Insights from Industry Leaders at IMARC

Published 02-NOV-2024 13:26 P.M.

|

17 minute read

- Commentary: From the floor at IMARC - Sentiment is up. Precious metals hot, battery metals not so hot. The least exciting placements can often be the ones that deliver. Minas Gerais government delegation in Sydney. A balanced view on the gold price. New: our quarterly Portfolio update.

- Quick Takes: PUR, EMD, 88E, MTH

- This week in our Portfolios: ONE, AL3

A few of our team was in Sydney this week for the IMARC conference, and to hear from some of our Portfolio Companies.

IMARC is the largest mining conference in Australia - so the big mining companies show up, but also well attended by small cap companies and investors.

The sentiment “vibe” is definitely improving, something we’ve been observing and pointing out in recent weekend editions.

Conferences are a great place to talk to CEOs, brokers, corporate advisors, investors and fund managers to get a feel for the general mood out there in the small cap markets.

The small cap markets are of course driven by the net average of the collective emotions felt by its participants.

Fear or greed.

“FOMO” or “happy to watch from the sidelines”.

Precious metals gold and silver are definitely the talk of the town at the moment.

Battery metals... not so much.

But we’re also conscious of how commodities cycle in and out of favour.

Riding waves of positive then negative, then positive sentiment.

And rewarding the patient.

...or the counterintuitive?

For example, battery metals stocks have been beaten down for the last ~2 years.

With gold and silver running, some decent battery metals stocks at all time lows are getting even further sold down.

Why?

Many patient battery metals investors will likely have been presented with a hot new gold/silver placement...

And when they look through their portfolio, thinking about what to sell to fund it, it’s probably one of their forgotten 2020 battery metals stocks first on the chopping block.

(admit it - you’ve probably thought about it too)

Putting more pressure on as the few remaining battery metals hold-outs finally capitulate to cycle into shiny silver and gold.

Even the coverage across the mainstream media of the “EV Revolution” has deflated in favour of wall to wall coverage of the US election, wars and inflation.

So is this the final bottom for battery metals stocks before the turn around?

We think it could be... and we’ve been adding to our positions in our battery metals companies over the last few weeks.

We’ve noticed a few headlines creeping in around electric vehicle sales:

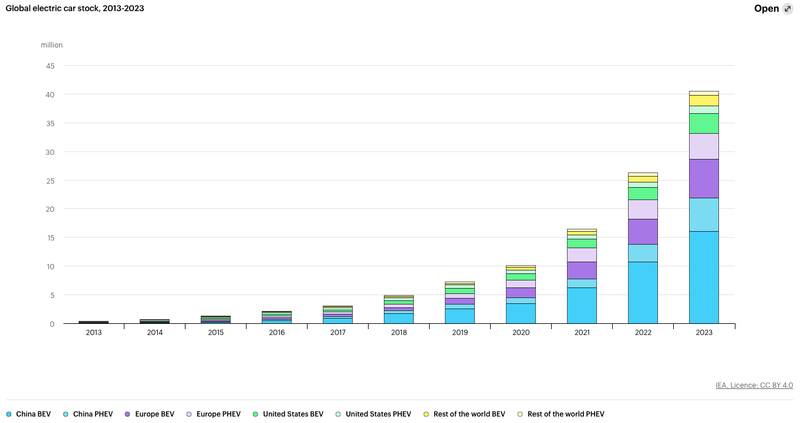

After the heat of expectations of sudden EV takeover back in 2020-21 cooled over the last 2 years, the number of EV sales has actually been quietly growing:

(Source - IEA Trends in EVs)

Last year there were 75 million new cars sold, and only 18% of those were EVs.

So there is still plenty of growth to come.

It may take a bit longer than everyone thought back in 2020, but as more EVs are sold more battery metals are needed.

We talked about how battery metals prices may need to cycle up again in the medium term to attract another batch of funding into battery metals juniors to kick their projects into the next development phase.

We discussed what a potential lithium comeback could look like a few weeks ago here.

We have also seen Rio Tinto throw its hat in the ring for a “bottom of the market” acquisition of Arcadium Lithium for US$6.7Bn.

