comes in the form of US government initiatives as the country launches an all-out push to re-shore its supply chains amid an energy transition, a war and other geopolitical friction.

In our view this company is perfectly placed to capitalise on these tailwinds ...IF it can successfully execute on its plan (as always there are risks that we will outline when we share our Investment Memo).

Our new Investment will be announced on Monday, including our initial Investment Memo on why we Invested, what are the key objectives we want the company to achieve in the next 12 months, what are the risks, and our Investment plan.

North American Critical Minerals - Macro theme

When we released our outlook for the year ahead, we realised that the North American critical minerals macro theme was one we needed more exposure to.

This macro theme has been a few years in the making.

The 2020 COVID pandemic, followed by the Russia/Ukraine war has changed the way world trade is conducted.

Especially after multiple instances of countries withholding access to critical resources or technology as a geo-political weapon.

In the US, decades of globalisation have led to the hollowing out of the country’s manufacturing/commodities complex and exposed shortages of critical raw materials/supplies.

Aside from the gap in the USA’s uranium supply and enrichment capability, ~80% of the world's lithium hydroxide processing capacity is controlled by China along with 63% of rare earths production (+85% of rare earths processing).

Recognising this, the US has signed into law policies to spend ~US$2 trillion over the next 10 years to build up a domestic, secure supply of the critical raw materials and processing capabilities needed for industries like Electric Vehicle (EV) batteries, solar and wind power, nuclear energy and manufacturing of semi-conductors.

- Inflation Reduction Act (IRA): ~US$400 billion over the next 10 years towards clean energy technologies and supply chains INSIDE the US.

- Bipartisan Infrastructure Law (BIL): US$1.2 trillion over the next 10 years on US based infrastructure.

- CHIPS & Science Act: ~US$280 billion over the next 10 years on domestic semiconductor manufacturing, R&D and wireless supply chains.

We saw the first signs of this huge shift when the US started announcing loans and grants to ASX-listed critical minerals companies.

Here are a few examples of that (proposed or executed agreements):

- Syrah Resources - $350M in grants to expand its natural graphite facility in Vidalia, Louisiana (source)

- Novonix - $240M for its new plant in Chattanooga, Tennessee, targeting production of 30,000 tonnes of synthetic graphite (source)

- Ioneer - $700M conditional loan commitment for Rhyolite Ridge Lithium-Boron Project (source)

- Lynas - $173M to build a rare earths refinery in the southern states of the US (source)

The natural extension of the US funding of ASX-listed critical minerals companies is for the US to start looking closer to home.

It’s clear...

The US with its partners (like resource rich Canada and Australia) are hell bent on securing critical minerals.

Call it de-globalisation, reshoring, resource nationalism - but one thing is clear:

The US wants it to happen ASAP.

As a result, it's “go time” for North American based critical minerals projects, and we’ve been closely tracking companies that can give us the right exposure to this macro theme.

There’s a common thread here too - and that’s energy.

But that energy needs to be clean, which brings us to one critical mineral which lies at the centre of the US energy conundrum right now.

We’re talking about uranium - the fuel for nuclear reactors.

How critical is uranium for the USA and North America?

Uranium is arguably one of the most at risk commodities in the energy supply chain given the current high friction East v West geopolitical environment.

In the fallout of the Russia/Ukraine conflict the US, Europe and other western countries all introduced sanctions targeting Russia’s energy industry (oil, gas, goal etc).

One sector that wasn't at all sanctioned was the uranium sector.

Until this week, the uranium industry has flown under the radar of sanctions.

This isn’t because the US forgot about it or because it isn't important to anyone... rather, it’s because there is just no alternative to replace the supply of enriched uranium that comes out of Russia and China.

And as for the supply of raw uranium, most of the world's direct (mined) supply doesn't actually come out of Russia, making it only a second order target of sanctions.

Targeted first were things like oil and gas produced in Russia and sold to the world. The uranium market works a bit differently.

Russia doesn't directly control uranium mine supply, instead it controls the more opaque (but significantly more important) uranium enrichment industry.

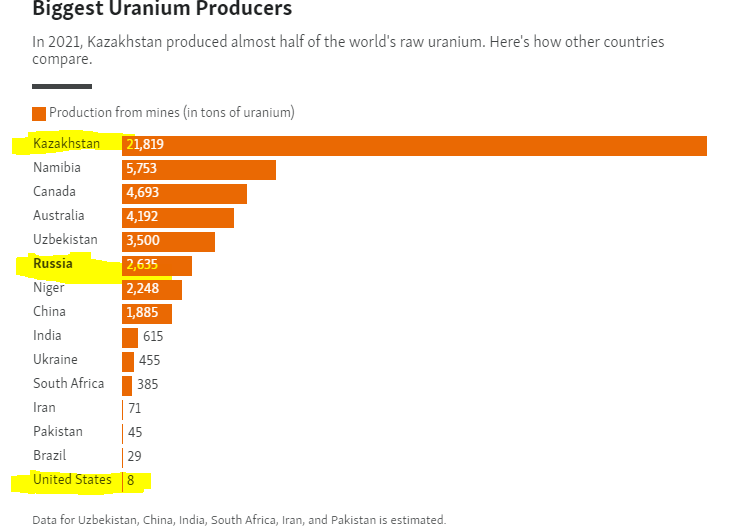

As of 2021 Kazakhstan produced over 50% of the world's raw uranium supply. The US, on the other hand, produces barely any.

