Big Movers and Key Trends Uncovered

Published 08-FEB-2025 17:53 P.M.

|

21 minute read

- Commentary: China’s latest export controls on defence minerals, hedges leading to “risk on” market? Our analyst report from Mining Indaba conference

- Quick Takes: 88E, SGQ, CAY, EMD, IIQ

- This week in our Portfolios: JBY, L1M

Markets were action packed this week.

Some highs, some lows and a lot of jockeying by investors and governments around defensive assets and defence minerals.

We think this could be how a new wave of more “risk on” fervour eventually forms in the market.

Today we’ll explain how we think this could play out.

First though, the big news was this:

US President Donald Trump's wave of tariffs against China led to retaliatory export controls on defence minerals.

(Source)

Previously the market lingo was “critical minerals” - this has now increasingly shifted to “defence minerals”.

At the end of last week, there was word of trouble with physical gold deliveries in London too:

(Source)

Physical gold is traded using contracts, not often physical delivery is requested, generally in the past most are satisfied with these contracts for physical gold, but it seems more and more are asking to actually claim the gold bullion and keep it themselves.

A surge in gold shipments to the US has led to a shortage of bullion in London, where the wait for bullion deliveries from the Bank of England vaults has risen from a few days to between four and eight weeks.

People get a bit nervous when they can’t get their hands on the physical gold quickly enough.

In this case, New York traders have stockpiled US$82BN in gold likely because of fears over Trump’s tariffs.

If things like this keep happening, it should only further fuel the precious metals beast, as the supply constraint out of London is of an entirely larger scale to the long lines at bullion shops we’ve seen ourselves.

It points to a further strengthening of our key investment theme for 2025 - global uncertainty.

The effects of this theme were clearly visible at Africa’s premier mining investment conference Mining Indaba, which took place in Cape Town this week.

Africa looks set once again to be at the centre of a mammoth push by investors and governments to protect themselves against rising global uncertainty.

(We sent one of our analysts this year and will share their first hand account of the conference later)

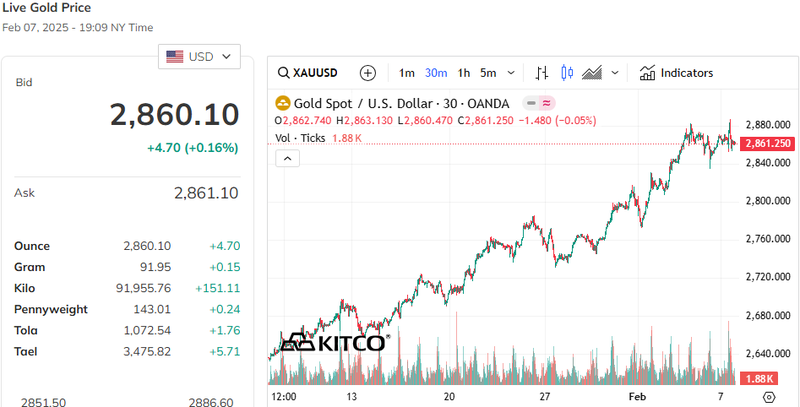

Before we get to that though, what on earth is happening with gold and silver prices right now?

It’s quite a sight to behold.

Just check out the pretty much straight line ascent on the gold price chart for the last month - up a nearly 10% since the start of the year:

And the similar but more choppy silver price chart that is still threatening a sustained punch above US$32/oz over the same time frame:

Price charts like these remind us of stock price charts from the 2020-2021 small cap bull market, except they are for commodities that are often seen as a hedge against global uncertainty and currency devaluation.

Here’s what this could mean for small caps...

Gold and silver leading the charge: from hedge to “risk on”?

Hedges are definitely IN for the market right now.

Are governments doing a bit of “hedging” of their own by rushing to secure defence mineral supply chains?

More on that below.

But let’s start with the millennia old concept of “hedging”.

Hedging is basically a risk management strategy employed to offset losses in investments by taking an opposite position in a related asset.

Gold and silver are the obvious ones in times of global uncertainty.

Silver has a bit more “risk on” flair to it than its big yellow brother.

