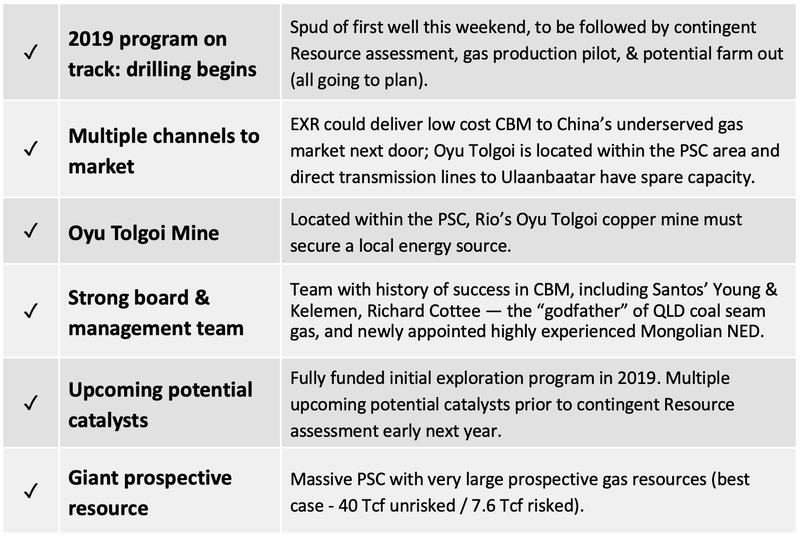

Our Top Pick of 2019: Elixir Energy (ASX: EXR) Drilling This Weekend

We’ve been waiting months for this, now the moment has finally arrived.

The Next Oil Rush’s Top Energy Pick for 2019, Elixir Energy (ASX:EXR) will this weekend start drilling its first well into its independently assessed 40 trillion cubic feet best estimate, unrisked, recoverable gas resource on the doorstep of China.

The stock has been up as high as 50% since we first brought readers the story on 11 July 2019, however with the drill bit set to start turning this weekend, and the company still with a sub-$25 million market cap, it might only be the beginning.

The drilling program has been expanded from two core-holes (plus an optional third core-hole) to two to four stratigraphic chip-holes, in addition to the drilling of two firm and fully evaluated core-holes. The option to drill a third core-hole remains.

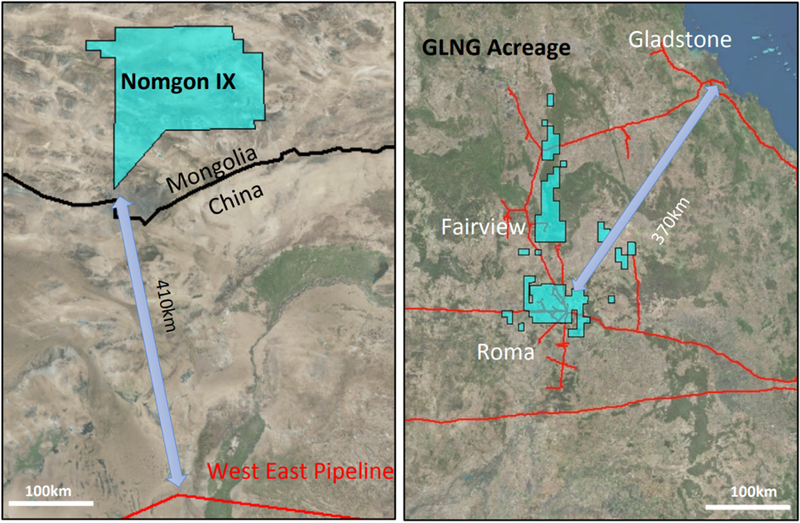

Located in the South Gobi Desert on the Mongolia-China border, EXR has a 100% interest in a mammoth seven million acre (30,000km2) production sharing contract (PSC) – the Nomgon IX coalbed methane (CBM) PSC — entered into with the government of Mongolia itself.

The PSC lies over a major Permian coal bearing region and has a giant independently certified CBM risked 'best case' prospective resource of 7.6 Tcf and as we mentioned above, an un-risked ‘best case’ prospective resource of 40 Tcf.

