Upcoming Price Catalyst: EXR flow test in April.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,622,858 EXR shares and 1,071,429 EXR Options at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time.

Elixir Energy (ASX:EXR) just upgraded its prospective resource by ~3X to 3.6 trillion cubic feet.

And in April EXR will be flow testing it...

The flow test is when we will find out if EXR can produce commercial flow rates of gas.

The flow test is a material catalyst - it will either re-rate EXR’s share price up or down - depending on how much gas flows out of its well...

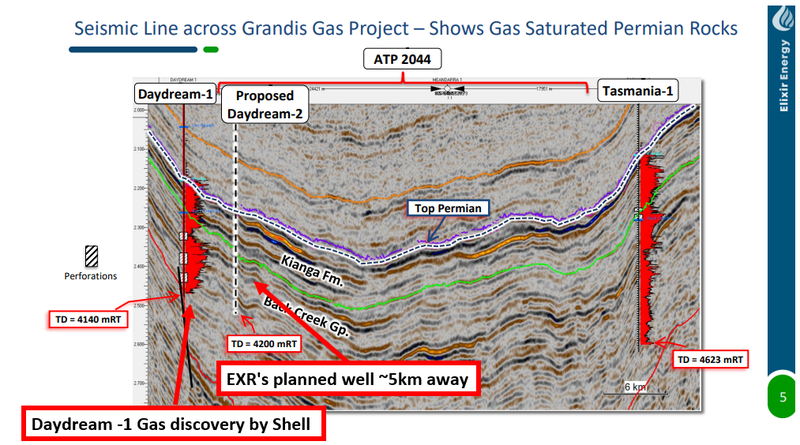

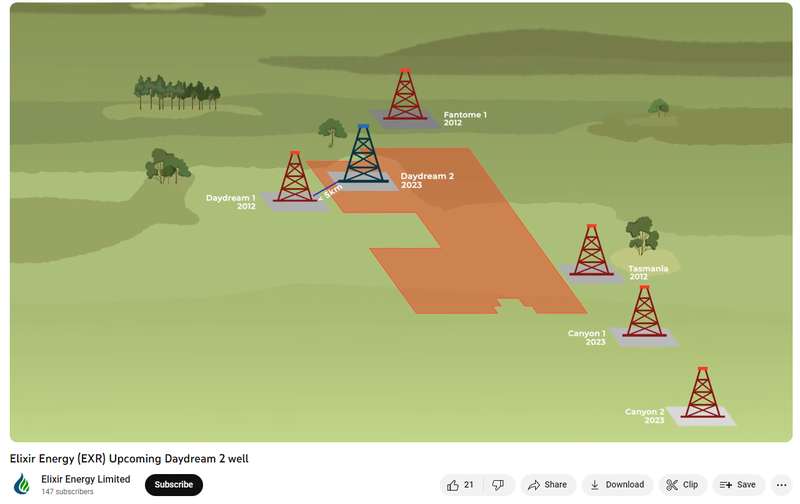

Two months ago EXR drilled its Daydream-2 well at its Queensland gas project.

EXR’s drill was an “appraisal” well, meaning the company was drilling a known gas discovery.

The main objective was to confirm already known data and prepare the well for a flow test BUT...

EXR hit everything it expected and more...

Here is what happened:

- Expected News: EXR hit unconventional tight gas structure with net pay of ~154m across these zones.

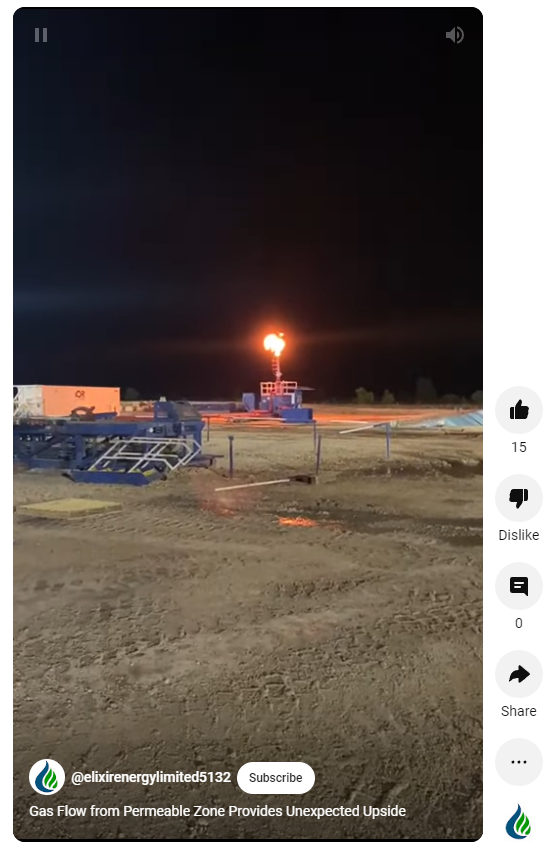

- Unexpected News: EXR hit a conventional section at the end of its well flowing free gas to surface. Field estimates were for ~50,000 cubic feet of gas - which had to be flared...

