EMN pulls in US$100M in non-dilutive funding for high purity manganese project

We don't see these kinds of funding deals come along often - especially for $42M capped companies.

The size of this funding round is more than 3 times the company’s last traded market cap.

Our high purity manganese Investment Euro Manganese (ASX:EMN) just signed definitive agreements for US$100M in non-dilutive funding to help build a strategically important battery materials project in Europe.

EMN was capped at $42M before today’s news.

Europe needs EMN’s high purity manganese for its Electric Vehicle battery market... it's the only sizeable resource of manganese in the entire EU.

High manganese battery chemistries allow battery makers to strip out some of the costs associated with other battery metals like nickel and cobalt.

All the major players in EVs have announced intentions to use more high purity manganese in their battery chemistry - VW, Tesla, GM, Mercedes and Stellantis.

According to CPM Group, more than 90% of the world’s high purity manganese supply comes from China.

Previously, EMN had said they were negotiating with parties which had demand for over 100% of EMN’s annual production capacity.

And then like magic, we have a deal.

Here’s the quick version of today’s funding agreement:

- US$100M ($151M) - A US$50M loan facility with a 12% per annum interest rate, convertible into a 1.29-1.65% royalty on project revenues.

- US$20M on closing, expected by the end of this month.

- US$30M received on milestones before final investment decision (FID).

- A further US$50M in exchange for a 1.93-2.47% royalty on project revenues following a final investment decision (FID).

- Major financier - the financier is Orion Resource Partners Group, a US$8.2BN asset management firm based in New York.

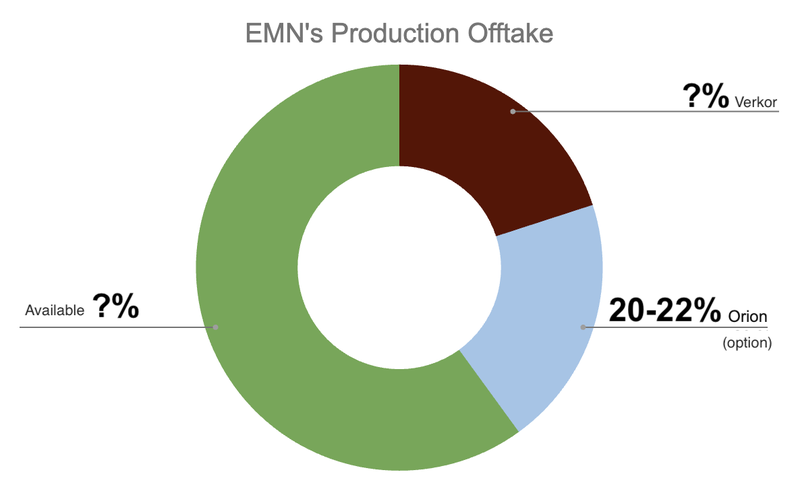

- Offtake option - Orion has an off-take option of between 20-22.5% of the Project’s high-purity manganese total production for a term of 10 years from first delivery.

- Non-dilutive - EMN is exchanging royalties from future revenue for access to funding. We think it is by far the most sensible funding agreement in the current circumstances - a major immediate win for EMN.

- Imminent funding boost sets up EMN to accelerate development - with US$20M due on closing in the next few days, EMN can move much quicker in the development of its project. It's now much better funded to do all important work like securing permits and marketing its products to potential customers.

That’s correct, US$20M from Orion is going to imminently hit EMN’s coffers, and the company was capped at just $42M prior to today’s news.

We think that imminent cash hit should not just help EMN from an operational perspective, but also very quickly change the valuation calculus for the market (re-rate) AND underpin the company's valuation moving forward in a market that is crying out for more capital.

Again, the impact of this agreement has already been felt in Canada, where EMN’s TSX-V listed shares traded up as much as ~111% at one point in overnight trading.

Quick re-cap: EMN’s projects

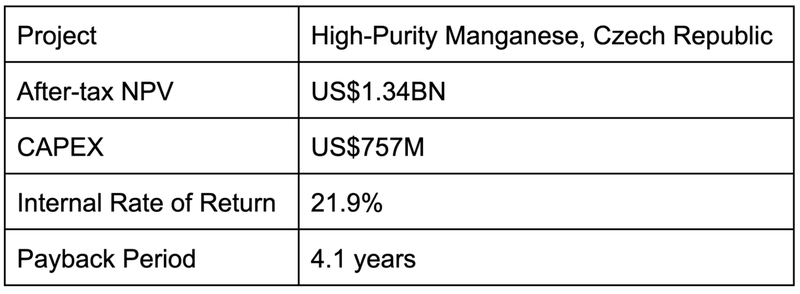

High Purity Manganese Development, Czech Republic

EMN’s main project is a mine tailings rehabilitation development in the Czech Republic, which is the largest manganese resource in the EU.