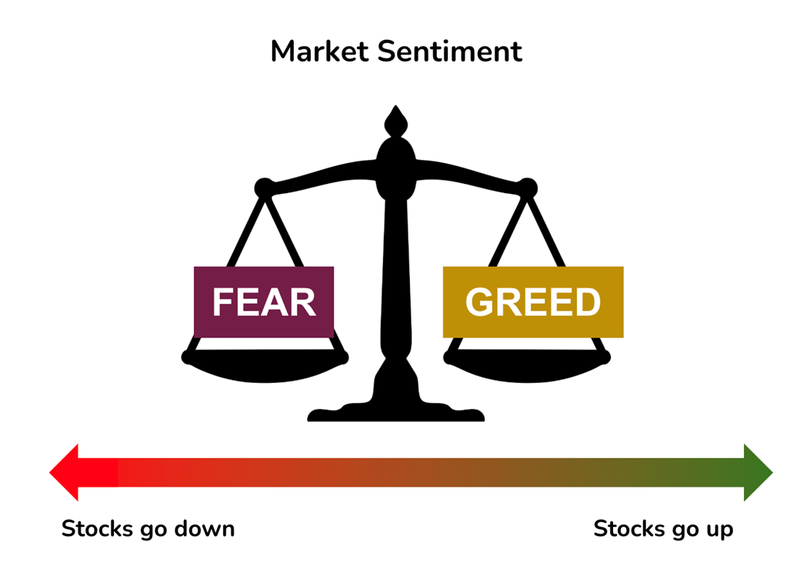

With the concept of a hedge - people typically think of hedges as defensive investments.

A fear based investment in the binary fear/greed market spectrum of emotions.

Typically we see stocks go up when greed is greater than fear, which can be seen in this very simple image below:

Hedges are usually motivated by “fear” in some way.

I.e. the thinking is “Things could go wrong - what can we do as investors to protect against downside risk?”

“Risk on” investments on the other hand are usually motivated by greed.

I.e. the thinking is “How do I capitalise on a potential upside scenario?”

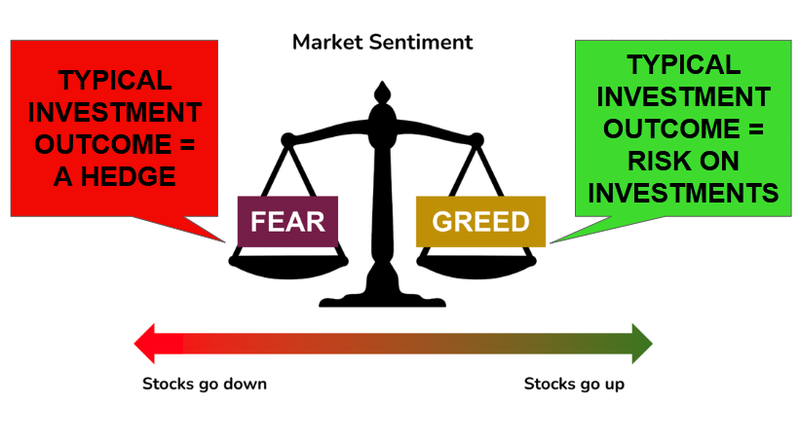

But sometimes there’s a thin (or blurred) line between hedging and “risk-on” investments.

Take gold and silver prices for instance.

Given their sustained rises, we think on some rare occasions (like we’re seeing now) it feels like the hedging and fear market mentality is getting mixed up, changing and may potentially manifest itself in a NEW form of the “risk-on” and greed market mentality.

In other words, we think gold and silver stocks have increasingly become an outlet for the pent up “risk on” angst in the market after a particularly nasty 2-3 year bear market for small caps.

It’s like the trauma of the bear market is finding a new way of expressing itself.

This time in gold and silver stocks, and increasingly, small cap gold and silver stocks.