(Source)

And since then, EXR has:

- Increased its resource base - Just yesterday EXR increased the (2U) prospective resource in coals to 3.6 trillion cubic feet of gas.

- Put out lab results from the well - EXR confirmed pressures 80% higher than Perth Basin success story AWE’s Senecio-3 well and porosities >10% in its sandstone intervals. Generally, the higher the pressures & porosities, the better the flow rates are for a project.

- Started mobilising for its flow test - With flow testing to start in mid-April.

The expectation going into the program was to find unconventional gas reservoir and then stimulate (frack) it to flow gas - like the other discoveries in the region.

But the free gas section was the big material news that could have implications on how the basin is viewed not just by EXR but oil and gas majors drilling in the region too...

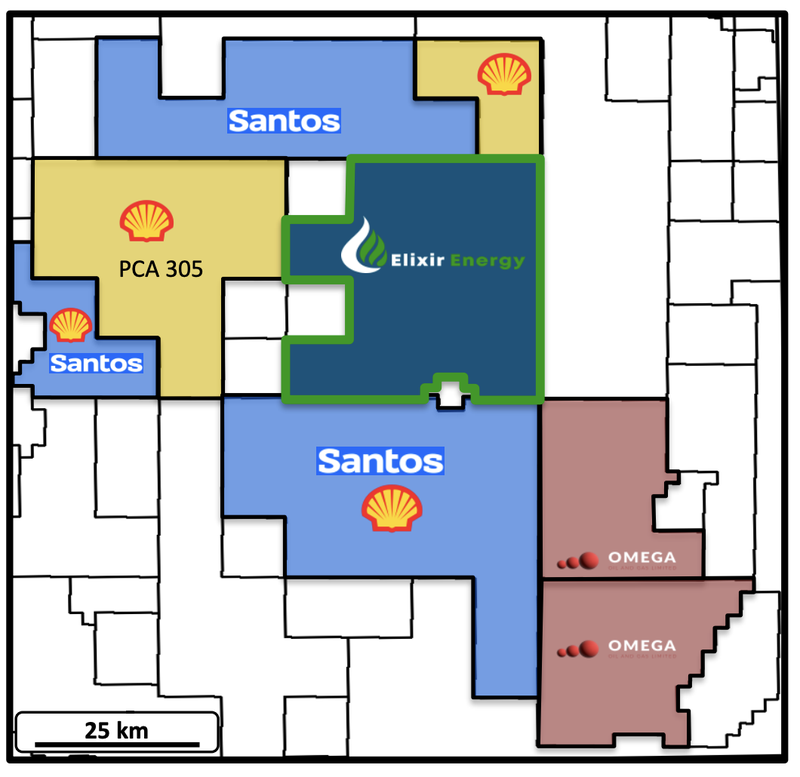

One of those majors drilling in the region is Shell and no doubt they would have taken a keen eye at the unconventional section EXR hit at Daydream-2.

(Source)

After all, Shell is the one who acquired BG Group for £47bn.

BG were the ones that initially made the Daydream-1 discovery ~5km away from EXR’s well back in 2012.

Up until now, everyone who has been active in this part of QLD has been working with the theory that the type of reservoirs at play need to be drilled, fracked and then flow tested.

After EXR’s result last year, we wouldn’t be surprised to see other companies start looking for conventional reservoirs either...

But for now we are more interested in what EXR is doing.

Specifically - EXR’s upcoming flow test in April.

In less than two months' time, EXR expects to be flow-testing its Daydream-2 well.

The objective for the flow test being to show the well can produce flow rates that are considered commercially viable.

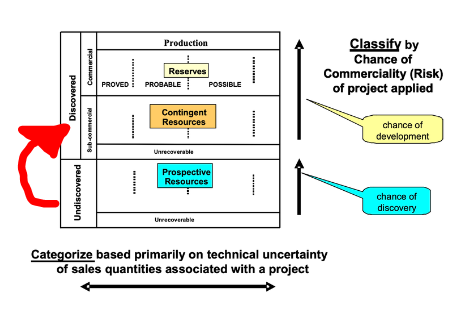

AND to try and convert some of the giant 3.6 trillion cubic feet prospective resource into the contingent/reserves category.