COP29 starts in two weeks time in Azerbaijan and we will be watching to see if “critical minerals” or “battery metals” is on the agenda.

So battery metals stocks are beaten down, EV sales are rising and there are a few sniffs of an improvement in sentiment...

We have been participating in the capital raisings that our battery metals stocks have been doing (at lower prices to our Initial Entry Price to average down on our position) in anticipation of a return of sentiment.

In the last month we have participated in placements/increased positions in our lithium brine hopefuls PUR, PFE and MAN.

As a case study, one of our most successful “while sentiment was at rock bottom” placements we participated in was back on the back end of the biotech lull.

When nobody wanted to hear about early stage biotechs, our Portfolio company DXB ran low on cash and launched a heavily discounted placement, with TWO attaching options and a convertible note.

Even though at the time it was a hard one to agree to, we put in a little bit of cash to support the company while it was down.

(we wish we did a lot more, easy to say in hindsight but at the time it was hard to press the “transfer funds” button)

A few months later DXB announced a significant commercialisation deal and went up nearly 10x over the next 10 months:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Now this was an example of when it worked out, it’s certainly not the expectation.

At the very same time we also participated in another “hard to get excited about” placement to support one of our other early stage biotechs BOD, which went into administration a little while later after the raise ultimately didn’t complete.

So it can go either way for these “bottom of the market” investments.

But our high-risk, high-reward style of investing means that we only need a few outsized winners to make up for the portfolio losers.

This worked with DXB during the biotech bear market, we are betting that averaging down in our battery metals Investments will work out when battery metals cycle back up again.

Brazil’s Minas Gerais is the place to build a mine - we have 3 Investments there...

Back to the conference in Sydney - we attended a session on the side of IMARC called the “Brazil Mining Lunch” which was hosted by Jane Morgan Management.

One of our best ever Investments presented - Latin Resources (ASX:LRS) which is a lithium development company located in Minas Gerais.

LRS made a lithium discovery in early 2021 and rapidly defined a lithium JORC Resource.

Earlier this year LRS announced an offer to be acquired by $8.7Bn capped Pilbara Minerals for ~$600M.

After our success with LRS we looked for other investments in the Minas Gerais region including L1M and SGQ.

In addition to LRS, both L1M and SGQ presented at this event.

The first speaker was João Paulo (JP) Braga the president of Invest Minas - the organisation is Minas Gerais State Government's investment promotion agency.

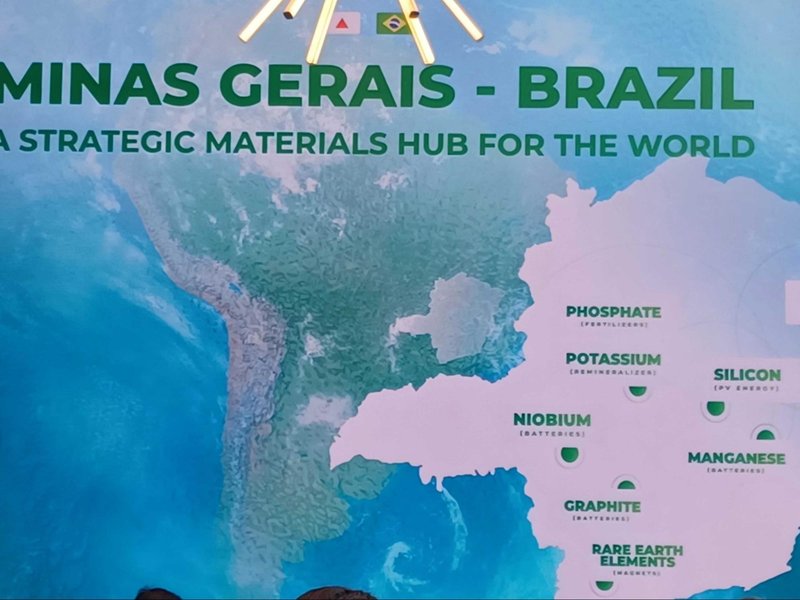

Below are some of the reasons Minas Gerais is a mining powerhouse:

JP is incredibly passionate about bringing mining business to this part of Brazil - which is positioning itself to become a strategic minerals hub exporting to the wider world:

If you look closely you can see some of the materials that we Invest in.