This Permian coal region is of the same age as that of Santos’ (ASX: STO) prime Queensland coal seam gas (CSG) acreage and in terms of geologic quality, it stacks up remarkably well on a number of fronts when compared to Queensland’s Bowen Basin.

Aside from the geology a key difference between the Bowen Basin and EXR’s ground is the distance to the biggest energy consumer of the next century — China. And a clean gas resource of the scale Elixir is looking to prove up is just what China needs right now.

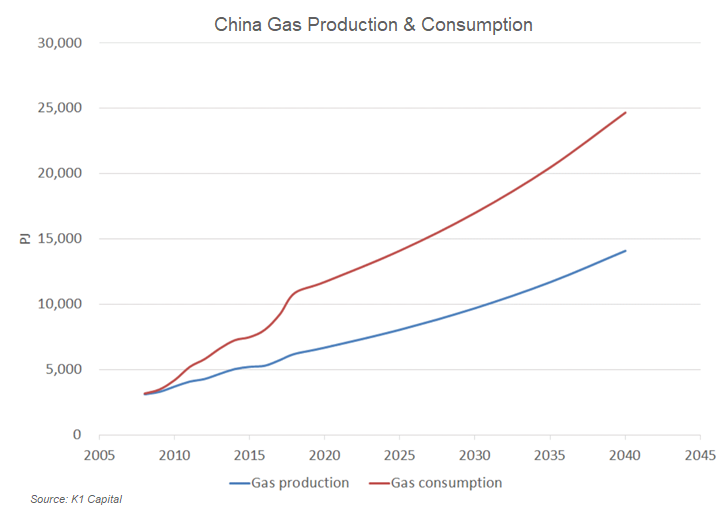

Chinese gas demand is expected to more than triple over the next 15 years and the country does not have enough gas within its own borders. It needs to provide enough electricity for its growing population, all the while working to reduce deadly particulate emissions from coal and combat global warming.

There will be no shortage of hungry customers for EXR assuming it can prove up the true scale of this gas resource.

Sitting within Elixir’s PSC is the Rio Tinto (ASX: RIO) operated Oyu Tolgoi mine, which is currently importing electricity from China, yet is required by the Mongolian government to source a local energy supply.

EXR’s current exploration program was designed to be the most technically advanced ever conducted for CBM (coal seam gas (CSG), as it is known in Australia). Each well is expected to take 15 to 20 days to complete and will involve substantial coring.

Positive drill results over the coming weeks may ignite the market and re-rate this sub-$25 million capped stock.

EXR is led by a management team and board with a history of CBM success, including the godfather of Queensland coal seam gas, Richard Cottee, who famously took Queensland Gas Company (QGC) from a $20M capped junior into a $5.8B takeover play.

In his letter to EXR shareholders in last month’s Annual Report, Cottee pointed to the company’s “eye-watering risk/reward equation”.

He explained that the major de-risking task he faced in 2002 at QGC, is similar to that facing Elixir now.

“Elixir’s Mongolia coal seam gas (CSG/CBM) acreage appears to contain a large portion of gas-prone coal with acreage roughly equivalent to what QGC held in 2002, when QGC had a similar market capitalisation,” said Cottee.

Six years later QGC was taken over for A$5.8 billion by BG Group, and its gas is now largely sold to China. $20M to $5.8B in six years is serious value creation – we are sure Mr Cottee would like to repeat that story with EXR.

Also on EXR’s board are highly experienced former Santos (ASX: STO) execs Neil Young and Stephen Kelemen — the latter was in charge of the proving up and developing of Santos’ CSG assets as QGC was evolving.

With the first spud scheduled for this weekend, upcoming catalysts for value creation include drilling results — due in late 2019, a contingent Resource assessment — scheduled for early 2020, and then a gas production pilot later that year. If the boxes keep getting ticked we would assume EXR would then farm-out a portion to a larger partner.