🎓 Learn more about why contingent resources matter here: How to Read Oil & Gas Resources

At the moment EXR has ~395bcf in contingent resources, we are hoping to see that number increase after the flow test.

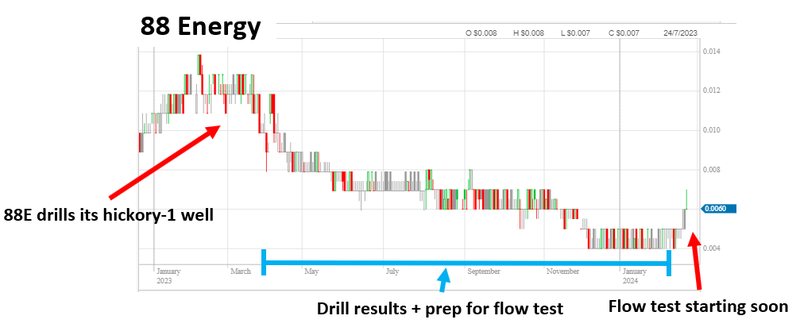

88E up 30% this morning

Another one of our Investments is just days away from a flow test is 88 Energy.

88E, like EXR, drilled its well last year and chose to run its flow test a few months later.

During that quiet period between the first drill and the flow test 88E’s share price did what EXR’s has been doing for a few months now.

Trading down from the prices we saw immediately before/after the drill program.

Now with the flow test just days away, we have started seeing some action in 88E’s share price.

(88E also just announced progress on its farm-in to a new Namibian project.)

EXR is trading well below the post drill highs (~12c) and the price of its last cap raise (8.5c).

We think that it is all about market sentiment and that EXR, like 88E could start to get interest again as we get closer to the flow test in April.

Over in Zimbabwe, we are waiting on IVZ to reveal their forward plan after they have had enough time to process all the data from their Mukuyu-2 discovery back in December.

We expect a flow test from IVZ in the medium term based on the fact that IVZ ran a “7 inch production liner” in the discovery hole... in anticipation of running a flow test.

We are keenly anticipating IVZ’s forward plan and timings to be released.

NHE is also planning flow tests in 2024 after lab results revealed very high helium concentrations of 2.46%.

Looks like 2024 is going to be the year of the flow test... with 88E and then EXR as the first cabs off the rank.

What we want to see from EXR’s flow test -

From EXR’s flow test the main thing we want to see is EXR taking its giant prospective resource into a higher classification.

For us, EXR’s Daydream-2 well is less about trying to get EXR’s project into production as quickly as possible and more about proving up and de-risking its project.

EXR is a small cap explorer and so we think that the more logical steps to unlocking value from its projects are around de-risking the project to the point where it is in the “sweet spot” for bigger companies to engage with EXR on a deal.

Especially considering EXR’s project is surrounded by heavyweights of the industry like Shell and Santos.

Rarely do we see small cap oil and gas players discover, define and then put projects into production...

Almost always, once the smaller company has de-risked a project, a bigger player comes knocking...

We will be putting out our bull,base and bear case expectations for the flow test closer to the program starting in mid-April.

Can EXR replicate the Perth basin success stories?

In our last EXR note we looked at how EXR’s project compares to some of the discoveries we saw across the Perth basin over the last decade.

See our note here: Did EXR Just Unlock Another Australian Deep Gas Play?

The reason we compared EXR’s result to the Perth Basin was because of the analogues with what EXR did at Daydream-2 and Australia’s largest conventional onshore discovery in the last 30 years.

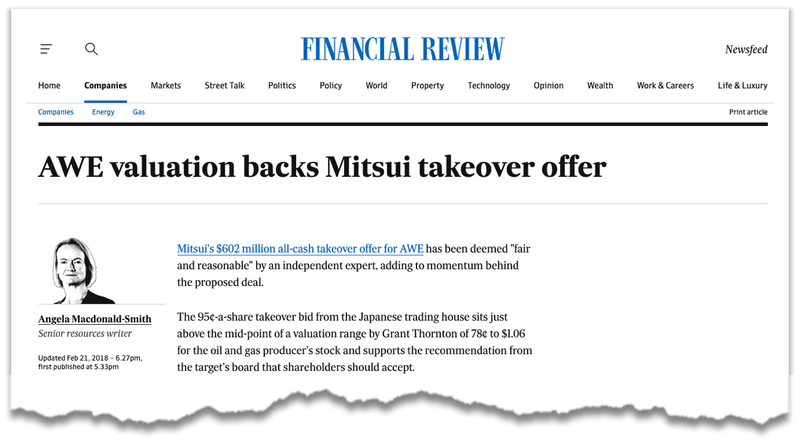

That discovery was made by AWE in 2014.

