Surprise Flow rate? Sounds good to us EXR

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,327,858 EXR shares and 1,071,429 EXR options at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time.

Surprise?

EXR just announced 1.3 mmscf per day stabilised flow rate from its Daydream-2 well.

It also achieved a peak flow of 2.3 mmscf per day...

Wait... what?

EXR wasn't meant to be doing a stimulation and flow test till ~ May, right?

Isn’t the flow test meant to be happening next month?

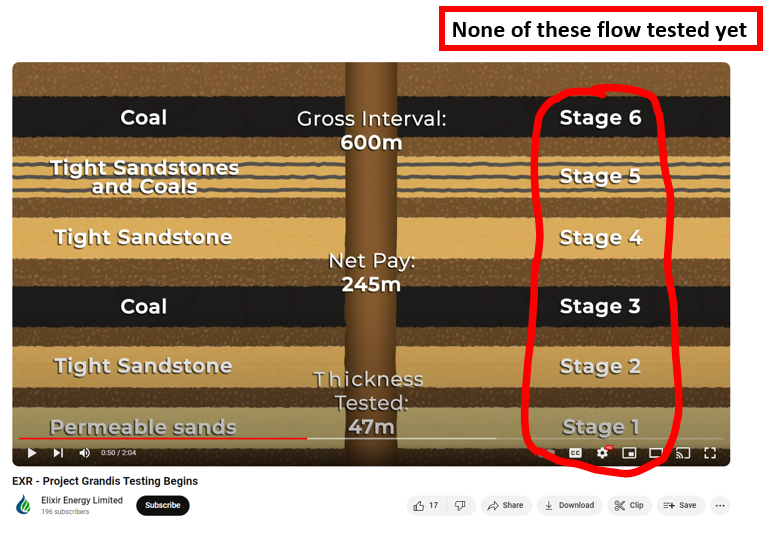

Today's announcement is ONLY from the unexpected FREE GAS zone that they hit while looking for tight gas.

It’s the flow rate from the zone that DOESN’T need stimulation...

There are still SIX more tight gas zones that will be stimulated and flow tested in the coming weeks.

With a big start of 1.3 mmscf per day gas flowing from the free gas zone, we just need a few more mmscf/day from the 6 further zones for the flow to be commercial (in our opinion - more on this later).

And we will find this out in the coming weeks when EXR runs the planned stimulation and flow tests...

EXR says that today's free gas flow is the deepest unstimulated flow of gas in onshore Australia East of the Perth Basin.

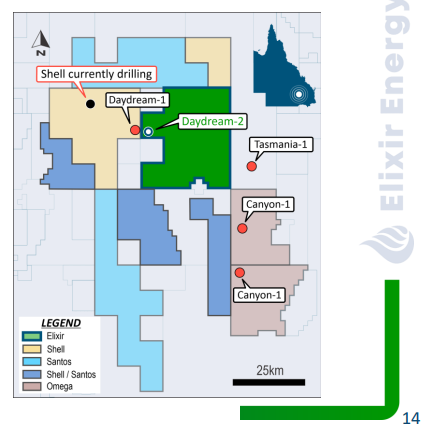

(which is basically all of Australia - check out our handy map below)