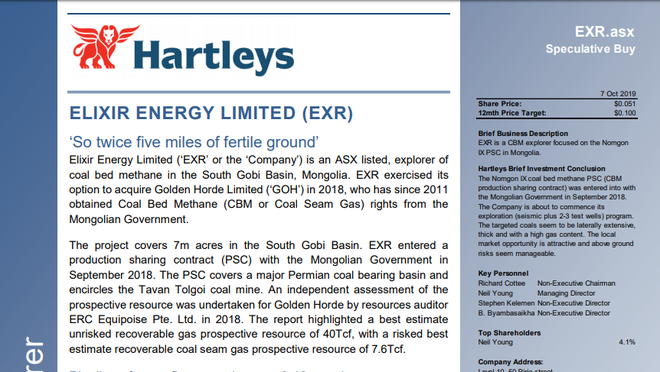

The opportunity here has led respected analyst John Young of K1 Capital to assign a $0.22 per share valuation to Elixir — our Pick of the Year — while Patersons Securities have recognised it as “one to keep an eye on” as a good way to play the China gas thematic. Hartleys have also said it’s a ‘Buy’, valuing the company at more than double its current market cap.

Share Price: $0.048

Market Capitalisation: $24 million

Here’s why we still like Elixir Energy as Next Oil Rush’s Energy Pick of 2019:

It was early July when we highlighted Elixir Energy (ASX:EXR) as the Next Oil Rush’s Pick of 2019 — Introducing Our Top ASX Energy Pick of 2019 — and already the stock has begun to deliver for shareholders.

As you can see on the chart below, Elixir has surged from below 4.0 cents per share in July to as high as 6.5 cents as the company progresses its planned exploration program.

However, it’s early days still and we expect the stock will gain plenty of attention once drilling commences and results begin to arrive.

Here Neil Young speaks to the stock's recent performance:

The Nomgon IX CBM PSC: a giant gas prospective resource

Located in the South Gobi Desert in Mongolia, immediately next to the Chinese border, Elixir’s Nomgon IX coalbed methane (CBM) production sharing contract (PSC) covers an area of around 30,000km2 (over 7 million acres).

The PSC has a “giant prospective gas resource” with an unrisked best case recoverable prospective resource (‘best case’ (2U)) of 40.1 Tcf, and a risked best case resource of 7.6 Tcf, which is just slightly less than the total volume of gas consumed across all of China in a year.

This is a region that is exceptional in its combination of massive potential gas and renewable resources, minimal competing land uses, and a location right in the heart of Asia.

Gas and renewable energy are symbiotic — renewables are intermittent and can be fired up by adding gas to the mix and therefore enhancing renewables value. It’s something that is being embraced by the world’s largest petroleum companies such as BP, Shell, and Total that see a future in renewables enhanced by gas. The South Gobi has incredibly good renewable resources and the combination of the two would add value to both.

This video provides a look at Elixir’s Nomgon IX PSC:

Here's Neil summarising the CBM opportunity at the PSC:

Demand & China’s gas market

The rapid rise in China’s gas demand has been driven by air quality concerns in its major cities and legislation changes have resulted in a switch to gas from coal and an increase in renewable energy. Gas also provides major greenhouse emission benefits over coal.

The Chinese government has a target of gas supplying 15% of total energy consumption by 2030, and while air quality remains poor by international standards it is likely that China’s targets will be progressively tightened, providing ongoing support for gas demand.

Estimates from BP point to China’s natural gas demand almost doubling to 14% of total energy demand by 2040, even taking into consideration a rise in renewables’ share from 3% today to 18% in 2040.

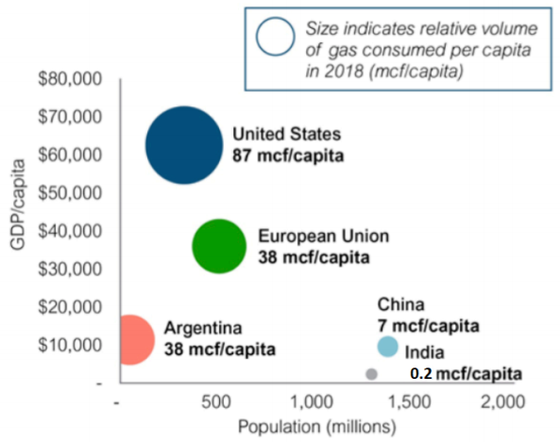

Here you can see that there is significant potential for per capita consumption growth in China when compared to more developed regions including United States, the EU, as well as Argentina.