AWE was drilling an unconventional appraisal well in known gas-bearing reservoirs (Dongara/Wagina), BUT the well was drilled deeper to test seismic targets at depth and hit conventional gas.

AWE’s Waitsia became the largest conventional onshore discovery in Australia in over 30 years.

Four years after the Waitsia discovery, AWE was taken over by Japanese conglomerate Mitsui for $602M.

(Source)

Similar to AWE, EXR hit conventional gas while drilling an unconventional focused appraisal well.

Of course it's still very early days for EXR but we are looking forward to seeing what comes from the project especially considering EXR has a team that has built up and sold small cap explorers before.

EXR’s Chairman Richard Cottee took Queensland Gas Company from a $20M capped junior through to a $5.3BN takeover back in 2008 - the company doing the buying was BG Group (now Shell)...

AND EXR’s Managing Director Neil Young and Director Stephen Kelemen are both ex-Santos management.

(Source)

Overall, whatever EXR has found, we think it has the team in place to drill out and make something of its project.

What’s next for EXR?

Flow test of Daydream-2 in mid April 🔄

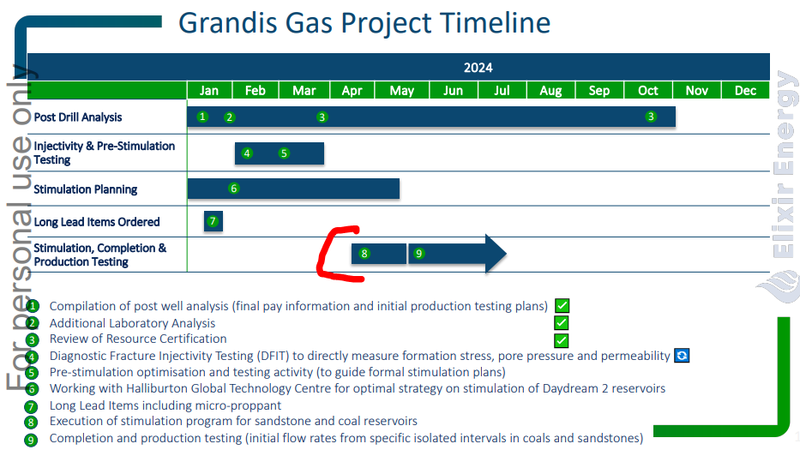

EXR expects the flow testing program to start in Mid-April 2024.

Over the next 2 weeks EXR expects to complete a wellbore clean out and “Diagnostic Fracture Integrity Tests (DFITs)” to start in March ahead of the flow test.

Below is a timeline EXR had previously released for the Daydream-2 well:

Ultimately the flow test in 2024 will be the major catalyst to see if EXR can achieve our Big Bet, which is as follows:

Our Big Bet for EXR:

“EXR to achieve a $1BN market cap through successfully advancing one or more of its three projects: its Mongolia gas project, Mongolia green hydrogen project, and/or its Queensland gas project.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EXR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Context on EXR’s Daydream-2 well & the latest from MD Neil Young

Leading up to its drill program last year EXR put out a pretty decent summary of what it was trying to achieve in video format.

For those who missed it check out the following video:

(Source)

EXR’s Managing Director Neil Young also put out a video recently giving a bit of an overview of where EXR is and what it expects to come next for EXR.

Check out what Neil had to say here:

(Source)

What are the risks?

The results from EXR’s Daydream-2 well are relatively strong so far but the main risk for EXR is still “commercial risk”.

As is with any oil & gas project, discovering a resource is just one of the two factors in proving a company has something of value.

The second and usually the more important part is to show that the discovered resource can flow to surface at rates that make the project commercially viable.

Without strong flow rates the economics of a project never stack up and most projects can sit idle for decades until new technologies are created to help suck that resource out of the ground or until prices for oil and gas are high enough to make lower flow rates feasible.

EXR is now a few weeks away from flow testing its Daydream-2 well where we will find out whether or not EXR’s project can produce oil/gas at commercially viable rates.

Uneconomic flow rates would mean EXR spends a lot of capital for very little return in terms of shareholder value, which we think could lead to a re-rate down in EXR’s share price.

As a result we think “commercial risk” is the key risk to our EXR Investment in the short term.

To see all the risks to our EXR Investment thesis, check out our EXR Investment Memo here.

Our EXR Investment Memo

In our EXR Investment Memo, you can find the following:

- Our EXR Big Bet

- Key objectives for EXR

- Why we are Invested in EXR

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.