The IVZ Bidding War Has Officially Begun - Drilling in July

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 6,625,290 IVZ shares and 65,072 IVZ Options and the Company’s staff own 81,690 IVZ shares and 10,845 options at the time of publication. S3 Consortium Pty Ltd has been engaged by IVZ to share our commentary and opinion on the progress of our investment in IVZ over time.

Our 2020 Energy Pick of the Year, Invictus Energy (ASX:IVZ) is only a few months away from drilling the largest seismically defined, undrilled oil and gas structure in onshore Africa.

To get an idea of how big of a prospect IVZ is targeting, consider that the Bass Strait, which has supplied the majority of domestic gas demand in Australia for over 50 years, had reserves of ~10 trillion cubic feet (Tcf) at its peak.

IVZ, meanwhile, is targeting a gross prospective Resource of 9.25 TcF gas, plus 294m barrels of gas condensate (1.9 billion barrels of oil equivalent) - almost the same size. Of course, IVZ has a ‘prospective’ resource, and any discovery or proven resource will be smaller, however the numbers provide for some context on the elephant scale 9.25Tcf gas target.

The scale of the target is such that IVZ could make a meaningful contribution to Zimbabwe’s entire domestic gas supply, and maybe even export to energy hungry neighbours such as South Africa.

IVZ’s planned first well will drill down to 3,500m and pierce through six stacked targets in one go, with multiple multi-tcf prospects to test.

Yesterday, IVZ confirmed that well-pad construction had commenced.

And most importantly, IVZ confirmed it has now received THREE competing farm-in offers for the upcoming drilling program.

The three offers include an updated and improved offer from the current non binding farm-in partner, Cluff Energy Africa. While ongoing due diligence and internal approvals are being undertaken by additional parties.

The bidding war is clearly heating up, with so many parties wanting exposure to IVZ’s upcoming drilling event.

Those who have been following our coverage of IVZ will know that when we first covered the farm-in agreement with Cluff Energy Africa in December last year, we said it could prove to be like the “first bid at an auction”.

At the time, the significance of the deal being “non binding” showed that the deal was non exclusive and could be terminated by either party.

Our thinking was that as IVZ completed the 2D seismic data processing, generated additional drilling prospects and leads, the attractiveness of the project to farm-in partners would increase.

Yesterday’s news now confirms this thinking.

Since the signing of the non binding agreement with Cluff, a lot has changed and we suspect that this is why there are now three competing offers to farm-in to the project.

The two major developments at the project level are as follows:

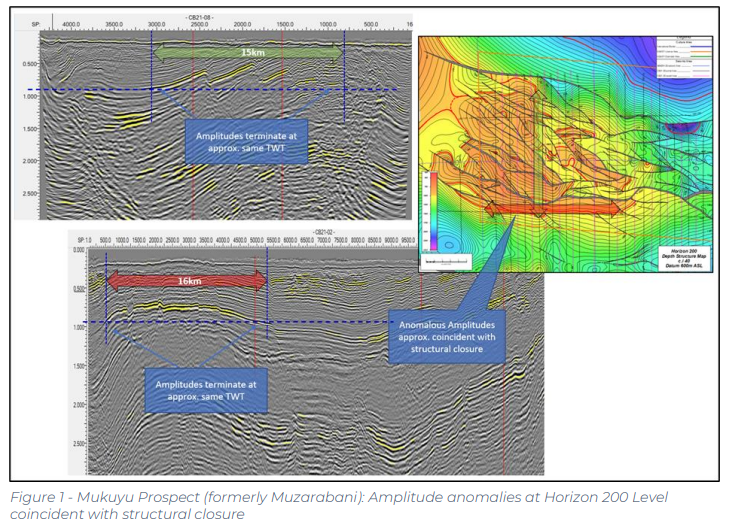

- 2D seismic data processed: Results confirm extensive seismic anomalies at multiple levels for the Mukuyu prospect, the identification of a substantial new shallow target measuring ~15km x 16km identified and more prospects and leads along the basin margin.