On a per capita basis China’s gas demand is tiny compared to the likes of USA. The US consumes about 25 trillion cubic feet of gas per year, while China in total consumes just 4-5 Tcf. Clearly there is a likelihood of much stronger demand out of China as its economy continues to develop and becomes cleaner.

A lot of gas is produced from coal seams in China – both under specific PSCs and by mining companies, however China’s domestic gas demand already significantly exceeds domestic supply from all sources and this shortfall is expected to increase.

One issue is that Chinese coal basins are generally younger than Permian so are not as productive, meaning demand growth can’t be met by indigenous gas options.

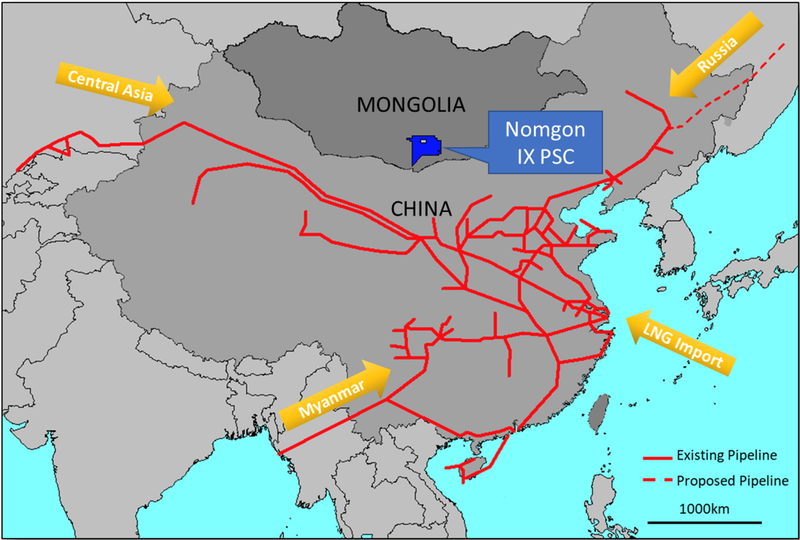

Because of its inability to produce enough local supply, China is importing gas and it is doing so from every direction to gain diversification — from both an economic and a geopolitical point of view.

The shortfall is being met by pipeline imports from Central Asia and Myanmar as well as more pricey LNG imports along the coast, while pipeline imports from Russia via the Power of Siberia pipeline are expected to commence this year.

China’s gas network, as seen below, includes a 5,000km pipeline from Turkmenistan. There’s a pipeline being built from Russia which is 3,000km long. Then there’s offshore gas piped in from Myanmar, which crosses over mountains to reach southern China.

Compared to any of these options — let alone the seaborne gas from Australia and other countries — Mongolia is exceptionally well placed. Located on the Chinese-Mongolian border, the PSC is just 410km from China’s East-West Pipeline.

Below you can see the impressive size of Nomgon IX (left) at 30,000km2 and its proximity to the Chinese pipeline. This is similar in distance to Santos’s GLNG licences in Queensland (right) to the Gladstone LNG port in Queensland. The gas is transported by pipeline from a hub in the Santos acreage to the port of Gladstone where it is liquefied at vast expense, put on boats and shipped to locations including China.

The terrain of the two is similar too — very flat, dry, and sparsely populated. If you want to build a pipeline, that’s the sort of terrain you want to go through. It’s “a very simple exercise” says Neil Young and he would know, having been part of the Santos Gladstone LNG team.

Gas is expensive to move

A key point about gas is that it’s very expensive to move. If you need to deliver gas by ultra long distance pipelines like those supplying China, then about half the delivered cost is the pipeline cost. That’s also true if delivering by boat.

Therefore, if gas is located proximate to a market the cost advantages are very significant. To put it into dollar terms, Australian gas lands in China at about $10, about $5 of that has to pay for the transportation.

Mongolia’s proximity would make pipeline costs much lower than from the current distant alternatives and will also provide diversification over buying more from, say, Russia or USA.

That said, due to the major supply shortfall anticipated in China, economic growth and government policy are anticipated to be more important drivers of gas demand in China than simply price.

Not only is Elixir’s PSC proximate to Chinese distribution networks but it could fill much needed domestic supply as Mongolia’s existing electricity supply fleet is near breaking point with new generation required.