This is the project that Orion has just committed US$100M into funding.

In August of last year, EMN released a DFS for that project with the following economics:

You can read our full take on the DFS here: EMN DFS delivers US$1.34 billion post-tax Net Present Value

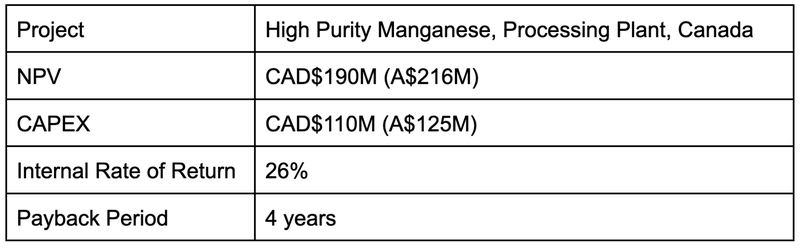

High-Purity Manganese Processing Plant, Quebec, Canada

EMN is also working on a second project - with plans for a high purity manganese plant in the rapidly emerging Becancour battery hub in Quebec, Canada.

In August of this year, EMN released a scoping study with the following economics for that project:

You can read our full take on the Scoping Study here: EMN’s North American battery metals push gathers steam

With two economically viable projects, we think that EMN is well placed to take advantage of the global energy transition and particularly the “friendshoring” of critical raw minerals that is taking place in both the EU and North America.

EMN’s pathway to project financing

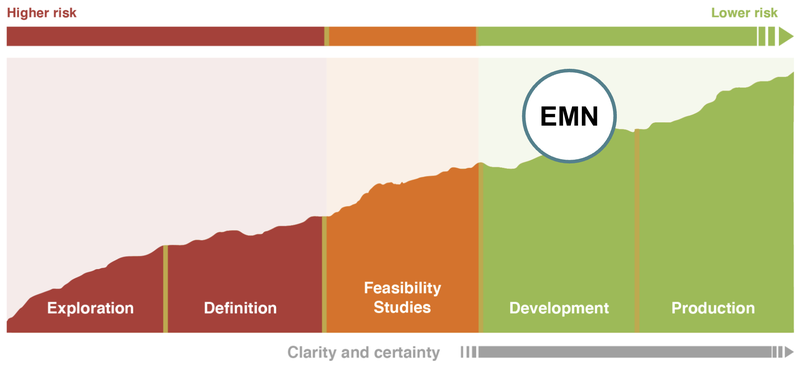

EMN is a later stage development company, this means that project financing can look quite different to typical exploration projects.

The company has completed its DFS and is moving through the “development” stage of the mining company lifecycle - key milestones are related to securing offtake partners, funding and key permits for its project:

We’ve seen small companies across the mining company lifecycle raise capital at steep discounts often with various free-attaching options just to sustain themselves in the recent rough market.

But we think EMN has effectively pulled a rabbit out of the hat with today’s deal.

Non-dilutive funding is golden right now, and EMN has secured it.

What’s more, with one financier locked away EMN has now taken a major step towards production of its high purity manganese project which has a US$1.34BN NPV, and chipped away at its US$757M CAPEX for the project.

It’s a signal of intent from EMN and Orion, and we expect more financiers will start to line up to get a piece of the project.

Previously, EMN had said they were negotiating with parties which had demand for over 100% of EMN’s annual production capacity.

The company had already signed a non-binding offtake term sheet with French battery manufacturer Verkor in January of this year.

So EMN now has at least two potential offtakers in the building - one of which is now ponying up to ensure the project gets off the ground and they have a chance to get a piece of it.

As the manganese offtake pie shrinks, we expect offtakers to become increasingly serious about their offers and financing to become more easily secured.

It’s a carefully crafted process - led by EMN’s President and CEO Matt James and his team who have really delivered today.

Today’s news is a large step forward towards our EMN Big Bet:

Our Big Bet for EMN:

“EMN significantly re-rates to a $1BN+ market cap on becoming a High Purity Manganese producer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our EMN Investment Memo.

While the market is yet to really take off again, there’s precedent for the type of company re-rate that we reference in our Big Bet.

One such company was Lynas Rare Earths, which achieved a peak market cap of more than $10BN over a few market cycles.