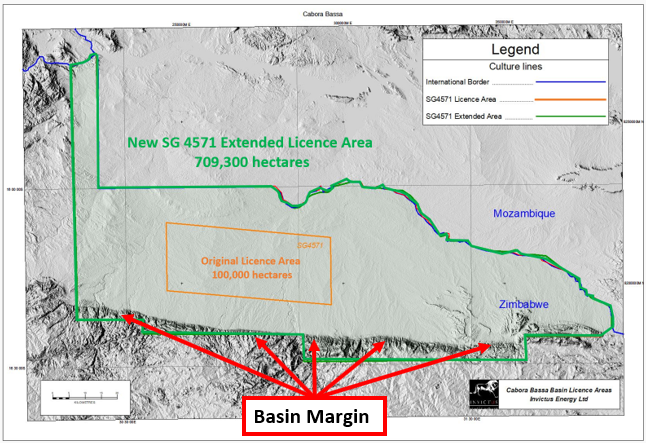

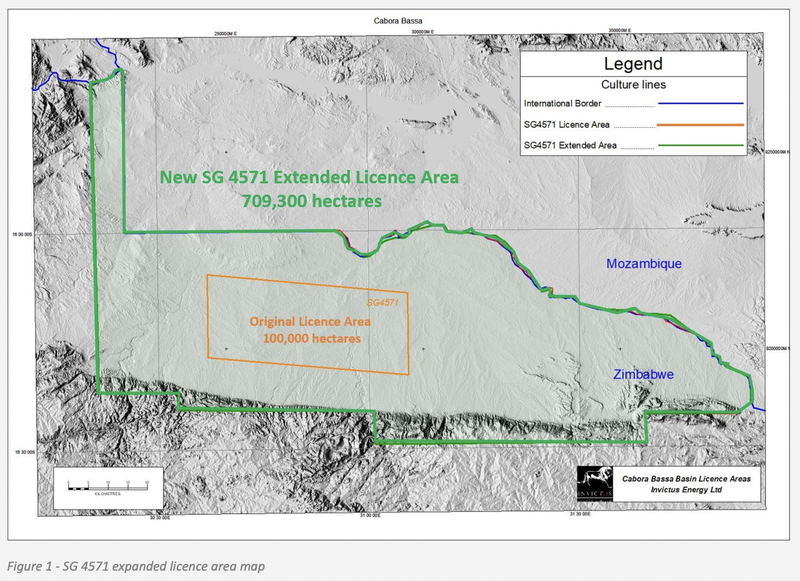

- 7x increase in project size: The project size has increased ~7x, from 100,000 ha to 790,300 ha, following the signing of a Heads of Agreement with Zimbabwe’s Sovereign Wealth Fund.

IVZ is now in a far superior position to negotiate with the three interested parties in the farm-out process.

Having more than one party interested will create an almost auction room style bidding war, which could yield IVZ the most favourable farm out terms.

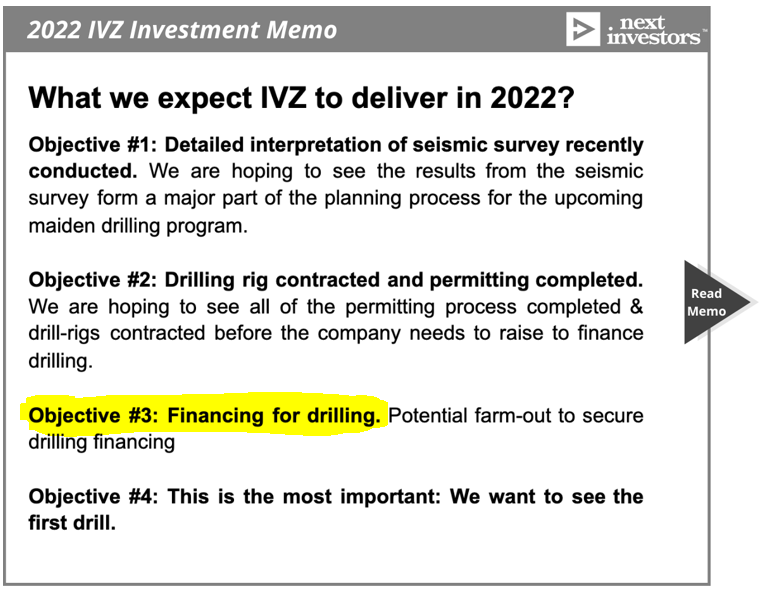

With the upcoming two well drilling program expected to cost in excess of US$12M, we set the financing of the drilling program as key objective #3 in our 2022 IVZ Investment Memo.

The farm-out process is a crucial step toward de-risking the financing of the upcoming drilling program.

We hope that IVZ can get a deal locked away in time for the July drilling program.

Yesterday IVZ also released an updated Investor Presentation, which gives a good summary of the company and what we can look forward to over the coming months.

