JBY gold hit: 520 metre extension to gold mineralisation?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,979,167 JBY shares and the Company’s staff own 33,334 JBY shares at the time of publishing this article. The Company has been engaged by JBY to share our commentary on the progress of our Investment in JBY over time.

Another new all time high for gold overnight.

JBY just released their first gold assays...

James Bay Minerals (ASX: JBY)’s project in Nevada, USA has a foreign 1.18Moz gold and 7.6Moz silver resource..

The resource includes an inferred high grade component of 796,200oz gold at 6.53g/t.

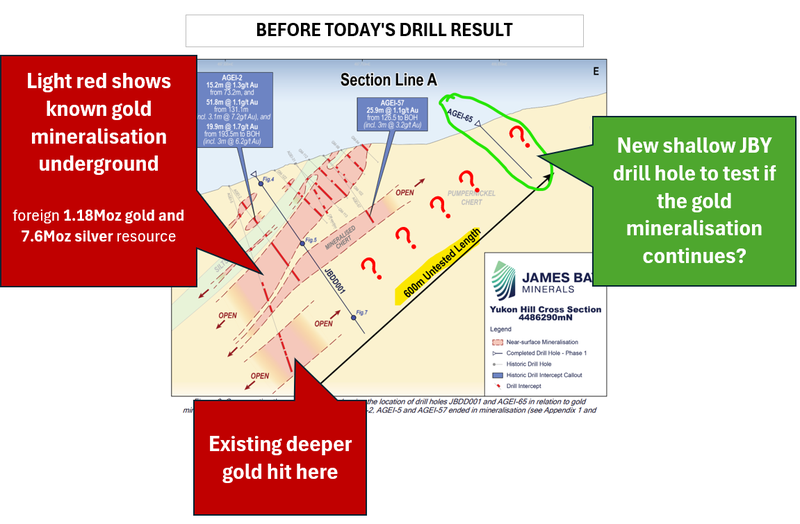

The resource is open in all directions...

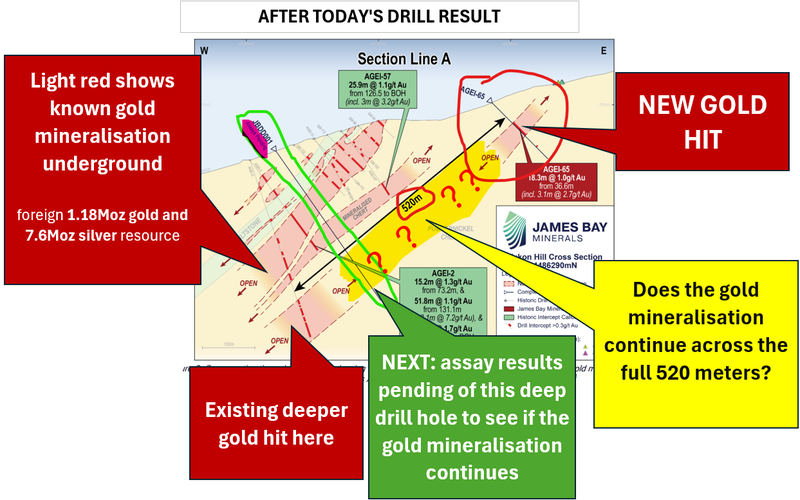

AND today, an 18m hit at an average gold grade of 1g/t showed that the gold might actually extend ~520m to the east of the current resource.

Until now, drilling hadn't really tested for extensions to the east...

AFTER today’s drill result - a potential extension 520m away from the existing resource area?

To confirm this potential 520m of additional gold mineralisation, JBY will need to drill deeper holes in the yellow highlighted part of the above image and deliver more gold hits.

The deep drill hole shown in green above has been drilled already and we are just waiting for the result...

And more drilling is scheduled for the next few months.

