Two offtake term sheets in two weeks.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,223,000 EMN shares at the time of publishing this article. The Company has been engaged by EMN to share our commentary on the progress of our Investment in EMN over time.

Two offtakes in two weeks.

And possibly “Strategic Project Status” at the end of the year...

Momentum is now building for our EU based critical mineral Investment Euro Manganese (ASX:EMN).

EMN is a late-stage development company with a high-purity manganese project in the Czech Republic.

High purity manganese is an important battery material for next gen batteries.

According to CPM Group, more than 90% of the world’s high purity manganese supply comes from China.

Last year, EMN signed a US$100M financing deal with Orion Resource Partners for a non-dilutive royalty over the project.

This was external validation of EMN’s project by a large private equity player willing to put their cards on the table.

Since then EMN has had two primary goals.

Offtakes AND financing.

A contract for future supply of product - offtakes firm up the financing picture because banks and other financiers need to know that there will be customers once the project gets into production.

Offtakes and financing are closely linked.

After months of wheeling and dealing, EMN has now secured TWO offtake term sheet agreements in the last two weeks and we think there is more to come.

We think that this rapid fire offtake may place pressure on other interested parties, cascading into a number of offtakes in short succession.

Ultimately, there is only so much product EMN can produce, and interested parties sitting on the sidelines may get FOMO (fear of missing out) and secure their manganese supply.

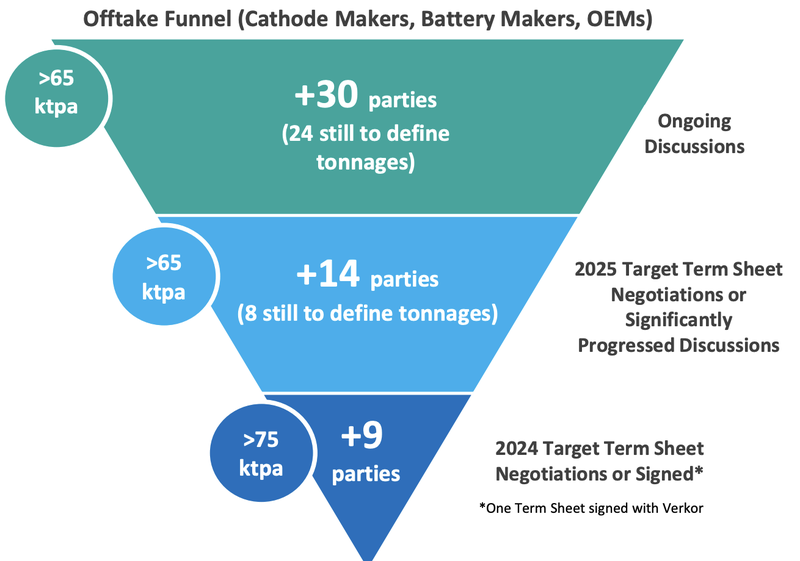

EMN says it has over 50 companies in its offtake pipeline, each at different stages of discussions (this image was from before this weeks offtake news):

What makes EMN’s manganese different from other sellers is its location within Europe.

The European Critical Minerals Act and the Inflation Reduction Act are two key pieces of legislation that encourage raw materials to be purchased from friendly nations.

Today, EMN announced that it had applied for “Strategic Project Status” under the European Critical Minerals Act... and we think it has a good shot of getting it.

This is because:

- EMN is a later stage “development ready” asset. It has completed a DFS and will benefit greatly from the project status.

- High-purity manganese is a critical mineral in the EU.

- EMN’s project is effectively a recycling project, repurposing an old tailings dam and refurbishing the site. This gives EMN very high ESG credentials.

- EMN’s project is strategically located in the Czech Republic, with key access to manufacturing hubs in Europe.

We think that this makes EMN’s manganese more valuable to potential customers and if EMN is able to successfully convey this message it should be able to sign the offtakes it needs to lock away future production.

The reason why offtakes are so important to EMN is because it unlocks the next big challenge for the company....

Project financing.

Project financing is one of the most difficult stages for any mineral development company.