By transitioning to becoming a producer, Lynas effectively was the first large scale non-China source of rare earths - minerals now widely recognised as crucial to the energy transition.

Noting that EMN’s current CEO Matt James is a Lynas alumni, we want to see him bring all his experience and networks he picked up in his time there, into spearheading EMN into production too.

Today, we’ve got more on:

- Who is EMN’s financing partner, Orion?

- Why is high purity manganese so important to EVs?

- The EU Critical Raw Materials Act

- What has EMN done since our last note?

- Risks

- Our EMN Investment Memo

Who is EMN’s financing partner, Orion?

Founded in 2004, Orion Resource Partners Group manages US$8.2BN for institutional investors, with its headquarters in New York and five other offices in Denver, London, Sydney, Melbourne and San Francisco.

Orion has previously helped fund a range of development projects such as:

- US$110M loan facility for ASX-listed Sheffield Resources.

- US$25M funding package for Andrada Mining which has a Namibian lithium, tin and tantalum project.

- US$55M funding package for Nordic Mining.

All of these developments happened in the last 18 months - so it seems clear to us that Orion is intent on deploying capital at a time when the market is struggling.

Why is high purity manganese so important to EVs?

Investors began to pay attention to manganese (specifically High Purity Manganese like EMN’s) when Elon Musk dropped the word “manganese” in a 2020 Battery Day presentation.

(Source)

The significance of high manganese battery chemistries is that they allow battery makers to strip out some of the costs associated with other battery metals like nickel and cobalt.

Car makers are looking for the best bang for buck when it comes to battery chemistry make up.

Previously, all the major players in EVs announced their intentions to use more high purity manganese in their battery chemistry - VW, Tesla, GM, Mercedes and Stellantis.

EMN’s project is ambitious — big enough that it could help drive down the cost of batteries in the West.

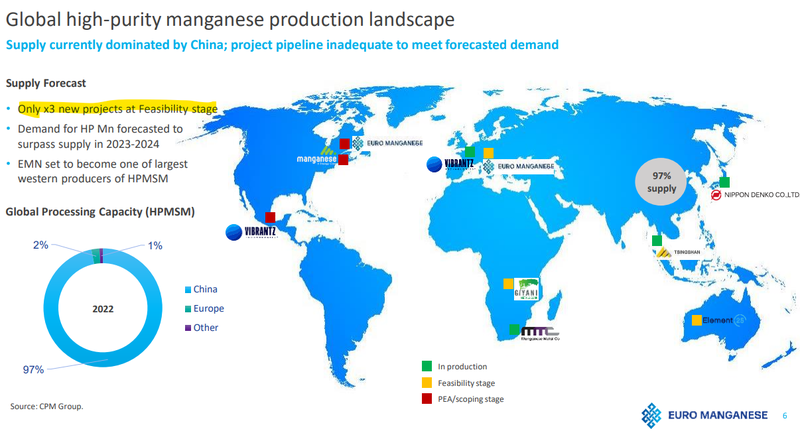

It will also enable both Europe and North America to secure their own supply at a time when China supplies over 90% of the global high purity manganese market, and roughly 97% of the processing capacity.

There are only a handful of projects outside of China that could help meet the demand for ex-China supply at a time when demand is rising more generally.

And as of a few months ago, there are only three projects at the feasibility stage, one of which is EMN’s project in the Czech Republic:

(Source)

We think this means that as project financing accelerates for EMN, the speed to market could mean that the company could charge a premium for its products and an upside economics scenario could be realised.

EU Updates its Critical Raw Materials Act

Last week the European Union proposed updated legislation to the Critical Raw Materials Act.

This piece of legislation is the EU equivalent to the Inflation Reduction Act that spawned a rush of critical minerals explorers in North America.

Importantly, the EU has set a framework for permits to be granted for critical minerals projects by setting time limits on how long these permits can drag on for.

A key term in recently agreed changes to the Critical Raw Materials Act limits permitting processes to 27 months for extraction projects and 15 months for processing and recycling projects.

(Source)

For large scale investors in development-stage companies like EMN, these time limits provide a significant degree of certainty over the maximum amount of time that the company will need to wait until a permit is granted.

It also accelerates the permitting processes and means that projects are not left stranded due to excessive bureaucracy.

We think that this particular change will unlock stalled investment decisions as seen today with EMN’s deal with Orion.

Another key change to the legislation that was proposed was that the EU will increase its target for recycled critical minerals from 15% to 25%.