While the PSC appears to be in the middle of the desert where there is no infrastructure, that is not actually the case. The Nomgon PSC contains considerable existing electricity transmission infrastructure and is crossed by multiple transmission lines.

Notably, a 330 kV line currently imports power from China to power Oyu Tolgoi, plus there’s a large scale 220 kV line running south from Ulaanbaatar to Oyu Tolgoi that has substantial spare capacity.

Any electricity generated in the South Gobi and delivered into the national grid would reduce coal-fired pollution in the country’s capital, Ulaanbaatar — a major priority for the government as Ulaanbaatar is home to more than 40% of the country’s population.

Here Neil considers EXR's potential gas customers:

2019 exploration program underway

The objectives of the 2019 exploration program at the Nomgon IX CBM PSC is to determine the presence and thickness of coal, gas content and composition, permeability, and progress towards booking contingent resources.

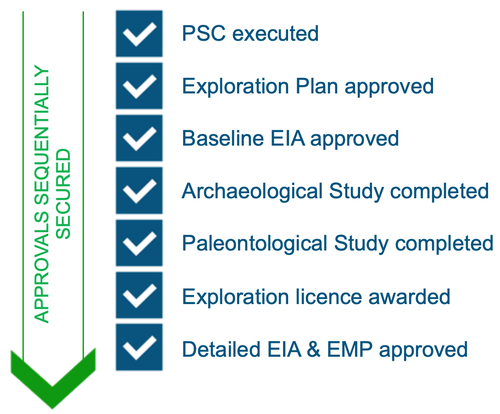

Elixir has secured all exploration approvals and is set to progress to the spudding of the first well. The ease and speed with which the approvals were granted speaks to the strength of the team and the relationships with various levels of the Mongolian government. In global terms, the securing of approvals was remarkably rapid — approvals have been known to take considerably longer in many countries.

So far, Elixir’s exploration program has this year focused on obtaining those approvals and, more importantly, gathering data from multiple sources including the recently completed seismic survey, stitching it all together and working out the optimal places to start exploration.

Seismic Survey complete

The 2019 Nomgon IX Seismic Survey has now been completed with the process taking just over a month from August to September. Elixir partnered with Mongolian contractor Micro Seismic LLC who has substantial experience in the region.

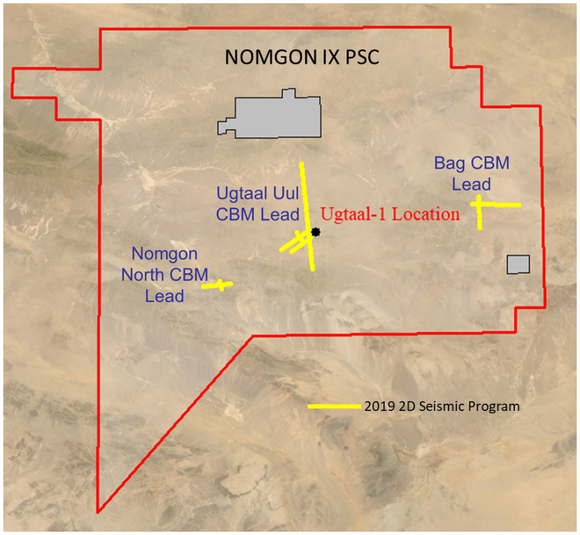

The survey acquired 131km of 2D data over key coal seam gas (CSG) leads at Ugtaal Uul, Nomgon North and Bag.

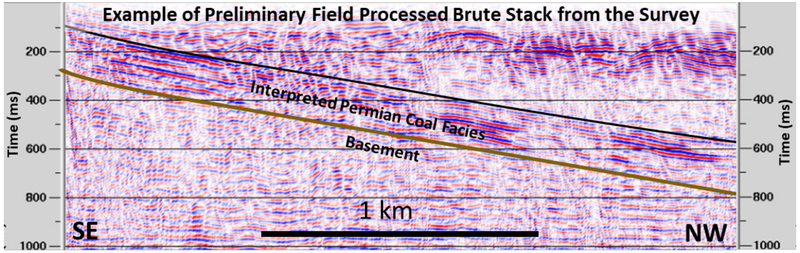

The seismic indicates coal seams at the right depths:

Initial work has allowed the company to target its first well locations and while it’s still processing some of the seismic outputs, Elixir expects to soon have a fully processed and interpretive set of seismic results.

