Can ONE deliver contracts as we emerge from the 2022 tech wreck?

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 8,195,000 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

The tech wreck of 2022 saw mega-cap to small cap tech share prices take big haircuts.

In response, nearly every tech company switched focus to preserving capital, reducing costs and showing profitability, until tech sentiment turns.

With tech share prices beaten down, recent earnings calls and financial reports have seen the market reward tech companies that have adapted, survived and emerged stronger.

Those that got the foundations right.

This means cutting costs, keeping existing customers and closing more deals.

So they can expand aggressively when the time is right.

Our healthtech Investment, and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) released its latest quarterly today and it showed us how ONE has adapted during a tough time for tech.

At its core, ONE is a tech company that uses cloud technology to provide hospital patients a “virtual care and digital control centre” at their bedside that delivers the best possible patient experience during their stay:

With its powerful data insights and analytics, it saves hospitals money as well.

But over the last 12 months tech stocks went through the wringer, and ONE’s experience has been no different.

ONE’s share price was happily trading around the 40c mark for most of 2021, then in 2022 got swept up in the broader tech malaise and is now sitting at around 10c.

A great move and some good fortune from ONE was raising $20M at 23c literally weeks before the tech crash (we participated in this placement) - having cash during a tough financing environment is critical.

From the current 10c base, we think a couple of the delayed, material contracts the market expected last quarter will be well received if ONE can deliver them in the next few months.

The tech heavy NASDAQ is up 11% in the first four weeks of this year, so with the potential green shoots for tech stocks showing up in the market after this recent tech “winter”, we think now is the time to re-examine what remains one of our favourite tech Investments.

In this context, here are our quick takeaways from the ONE quarterly:

- Appropriate belt tightening - ONE reduced its workforce (like nearly all tech companies did) and expects cost savings €2.0M (A$3.1M) over 2023. Staff costs were down 13% compared with the September quarter as well. This led to an acceptable net operating cash outflow of €0.6M (A$951K).

- Receipts uptick on last quarter - €3.7m (A$5.8m), this was up 62% on last quarter. Granted, this was still down on their record quarter from the same time last year (€5.5M).

- Strong customer retention, leading to expansion - we note that key customer NYU Langone signed an expansion contract for 1,000 beds to deploy in the next six months. That should help take ONE past the 15,000 beds we wanted to see it hit in 2022.

- Sales pipeline still growing - on the back of lots of interest from hospitals stretched by the pandemic, ONE added RFP requests for a further 4,358 beds during the quarter. This sales pipeline is maturing with ONE being “selected as vendor of choice” for two new US health systems for a minimum of 2,150 more beds. In this tech climate, we think new investors are waiting to see ONE convert this pipeline into contracts and revenue, in the near term.

All up, we think this was a solid quarterly for ONE given the macro circumstances, and it should set the company up nicely if it can continue to close deals.

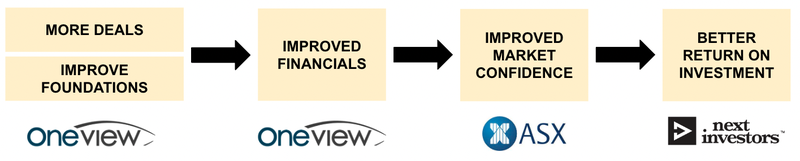

Here’s how we think ONE’s strategy can work for us in the current tech environment in simple form:

Note: this is our view of ONE’s strategy, and we made this image, not ONE.

To put some numbers around ONE’s progress - there was a key update in this quarterly:

“[ONE] added €22.4m (A$35m) in new TCV [Total Contract Value] sales from existing and new customers in 2022.”

Annual Recurring Revenue (ARR) is the yearly cost to licence ONE’s software, and is reported to the top line in the year that it is used.

Total Contract Value (TCV) is the ARR multiplied by the number of years a contract is signed for, plus the value of any other services included in the contract - in other words the total value over the life of the contract.

These TCV sales will gradually show up in the coming year and subsequent years over the life of contracts as ONE firms up its Annual Recurring Revenue model (ARR) - where cashflow is smooth and attractive for investors.

ARR is a metric that forms the backbone of “subscription economy” companies.

And ARR forms the basis of our Big Bet for ONE.

Our ONE Big Bet:

ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1BN valuation (based on 5x to 10x forward ARR multiple) and be acquired by a large health tech provider.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

To see how ONE is going against our Big Bet - we’ve got a Progress Tracker which provides a quick summary of ONE’s progress since we Invested:

See our ONE Progress Tracker

It only takes a few minutes to scroll the ONE Progress Tracker to get a quick helicopter summary of its progress, something that we find helpful to do before reading each new ONE announcement.

A quick scan of the Progress Tracker helps give context to how new announcements contribute to our Big Bet and near term Investment Memo objectives for ONE.

How ONE’s quarterly tracks against our Investment Memo

There was no update on the precise number of beds, but we think ONE is just shy of the 15,000 beds we wanted to see the company have by the end of 2022.

Revenue growth has been slower than hoped for, however, the €22.4m (A$35m) in new TCV [Total Contract Value] sales from new and existing customers in 2022 gives us big hopes for the future.

In its half yearly report from August last year, ONE revised its 2022 revenue guidance from a range of €12.5 to €14m (~A$18M - A$21M) down to €9 to €9.5M (A$13M - A$14M).

With €8.8M ($12.2M) in receipts for the year ONE is in the vicinity of its lower bounds of guidance.