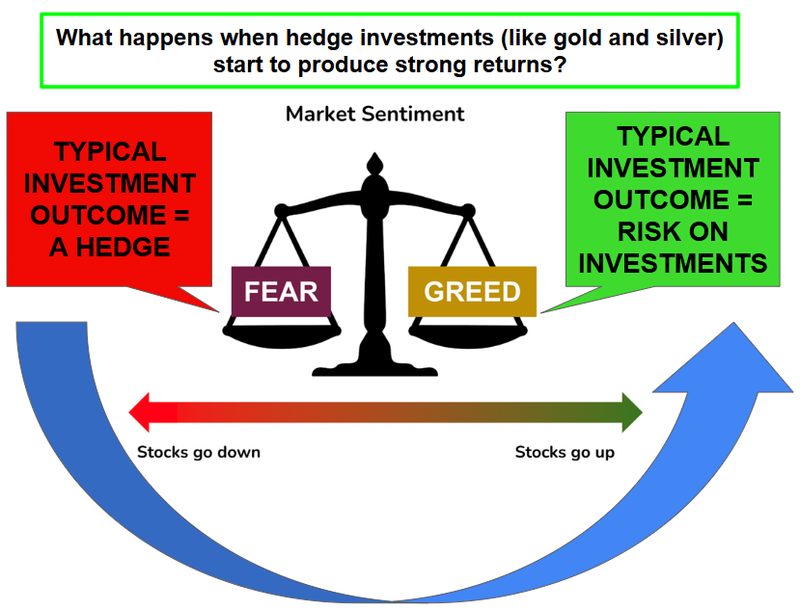

So we get a hedge and fear/”risk on” and greed image that looks a bit like this:

That’s right, gold and silver, supposedly “hedge-like” investments can develop their own “risk on” mojo via stocks, and the market can swing back to greed, at least in certain areas.

(At first... we hope it eventually spreads to other parts of the small cap world)

We were a bit early to the party - gold was one of our top macro themes for 2023.

But after a slow start, there was finally some upwards traction for gold and silver price movements back in May last year:

Read the Weekender: Commodity Prices just keep Running

A raging bull of a precious metals price run is now flowing through to gold and silver stocks - where we have seen some serious re-rates within our Portfolio companies this year.

A rise in the underlying commodity price often takes time to flow through to stocks in the smaller end of the market.

If physical gold and silver holdings are the initial market move as a hedge, rising prices for these commodities often manifest later in more “risk on” trading in small cap stocks that could benefit from these rising prices.

Point is, we’ve been going deep on the gold and silver markets for a few years now.

We have collated what we’ve learned about gold and silver over this period (and profiled 6 of our gold and silver Investments) into this new e-book:

As we mentioned before, we’ve already seen re-rates in some of the stocks in the e-book.

Defence minerals could also benefit from the same thing driving gold and silver prices - global uncertainty.

This is the broad global investment theme that we see driving capital flows in the market right now.

So like we mentioned at the start of this year, specific sectors we will be looking for new Investments include:

- Gold and silver

- Defence technology

- Defence materials/metals

- Other strategic, critical materials (for semiconductors, critical technologies etc)

Again, if you know of any ASX listed companies that fit into one of the above categories, please reply to this email with the stock code (and a short description), and we will take a look.

We are also interested in seeing private/pre-listing companies and seed offers in the above sectors - again, just reply to this email.

So that’s what we think investors and the market are up to with hedging right now and where things are going in the future.

But governments around the world are pretty spooked too, and as a result are deploying large amounts of capital to shore up supply chains.

While investors pile into supposedly defensive assets like gold and silver, it’s now also prime time for defence minerals.

Global uncertainty means governments are hedging too: New China defence minerals export bans announced this week

This week, China imposed further export restrictions of defence minerals.

Materials affected by China’s new export controls include: tungsten, tellurium, bismuth, indium and molybdenum-related products.

All materials that play some important roles in defence supply chains.

Coming back to that idea of a hedge - critical minerals have been re-cast as defence minerals, which are also a hedge like gold, except for governments.

Stockpiling, government funding of defence mineral projects - it's all a defensive play.

Except instead of investors hedging against currency devaluation like with gold and silver, governments are also hedging against supply chain breakdowns in the event of potential conflict.

Which in turn, we’ve seen already leading to some major “risk on”-style runs for companies with defence mineral projects.

As before, we expect to see more of this in 2025.

This view is based on past investing experience across different global investment themes of the last 5 years in particular.