So what’s changed since the first farm-in offer?

Towards the back end of last year, IVZ received the first farm-in offer from Cluff Energy Africa, a private partnership between UK based resources entrepreneur and oil tycoon Algy Cluff OBE, and British billionaire Lord Michael Spencer.

At the time, the deal was structured so that Cluff would contribute 33% of the drilling program's funding in exchange for a 25% interest in the project.

We covered that deal in detail in a previous note which can be read here: IVZ Commits to farm-in Deal with British Tycoons - But Maintains Open Relationship.

The market almost immediately reacted to the deal negatively, with the IVZ share price reaching 52 week lows at ~10c per share - an almost 20% drop off the back of that announcement.

In our note we emphasised that the market was missing the point that the offer was “non binding”, meaning that at any point IVZ could cancel the agreement and look to either farm out the project to an interested party with a more attractive farm out an offer, or simply raise the funds and go it alone.

We likened the deal to an opening bid at an auction, which we expected would increase the interest in IVZ’s project.

A lot has changed with the project since that first offer by Cluff and with yesterday’s news confirming there are now three separate interested parties with three separate farm-in proposals, it’s worth taking a look at exactly what those changes are.

First of all, IVZ has completed processing and analysed all of the 2D seismic data.

Just weeks ago, IVZ confirmed that the 2D seismic data (acquired data in 2020 for 840km) and the US$30M in legacy datasets leftover by Mobil had been processed and interpreted.

The 2D seismic data brought with it three major takeaways:

The first is the presence of extensive seismic anomalies at multiple levels for the Mukuyu prospect where IVZ were initially planning on drilling.

This confirms that IVZ was looking in the right area and that an oil and gas structure does seem to be present in this part of the project.

Alongside this, IVZ confirmed that it has found an additional shallower target in the same prospect measuring ~16km in strike length and ~15km down dip.

Importantly, both of these amplitude anomalies terminate at approximately the same time across all dips and strike lengths. IVZ thinks this could be the indications of a “trap”, which allows for pressure to build up and oil and gas deposits to form over millions of years.

Finally, the seismic data also threw up an extensive array of prospects and leads along the basin margin.

The seismic data confirmed that these prospects demonstrate similar seismic anomalies, but the prospects need to be further analysed before they could be added to the upcoming two well drilling program.

IVZ is now in the process of firming up the highest priority target from these prospects along the basin margin. It is planning this as the second well in the two well drilling program this year.

These new prospects/leads is that the project’s future exploration potential is significantly improved.

These prospects mean that IVZ doesn't get only one attempt at a major discovery. If the first well is not successful and no discovery is made, IVZ gets a second chance at making a discovery.

On the flipside, in the event of a discovery, IVZ can look to expand its resource size by drilling these new leads.

To see our commentary on the significance of a basin margin check out our previous note here.

The second major change at the project level relates to the signing of the Heads of Agreement (HOA) with the Zimbabwe Sovereign Wealth Fund:

The HOA, signed ~30 days ago, has led to an increase in the overall project size from ~100,000 hectares to a total of ~709,300 hectares.

IVZ now controls 700%+ more ground - a massive upsize in the scale of the project:

There were three other key takeaways from IVZ’s HOA with the Sovereign Wealth Fund of Zimbabwe outside of the increase in project size.

1 - Second well before June 2024:

Changes to the work commitment — in this second stage of exploration, IVZ has committed to drill a second well before June 2024.

IVZ has already fast tracked this and it is planned for inclusion in this year's drilling program.

2 - 10% back-in-right for Sovereign Wealth Fund:

The negotiation of a 10% back-in-right is effectively a right of first refusal for the Sovereign Wealth Fund to take a 10% free carried interest in the event of a discovery being made.

Effectively, IVZ would lose a 10% equity interest in the project in exchange for having the Sovereign Wealth Fund involved as a partner in the project.

We think that the 10% equity interest is acceptable, given it brings the government into the project as an equity partner and in the event of a discovery, the parties' incentives are aligned to commercialise the project.

Projects like this, which have basin unlocking potential, can only be commercialised with government support around infrastructure development and assurances. That would make it particularly interesting to a farm-in partner as the project is essentially de-risked from a government perspective.