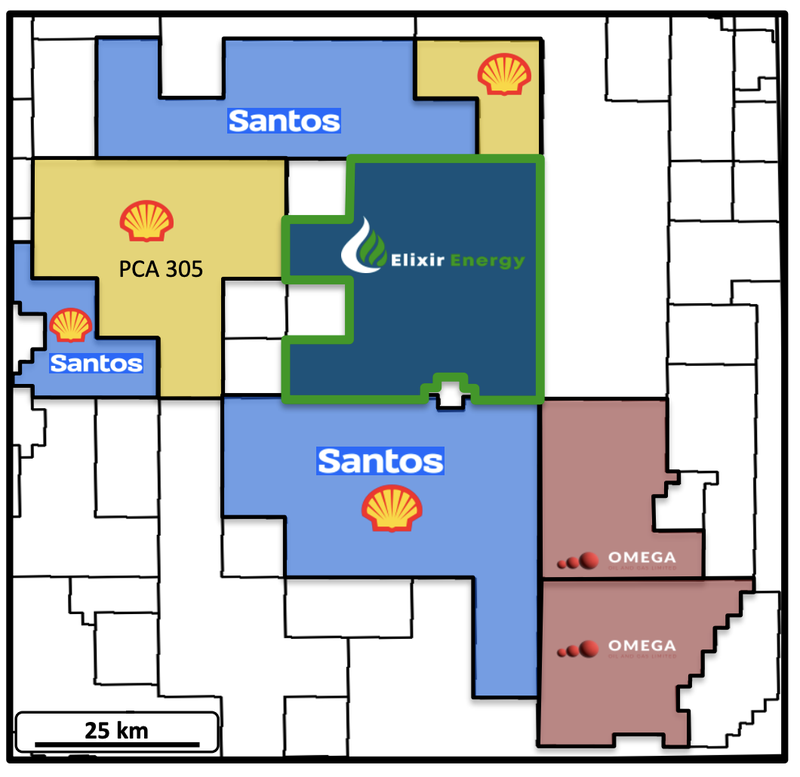

This opens up all sorts of new possibilities of free gas in the basin for EXR - and its direct neighbours - majors Santos and super major Shell...

How did EXR get here?

6 months ago EXR drilled its Daydream-2 well.

The target at the time was tight gas reservoirs, which would need to be stimulated before being flow tested.

The unexpected surprise post drilling was EXR hitting a free gas column.

Free conventional gas - like what EXR hit - is the easier type of gas to commercialise as it typically flows to surface naturally.

We covered that news on the day here: Did EXR Just Unlock Another Australian Deep Gas Play?

And today EXR wrong footed the market (again) by announcing an unexpected flow test on that free gas column...

It's flowed at a stabilised flow rate of 1.3mmscf per day already - a rate that is already pretty strong on its own.

(the peak rate was a lot higher at 2.3mmscf per day)

And EXR still has the other unconventional zones left to stimulate and flow test.

That flow test is happening in the coming weeks..

If the combined flow test for the well hits >5mmscf per day number than we think EXR could unlock:

- Resource upgrades/updates - EXR can upgrade its existing 395 BCF contingent resource and 3.6 TCF prospective resource into a bigger contingent number OR a maiden reserve number for the project.

- Partnership interest - Flow test data gives potential farm in partners strong data to work with, and also gives a good idea of the commercial potential for EXR’s project. EXR has previously mentioned its aiming to “gather data for a 500 well development”...

We already know the majors like projects of serious scale, and have an interest in this part of the world already.

Shell is drilling next door to EXR and is looking to emulate the success of a well previously drilled by BG group ~10 years ago.

Remember Shell took over BG Group for £47BN - the same company that initially made the Daydream-1 discovery ~5km away from EXR’s well back in 2012.

EXR already has in place data sharing agreements with majors Santos and Origin.

The Santos partnership is especially interesting because it is centred around “exploring regional prospectivity” - encouraging technical discussions about the deeper exploration plays in the region.

(Source)

Here is a map showing where EXR’s project sits relative to Santos and Shell:

EXR delivering a commercial total flow rate from the well is the key step needed to start off partnership discussions with majors (who will hopefully farm in to do another well).

The surprise flow today from the free gas is an unexpected great start.

In the coming 6 to 8 weeks EXR will stimulate and flow test the SIX tight zones, which we hope combined, will add up to a commercial flow...

What we think a strong (commercial) flow rate looks like:

So as it stands, EXR has per day from just one part of its well.

The free gas (conventional) column that produced today’s flow came from a reservoir ~17m thick.

EXR is still yet to stimulate and test the other ~245m of net pay across the unconventional parts of the well.

So there is scope for EXR to add to its flow rate significantly.

Going into the flow rate our expectations across all reservoirs are as follows:

- Bull case = >5mmcf per day flow rate

- Base case = 2-5mmcf per day flow rate

- Bear case = <2mmcf per day flow rate

AND we think these numbers would be a conservative take on the project's overall potential.

In a recent video, EXR mentioned that the stimulation program would be on only ~19% of the overall net pay of the well:

(now, before you scroll over without clicking - it’s only a 2 min video, an easy watch that explains the current well and planned stimulation and flow test - you can watch it here)

(Source)

So technically, EXR could go back and frack the remainder of the net pay zones and get an even higher flow rate.

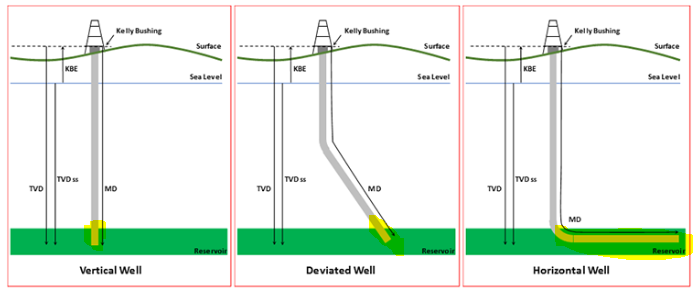

ALSO, EXR’s Daydream-2 is a vertical well - EXR could later try to increase flow rates by drilling horizontal/deviated wells which could tap into bigger chunks of its reservoirs.