Again, we have three Investments in Minas Gerais in Brazil, who were all speaking at this event:

Latin Resources (ASX: LRS) - Lithium developer, one of our best Investments ever, in process of completing acquisition by ASX lithium heavyweight Pilbara Minerals

Lightning Minerals (ASX:L1M) - Lithium explorer, seeking to replicate the success of LRS by making its own lithium discovery, in close proximity to LRS.

St George Mining (ASX:SGQ) - Niobium (and rare earths) developer, which is acquiring a project right next to the largest supplier of niobium in the world.

Each speaker noted how strongly supportive the state and local governments have been in ensuring their projects could advance as quickly as possible.

LRS’s Chris Gale, for instance noted that LRS was able to achieve what it has in Minas Gerais, in roughly a third of the time it would take to make the same amount of progress in Western Australia.

L1M’s Alex Biggs repeated a couple times how, thanks to government support and good access to local labour and skilled geologists, L1M’s exploration efforts cost a third of what they would in Western Australia.

Meanwhile both L1M and SGQ formalised their relationship with Invest Minas, by signing an MoU which outlines how these two companies will work with Invest Minas to advance their projects:

- Licensing - think fast tracked drill permits and the like

- Environmental approvals - Invest Minas provides support in ensuring environmental approvals move quickly through the process

There were signing ceremonies at which these MoUs were established.

Below is L1M’s Alex Biggs with Invest Minas:

And SGQ’s John Prineas with Invest Minas:

With these agreements in hand, we think it all adds up to Minas Gerais being a great place for critical minerals projects to get off the ground and quickly churn out results and newsflow.

Gold and silver at IMARC

We caught a session at IMARC presented by ABC Refinery’s Nicholas Frappell who is the Global Head Institutional Markets at the company.

ABC Refinery refines roughly 50% of the gold in Australia - so it is a big player in the domestic gold market

(for anyone out there who holds physical gold or silver, chances are you'll have an “ABC bullion” stamped item in your collection).

It is a division of Pallion which is the largest precious metals services group in Australasia.