The big banks, who write the big cheques, tend to have the lowest level of risk tolerance.

This is why they want to see offtake agreements and secure revenue over the project, before providing any capital to the project.

From a more immediate perspective, the next tranche of EMN’s funding is contingent on signing offtakes.

It needs to get to 40% of production committed with binding offtakes to unlock the next US$30M in funding from Orion.

These funds will reduce the total CAPEX outlay for the project, but there is still a big funding mountain to climb.

These are the CAPEX and NPV of the project from a 2022 DFS:

- An After-tax Net Present Value (NPV) of US$1.34 billion (~$1.92BN)

- An Initial CAPEX of US$757.3M (~$1.1BN) with an internal rate of return of 21.9% and a 4.1 year pay back period.

In a high interest rate environment, that’s a big CAPEX number to put together.

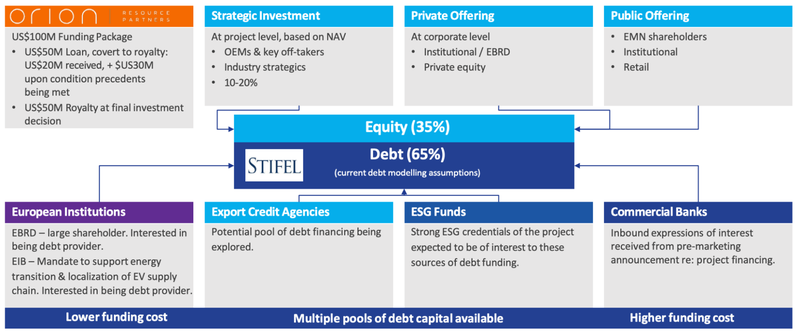

But, EMN does have a plan:

(Source)

It’s a complex web of banks, export credit agencies, equity and debt arrangements and although funding is a BIG challenge, we think that EMN will be well placed to get there.

Firstly, because it has the backing of Orion, which provides external validation of the project, but does carry risk if other elements of the complex web don’t click into place.

Secondly, because EMN’s CEO Dr. Matthew James has helped secure project financing before.

For a “little known” company called Lynas Resources...

Well, it was little known when Matthew James worked there, now Lynas is a $6.5Bn rare earths producer and one of the major mining companies in Australia.

So we are backing Matt James to do it again with manganese.

This brings us to our big bet...

Our EMN Big Bet

“EMN significantly re-rates to a $1BN+ market cap on becoming a High Purity Manganese producer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our EMN Investment Memo.

EMN project could get “Strategic Project Status”

One thing that we think will accelerate the company’s progress will be if it can secure “Strategic Project Status” with the European Commission.

“Strategic Project Status” is a new term given to projects inside Europe that the EU government see’s as important for security of supply regionally.

We think that EMN’s project fits this bill.

Today, the company announced that it submitted the application, with a determination expected to be made in December this year.

For investors, we think this application will create a catalyst for the company and a binary outcome to look forward to that, if positive, will add significant value to the project.

If granted EMN will enjoy a host of benefits including:

- Greater access to financing (on favourable terms)

- Increased potential for grant funding and support

- Accelerated and favourable permit approval process (strict 27 month permitting periods)

Ultimately, we think that EMN application will be very strong because:

- EMN is a later stage “development ready” asset. It has completed a DFS and will benefit greatly from the project status.

- High-purity manganese is a critical mineral in the EU.

- EMN’s project is effectively a recycling project, repurposing an old tailings dam and refurbishing the site. This gives EMN very high ESG credentials.

- EMN’s project is strategically located in the Czech Republic, with key access to manufacturing hubs in Europe.

A closer look at EMN’s offtake term sheets

An offtake agreement is a binding contract between a mining producer and a buyer for the future product produced (at an agreed price).

For mining companies like EMN, securing an offtake agreement is important because it provides certainty of revenue for its future production, which helps secure project financing from lenders and investors.

For buyers, it guarantees future supply of raw materials.

Offtake agreements are particularly valuable for mining projects involving commodities with less established demand.

Like high-purity manganese.