For now, our focus is on the results of the current flow test, but the potential upside to further increase the flow rate is important - especially from a corporate interest perspective.

It's the sort of thing we expect anyone looking at EXR’s project from the outside to be thinking about.

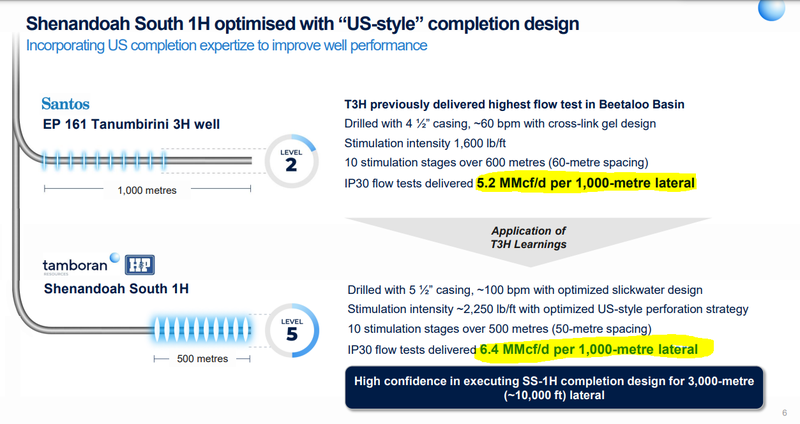

A good example of this type of corporate interest is in the Beetaloo basin in the NT.

The Americans (who have a heap of experience with unconventional oil and gas projects in the US) came in and took the driving seat for Tamboran Resources and are now running large scale stimulation programs over their projects.

(Source)

For some context on flow rates - Tamboran is getting 5.2 to 6.4 mmcf/day of flow in horizontal wells (on a 1,000m lateral basis).

Tamboran is currently capped at around $390M - almost 5x bigger than EXR right now.

On JUST its free gas zone EXR has achieved 1.3 mmcf - now we wait for EXR to stimulate and flow test the SIX other tight zones to try and reach 5 mmcf (our internal bull case)

There are obvious differences between the projects i.e the location and type of well being drilled (horizontal/vertical wells) but Tamboran’s results give us a good idea of what corporates see as “success”.

Here is an image showing why horizontal/deviated wells can sometimes have stronger flow rates then vertical wells (because they capture a bigger area of a reservoir):

(Source)

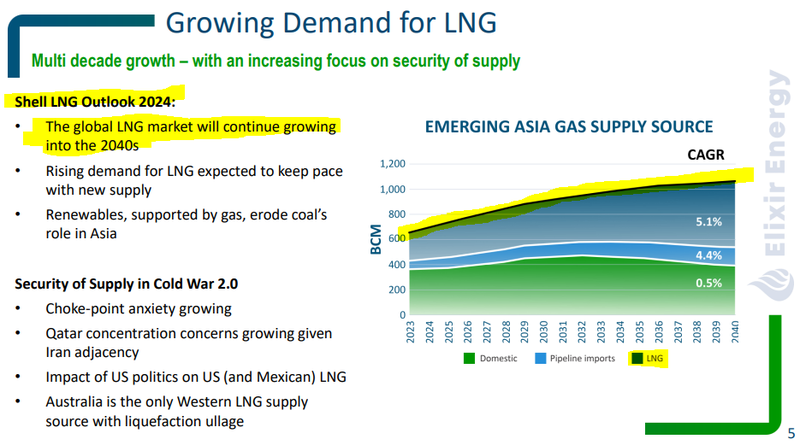

East coast gas macro investment thematic

Another thing going for EXR’s project is that it sits in QLD, where it has exposure to:

- The global Liquefied Natural Gas (LNG) markets - The three LNG plants in Gladstone next to EXR’s project have never operated at full capacity and could take more gas feedstock to ship to international markets.

