How do Fund Managers Invest in Small Cap Stocks?

Published 14-JAN-2022 09:54 A.M.

|

17 minute read

We hold long term positions in small cap companies with top management teams, in macro themes we think will do well in the future.

Our investments are generally early stage companies that are under ~$25M market cap.

We maintain a diversified portfolio of over 20 positions (currently ~40 across all portfolios) in the hope that 2 or 3 will achieve an outsized return and outweigh the companies that may fail.

We hold these positions over 3 to 5 years while the company executes its plans. We try to take some profit as the share price (hopefully) re-rates along the way.

We are seeking 1,000% gains over the long term.

In our own experience, the best place to achieve 1,000% returns is by investing in higher risk, early stage companies and holding a position as they try to achieve their objectives over time to increase “certainty” around their business. There will be some failures along the way however - that’s part of the risk at this end of the market.

As a company (hopefully) progresses through its development stages, the following will occur over time:

- Increased certainty leads to investors with a lower risk profile to enter and hold

- More people learn about the company and the daily trading volumes increase

- The share price sustainably re-rates upwards and the market cap of the company increases.

...and a $25M company (hopefully) becomes a $100M+ company.

Lowered investment risk, increased market cap and higher trading volumes are very important progress points for an early stage company, because it means that professional fund managers and institutional investors are then “allowed” to invest.

Holding an early stage investment as it successfully executes its plan and becomes “investable” by professional fund managers is one of our key objectives as early stage investors.

It means that our investment can attract larger pools of capital from professional fund managers, who are usually very long term holders, and having them on the cap table underpins the new higher market cap (and share price).

These fund managers invest because they want to hold a position while the company executes more objectives and further de-risks - going from say $100M to $500M market cap, where they can THEN attract capital from even bigger, later stage professional fund managers.

So why can’t professional fund managers invest in the early stage companies that we invest in?

As we mentioned above these fund managers often rely on a company being “more established” which generally translates into companies with higher market caps versus the stocks we consider to be micro caps.

This naturally means these fund managers are sidelined in our investment universe and are simply not able to make investments for a variety of reasons:

We believe these 3 key reasons are:

- Liquidity - Related mostly to trading volumes in a particular company.

- Benchmarking - Related mostly to measuring the funds performance.

- Position-sizing - Related mostly to the size of a company’s market cap.

1 Fund managers need liquidity

These professional fund managers often have their funds open for “redemptions” - meaning, if investors in the fund want to take out their capital at any time they can simply apply for it, and the fund managers need to free up enough cash to pay back that investors' redemption.

When we invest in a micro cap stock ahead of the market becoming interested in it, there is usually low trading volumes and little publicity online.

The lack of trading volumes and publicity means these stocks are un-investable for these funds - let's run through a hypothetical redemption scenario to try and understand why.

Let's say one of these funds has managed to take a $500k position in a micro cap stock that has a $5M market cap, their shareholding makes up 10% of the company’s shares on issue.

Now let's say that 3 or 4 of the investors in that fund have gone off and purchased a new home. They are now approaching settlement and ask the fund manager to send back their cash (referred to as a “redemption”).

Nothing has changed in markets or with the company that the fund invested in BUT the circumstances of the investors in the fund have.

These fund managers are now in a position where they have become “forced sellers”. They need to liquidate some of the funds positions to make sure they can pay back the investors who want to redeem their funds.

That fund manager now logs into their brokerage account and realises they need to sell some of that $500k investment but have quickly realised that the market is still yet to catch onto the potential of the company.

They have now become forced sellers of 10% of the company’s shares on issue at a time when there are little or no buy bids.

This level of selling pressure can kill a company’s share price and may mean that the $500k position is sold at a deep discount - crystallising losses in an investment that the fund manager may still believe will be a good investment in the long run.

Professional fund managers can’t afford to take on small, illiquid investments and need to have certainty about their ability to exit a stock.