Mined uranium on its own is not useful as a fuel for nuclear reactors.

Once mined, it needs to be “enriched” before it can be used in nuclear power stations

This is where the Russia/China dominance comes into play.

Together the two countries control ~63% of global enrichment capacity.

As is the case for mined uranium production, again the US has almost no domestic enrichment capacity.

The answer to why sanctions were never placed on the uranium supply chain is relatively simple: the US and the West simply can't replace the enriched uranium supply coming out of Russia and China.

Again, the US is most vulnerable to uranium industry supply chain shocks because it has the world's largest nuclear reactor fleet - nuclear power accounts for ~20% of electricity production in the US.

Turning off its key supply routes via sanctions would be like shooting its domestic nuclear power industry in the foot.

Yet this week, the US took the first steps towards doing just that...

US senators Joe Manchin and John Barrasso (both from the senate energy and natural resources committee) this week introduced the Nuclear Fuel Security Act (NFSA).

The bill’s ultimate purpose being, “To establish a nuclear fuel program with the purpose of onshoring nuclear fuel production to ensure a disruption in Russian uranium supply would not impact the development of advanced reactors or the operation of the United States’ light-water reactor fleet”.

Senator Manchin’s comment is enough to tell the story, “American energy security and independence is impossible when we continue to rely on Russia and Vladimir Putin for the uranium we need to power our nuclear reactors”.

The CEO of $2.1BN US-based developer Uranium Energy Corporation, which holds projects next door to our earlier stage US-based uranium exploration Investment, GTI Energy (ASX: GTR), jumped on the news with the following tweet.

Here we go.

— Amir Adnani (@AmirAdnani) February 15, 2023

House Energy & Commerce Committee bill has been introduced (HR-1042) to immediately ban Russian low-enriched #uranium into the U.S. 🇺🇸

👉 https://t.co/pk6JHPWN0a pic.twitter.com/pPU3bSlQfd

With this, we think the macro environment for uranium is approaching an inflection point where the momentum, especially inside the US/North America, starts to increase exponentially.

There remains significant US domestic demand from its existing mature nuclear power fleet. And now, the introduction of the Inflation Reduction Act brings ~US$400BN in government incentives into law to develop domestic clean energy supply chains.

Of note, US$700M of that funding is being specifically directed to the enrichment space.

As a result, we think that one of the best places to Invest in the uranium sector is in the US/North America.

We have been looking at new Investment opportunities in this uranium space for a while now but it was only yesterday that we finalised an Investment in a company that fits the bill - specifically around its part ownership of uranium enrichment technology.

Our new Investment in uranium enrichment and USA based uranium assets will be announced on Monday morning. It will include our Investment Memo on why we Invested, what are the key objectives we want the company to achieve in the next 12 months, what are the risks, and our Investment plan.

Speaking of North American critical metals...

We are bullish on the US based critical metals thematic this year.

Last week we added a new Investment in an early stage explorer that’s chasing two of our favourite commodities — lithium (Canada) and rare earths (USA).

That Investment was Megado Minerals (ASX:MEG).

MEG has just acquired a lithium project in the same region of Canada as lithium market darling, the ~$1.7BN Patriot Battery Metals.

On announcement of the acquisition the MEG share price popped as high as 120% before finishing the day up around 35%.

The vendor of the MEG assets also vended part of the Patriot assets into that company - part of the Corvette discovery, which led it from a $553M IPO in December 2022 to its current market cap of ~$1.7BN.

MEG’s on the ground exploration in Canada will be conducted by a related entity of the vendors - these folks were intimately involved in Patriot’s discovery, pre and post its IPO.

Post transaction, the vendors will hold ~ 18% of MEG shares, and the related entity will be conducting 3 years of exploration work for MEG.

So MEG is not just getting a prime piece of real estate it’s also got an on the ground exploration team incentivised for success.

MEG has picked up a 130 km2 contiguous package of claims in the James Bay region of Canada.

This region is a fast emerging lithium hot spot, with not only Patriot but the $318M capped Winsome Resources also successfully making a lithium discovery.

While MEG isn’t expecting to drill in the James Bay until the end of 2023, we expect that the success of Patriot could generate some buzz and interest in MEG’s drilling campaign in the lead up to that program.

MEG’s ground is in the underexplored Aquilon Greenstone Belt. Greenstones are the type of rocks that are known to host valuable mineralisation — the same kind of rocks that delivered Patriot’s lithium discovery.

So MEG is in the same region as Patriot, and has ground with similar geology and a similar structural setting, which is favourable for lithium discoveries.

