Accelerating growth, when will the macro catch up?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,525,000 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

We first invested in Oneview Healthcare (ASX:ONE) back in March 2021, naming it our Tech Pick of the Year thanks to its mature technology, revenue and sticky customers, and it looked like ONE was about to accelerate growth.

At that time, ONE had signed on ~9,000 hospital beds around the world, providing patients with a “virtual care and digital control centre” at their bedside.

That figure had taken 13 years to achieve, and by 2021 ONE had a proven product — cloud-hosted patient dashboards that help to make hospitals more efficient and patients more engaged in their own care — and it appeared to be on the cusp of accelerated growth.

Over the past 18 months, ONE drastically picked up the pace, adding a further ~5,000 beds — a more than 50% increase, in just a fraction of the time it took to sign the first 9,000 beds.

This growth saw ONE shares deliver a very good run during 2021 but, unfortunately, the global tech wreck that started on the NASDAQ back in January this year poured a big bucket of cold water on ONE’s share price (and pretty much every other tech stock).

These macro headwinds led to ONE’s share price pulling back to ~9c, which is pretty close to our Initial Entry Price of 6.5c in March 2021 — pretty much pricing out all the progress made since.

A very good move by ONE was to secure $20M in a placement at 27c in November 2021, literally weeks before the US tech crash started and tech funding dried up.

This provided ONE with a significant cash buffer to continue executing on its growth plans while we all wait for global tech sentiment to improve.

We participated in this placement at 27c.

Since then, ONE has secured its biggest ever deal and the dynamics around health tech appear to be shifting in ONE’s primary target market, where US hospitals were brought to the brink by the pandemic and the costs associated with staffing them in a time of crisis.

This was the lightbulb moment for US hospital administrators when it comes to tech driven efficiency — evidenced by the surge in ONE’s sales pipeline, as reported in the latest ONE Investor call (we provide a summary of key takeaways later in this note).

We see this sales pipeline as a “dam waiting to burst” and bring with it a flood of new hospital sign ups, more contracted beds, and ultimately, big revenue growth and sustained profitability — ideally with the majority of this news flow timed with a recovery in tech sentiment.

We also note a research report by a group called MST Access which summarises the key value points of ONE and assigns a price target of 30c. Our summary of this report and a link are included in today’s note.

While it’s always great to see a high price target on one of our Investments by another analyst, remember that these price targets are estimated using a number of assumptions that may not happen. Reports such as these are useful to assist research, but should not be solely relied upon for making investment decisions.

We are long term holders in ONE, and even though its share price has come back to near our original entry price after a great price run last year, we still hold 80% of our original position.

As long term holders, and as much as the US tech wreck has beaten up tech stocks, we are patiently holding to, hopefully, see ONE deliver on our Big Bet.

Our Big Bet for ONE is as follows:

ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1BN valuation (based on 5x to 10x forward ARR multiple) and be acquired by a large health tech provider

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

The key thing we want to see from a broad perspective over the next few years is more deals (obviously), importantly with new deals being signed at a faster rate.

Rapid growth is what gives growth stage technology companies a higher valuation, because investors are betting that the growth will continue to accelerate into the future.

Again, ONE has already added 5,216 beds in the last 18 months, compared to taking 13 years to add the first 9,259 beds.

So while it has been a bumpy ride for ONE during the 2022 tech wreck, we are still holding and waiting for the risk-off mood in tech to change as the interest rates picture becomes more clear.

While it’s expected that a tech stock like ONE will get dragged down during a global tech sell off, we are surprised to still see ONE trading as low as the 9c mark in recent weeks.

Macro themes aside, if we look at ONE’s progress over the last 18 months the business is actually in a very strong position and delivering the important accelerated growth.

For a quick summary of ONE’s progress since we Invested, here is our brand new ONE Progress Tracker which includes links to all our previous coverage:

It only takes a few minutes to scroll the ONE Progress Tracker to get a quick helicopter summary of its progress, something that we find helpful to do before reading each new ONE announcement.

A quick scan of the Progress Tracker helps give context to how new announcements contribute to our Big Bet and near term Investment Memo objectives for ONE.

How do the latest ONE half year results stack up against Memo?