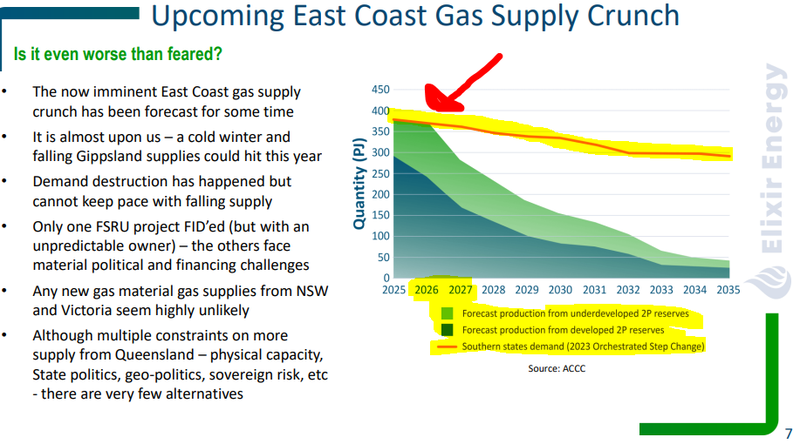

- The east coast gas markets - East coast is forecast to be short gas in 2028 and expected to start experiencing momentary shortages in 2025-6. EXR could provide gas into that market.

Both markets are challenged from a supply demand perspective and we think that in the medium term, the pressure will be to the upside.

Global markets had a supply shock in 2022 when the Russia/Ukraine conflict broke out.

The Europeans were scrambling for supply and were resorting to importing LNG from places like Australia.

That put pressure on global LNG prices. With demand from Asia always increasing, we think demand for LNG products will continue to be high going forward.

EXR’s project sits next to the LNG plants in Gladstone that have never operated at peak capacity and can therefore take in new gas supplies.

As for the east coast market, the story for a long time has been that there will be a big supply crisis due to falling investment in new supply and falling production from the Gippsland gas fields in offshore Victoria.

The Australian Energy Market Operator (AEMO) event put out a statement titled “Gas market outlook signals need for new investment” which says supply shortages could start as early as the 2025 winter months.

The AEMO specifically said “AEMO’s latest gas market outlook for Australia’s east coast has forecast a gap in gas supply for southern states from 2028, as production from Bass Strait continues to decline faster than demand”

Santos’ CEO also agrees and is calling for regulatory easing to allow more investment in the sector...

We think EXR is about to deliver major catalysts from its QLD gas project at the right point in time, just ahead of the macro theme heating up.

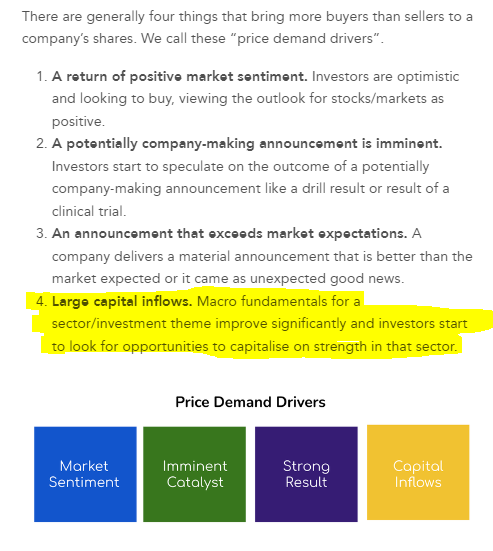

Long time readers will know that we think how hot a macro investment thematic oftentimes can have the biggest impact on a company’s share price.

🎓 See our educational article on what makes share prices go up here: Why do shares prices go up?

Hopefully as the project is advanced, EXR’s share price responds to what we hope is good news and the company’s valuation grows as a result - this forms the basis for our EXR Big Bet which is as follows:

Our Big Bet for EXR:

“EXR to achieve a $1BN market cap through successfully advancing one or more of its three projects: its Mongolia gas project, Mongolia green hydrogen project, and/or its Queensland gas project.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EXR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What are the risks?

The results from EXR’s Daydream-2 well are relatively strong so far but the main risk for EXR is still “commercial risk”.

The upcoming flow test results will ultimately dictate whether or not EXR’s project can produce oil/gas at commercially viable rates.

Uneconomic flow rates would mean EXR spends a lot of capital for very little return in terms of shareholder value, which we think would lead to a re-rate down in EXR’s share price.

EXR will also likely need to raise capital to fund its tests in 2024, so “funding risk” is still apparent for EXR.

To see all the risks to our EXR Investment thesis, check out our EXR Investment Memo here.

Our EXR Investment Memo

In our EXR Investment Memo, you can find the following:

- Our EXR Big Bet

- Key objectives for EXR

- Why we are Invested in EXR

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.