Here’s the short story on those 5 years:

The battery minerals bull market boom of 2020-2021 gave way to the critical minerals macro theme over 2022-2023 (albeit in a bear market).

2024 heralded the start of the precious metals bull run - which looks to have plenty more to run.

And that precious metals bull run we think may eventually flow more into a “defence minerals” macro theme in 2025 and beyond.

So in summary: it's precious metals right now, but the flow of money to defence minerals or those minerals with a “high probability of supply chain disruption” is growing.

This view was confirmed by one of our analysts who recently attended the annual Mining Indaba conference in Cape Town.

Mining Indaba is one of the premier mining investment conferences in the world - and Africa looks once again set to become a hub of investing activity as the global uncertainty theme unfolds.

Here’s our analyst’s account of the conference and more on what opportunities that the global uncertainty theme is throwing up.

All eyes on Africa: Our analyst went to Mining Indaba, here’s what happened

Cape Town was buzzing this week.

Ministers, brokers, geos, drill contractors all flew in from around the world for the premier African mining event of the year.

Mining Indaba.

This week, no commodity was talked about more than gold.

Even on the way to the conference, walking through the streets of Cape Town, there were dozens of locals hired to wear “cash for gold” advertising signs.

And while gold paved the streets of Cape Town, so did it dominate the conference agenda.

Almost every broker and small cap junior that I spoke to had a gold project to hawk.

Always at an ‘undervalued price’, and the pitch was often accompanied by a quick check of the gold price.

Is it at US$3,000 yet?

Quite a bit has changed since the last time we were at Indaba.

A lot less “energy transition” and a greater focus on the traditional commodities that shape the African landscape.

Gold, copper, bauxite, iron ore, diamonds...

(a little bit of lithium still, and uranium too).

Throughout the first month of 2025 we have written a lot about positioning our portfolio for a macro thematic of "global uncertainty”.

At the conference I tried to identify what (if any) the role of Africa would be in potential trade tensions and global conflicts with the US and the rest of the world.

From the conference it appeared that Africa is staying out of “picking sides”.

But because of its rich mineral wealth it is strategically important to both the East and the West in securing critical material supply chains.

Listening to each country representative speak, it is clear that the projects that advance the socio-economic goals of that country will be favoured.

Which is why engagement programs at the local grass roots level are so important for Africa.

One big mining project can be transformational for an African country.

But also, one big mining project could be the answer to supply chain bottlenecks for the US, Europe or China.

One of the most interesting discussions that I had throughout the week was with a delegate from the United States who had helped to write the US critical minerals strategy.

Because of how core “critical minerals” were to our investment thesis for 2025 I wanted to dig a bit deeper and hassled him for some more information.

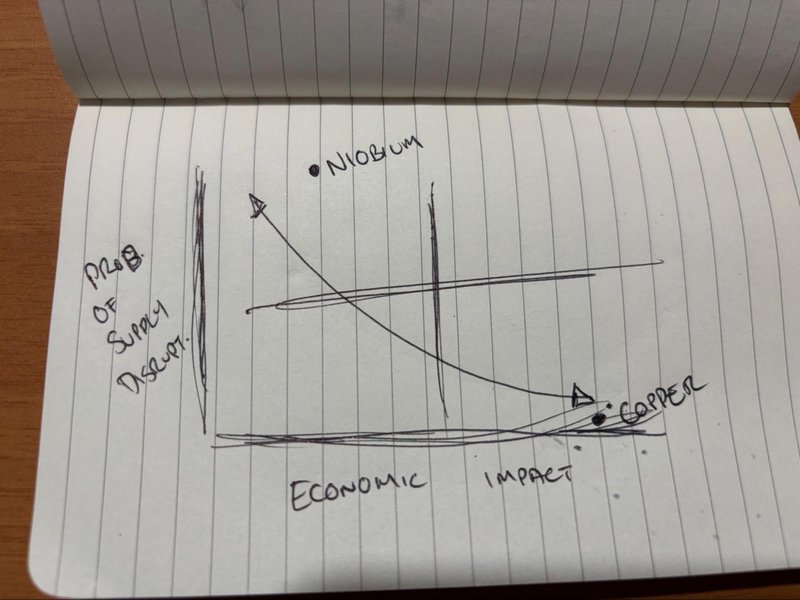

He went through the whole methodology with me and there are two main factors that affect which minerals are considered ‘critical’ (1) Probability of Supply Disruption (2) Economic Impact.