ONE released its half year results in late August, and although the raw financial data may not have thrilled the market, there were enough green shoots across our favoured metrics (contracted beds/sales pipeline) to make us optimistic about ONE’s future trajectory.

Our target for this calendar year was a total of 15k contracted beds:

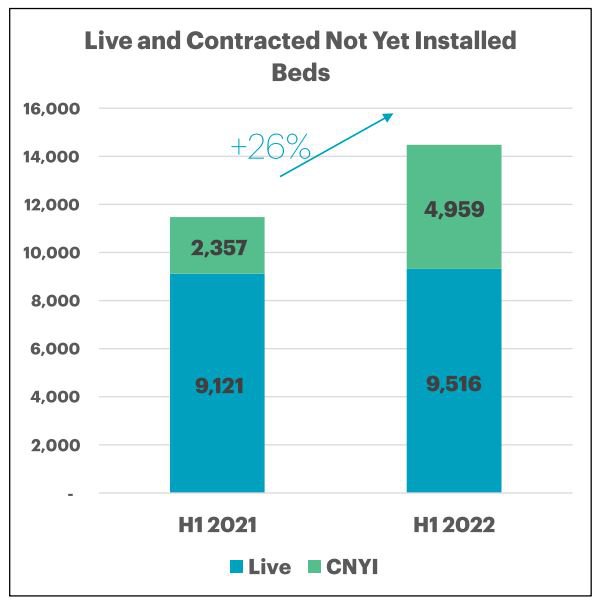

ONE is now very close to hitting our 15k contracted beds in 2022 metric:

ONE is currently sitting on 14,475 beds - another deal should push ONE over the threshold for our target contracted beds metric.

Granted, we were hoping for faster revenue growth from ONE as contracted beds started to tick up and it seems ONE had been too.

In its half yearly report, ONE revised its 2022 revenue guidance from a range of €12.5 to €14m (~A$18M - A$21M) down to €9 to €9.5M (A$13M - A$14M).

That’s a circa 30% downgrade in revenue for 2022, which ONE says comes down to timing delays on non-recurring revenue.

Think of one off hardware purchases and the like - bearing in mind that ONE still managed to clock 26% growth in the year since its 2021 half year results.

We’ve previously highlighted how many older US hospitals rely on old-fashioned set top boxes in patient rooms and how ONE was shelling out to overcome this hurdle.

Our view on ONE’s half year results is that we’re satisfied with progress, and patiently waiting for ONE to deliver in a big way in subsequent quarters.

The reason we are ok with this revised guidance is that according to ONE the revision is due to several key deals being DELAYED to 2023, which means that they should still come into next year's numbers.

Hospitals are complex, slow moving beasts and take a long time to make buying decisions or implement organisational change - which is a pain when trying to sell in technology like ONE, but on the flipside hospitals become sticky, long term customers once they have finally signed on.

In a different market environment, the focus would be more squarely on ONE’s future growth rather than its immediate results.

During the peak 2020/2021 market fever for tech stocks, ONE’s progress on users/contracted beds would likely be enough to see big funds line up to take a slice.

But inflation has played an outsized role in shifting market expectations and growth alone isn’t enough anymore, especially for tech companies like ONE.

That being said, ONE’s solution is seeing an uptick in interest, which, backed by a healthy 30 June cash balance of €10M (A$15M), we think should provide a launching pad for ONE to try and chase down a dominant position in the US market.

In other words, we anticipate ONE being on the precipice of more substantial and sustained growth — growth that could extend for years to come and into an improving secniment for tech stocks.

There are now at least 9,500 beds in ONE’s sales pipeline (RFIs/RFPs) with the company saying in its recent conference call that it expects to close on ~5k of these beds by year end.

RFIs and RFPs are formal processes for evaluating ONE’s tech for implementation in a hospital.

For a more detailed discussion of ONE’s sales pipeline and what RFIs and RFPs are - read our previous coverage.

So if ONE can make good on these numbers, that would easily smash through the 15k beds metric. What’s more, we think it would likely secure a breakthrough second positive operating cash flow quarter.

Repeat the operating cash flow positive caper a couple more times and all of a sudden, ONE’s market share push has garnered big momentum.