So, with that in mind, let's take a look at EMN’s two new potential offtake partners:

Blue Grass

Blue Grass is a US-based chemicals manufacturer.

The company produces various manganese-based products which are then on-sold to battery makers.

The term sheet is contingent on qualifying EMN’s manganese product within Blue Grass’ supply chain.

Pricing is based on an index-adjusted western benchmark price.

This basically means that Blue Grass could pay a premium, to source the manganese from a friendly country and a project with good ESG credentials.

This is effectively a “green premium” and something that mining companies have been talking a lot about.

“Green premiums” generally work on lower volumes and in private arrangements.

Given Blue Grass’ commitment to extremely high standards for its raw materials, it makes sense why they would pay the premium for EMN’s manganese.

This cost will likely be passed on to their customers (and a point of difference for the company).

In order to finalise the deal Blue Grass needs to “qualify” EMN’s manganese.

Now that EMN has its Demonstration Plant up and running, it will send samples over to Blue Grass to test and confirm the quality of the product.

It is important to note that no tonnage numbers were published by EMN (likely so that it didn’t lose bargaining power with other potential customers).

However, the tonnages will become clear when the deal is binding.

Wildcat Delivery Technologies

Wildcat Delivery Technologies is a cathode manufacturer based in California, US.

Its goal is to create a nickel-free and cobalt-free battery for Electric Vehicles.

The deal signed with EMN is again for 7 years worth of manganese production.

The deal is contingent on Wildcat constructing its US plant which is expected to be complete at the back end of 2026.

This timing aligns with EMN’s manganese production timelines.

EMN’s offtake strategy

EMN’s strategy is to secure non-binding offtake term sheets with several companies (and hopefully have more than enough to fill future production).

Our hope is that now that a few deals have been announced, more companies will sign term sheets with EMN in order to secure supply.

Ideally, EMN would be oversupplied with non-binding offtake agreements for a buffer in case any of the deals fall through.

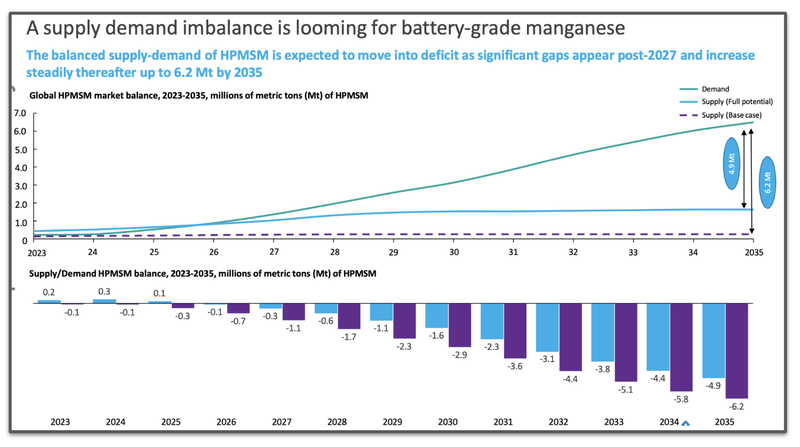

Ultimately, there is only so much production that EMN can sell, and a supply/demand imbalance is looming for battery-grade manganese.

EMN’s pitch is that buyers will need to secure their manganese supply soon so that they don’t scramble for raw materials and just buy from China, which dominates the high purity manganese market.

Thus, forgoing any tax credits from the EU or the US.

We think that this pitch has been harnessed over the last twelve months and now we are starting to see results through these offtake deals.

Where is EMN’s project at?

Our Investment journey in EMN has been a bit of a rollercoaster.

We first Invested in EMN in 2020 at 6.5 cents just at the start of the critical minerals bull market.

The company’s share price hit a high of 96.5 cents during that time but has since come off significantly and now it trades less than our initial entry price at around ~4.5 cents.

Across the board, critical minerals projects have been out of favour, with lithium in particular suffering.

However the manganese price has grown (primarily driven by a short term supply shock when a cyclone hit the largest manganese mine in Australia).