The chart he drew looked a little something like this:

The commodities under the curve (like copper) are not considered ‘critical’ while those to the right of the curve (like niobium) are.

This is because even though copper has an extremely high economic impact, the US sources its copper from a multitude of friendly nations.

We debated about the nuances of ‘where to draw the line’, and why uranium was left off as a critical mineral.

(because it was more akin to a fuel rather than a mineral).

Interestingly, byproduct commodities move higher up the "probability of supply disruption” because their production is not generally as sensitive to price changes.

We also discussed how China often acts like a “one-country OPEC” when it comes to a bunch of minerals like graphite, lithium and rare earths.

OPEC or the Organization of Petroleum Exporting Countries controls 40 percent of the world's crude oil supply and plays a huge role in dictating where the price of oil trades at any given time by coordinating to either increase or decrease global oil supply.

China has similar (and oftentimes much higher) market shares across a range of critical raw materials.

China controls so much of the supply chain that it can affect the price by turning on and off production, flooding the market or tightening supply.

By depressing the price or altering supply, this creates an uncertain environment for financiers of projects, in turn hurting the development of new mines in the West or within the borders of allied/aligned countries.

This is a problem for the US, and they are looking at how to stop it.

This was just one of the many fascinating discussions that I had during the week.

Who was there from the Next Investors Portfolio?

There were four companies in our Portfolio that I saw while at Indaba:

- Minbos Resources (ASX:MNB) - Started construction a few weeks ago on its phosphate plant in Angola. Forecast for ~US$55M in EBITDA per year.

- Tyrana Resources (ASX:TYX) - Lithium in Angola. Partnered with Chinese giant Sinomine TYX is also looking for other opportunities in the Angolan region.

- Evolution Energy Minerals (ASX:EV1) - Construction ready graphite project in Tanzania. Major investor and offtaker is BTR New Materials Group, one of the largest anode manufacturers in the world.

- Heavy Minerals (ASX:HVY) - Garnet projects in Australia and Mozambique. PFS for its Australian garnet project scheduled for this quarter.

First, I was eager to meet the new London-based CEO from EV1, George Donne.

Although he has only been CEO for a few months it was clear that he was brought in to help the company with the larger financing piece.

Donne has a track record here, as VP Business Development at Giyani Metals Corp Donne secured over USD $30 million in equity and project financing and advancing off-take negotiations with international OEM

He was sharp, and extremely well connected and plugged into the battery metals space.

The company has a solid mine plan, all the key permits and 90% of the production in offtake.

(particularly with major anode company BTR New Materials Group)

I also bumped into Adam Schofield from HVY.

HVY is scheduled to publish the PFS this quarter.

A pre-feasibility study (PFS) is an economic study that will show how HVY’s project can make money from its garnet project in WA, hopefully paving the way for financing and ultimately, mine construction and production.

I also saw Lindsay Reed from MNB and David Crook from TYX both of which were highlighted on Angola Day.

Angola Day: “All Protocol Observed”

This year marks Angola’s 50th year of independence.

Opening the day were remarks from Diamantino Pedro Azevedo the Minister of Mineral Resources, Petroleum, and Gas for Angola.

His message was simple and direct.

An open arm invitation to the investment community to come to Angola.

With passion, he chanted, "Angola, Angola, Angola," and a packed room of 300 people answered in kind, "Angola, Angola, Angola".

Diamantino was the same minister that we saw in 2023 making the exact same invitation.

Come to Angola, we will help you.

And since then, companies have listened.

Both Ivanhoe Mines and Anglo America have made investments in the country since that first message in 2023.

And the Angola room was the most packed talk out of any that I attended.

Presenting on that day was TYX’s Managing Director David Crook.

A quick little story about what happened.

The speakers were running WAY overtime and TYX almost got bumped to make time for the Minister to give one final closing address to the room.