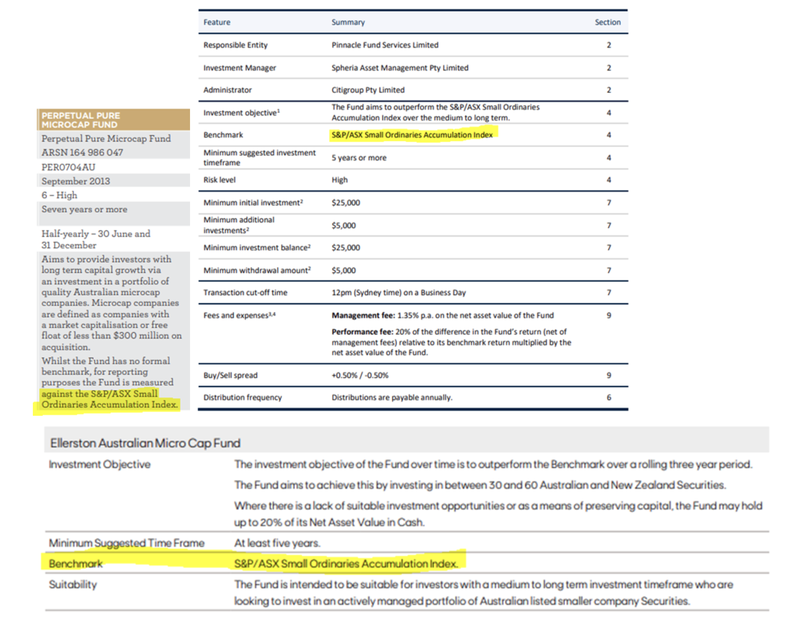

Below is an excerpt from Perpetual’s PDS (Product Disclosure Statement) which shows they are required to invest only in companies with higher market caps & more trading volumes:

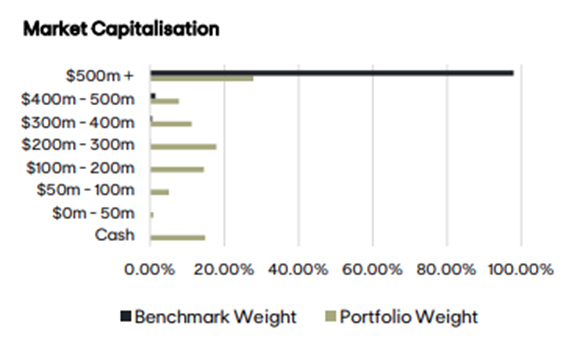

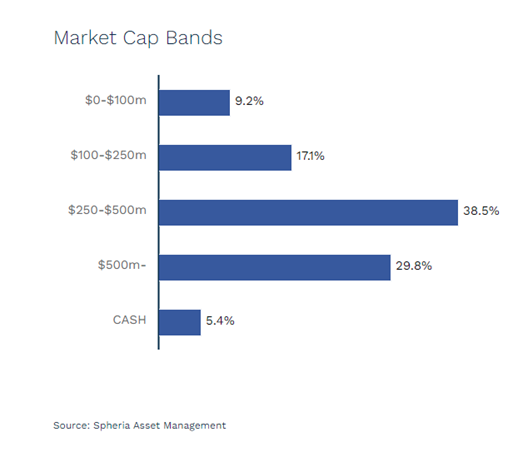

Below you can also see the bulk of other “Micro Cap fund” holdings are in companies with market caps well above the $100M mark:

2 Fund managers need to perform relative to a benchmark

Professional fund managers live and die by their performance relative to a certain benchmark.

If they underperform, investors will pull capital and if they over-perform they attract more capital. This generally leads to fund managers tracking the composition of these benchmarks closely as opposed to building a portfolio from scratch.

Most of the funds that are marketed as exposures to “Micro-caps” will be benchmarked against the ASX Small cap all ordinaries index (ASX: XSO). Reading through the eligibility criteria for this index, it’s pretty clear that only stocks above a certain market cap with trading volumes that are considered “Institutionally investable” are targeted by these funds.

This means the professionals will generally tend to favour more established companies that are either already profitable, revenue generating or simply-put have a much larger market cap.

This leaves a large part of the micro cap universe (<$100M market caps) as uninvestable to these fund managers. This is where the opportunity lies for early-stage investors like us.

Naturally we are trying to look for the company that these same professional fund managers one day will be looking to buy at much higher share prices - when the company has progressed through the stages of a company’s lifecycle and have become “institutionally investable”.

Below are images in some of these funds' PDS showing the funds benchmark.

3 Fund Managers need to take bigger positions

This brings us to the last of the reasons - position sizing.

Often these professional fund managers are investing upwards of $50M, across a portfolio of stocks. This will inevitably lead these funds to shun any company that is considered “too small” simply because they can't take a big enough position without seriously moving the price of the company or there just isn’t enough shares for sale.

Let's run through another hypothetical scenario:

If a fund with $50M in funds under management wanted to invest 5% of their fund in a particular stock this would make for a $2.5M investment.

Now let’s say that investment is a junior exploration company that is capped at $10M, and the fund is trying to build a position that makes up 25% of that particular company’s market cap.

This type of investment simply isn't possible without moving the share price of that junior explorer by say +50-100% because the buying pressure outweighs the amount of shares for sale.

These type situations no matter how tempting are almost never executed at the fund-level, mostly because of the two other key reasons we mentioned above “Liquidity” & “Benchmarking”.

Fund managers just have to wait until this exploration company delivers some good results and achieves a market cap and liquidity that moves it into “investable” grade. Often this means buying it at a share price well above where we would have been making our investment.

In essence these professionals are limited by the sheer size of the funds they manage, they are not able to take positions in early stage, high-risk high-reward companies with market caps below a certain $ figure.