Drilling starts now

Drilling will start this weekend, as announced this morning, with the spud of the BO-CH-1 chip-hole. The aim of the drilling campaign is to deliver the data required to book the country’s first gas discovery by early next year.

After some logistical issues in China were resolved, the international standard desorption and permeability testing tools arrived from the USA and Australia, respectively. These tools have been set up to be deployed to the field when the core-holes commence and initial training in their use with the local contractors undertaken.

The drilling program has been expanded to include two to four stratigraphic chip-holes in addition to the drilling of two firm and fully evaluated core-holes. The option to drill a third core-hole remains. Two rigs will be used.

The chip-holes will drill conventionally through the stratigraphic section, with chips or cuttings taken and logged without the need for full hole coring.

The chip-holes will be used to gain valuable information about the general geology and confirm coal continuity. They will also support and substantiate the recently acquired 2D seismic program, assist in the final placement of the two fully evaluated core-holes, and seek to de-risk locations for next year’s drilling program.

Side by side with the core-holes, the chip-hole program is a highly cost-effective way of gathering geological information, with each well expected to take only around seven days.

It’s expected to be a useful exploration tool over the very large Nomgon PSC area in the future. The program will be undertaken on two drilling rigs.

Elixir plan to announce the results of the chip-hole program once the four well program is complete and before the more comprehensive two well core-hole program begins in the latter half of October.

Elixir is using the highly respected Mongolian owned and operated drilling contractor, Erdenedrilling LLC for the drilling program. Experts from both Australia and USA have also been brought in to help supervise the drilling of the core-hole wells and to ensure that the testing of the data can be verified and audited by international audiences.

The campaign has been designed to be the most technically advanced ever conducted for CSG in Mongolia. It will provide information not only for this year’s plans but will also help guide next year’s plans as well.

Each well is expected to take 15 to 20 days to complete and will involve substantial coring, after which the wells will be remediated. The chip-holes will each take less than a week to complete.

Here Neil explains the drilling program, including initial chip-holes and the core-holes:

Elixir will be providing regular market updates as the planned wells deliver the key data gathered on coal thickness, gas content and permeability.

On completion of the current 2019 exploration program (2D seismic, chip-hole and core hole drilling), the geological risk of the project will be significantly reduced.

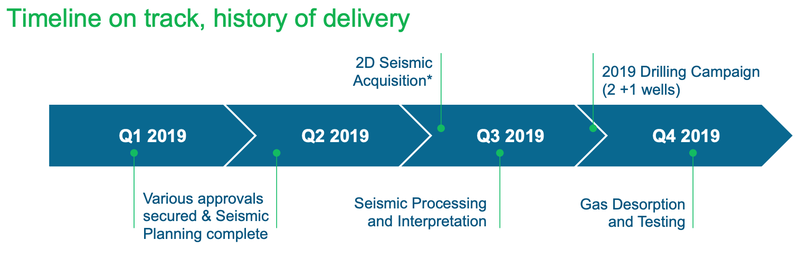

Here’s a snapshot of the year’s exploration program (taken from before the drilling program was expanded), with just gas desorption and testing still to take place after the completion of the drilling campaign:

Once available, the results of the drilling and seismic survey will feed into an updated, independently verified resource estimation process around the start of the 2020 calendar year.

A successful drilling program will lead to a booking of contingent resources — initially in only a small part of the PSC — that would be the first discovery of a gas accumulation in Mongolia.

The huge area of the PSC provides numerous target areas for further exploration using seismic, core-holes and stratigraphic wells. Delineation will require a pilot production test, the design of which is contingent on the results of the current work. A successful test would then provide the foundation for an initial reserve booking.

Here Neil outlines the objectives of the drilling program and what to look for in the results:

2019 exploration funding sorted

The 2019 exploration program remains fully funded, with Elixir having received strong support for a placement of new shares in May, when it raised $3.6 million. The funds were earmarked to pursue the seismic and core-hole drilling program (with options to expand the drilling program beyond an initial 2 well plan), meet all government rents, fees and bonuses required under the PSC and cover working capital requirements.