Australia is the world's 3rd largest producer of Manganese and that mine alone accounted for ~11.5% of global supply...

(Source)

Despite a relatively strong backdrop for the manganese sector EMN’s share price has come off a long way from its highe.

What we think has affected EMN the most is the challenges faced by most late-stage development companies.

Slow to get offtakes and slow to get financing.

These are the two key project risks that sit around EMN and it can often be a chicken or the egg problem.

Banks will be reluctant to lend to companies that don’t have a guaranteed future cash flows (offtakes) and offtake agreements don’t want to lock in their future supply with a company that hasn’t yet secured financing to reach production.

When this happens, investors generally leave the stock to chase companies with more imminent news and catalysts with more predictable timing.

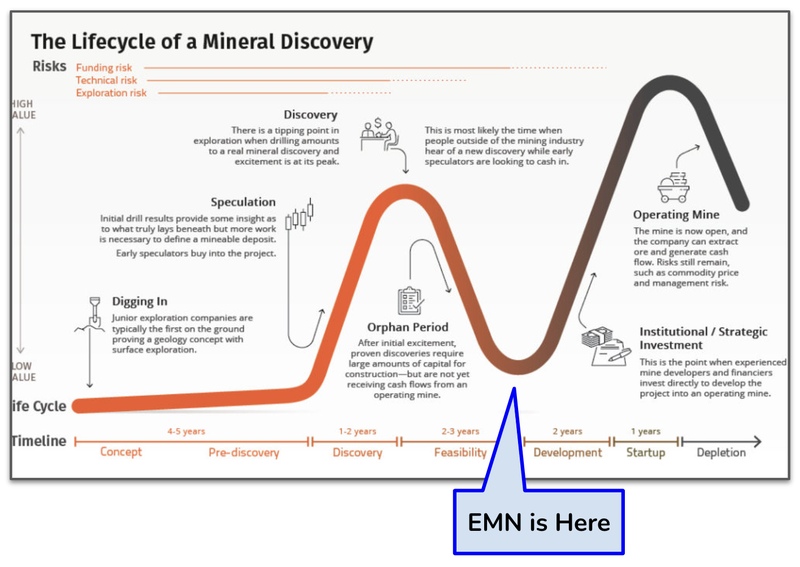

This is typical of development stage companies that sit in the “financing” purgatory between the final feasibility study and a final investment decision.

However, once the offtakes and the financing is secured then the stock will generally re-rate (and it can happen fast), as it moves towards production.

This pattern is best shown by the Lassonde Curve.

This curve is designed by Canadian mining executive Pierre Lassonde, and shows the typical share price cycle for mining companies.

It outlines how mining company share prices tend to:

- Rise sharply after an initial discovery, then

- Decline during resource definition and feasibility studies before,

- Rising again as the company moves into production.

For these companies, when the momentum turns, it turns quickly.

We are hoping that these two offtake agreements for EMN are a sign of momentum to come for EMN and it will be a strong next 12 months for the company.

What is next for EMN?

Offtakes, Offtakes, Offtakes

The main name of the game for EMN is... you guessed it, offtakes.

These are key deals that will unlock the next round of funding for EMN as well as provide confidence for project financiers to get behind the stock.

Results of application for “Strategic Project Status”

In December we will know whether EMN has been successful in securing strategic project status for its HPM project in the Czech Republic.

We think that this could be a key catalyst for the company with a predictable timeframe and binary result...

The exact kind that we like as Investors.

What could go wrong?

Sales / Offtake

EMN is selling a specialised commodity.

There is a lot of education that the company needs to do in order to explain the value of securing high-purity manganese supply.

Product qualification processes can also take time, and EMN has experienced delays in the past.

If EMN is unable to sell its product, then banks will be reluctant to lend money to the company in order to finance the project.

In addition, there is another US$30M worth of funding that EMN will unlock once it hits 40% production. If this milestone is not achieved, then the prospects of EMN succeeding will be difficult.

Our EMN Investment Memo

Click this link to access our investment memo for EMN which includes:

- Key objectives for EMN

- Why we invested in EMN

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.