So what does this mean for early stage investors like us?

Now bringing this all together, there are obvious advantages to allocating capital to a professional fund manager - they charge a small fee and do all of the work.

For the reasons we discussed above, the limitation with this style of investing for us has been that they can't invest in the company’s we consider true micro cap stocks - with market caps <$50-100m.

This is where we think we have our edge, with professionals limited by their investment mandates and not being allowed to invest in the companies we look at...

We think by doing our research and investing ahead of the markets we can back the companies that one day these professionals can invest in at much higher prices

Naturally this means that the ultimate aim for early stage investors like ourselves is to invest in companies with high quality future prospects and hope that they can grow into stocks that these professional fund managers are able to invest in, to take them through their next stage of growth.

We maintain a diversified portfolio because early stage investing is high risk with a lot of uncertainty around execution.

Most small companies we invest in will fail to achieve enough of their objectives to progress to a stage that becomes investable by professional fund managers, but for the few that do we expect to deliver significant returns.

We spend our days trying to identify early stage companies that we think have the highest chance to deliver their business plan, and move to a stage that can attract institutional capital.

We aim to hold a position along this journey from $25M market cap to $100M, then to $500M and hopefully beyond, with the company collecting progressively bigger institutional funds along the way.

📰 This week on Next Investors

On Thursday our Our 2021 Tech Pick of the Year Oneview Healthcare (ASX:ONE) delivered a milestone quarterly report showing an impressive €5.46M ($8.6M) in cash receipts, up 280% on the prior quarter and up 101% vs the previous corresponding period - its first ever cash flow positive quarter.

In our coverage of the $20m capital raise in November last year, we said ONE was perfectly positioned to aggressively pursue a “land grab” growth strategy which basically means ONE invest heavily in user-growth, the positive cashflow will mean ONE can now be even more aggressive with this strategy.

Importantly the quarterly highlighted that they managed to deliver the first 749 WeTek hybrid set-top boxes. These coax boxes act as a gateway for ONE to be able to sell the higher-margin SaaS solution to older hospital wings that previously could not implement ONE.

📰 Read the full take here: ONE delivers record quarter and unlocks legacy hospital sales.

🗣️ Quick takes on key portfolio company events this week:

Invictus Energy (ASX:IVZ)

On Wednesday IVZ announced that applications for shares in the Share Purchase Plan (SPP) exceeded the targeted $2m on the first day of the SPP. We applied for our full entitlement and aren't surprised other shareholders are doing the same thing.

In response to the massive amount of demand for stock IVZ have increased the capital raise amount to $3m.

The SPP is being done on the same terms as the $3.5m placement that was completed on the 29th of December. The shares are being offered @10c and come with a 1 free option for every 2 shares subscribed for, exercisable @14c with a 3-year expiry.

With the shares being offered at a 20% discount to the SPP and the options already almost in the money, we expect applications by shareholders will exceed $3m by a significant amount.

A few readers have asked, and yes - we have applied for the maximum allocation in this capital raise, across both entities in which we hold IVZ positions.

IVZ was our 2020 Energy Pick of the Year and we are very excited that IVZ is finally drilling its basin opening well in the next few months.

Next: We want to see detailed results and final interpretations from the 2D Seismic data acquired, and the finalising of the SPP.

Tempus Resources (ASX:TMR)

This week TMR announced that it has commenced the 2nd phase of exploration at its gold project in Ecuador.

The phase 2 program is a larger scale follow-up to the initial reconnaissance work conducted during February 2021 and will largely be made up of geochemical sampling work over the areas that were covered by airborne surveys in Feb-2021.

With Canada in the middle of winter and drilling stopped at its gold project over there, this is welcomed news for us.

Next: We want to see the results from the exploration program in Ecuador whilst we wait for the Canadian Winter to pass and the next Canadian drilling season commences.

Vulcan Energy Resources (ASX:VUL)

On Tuesday VUL announced that it has signed an MOU and a term sheet with Nobian, a European leader in the production of essential chemicals with revenues in 2020 of €1 billion to assess the feasibility of a joint-venture for the development, construction and operation of the central lithium plant (CLP). .

In our 2022 investment memo for VUL we said that we wanted to see more strategic partnerships signed in the new year. For an MOU of this calibre to be executed this early in the year is a testament to the management team at VUL doing what they say they will.

The joint-development project is split into 3 different stages which ends with project investment negotiations with Nobian following the conclusion of the Definitive Feasibility Study (DFS). The stages are as follows:

- Phase 1: Joint DFS for the development, construction and operation of the central lithium plant (CLP).

- Phase 2: Operation of VUL’s electrolysis Demonstration Plant at Nobian’s existing site in Frankfurt.

- Phase 3: Parallel to phase 2, design/engineering, construction, start-up and joint operation of the CLP at commercial scale. Vulcan and Nobian will also discuss chlorine and hydrogen offtakes , which are planned by-products of Vulcan’s CLP.