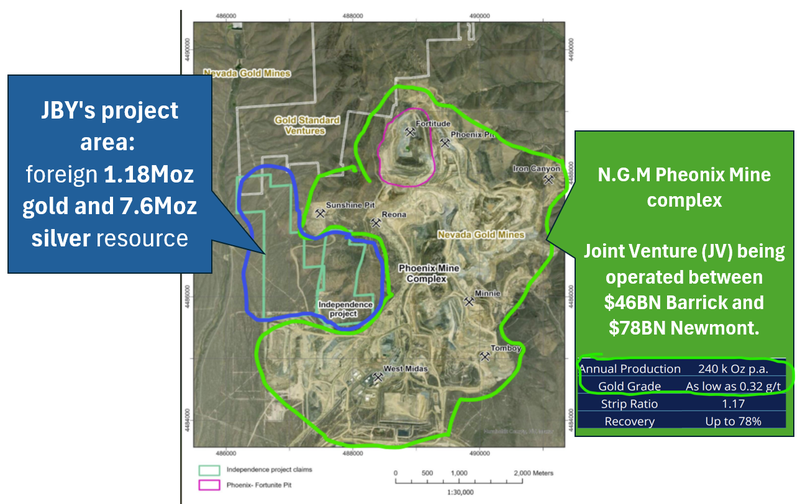

JBY’s project is surrounded by existing gold mines in the “N.G.M Phoenix gold complex” - a Joint Venture (JV) being operated between gold mining majors $46BN Barrick and $78BN Newmont.

Nevada is also home to some of the lowest cost mines in the world.

You can actually see all the existing mining pits inside the green circled area on the above satellite image.

These mines produce 240,000 oz of gold per year - from grades as low as 0.32g/t.

240,000 oz of gold per year is ~$1BN at today’s gold price, which just hit yet another all time high overnight of US $2,843 per oz.

JBY’s project has had over US$25M in capital spent to get the project to where it is today.

JBY’s project also has a 2022 Preliminary Economic Assessment (PEA) which shows it could produce 32,050 ounces of gold per year for 6 years at a cost of US$1,078 per ounce. (source)

At today’s gold price that's US$90M in revenues with costs of US$35M per annum for six years...

JBY’s 1.18Moz gold and 7.6Moz silver resource is “open at depth and in all directions”

Meaning that more exploration drilling could increase the size if JBY can deliver more successful drilling.

This morning JBY released the first batch of assay results from its drilling program.

The drilling is a mix of RC and diamond drilling - JBY is looking for shallow mineralisation with the RC rig and is also putting a few deeper holes into the project with a diamond rig to test for extensions at depth.

The assays from the deeper drilling are pending.

BUT today we did get the results from the RC which showed that JBY’s gold project might actually extend to the east of its tenement boundary (~520m to the east).

So it's good to see that the drilling to the east has delivered gold mineralisation... we are hoping it means an extension to the current resource footprint in that direction.

NEXT: we want to see the result from JBY’s first deeper diamond drillhole to see if the mineralisation extends between today’s hits and the existing resource.

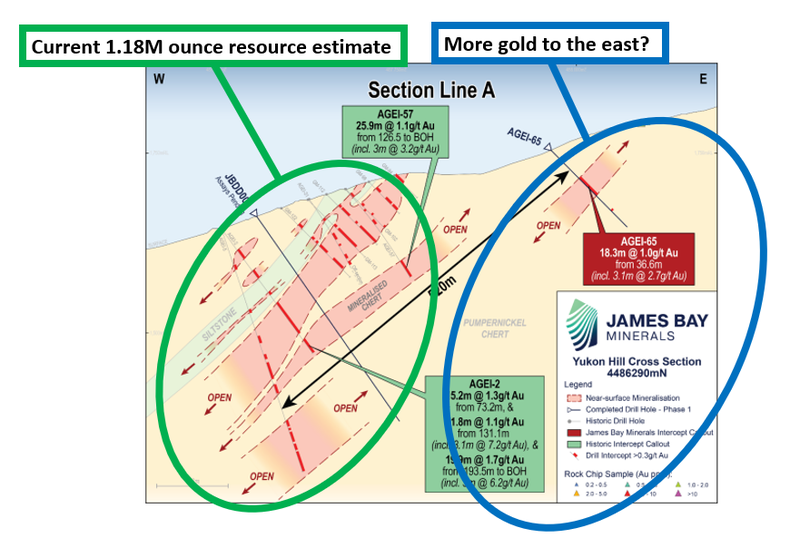

Ultimately, we are hoping there is a lot more gold to the east of its existing resource.

At the moment it's too early to say for sure, but the first result looks pretty decent, and is showing that there may be more gold toward the east of JBY’s current resource:

Exploration is a big part of the JBY story

At the moment, JBY’s current resource is a “foreign” resource estimate.

A foreign resource estimate is an accepted form of resource modelling across North America.

ASX listed companies are required to state their resources under the JORC code which often means companies need more drilling data before they can convert to JORC.

The current drilling will be used to convert it into JORC status.