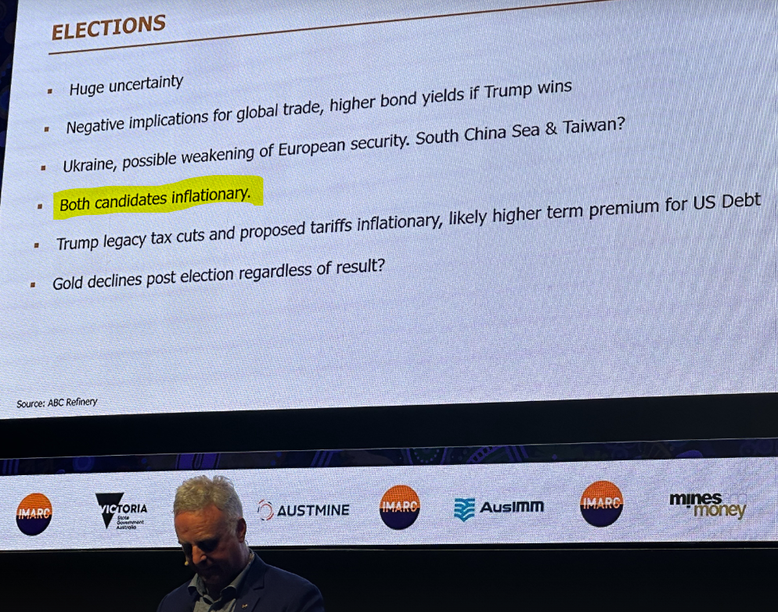

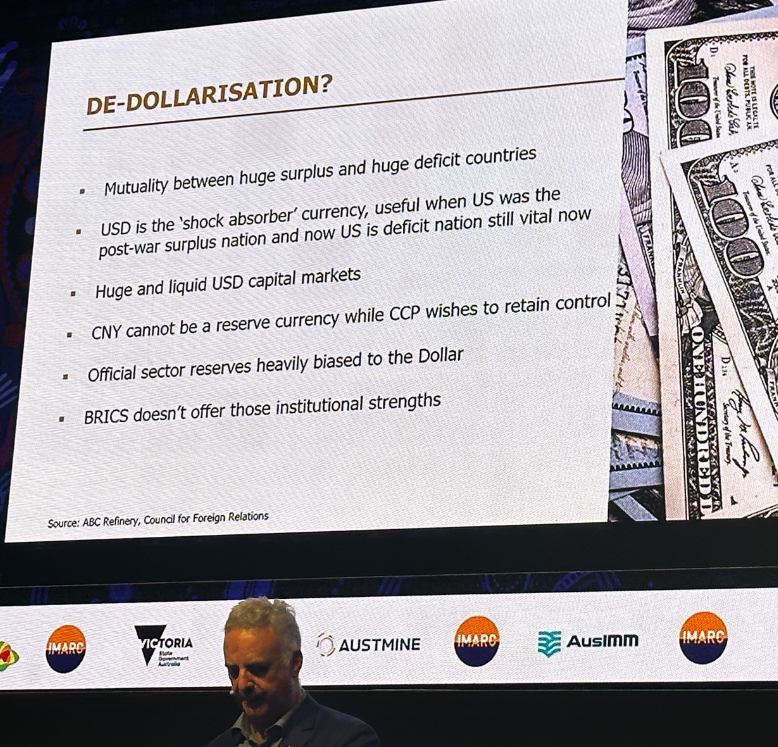

Now there are a lot of “spicy” theories out on the internet about why gold and silver prices have been moving up.

Frappell is in the physical precious metals industry and shared some great balanced insights on what he thought is (and is NOT) driving precious metals prices.

The environment for gold and silver remains strong in the long-term, according to Frappell.

Frappell's views were that the reasons for the recent upwards moves in the gold price were more due to:

- Inflation (gold remains the classic hedge)

- US elections (uncertainty)

- US rate cut (adds more fuel to inflation)

- US government debt (tied to US dollar fluctuations)

- Ongoing wars (particularly Ukraine)

He was NOT convinced that golds price rise was being driven by

- A “move away from US currency as the global reserve” and/or

- A BRICS currency as competitor to the US dollar

Frappell’s views are in contrast to some of the more extremely bullish opinions on gold out there.

So we thought it was a good balanced view on the markets from an industry insider.

It also made us feel more confident about some of our latest Investments, continuing their runs.

Some of the best performers in our Portfolio this year have been gold and silver companies:

Here are the highlights:

- Mithril Silver and Gold - high point of 715%

- Sun Silver (ASX: SS1) - high point of 582%

- Titan Minerals (ASX:TTM) - up ~100% year to date

Meanwhile our latest precious metals Investment could benefit from all time high gold prices as a current producer: Kaiser Reef (ASX:KAU).

We’ll be watching KAU’s progress closely as the company starts to mine fresh high grade ore at depth - and processing it immediately to sell into high gold prices.

What ties all these companies together is that they are all to varying degrees, later stage.

These aren’t complete exploration rolls of the dice - they all have defined JORC resources, but are continuing to grow their resources, delivering high grade exploration assays at a time when market sentiment rewards these results.

We’ve mentioned previously how it seems to take time for capital to roll downhill from the big cap producers, then to mid-caps (smaller producers, developers and the like) and then finally to small caps (often explorers, but we’ve managed to Invest in some more advanced small caps).

So the above results across our precious metals Investments appear to be well timed.

Something underlined by the recent strong placements done by a couple of these companies to large institutional investors (see Jupiter Gold and Silver Fund for MTH and Nokomis Capital for SS1).

We’ve also been doing a bit of reflection on our previous Investments and improvements on how we communicate about our Investments going forward.

Here’s more on that.

Quarterly Portfolio Update

It has been almost 5 years since we launched our Portfolio Model - in that time we have seen a bull market, bear market and some successes and disappointments.