Another great partnership secured by the VUL team.

Next: We want to see VUL’s demonstration plant operating, the DFS complete, and a Vulcan listing on the main German bourse.

Pursuit Minerals (ASX:PUR)

PUR started this week by announcing that it had completed some sampling and reconnaissance works identifying three ultramafic units at its PGE-Nickel-Copper-Gold project. It is still relatively early days with this project with all of these works being performed as part of overall drill target generation works.

Later in the week PUR also put out its exploration plan for the March quarter 2022. The exploration plan shows us that a lot of this quarter will be made up of geochemical and geophysics works leading to drilling programs in Mid-2022.

Overall a relatively quiet Q1 for PUR but it will be interesting to see what comes of all this target generation work.

Next: We want to see follow up auger geochemistry at the Phil’s Hill prospect to help form the basis for the next batch of drill-targets at the Warrior project.

Dimirix (ASX:DXB)

This week DXB announced that it had dosed the first patients in India for its Phase III study of respiratory complications associated with COVID-19.

As the affects of Omicron are run rampant through Australia, disrupting key supply chains and school openings, the importance of a treatment that can work across all COVID variants is becoming more and more important.

With ethics approved in both Australia and India, DXB is undertaking patient recruitment and analysis for its Phase III clinical trial.

Last week Indian health officials flagged ‘safety concerns’ over Merek’s antiviral COVID-19 treatment. In comparison, DXB’s solution is anti-inflammatory, with a very strong safety profile.

If DXB’s treatment is effective (which will only be confirmed through a rigorous Phase III clinical trial of roughly 600 patients), DXB will be well placed to commercialise its technology and help alleviate the stress of the COVID-19 pandemic.

Next: Each of DXB’s phase-III clinical trials have begun (two for COVID-19 and one for FSGS). We want to see patient recruitment updates on each of these trials and hopefully some positive results from the COVID-19 studies before the end of the financial year.

Creso Pharma (ASX:CPH)

On Tuesday CPH announced that they had been invited to register as a potential supplier to Health Canada’s Special Access Program for CPH to supply psylocibin to healthcare professionals seeking evolutionary treatments for patients through the SAP (Special Access Program).

This is welcomed news after the bad-press CPH received at the back-end of 2021 but there is still a lot of work to be done before anything comes of this, especially considering it is only an invitation and nothing more.

Next: Similar to what we said in previous weekend updates, we want to see a more coherent governance structure & a high end CEO appointment at CPH.

In our other portfolios 🧬 🦉 🏹

🦉 Wise-Owl

FYI Resources (ASX:FYI)

On Monday our battery metals investment FYI put out an update on the high purity alumina (HPA) pilot plant operations with the average HPA purity achieved for the 2nd week samples returning 99.9978% Alumina.

The pilot plant operations are being run together with FYI’s US listed partner Alcoa (Capped at over $10bn) with the ultimate aim of forming the basis for the commercialisation of FYI’s innovative process for refining high quality HPA.

With a third-run planned for the week starting on the 17th of this month we expect to see further refinement of the processing flowsheet and will be watching to see the results from next week's trials.

🏹 Catalyst Hunter

Techgen Metals (ASX:TG1)

Early in the week TG1 announced the acquisition of two new projects in two of the most talked about exploration regions in Australia right now.

The first project covers ~262km^2 in grounds and sits on the western edge of the Yilgarn province where Chalice mining recently made the massive Nickel-Copper-PGE Juilmar discovery. The second project is located in the Earaheedy basin covering a massive ~911km^2 in grounds near the Rumble Resources Chinook discovery.

Both projects are mostly made up of exploration license applications so it will be quite a while before any serious drilling work is done over them, nevertheless we think that they are good additions to the portfolio of assets TG1 holds.

The primary reason for our investment in TG1 was because it was giving us an exposure to grounds in tier-1 locations with a really cheap entry price. With a tiny EV of ~$3.8M TG1 and these new acquisitions added to the portfolio this thesis has just been strengthened significantly.

Next: We are watching to see the results from the drilling TG1 did at its copper project in the Ashburton basin.

🌎 Mainstream Media:

Hydrogen (PRL)

Bloomberg Green: How Hydrogen Could Solve the Energy Crisis (Bloomberg)

Healthcare (ONE, DXB)

‘A game of Russian roulette’: Victoria’s Alfred hospital expects 15% staff absent at Covid peak (The Guardian)

India Medical Agency Flags ‘Major’ Worries Over Merck Covid Drug (Bloomberg)

Lithium (VUL)

‘Tell ’em they’re dreaming’: Liontown CEO weighs in on lithium supply (AFR)

Supply Squeeze Risks Are Pushing Lithium Higher and Higher (Bloomberg)

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.