The ingredients are there, but we won't know how much MEG’s ground is worth until it gets out there and starts drilling, and that is a little while off yet.

It’s very early days here.

Again, we are unlikely to see drilling here until later in 2023, but with a $14.4M market cap (post share issue, at 5.8c) we like the upside MEG presents.

MEG has just received commitments for a $2.7M capital raise at $0.045 which we participated in. However, settlement won't be until late March — likely around the time the acquisition will be completed.

Of course, this is a micro cap stock so comes with significant risks.

There is an extremely low chance that MEG ever reaches a similar market cap to that of Patriot (~$1.7BN).

BUT we are Invested just in case it does... even a fraction of Patriot’s return on a successful lithium hit would be a great result for MEG from current levels.

Our Investment thesis also includes the significant attention on Patriot driving investor interest to MEG’s maiden drilling campaign.

Click here to read our MEG Investment Memo

Macro News - what we are reading

Lithium:

- Ford Plans to Build EV Battery Plant in Michigan With Chinese Partner

- Africa gears up to keep more of the profits from lithium boom

- Tesla Announces Date for 2023 Investor Day

- Tesla Is Considering a Bid for Battery Metals Miner

Battery Materials:

Oil and Gas:

- US to Sell 26 Million More Barrels From Strategic Oil Reserve

- What Big Oil’s bumper profits mean for the energy transition

- Is Russia weaponizing oil after natural gas misfire?

Rare earths:

US based commodities:

- The US plan to become the world’s cleantech superpower

- Debelle bemoans distortion created by Biden’s $US1trn green bill

Uranium

- U.S. ramps up advanced fuel production capabilities

- Carter, Peters reintroduce bill to strengthen U.S. nuclear energy

This week’s Quick Takes 🗣️

AKN: Exploration poised to commence at advanced U project

DXB: DXB secures non-dilutive funding ahead of key catalyst

GTR: GTR targeting maiden resource, geophysics in Wyoming

LCL: Trenching confirms gold discovery in PNG

LCL: New Cu-Au target in PNG district hosting multi-million-oz mines

LRS: 7 Diamond drill rigs on site, 3 more rigs on the way

PUR: Lithium brine in South America's lithium triangle - update

TTM: Promising gold intercepts at Meseta

This week in our Portfolios 🧬 🦉 🏹

🏹 ⚠️ New Investment: Megado Minerals (ASX:MEG) ⚠️

This week we added a new Portfolio Investment — Megado Minerals (ASX: MEG).

MEG is an early stage explorer that’s chasing two of our favourite commodities — lithium and rare earths.

The company just acquired a lithium project in the James Bay region of Canada, a 130 km2 contiguous package of claims in the same region as lithium market darling, the ~$1.7BN Patriot Battery Metals.

MEG’s on the ground exploration will be conducted by a party that was intimately involved in Patriot’s discovery, pre and post its IPO.

We are unlikely to see drilling here until later in 2023, but with a $11.2M market cap we like the upside MEG presents.

📰 Read our full Note: New Investment: Lithium in Canada with a side of US Rare Earths

🏹 Lanthanein Resources (ASX: LNR)

Our Investment Lanthanein Resources (ASX: LNR) confirmed a forward plan for drilling two types of targets at its WA rare earths project over the coming months.

Located in the Gascoyne region of WA, LNR is in the right neighbourhood for a rare earths discovery. It has ground right next door to the $400M capped Hastings Technology Metals, and the $310M capped Dreadnought Resources is also nearby.

LNR’s drill program will be targeting the same host rocks as its two larger capped regional neighbours:

- Outcropping shallow ironstones and

- A deeper carbonatite structure.

After a recent capital raise LNR has about $6.2M in the bank. It will use this to deliver 10,000m of RC/diamond drilling over the coming months, with the hope of delivering a new rare earths discovery.📰 Read our full Note: LNR is targeting a new rare earths discovery

⏲️ Upcoming potential share price catalysts

Updates this week:

- GAL: Is undertaking a second round of drilling at its Callisto PGE discovery in WA.

- This week GAL presented at the RIU explorers conference. To see that presentation click here.

- 88E: Drilling for oil in the North Slope of Alaska next to UK listed Pantheon Resources.

- 88E released a video detailing the upcoming Hickory-1 well. Check it out here.

- PRL: Awaiting final execution of a joint development agreement with Total Eren.

- On Friday morning PRL went into a trading halt pending “a material update in relation to the Binding Term Sheet entered into with Total Eren”. We have been waiting a long time for an update on this deal and look forward to providing our opinion when it is released.

No material news this week:

- EV1: Updated DFS looking to improve on the already relatively strong US$323M NPV; Framework Agreement with the Government of Tanzania.

- GGE: Preparing to drill its US helium project looking for a commercially viable flow rate.

- KNI: Drilling the first of its three Norwegian battery metals projects inside the EU.

- TMR: Maiden JORC resource estimate for its Canadian gold project.

- TYX: Assay results from the company’s maiden drill program.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.