The agitated host came out to cut off the presentations, ready to sternly cut off TYX.

But instead Minister Diamantino waved her off and said something to the effect of “I want everyone here to hear this man present”.

(A glowing endorsement from the Angolan minister)

TYX recently published assays over its lithium project with key partner Sinomine.

There are pegmatites everywhere over the project and TYX has only drilled a small part of its project area.

Now that TYX has been in Angola for a few years it is also looking to secure more ground in the region, utilising its networks within the country and its in-country team.

(Angola is rich in lithium, but also other commodities like gold and copper).

I met the in-country manager Paulo, a very articulate guy.

MNB, our other Angolan based project presented a little later in the week.

MNB started construction on its phosphate (fertiliser) a few weeks ago with production scheduled for later this year.

The focus of the discussion was on food security in Africa and how fertiliser is basically a giant “product booster” for food.

One of the key takeaways from the discussion was about the lack of fertiliser that was sourced internally within Africa.

For Angola to be competitive with countries like Brazil as an agricultural hub it needs to have its own supply of fertiliser.

On the demand side population growth is set to drive demand for fertiliser.

Particularly within Africa.

By 2050 two thirds of the world’s population growth is set to come from the South Sahara area in Africa.

This means a lot more food, and a lot more fertiliser.

MNB’s product is phosphate rich, which means that it is perfect for the Angolan climate to help farmers improve crop yields.

The company has an MoU for an offtake agreement with the largest agri-distribution business in the country, Grupo Carrinho, that provides fertiliser to nearly 2 million farmers each year.

MNB is set to get into production this year, hopefully just in time for the Angola 50 years of independence celebration.

Bauxite: Unlocking the Downstream Aluminium Door

I listened to quite a few panel discussions but there was one that stood out the most...

Bauxite: Unlocking the Downstream Aluminium Door.

There is no doubt about it, the largest exporter of bauxite (Guinea) wants to own their own downstream bauxite-aluminium supply chain.

And the topic of this panel was how the country was going to get there...

We made Canyon Resources (ASX:CAY) our 2025 Wise Owl Pick Of The Year.

CAY is developing a Tier One bauxite asset in Cameroon, Africa.

Bauxite is the key ingredient to make aluminium.

Aluminum is a critical metal for the energy transition and the defence industry.

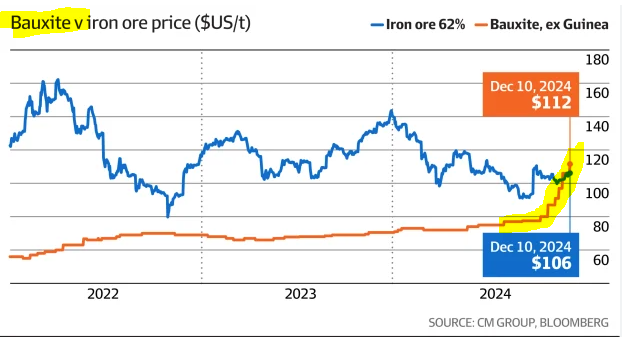

Over the last 12-months the bauxite price has been climbing, and for the first time ever took over the price of iron ore.

70% of China’s bauxite imports are from Guinea.

So, if Guinea reduces its bauxite exports in favour of local consumption China may need to buy the bauxite it needs to feed its aluminum smelters from somewhere else.

This entire talk was on how Guinea (and Ghana) are making a big effort to build up their capacity to make aluminium downstream.

Included in the talk was Hon Bouna Sylla, the Minister of Mines and Geology of Guinea.

(On the far right).

For Guinea to capture the downstream value of bauxite production it needs to:

- Build out cheap reliable sources of energy (Aluminium production is incredibly energy intensive)

- Attract risk capital to the region

- Improved integration and logistics

- Train a skilled workforce

If Guinea is able to solve these challenges, then it starts to capture downstream the value of selling aluminium.

(this is obviously bad for China’s aluminium smelters as it will need to find other sources of bauxite, pushing the price of the commodity up).

Guinea's second ever aluminium smelter is set to come online in 2027.

The drive to get more value out of the bauxite supply chain is a key reason other countries have banned bauxite exports in the past.