After 5 years, many of our early positions have run the course of our minimum hold period - some have succeeded, some are still trying and some have failed.

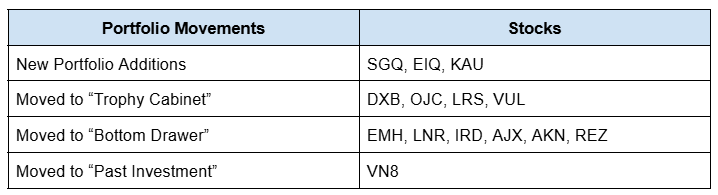

To better communicate the status of each of our Investments, we are introducing some new terminology that we will use in our Quarterly Portfolio Update and on the Portfolio table on our home page.

This update will be done quarterly and we will report on any changes to the status of our Investments in our Portfolios.

We have also renamed our “Finfeed” Portfolio to “Next Biotech”.

Definitions

📢 Active Mandate - A Portfolio Company that we have an active contract with to share our commentary (companies listed with a loudspeaker next to them).

Bottom Drawer - A Portfolio Company that has not delivered on our Investment Memo objectives in a reasonable timeframe, or a key risk has materialised. We hold a position in the hope that it may eventually deliver a surprise outcome or acquire a new project OR we may look to exit these positions to free up capital for new Investments.

Current Investment - A Portfolio Company that we hold a position in and are interested in the company.

Past Investment - A Portfolio Company that we no longer hold a position in.

Portfolio Company - A company that has been added to one of our Portfolios (Next Investors, Catalyst Hunter, Next Biotech, Wise-Owl, Emerge).

Trophy Cabinet - A Portfolio Company that has exceeded our expectations and either delivered on our “Big Bet” OR delivered an outsized return during our minimum hold period. The company will either continue as a Current Investment OR we may eventually exit the position.

(for other general definitions and see here)

Portfolio Update FY2024/25 Q1:

Here are the category movements for this quarter:

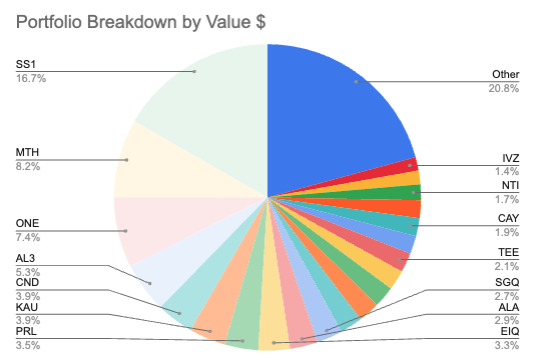

Our top positions by $ value:

If at any point in time you would like to see our holdings in more detail click here - this link can also be found on our “trust centre” page under “our holdings”.

We will aim to put this regular update out each quarter and provide you with updates on the positions in our Portfolio.

Updated hold conditions

Our strategy as Investors is to hold our Portfolio positions for long enough to give the company time to execute on its strategy, as outlined in our Investment Memos for each New Portfolio Addition.

Our minimum hold conditions and de-risking conditions can be found on our website here.

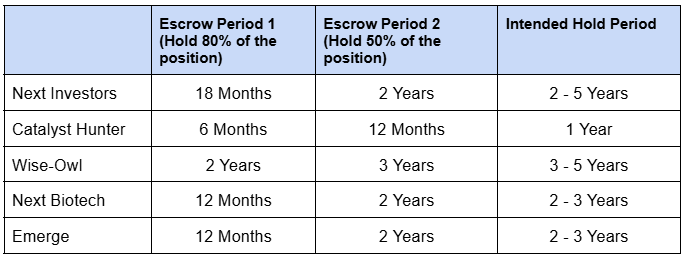

We are updating our minimum hold conditions for New Portfolio Additions.

Our original minimum hold conditions below still continue to apply to our current Portfolio companies:

Trading Blackouts and hold conditions:

- Hold 100% of a position for 90 days after initial coverage has been initiated (portfolio launch).

- Hold 80% of the position for 2 years after initial coverage has been initiated.

