Growing, growing…

Our telco Investment, Vonex (ASX:VN8) is rapidly increasing its revenue - the kind of top-line growth that may garner greater attention in the coming quarters.

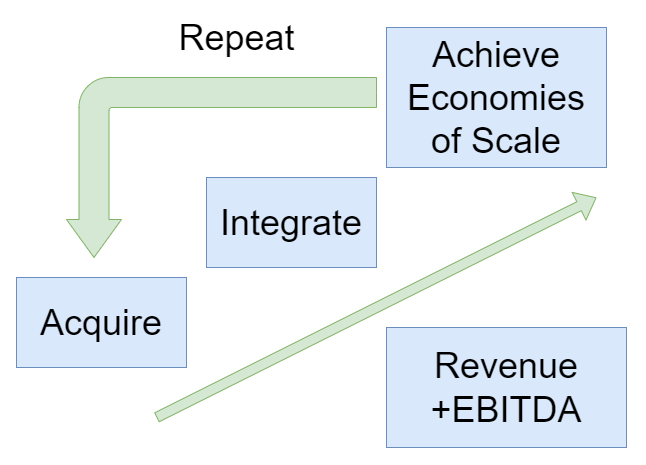

We think this is the right approach for a small-cap telco like VN8 and is part of what we view as its core strategy:

VN8 posted the following numbers in its quarterly:

- September quarter cash receipts of $10.5M up 48% Year on Year (YoY)

- Annualised recurring revenue (ARR) of ~$51M at 27 October 2022, up >60% YoY

- Operating Cash Inflows $1.6M

- Cash balance of $4.7M

Annual Recurring Revenue (ARR) is a key figure that many tech companies look towards - and acquisitions are often based around the smoothed out cashflows that ARR represents.

Assuming customer stickiness levels are high - ARR is a good basis for understanding the future trajectory (and value) of companies like VN8.

Sustained operating cashflow quarters like in Monday’s quarterly release (+$1.6M) should help as well.

While VN8 has been caught up in a broader market move away from tech, we’re hopeful that as VN8 acquisitions start to get integrated and gel, these kind of numbers can take VN8 higher up the charts.

VN8 is using mostly debt to fund its acquisitions (Longreach financing), which we think is a sensible non-dilutive move given its track record of successfully integrating acquisitions and building more efficient operations out of combined entities.

We estimated that VN8 has $22.5M in debt via the Longreach financing facility which matures in December 2024.

In our eyes, this is a good chunk of time in which VN8 can grow not only its top line revenue but also move solidly into profitability.

In short: if/when the market sentiment towards tech turns, we like VN8’s prospects.

Next up for VN8 is to complete integration of its latest acquisition, OntheNet, which should further boost revenues and EBITDA going forward.