In 2022 Indonesia banned exports and triggered a bit of a run on the bauxite price.

Recently Guinea (2nd biggest producer globally) blocked exports temporarily out of the country...

The blocked export sparked a rally in the bauxite price from ~US$60/tonne to where it trades now at ~US$110 per tonne.

(Source)

Our view is that a move by Guinea to go downstream in the bauxite/aluminium trade, could mean new bauxite projects need to be developed to fill in gaps in the supply chain.

That’s why we are Invested in CAY.

Overall it was a fantastic week, a big thank you to Hyve for putting on the event and a big thank you to the Cape Town locals for hosting me in your beautiful city.

What we wrote about this week 🧬 🦉 🏹

James Bay Minerals (ASX: JBY)

JBY released their first gold assays...

James Bay Minerals (ASX:JBY)’s project in Nevada, USA has a foreign 1.18Moz gold and 7.6Moz silver resource..

The resource includes an inferred high grade component of 796,200oz gold at 6.53g/t.

The resource is open in all directions...

AND this week, an 18m hit at an average gold grade of 1g/t showed that the gold might actually extend ~520m to the east of the current resource.

Read: ⛏️ JBY gold hit: 520 metre extension to gold mineralisation?

Lightning Minerals (ASX:L1M)

The drill rig is now contracted.

The start of drilling is locked in - the week of February 15th.

Will it deliver some shiny purple drill cores?

And can it repeat the success of one of our all time best Investments?

Our ~$8M capped Investment, Lightning Minerals (ASX:L1M) is now less than two weeks away from drilling its lithium project in Minas Gerais Brazil.

Read: ⛏️ L1M drilling booked in - 2 weeks to go

Quick Takes 🗣️

88E’s neighbour Recon Africa hits oil in Namibia

Ex-CBMM Niobium Boss Ricardo Maximo Nardi Joins SGQ

CAY receives key rail approvals

EMD releases positive MDMA trial data for PTSD

IIQ set for a busy period of newsflow this year

TTM gold hits from 3.1M oz Dynasty project

Macro News - What we are reading & listening to 📰

Defence:

China builds huge wartime military command centre in Beijing (Financial Times)

- China is building a massive military command centre near Beijing, estimated to be 10 times the size of the Pentagon.

- US intelligence believes the facility will serve as a wartime bunker, enhancing China's nuclear and military capabilities.

Where do the separated rare earths produced by Lynas actually go? (Live Wire)

- Western policies aim to reduce reliance on China for critical minerals, but without real buyers, Australia’s industry struggles to grow.

- US trade data is open, showing Lynas' rare earth shipments, while Australia's secrecy hinders transparency and investment confidence.

Greece's Prime Minister Mitsotakis Calls for €100 Billion EU Fund for Defense (Bloomberg)

- Greek PM Mitsotakis called for €100B in EU defense spending, joining other nations pushing for a stronger security strategy.

- The proposal aligns with concerns over Russia’s military buildup and debates over joint EU defense funding.

The revenge of the Mediterranean (Financial Times)

- Southern Europe is gaining economic and political influence, with Spain, Greece, and Portugal outperforming northern nations.

- The Mediterranean region’s strategic importance is rising due to migration control, global connections, and shifting EU power dynamics.

China expands critical mineral export controls after US imposes tariffs (Mining Weekly)

- China is restricting exports of five key metals, including tungsten and bismuth, in response to US tariffs.

- The move may raise global prices but is seen as a "warning shot" rather than a full market disruption.

Steve Baxter’s defence technology VC firm rules off first close, prepares to deploy (AFR)

- Steve Baxter's Beaten Zone VC fund secured a $10M first close to invest in defence tech.

- He sees growing opportunities as defence budgets rise and traditional investors avoid the sector.

Rare Earths:

Trump wants Ukraine's rare earth elements as a condition of further support (AP News)

- Trump wants U.S. access to Ukraine’s rare earth materials in exchange for continued support.

- He claims Ukraine is open to a deal as he pushes to end the war with Russia.

What we are watching:

The view from China: Exclusive interview with Ganfeng Lithium

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.