This would see the picture become a lot more rosy for ONE, meaning less need to tap the market for cash, and a sort of self-fulfilling prophecy where ONE is the go-to health tech solution for US hospitals. This would lead to even more US hospitals signing up, allowing for increased marketing spend that leads to more big deals.

In short, we still think ONE’s health tech solution for hospitals could spread like wildfire through the US healthcare system - and the conference call with ONE CEO James Fitter gave us a glimpse at how ONE intends to go about achieving that.

Summary of ONE conference call

A permanent link to ONE’s latest half yearly conference call (which we listened in on) can be found here.

The 35 minute call has plenty of good nuggets of information, which we’ve summarised below:

Key takeaways from the ONE conference call:

- Good pipeline of new business driven by increased sales and marketing spend.

- This pipeline includes imminent procurement decisions on ~5k beds, including high profile RFIs/RFPs, CEO James Fitter is headed to the US to present to potential clients.

- ONE had 7k beds in its network that needed coax set top box in 2020 - the biggest ever deal ONE has signed (BJC) was made possible in part by this hardware, allowing for further expansion with existing customers.

- 40% conversion of expansion opportunities - implementation hampered by supply chain, should improve.

- Nurse feedback driving new products - patient communication board being rolled out (notably at Kingman in Arizona) with the goal of freeing up nurses to provide better care.

- Revenue guidance downgrade - revenue guidance from a range of €12.5 to €14m (~A$18M - A$21M) down to €9 to €9.5M (A$13M - A$14M) due to timing delays on non-recurring revenue

- BJC expansion contract does not show up in these half year results - revenues to flow through later this calendar year.

- Opportunities in the pipeline are largely new hospital networks with upwards of 1k-2k beds being discussed - we see this lumpiness in deal flow as in keeping ONE’s usual approach, just the deal size is increasing.

- Of the ~20k beds in the sales pipeline, roughly three quarters are the more advanced RFP type, while one quarter are RFIs - CEO James Fitter classifies thecurrent crop of RFPs as serious buyers because hospitals are keenly aware of the need to change (not “tire kickers”) and renewals are not in RFP numbers.

- Hardware pricing is generally less aggressive - it's important to win the business first and then grow the lifetime value of the customer.

MST Access research note

We came across an initiation note (June 8th 2022) and an update note (August 31st 2022) from MST Access that takes an in-depth look at ONE’s progress and its financial metrics.

Here are our key takeaways from MST Access’s Initiation Coverage note (June 8th 2022):

- Launch of cloud solutions and NextGen Android products in CY21 - MST Access outlines a 60-70% reduction in hardware ownership costs which should improve ONE’s value proposition to customers.

- Projected 25% Compound Annual Growth Rate (CAGR) in live beds through to 2024.

- Free cash flow breakeven expected in FY2024 - as operating expenditure comes down.

- Significant addressable market in US - US hospitals spent US$1.39T in 2021 there are 920k beds and expenditure is going up.

- Big deals in US health tech space - Stryker’s acquisition of Vocera for US$3B in February, acquisitions are strategic given growth.

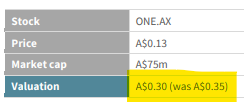

In part because of this acquisition, MST Access (as at June 8th 2022) valued ONE at 10-12x FY22 sales which would be 42-50 cents per share which in turn, implies a market cap of $217M at the lower bounds:

In a subsequent update MST Access discussed how ONE was tracking after the 1H22 results and its revised guidance.

Here are the key takeaways from MST Access’s Initiation Coverage note (August 31st 2022):

- Solid pipeline of new deals - ONE is in active expansion negotiations on ~1,900 beds across its US installed base

- Nurse time reduction metrics - time savings of between 1-12 minutes per avoided nurse call, highlighting the ability of its solutions to automate nonclinical workflows and reduce the nursing task burden

MST released a revised valuation for ONE shares:

Of course analyst predictions (including ours) cannot be relied upon alone, they are based on a number of assumptions that may not happen. M&A activity in the US health tech space could dry up, so this number should not be relied on to make any investment decisions.

It does, however, re-enforce our confidence that if ONE can close major deals in the coming months and tech sentiment stabilises or turns positive, the market would look favourably on ONE’s prospects of future growth.

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE in 2022

- Why we invested in ONE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.