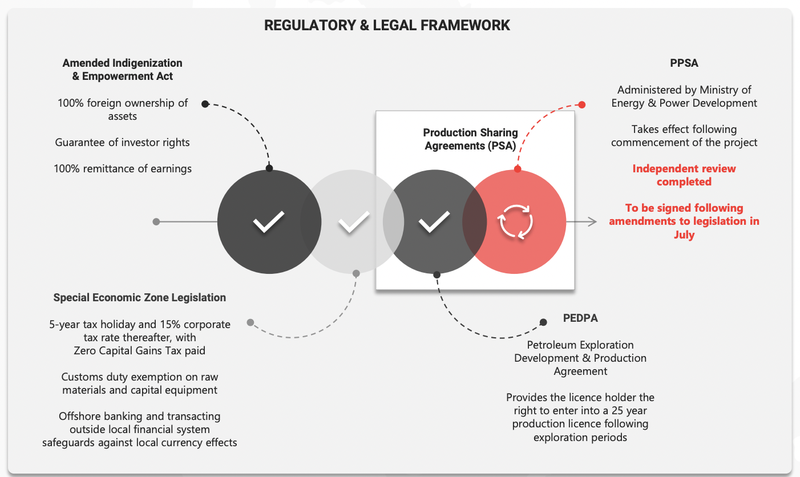

3 - PSA negotiations complete:

Negotiations over the Production Sharing Agreement are complete pending final governmental approvals.

The signing of the Production Sharing Agreement is effectively the final stage of permitting before IVZ has certainty around tenure, along with having fiscal and legal frameworks in place, in the event of a discovery when drilling begins in July.

Progress on this front would be of particular interest to potential farm-in partners who want to see a firming up of the permitting situation behind the projects before committing to a farm-in deal.

Bringing all of this together:

IVZ has completed all of the 2D seismic processing work — technically de-risking the project and making it a more attractive exploration prospect on a risk reward basis.

This is significant as farm-in partners who generally do a lot of technical due diligence before committing to a farm-in agreement would now be far more comfortable committing capital to the project.

IVZ increased its project size by over 700% and has brought in the Zimbabwe Sovereign Wealth Fund as a project level partner, de-risking the project from a permitting, political and permitting perspective.

Again a potential farm-in partner would see this as a major de-risking of the project, while the progress on the production sharing agreement would also increase their comfort in committing capital to the project.

What’s next for IVZ?

Heads of Agreement to be approved by Zimbabwe Government 🔄

IVZ is now waiting on formal governmental approvals for both the Production Sharing Agreement and the approval over the extended acreage position. The terms of the HOA with the Sovereign Wealth Fund are clearly set out so we expect this to be a formality.

Final drilling locations confirmed 🔄

With yesterday’s announcement, IVZ confirmed that the well-pad construction had commenced for the first well, which we suspect will target the highest priority Mukuyu prospect.

We still want to see IVZ rank its highest priority target for the second well in its upcoming two well drilling program.

IVZ points to this being at one of the basin margin prospects.

Farm-in agreement to be signed 🔄

IVZ now has three separate offers to farm-in to its project to help finance the upcoming drilling program.

The existing agreement with Cluff Energy Africa was expected to expire on 30 April ( the end of this week).

Given the new competing offers, including the new offer from Cluff, this expiry date isn't as relevant anymore.

Instead, we hope to see the three competing parties (and maybe more) bid it out to try and get a piece of the project ahead of drilling in July.

As there is still some time until drilling, we hope to see more interest in the project and for these parties to aggressively compete to farm-in.

Financing the now two well drilling program 🔲

The farm-in agreement will likely form the basis for IVZ’s upcoming financing needs.

As IVZ has now committed to a two well drilling program, we suspect the drilling costs will be higher than the previously estimated US$12M.

IVZ has a current cash balance of ~$7.35M. This isn‘t enough to solely fund the drilling program and we are yet to see what the new competing farm-in offers look like.

If the farm-in offers aren't funding a large proportion of the project, IVZ will likely need to look at securing more financing via another capital raise.

What comes from the farm-in agreement will give a better indication of IVZ’s own financing requirements.

The major catalyst - Drilling in July 🔲

IVZ has now started constructing the wellpad for the first well.

This is encouraging and the first sign that this drilling program is really happening since we first invested back in September 2020.

We expect to see some more site images over the coming weeks and months leading up to the July spudding.

Our IVZ Investment Memo for 2022

Below is our 2022 Investment Memo for IVZ where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations 12 months from now.

In our IVZ Investment Memo you’ll find:

- Key objectives for IVZ in 2022

- Why we invested in IVZ

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.