At June 30 it had cash in the bank of $4.4 million. Stockbroker Hartley’s says the current program will cost between $3.0-3.5m in total, meaning it would seem fully funded for this current program.

Since the 2019 exploration program is fully funded at a 100% ownership level, the company has considerable optionality to deal with issues such as potential partners in the future.

Coalbed Methane: an unconventional gas

One important fact to note is that exploration of coalbed methane (CBM) — or ‘coal seam gas’ — is quite different from conventional oil and gas exploration.

It turns out that CBM is much lower risk, in terms of the probability of finding what is being looked for (thick, gassy and permeable coal seams). However, once found, conventional oil and gas formations are more productive and have features like much higher flow rates.

The two are just different, rather than one being better than the other.

This type of CBM exploration program is not to find some incredible gusher of oil and gas —that’s not how unconventional petroleum works.

Rather, Elixir is conducting large scale scientific experiments to access data that when assembled together confirms the presence of gas. If these data points do all do come together then by around the start of next year Elixir will aim to book a contingent resource, meaning it will have discovered a gas accumulation in Mongolia — the first one in the country and surely a sign of more to come.

That fact that CBM has a higher probability of a discovery adds confidence heading into drilling, as does the fact that the South Gobi Basin — the location of Elixir’s PSC — hosts Permian coals, which are generally the best geological era for CBM.

Like the South Gobi, Australia’s Bowen Basin in Queensland — which hosts Santos’ gas projects — is Permian, where large volumes of methane gas have been shown to be held at shallow depths within Permian coals.

Looking even longer term, there’s an opportunity for Elixir’s PSC to play a role in the production of “green steel”, which involves producing steel with hydrogen. That hydrogen would be produced by splitting methane (CH4) into hydrogen (H) and carbon dioxide (CO2). The CBM wells could then be used to sequester carbon dioxide underground.

Research & analysis

K1 Capital

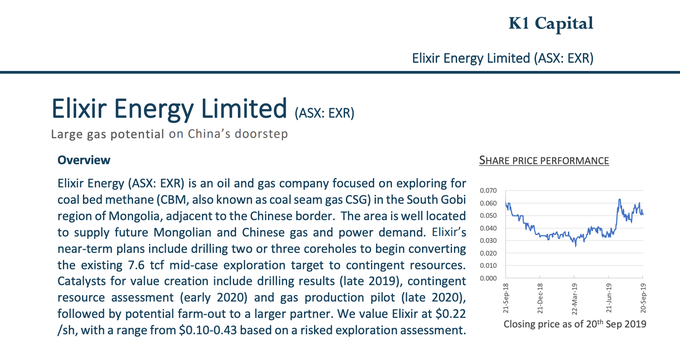

A research report released last week from K1 Capital, an independent research and analysis provider to the oil and gas and broader energy and resources sectors, gave a comprehensive overview of the business, the Nomgon IX PSC and the company’s prospects.

K1 Capital valued Elixir at $0.22 per share (with a range from $0.10-$0.43). This figure was based on a risked exploration assessment, drawing from the November 2018 independent prospective resource estimate and market trading multiples for peer companies — details of the methodology are available in the report.

Taking into account an anticipated dilution from raising funds for the 2020 exploration program (the 2019 program is funded) and expected exercise of share options and performance rights, K1’s valuation of Elixir ranges from $75m to $308m, driven by the wide range in resource size and EV/resource unit value uncertainty.

Importantly, the research report does highlight that being an early-stage speculative investment means there are no guarantees.

Yet K1 sees the real upside potential in Elixir being acquired by a larger entity, “we believe the value of the company will be ultimately be established by industry participants through a project or company transaction”. It noted that past transactions indicate that companies with large, well located, high quality resources can achieve strong interest.

Hartleys

Hartley’s have also produced a research note on Elixir. Analyst Aidan Bradley says, “With a current market capitalisation of circa $25m, the market is factoring in a very low conversion of the large current best prospective resource to contingent resources.

"While acknowledging that early stage CBM explorers are extremely difficult to value, we forecast an increase in project value towards $55m over the next 12 months." Bradley has a 10 cent 12-month target price and say it’s a Speculative Buy.

“At the moment, EXR seem to be as advanced as any competing local CBM project and with an experienced management team, large gas-in-place footprint and an active funded appraisal programme, is an interesting investment play on North East Asian gas demand,” he added.