(AND hopefully deliver an upgrade to the current numbers).

These are two of the key objectives we said we wanted to see JBY achieve over the coming 12-18 months:

Objective #2: Convert foreign resource estimate into a JORC resource

We want to see JBY convert its existing foreign resource estimate into a JORC resource.

Milestones

✅ JORC conversion commenced

🔲 JORC resource estimate completed

Objective #3: Upgrade existing resource estimate

We want to see JBY run an extensional drill program to expand its existing resource beyond the 1.18m ounce gold & 7.6m ounce silver resource.

Milestones

✅ Drilling commenced

🔄 Drilling results

🔲 Resource upgrade

At the same time we think there is a big bit of exploration upside that the market hasn't really started pricing into JBY just yet.

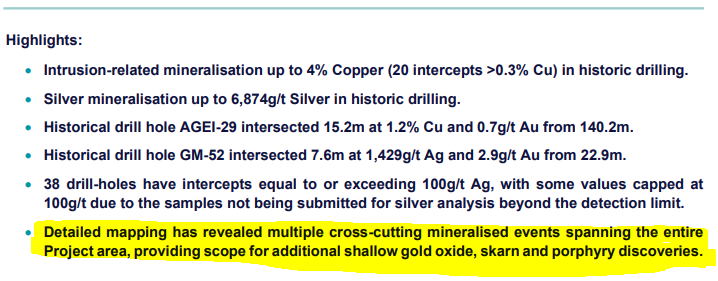

Late last year JBY put out assay results from old drillholes which showed copper and silver mineralisation.

20 of the old holes had copper grades >0.3% copper, 38 holes had >100g/t silver.

Pretty strong grades considering most of the old drilling would have been targeting only gold mineralisation.

A key takeaway for us from that announcement was the commentary on the potential to make “porphyry discoveries”.

The main reason it caught our interest was because of where JBY’s project sits...

JBY’s project is right next door to the Phoenix gold Complex - operated in a Joint Venture (JV) between $62BN Barrick and $73BN Newmont.

Across that complex, Newmont and Barrick have a ~3.3M ounce gold, 850Mlb copper and 35M ounce silver resource all near surface...

Here is how close the projects operated by Newmont is to JBY’s project:

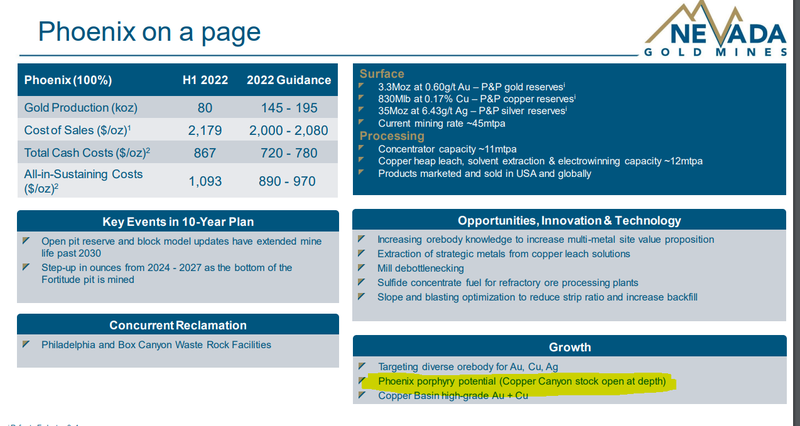

As we mentioned earlier, another reason today’s announcement caught our attention was because of the commentary around the potential to make “porphyry discoveries”.

The potential to make “porphyry discoveries” hasn't been a big part of the JBY story until today’s announcement.

But it's something that neighbours Newcrest and Newmont have talked about in their project presentations and project site visit decks...

Here is a slide from a recent deck for the JV which mentioned “Phoenix porphyry potential” for the project.

(Source)

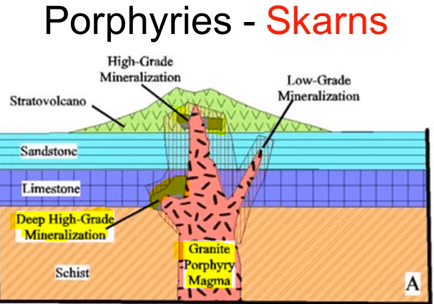

JBY’s resource is a mix of near-surface oxide mineralisation and a higher grade skarn structure.