- Hold 50% of the position for the mandated investment time frame by portfolio:

- Next Investors: 3 to 5 years

- Wise Owl: 4 to 7 years

- Catalyst Hunter: 2 to 3 years

- Finfeed: 3 to 5 yearss

- Do not trade in a stock for 3 days after an investment update is sent about that stock.

De-risking (Sell) Conditions:

Our investment strategy involves partially de-risking positions after a company delivers certain milestones that re-rate the share price. De-risk conditions are:

- If the company has released at least 3 material announcements and the share price has re-rated 300% - we can de-risk/take profit by selling a maximum 30% of the total position.

- If the company has released at least 6 material announcements and the share price has re-rated 500% - we can de-risk/take profit by selling a further 30% of the total position.

For New Portfolio Additions going forward, changes to the minimum hold conditions are as follows:

As today is the first update it is a bit of a long one, but in future these updates will generally be shorter with any other notices from the quarter included.

What we wrote about this week 🧬 🦉 🏹

Oneview Healthcare (ASX:ONE)

This week, our health tech Investment and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) released its quarterly report.

Revenues were up 191% on the same time last year.

We aren't going to jump up and down too much about this because it was mainly from delayed payments from last quarter that have been recognised in this reporting quarter.

BUT...

What really grabbed our attention is the announcement of a 2 year extension to ONE’s “value added reseller” agreement with the US$18BN hospital bed and medical device supplier Baxter International.

Read: US$18BN Baxter extends US reseller deal with ONE, expands to Canada.

Oneview Healthcare (ASX:ONE)

This week, our health tech Investment and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) released its quarterly report.

Revenues were up 191% on the same time last year.

We aren't going to jump up and down too much about this because it was mainly from delayed payments from last quarter that have been recognised in this reporting quarter.

BUT...

What really grabbed our attention is the announcement of a 2 year extension to ONE’s “value added reseller” agreement with the US$18BN hospital bed and medical device supplier Baxter International.

Read: US$18BN Baxter extends US reseller deal with ONE, expands to Canada.

AML3D (ASX:AL3)

AML3D (ASX:AL3) reported its quarterly results this week.

Off the back of signing Master Licencing Agreements (MLA’s) with the US Navy and Boeing Defence and Space earlier in the quarter.

Receipts from customers are up 16.5% on this quarter last year to $2.75M.

Operating cash burn was reduced to just $0.38M, leaving it with a cash position of $6.85M - that's a long 18 quarters of runway at current burn rates.

When we consider the list of major companies queuing up to use AL3’s tech this number is impressive.

Read: Global defence spending up, AL3 revenue up, US sales up.

Quick Takes 🗣️

EMD also secures ethics endorsement for psilocybin use

PUR published results for second drill hole over its lithium project.

88E seismic update & neighbour drill results weeks away...

MTH $12.5M capital raise supported by cornerstone investors

EMD partners with University of WA on novel Serotonin-Releasing Agent

Macro News - What we are reading & listening to 📰

Gold:

Investors’ ‘fear of missing out’ drives gold demand to record high (FT)

- Investor demand for gold surged to a record $100bn in Q3, driven by "FOMO" and geopolitical concerns.

- Central banks cut purchases, while wealthy individuals bought more for wealth protection.

Putin's Dollar-Primacy Challenge Runs Into Trouble (Bloomberg)

- Post-WWII, the dollar became the global monetary anchor, despite Keynes's vision of a more balanced system.

- Challenges like Russia and China’s mBridge and the digital yuan have struggled to displace the dollar, keeping it central in global finance.

Silver:

Five Major U.S. Banks Face Billions in Losses as Surging Silver Prices Pressure Short Sellers (The deep dive)

- Silver prices spiked nearly 8% in October, exceeding $33.60/oz, leaving major U.S. banks facing $1.3 billion in losses on short positions.

- High demand and speculation are fueling this surge, with First Majestic launching a silver mint to offer direct bullion access, potentially easing futures market pressure.

What we are watching:

Alasdair Macleod & Dominic Frisby on GOLD, BRICS and CREDIT

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.