Patersons Securities

Stockbroker Patersons Securities has also provided its opinion of Elixir, albeit a much briefer one than that of K1 Capital, or Hartleys.

Following Elixir’s presentation at the Good Oil Conference in Perth a Paterson’s analyst highlighted Elixir as “one to keep an eye on” in a brief note to clients. The analyst suggested that “Elixir may be a good way to play the China gas thematic — something that has been missing since Sino Gas’s departure from the ASX”.

The note explained that “The EXR team is technically astute and includes Stephen Kelemen (former manager of STO’s CSG business), Neil Young (ex-STO management, and has worked in Mongolia for the last eight years), and the ever humble Richard Cottee (Non-exec Chairman)”.

Patersons’ recognition that a key strength of Elixir is its management team and board, is one that we agree is key to the success of Elixir. It comprises an exceptional team of CBM industry experts...

Backed by an exceptional team of industry experts

Neil Young

Having founded Golden Horde Ltd in 2011 (which was later acquired by Elixir) to explore for gas on the Chinese border in Mongolia, Elixir’s managing director and CEO (and largest shareholder to boot), Neil Young, has been pursuing this opportunity in Mongolia for eight years.

This has understandably led to him developing strong relationships with Mongolian government bodies and technical experts over time. Young has more than twenty years’ experience in in the energy sector, and is a former business development manager at Santos (ASX:STO) where he helped build its coal seam gas (CSG) business.

Stephen Kelemen

Also from Santos, is non-executive director Stephen Kelemen, who is widely recognised as one of the foremost technical experts on CBM in the world. He is currently an Adjunct Professor at University of Queensland’s Centre for Coal Seam Gas and Deputy Chair – Petroleum for Queensland Exploration Council. Kelemen also has extensive technical experience as a director at Galilee Energy (ASX: GLL) — which has more than doubled its share price since April on a successful drilling program at its Glenaras gas project.

Kelemen this week confirmed his confidence in Elixir, acquiring 290,000 EXR shares. He is also due to be granted 5 million Incentive Options that are exercisable once the share price hits $0.10.

Richard Cottee

As mentioned, non-executive chairman, Richard Cottee made his name running Queensland Gas (QGC) and is considered the “godfather” of coal seam gas in Queensland.

Cottee led QGC from a $20 million market-cap company with a share price of 20 cents through to its acquisition by British Gas for $5.8 billion ($6 a share) all in just six years.

Bayanjargal Byambasaikhan

Previously a strategic adviser to the company, Elixir last week appointed Mr Bayanjargal Byambasaikhan as a non-executive director.

Byambasaikhan chairs the Business Council of Mongolia, the country’s leading business association and has been an adviser to the President of Mongolia. He co-founded NovaTerra, an investment advisory firm based in Ulaanbaatar that has successfully advised on corporate and infrastructure project transactions and financings since 2013.

He brings considerable experience to Elixir, having managed and closed financing for high-profile energy transactions in Asia, including Mongolia’s first wind farm/independent power project in 2012.

In 2015-2016, Mr Byambasaikhan was the chief executive of Mongolia’s sovereign investment company, Erdenes Mongol, where he served as board director of Oyu Tolgoi LLC, and other subsidiaries.

Here Neil outlines his experience in Mongolia and the strength of the team:

Key takeaways as we head into drilling

There are some major opportunities not just for Elixir’s Nomgon IX PSC, but further afield in Mongolia to serve the growing clean energy sector in Asia into the future. While they offer huge potential upside, these longer-term opportunities are still far from investor’s radars.

What is in focus now are the upcoming catalysts for value creation, including the drilling results — due in late 2019, a contingent Resource assessment — scheduled for early 2020, a gas production pilot later that year, followed by a potential farm-out to a larger partner.

Since our last article on Elixir back in July, when it was named our Top ASX Energy Pick of 2019, the stock is up 30%, having gained as much as 67% when it hit 6.5 cents per share — a figure still well below K1 Capital’s 22 cps valuation, as mentioned above.

That said — and with considerable analysis behind it — the real action is only now about to start, with the spudding of the first well at the PSC and not long after some answers to the big question of what lies under the surface.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.