The skarn mineralisation is important, first because of its high grade nature but also because it could be an indicator of porphyry mineralisation nearby...

Here is what it looks like on a diagram:

A big part of the reason we are Invested in JBY is because of the existing resource and the exploration upside to the project as it stands now.

The porphyry potential just adds a blue sky upside to the project that sits completely outside of our JBY Investment Memo.

This type of blue sky upside can be important in the long run - especially when your multi billion dollar neighbours are talking about it.

As Newcrest and Newmont operate the Phoenix complex and mine out the existing resources of the project they will look to add bolt on resources to plug into all of the existing infrastructure they have spent decades (and billions of dollars) building.

So if Newcrest/Newmont go out and prove a big porphyry discovery here, JBY could benefit just from its nearology.

The porphyry potential is all unexpected blue sky upside for JBY, the main reason we are Invested is for the shallower gold mineralisation...

For now, our focus is on JBY’s gold resource...

In the short-medium term we expect JBY’s valuation to be dictated by the movement in the gold price and how well the company can progress its gold project.

Next we want to see the results from the deeper diamond drilling - which will tell us if the 520m extension from today’s results connects to the area where the existing resource is:

Gold and Silver to continue their run in 2025?

So far it certainly looks like it...

Gold and silver both had a pretty strong year in 2024 - gold was up 27% and silver up 21%.

We think gold and silver are going to be one of the big stories of 2025.

Our view is that the macro themes that triggered the first rally back in 2018 and then again in 2020 are only stronger now:

- Global uncertainty is higher - sentiment to deglobalise is stronger and the world has gone into a sort of protectionist mentality.

- More geopolitical conflict - there are wars continuing in Ukraine/Russia, the Middle East and across Africa.

- Sanctions and tariffs are now being used more often - the Trump government is threatening to put in place sanctions and tariffs against countries that it thinks aren't playing ball...

- Global debt is increasing - all of the above is leading to more and more debt...

A combination of the above factors may be why the gold price is ripping...

The world is looking for a medium of exchange and store of value that sits outside of the current financial system and which is harder to confiscate...

We think that all of these factors will only become more and more prominent over the short term.

In this past Saturday’s Weekender edition we shared our gold e-book which lays out our bull case for precious metals.

We won't cover our views again today but for anyone wanting to see why we think precious metals are going to have a stellar run this year and beyond, here is the link to the e-book:

What we want to see next from JBY?

Assay results from the deeper diamond drilling 🔄

In the short term we want to see what comes of the deeper diamond drillhole JBY drilled beneath its existing resource.

The key thing we are looking for is to see if the gold structures match up with the extensional hits from today:

Ultimately we are hoping to see JBY confirm there is more gold to the east and at depth. This could mean JBY can add to its existing foreign resource in future resource updates.

JBY advancing its project forms the basis for our Big Bet which is as follows:

Our JBY Big Bet:

“JBY re-rates to a +$300M market cap by expanding its large US gold resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our JBY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What are the risks?

In the short term the key risk is exploration and resource risk.

JBY is currently running a drill program looking to verify and extend its current foreign resource estimate.

First of all there is no guarantee that the extensional drilling delivers any results that add to the resource number.

Second, there is no guarantee that JBY is able to convert all of its existing foreign resources into a JORC compliant resource.

Drilling will need to be done to verify the data that makes up the foreign estimate.

There is a risk the drilling fails to verify those results and the resource goes backwards once its JORC compliant.

Any downgrades to the resource OR poor exploration results could re-rate JBY’s share price lower.

Exploration risk

There is no guarantee that JBY can increase its existing resource estimate through exploration drilling. There is always a chance that drill programs fail to find any economic mineralisation that may not add to the project’s overall resource estimate.

Source: “What could go wrong” - JBY Investment Memo 25 November 2024

Resource risk

At the moment, JBY’s project has a “foreign resource estimate”. This means it is built on a different set of assumptions & guidelines relative to the JORC code that we are more accustomed to seeing on the ASX. There is no guarantee that JBY can convert all of its foreign resources into a JORC resource. If this risk were to materialise it may have a negative impact on the company's share price.

Source: “What could go wrong” - JBY Investment Memo 25 November 2024

To see other risks to our Investment Thesis, check out our JBY Investment Memo here.

Our JBY Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our JBY Investment Memo where you will find:

- What does JBY do?

- The macro theme for JBY

- Our JBY Big Bet

- What we want to see JBY achieve

- Why we are Invested in JBY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.