We believe this is because key deals in the pipeline that were expected to achieve guidance were delayed - hopefully we will see them land this quarter.

But when the ONE deals do come through, they are often material and for a long time.

In hindsight, it's probably better timing that the deals were delayed, because most positive news from tech companies was not being rewarded by the market during the peak of the tech wreck in 2022.

We have seen ONE successfully sign five and six year deals with Epworth HealthCare (Australia) and the BJC HealthCare network (USA), respectively.

So again, it’s encouraging to hear that there are two new healthcare systems “currently in contract negotiations” for a minimum 2,150 beds with ONE as “the vendor of choice”.

What we’re looking to see is ONE announce a couple more material deals into an improving tech macro tailwinds.

But until those tailwinds return, it's important for ONE to keep the foundations sturdy - which is why the belt-tightening (reduction of workforce costs) had to happen, like it did for nearly every tech company during 2022.

Put another way, prudent use of money isn’t as exciting as a big deal, but both can be equally significant when the broader market conditions aren't helping.

Sales pipeline still looks strong

As we said in our last note, we outlined how ONE had added 5,216 beds in 18 months, compared to taking 13 years to add the first 9,259 beds.

That’s an important inflection point for the company.

A lot of this growth has to do with the strains felt by the US healthcare system during the pandemic (ONE’s primary target market).

Hospitals are reaching out to ONE directly, looking to improve their care delivery systems, and despite the slow pace that these hospitals move at, it looks like ONE is on the cusp of sealing a couple big deals.

The sales pipeline in the US looks strong - ONE added more RFP requests for a further 4,358 beds during the quarter (read more on RFPs and RFIs here).

RFIs and RFPs are formal processes for evaluating ONE’s tech for implementation in a hospital.

The key for ONE is converting this interest in the sales pipeline into contracted beds and ultimately revenue.

We think a contributor to ONE’s current share price of ~10c is that the market had been expecting the deals by the end of 2022, and when they didn’t arrive the stock was sold down. We beleive the reverse will occur if the deals do come though in the next few months.

Marketing spend was below the levels that we would have liked to see at the time of writing our ONE Investment Memo in January 2022 - before the 2022 tech wreck played out.

Instead ONE has responded to the change in the macro environment and put in place cost cutting programmes which includes downsizing of the company’s office footprint and a workforce reduction program.

Almost every tech company adopted this tactic in 2022, reducing marketing spend until capital market and purchaser (customer) conditions improved.

The overarching ambition is to see ONE reach cash-flow breakeven, something that is even more important now considering where interest rates are and the difficult conditions for tech companies to raise new capital at decent valuations.

In hindsight, aggressively spending on sales and marketing made sense to us in January 2022, now with the economic environment where it is we like that ONE is adapting its strategy and hasn’t hesitated despite its cash balance being relatively strong at $10M.

ONE expects the full impact of the cost savings program to be felt in Q4 - meaning cash flows should improve from here (assuming big deals get over the line, see risks section).

We mention in our 2023 tech outlook that a major risk for the sector is “availability of capital” meaning tech companies with high cash burn find it difficult to raise new capital and share prices are punished as a result.

Again, a great move and some good fortune from ONE was raising $20M at 23c literally weeks before the tech crash (we participated in this placement) - having cash during a tough financing environment is critical.

We like that ONE is moving to address this risk by focusing on transitioning the business to a position where it can be as close to, if not at cash flow breakeven in a matter of months.

Check out our 2023 tech outlook here.

We note that ONE has provided limited updates on these partnerships. Partnerships like this usually take a while to get moving which may mean that ONE has to do most of the heavy lifting for sales in the near term, perhaps due to the complex nature of closing deals with slow moving US healthcare systems.

ONE noted in this quarterly the use of Android Set Top boxes for a client, OU Medical, that will begin installation early this year.

Lots of hospitals have this legacy hardware in the US healthcare system.

In the half yearly conference call last year, we heard ONE CEO James Fitter say there were 7,000 beds in its network that needed coax set top boxes in 2020.

We expect as the sales pipeline expands, the set top boxes will continue to be important.

These make it easier for ONE to sell its service into older hospitals who would otherwise need to upgrade their existing infrastructure so that it is compatible with ONE’s technology offering.

The “coaxial set-top boxes” help to solve this issue by getting rid of the need for these hospitals to invest in expensive infrastructure.

While ONE hasn't provided any specific update on how this is impacting sales, we expect this to be a fundamental improvement in ONE’s pitch to potential new customers & for its value proposition going forward.

With eight significant bid proposals submitted in the December quarter alone we are hoping an improved product offering leads to converted sales.

Risks

Here are the risks we are most conscious of for ONE at the moment and they are all closely linked:

With sales risk - there’s always a chance the deals fall through.

Competition risk is ever present for ONE - the company isn’t alone in the US healthtech market and this is linked to sales risk.

ONE has a cash balance of €6.4M ($10M) at the end of the 31 December 2022 reporting period. If big deals don’t close and revenue drops off further, that would eat into ONE’s cash balance, perhaps precipitating a capital raise down the track - this is a risk for most small cap companies.

One risk that we did not predict was “macro theme” risk - namely the tech crash which took most tech stocks down with it, until sentiment turns positive again and they rebound. We will include “macro theme” risk in all future memos.

So with the risks in mind, we are excited to hopefully see ONE deliver on its promised contracts in the near term coinciding with continued improving sentiment in the tech sector, and deliver a re-rate off the current 10c base

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE

- Why we invested in ONE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.