EMN’s manganese project is not a mining project, but rather a tailing rehabilitation project, as the company utilises mine tailings (waste products from an old mine) for its manganese input.

This has a range of environmental benefits and strengthens EMN’s ESG credentials.

It is possible that the project could be viewed increasingly favourably by the EU as it fits into the EU’s agenda to onshore critical minerals projects.

(Source)

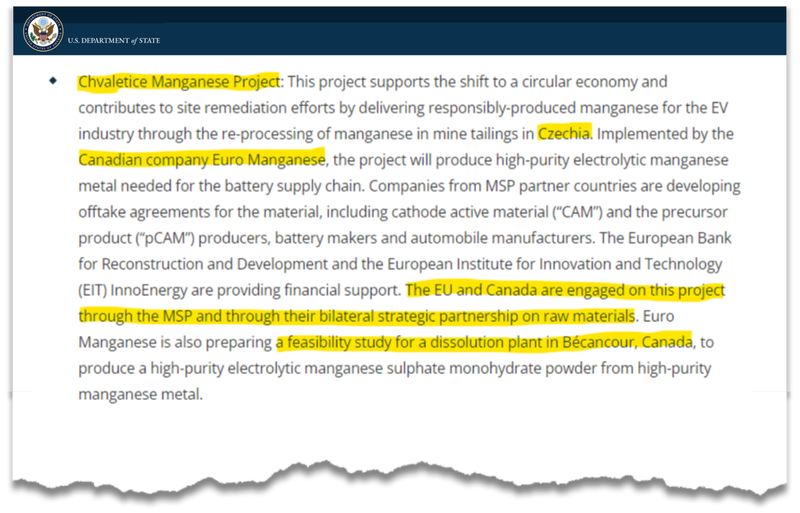

Indeed, EMN was given special mention by a newly formed intergovernmental body called the Minerals Security Partnership (MSP).

The MSP is an alliance of 13 countries and the EU that was created with the goal of encouraging public and private sector investment in the critical minerals supply chain with a particular focus on sourcing minerals from companies with high ESG standards.

In a October press release following a meeting of the MSP in the UK, EMN got plenty of attention from the alliance:

Below is an excerpt from the press release (we also like that EMN’s project was the first mentioned):

(Source)

Ultimately, we think the impending regulatory changes and increasing awareness from intergovernmental bodies like the MSP bode well for EMN as clarity around project permitting is advanced and the company’s importance to the EU grows.

What has EMN done since our last note?

Euro Manganese Produces Sulphate Product - November

EMN announced that it had produced its first “sulphate” product from its demonstration plant.

This was important because high-purity manganese sulphate monohydrate HPMSM is the more desirable product. We said we thought there would be three flow on effects from the sulphate product:

- Gets the product it into the hands of more potential customers

- Which in turn could ratchet up offtake discussions

- Which could further help underpin project financing

And it clearly seems to have been the case as today’s financing was announced just two weeks after EMN made this breakthrough.

EMN completes Land Access Agreement with CEZ - October

Land access is crucial to EMN’s plans for the project in the Czech Republic, and this agreement with the Czech energy company (CEZ) sees EMN get land access to 60% of the Proven and Probable manganese Reserves in the Chvaletice tailings area.

EMN has now secured access to 85% of the total reserves of the project.

EMN's Manganese Project selected for Inter-Governmental Support - October

This was a big one - the Chvaletice project in the Czech Republic was announced as a project to be supported under the inter-governmental Minerals Security Partnership.

The Minerals Security Partnership (MSP) is an alliance of 13 countries and the EU that was created with the goal of encouraging public and private sector investment in the critical minerals supply chain with a particular focus on sourcing minerals from companies with high ESG standards.

This level of government support could have helped firm up Orion’s commitment to funding.

EMN awards EPCM contract, gives permitting update - July

EMN announced that it had awarded a Engineering, Procurement, and Construction Management (EPCM) contract to Wood Australia. We said that the award’s 12 month horizon indicates that EMN feels it can wrap up the financing and permitting quickly. So this was an early indicator of momentum behind the project.

What could go wrong for EMN?

Product risk - EMN needs to get its high purity manganese products, particularly the sulphate product into customers hands. These products will need to be qualified for use in EV batteries.

Development risk - EMN’s Czech Republic project is in the development stage which means it could face delays if regulatory, permitting, or financing requirements are not met (see below).

Regulatory/permitting risks - EMN is making good progress on its permitting needs and although this should speed up with additional moves from government bodies, there’s always a chance that jurisdictions drag their feet.

Market risk - prior to today, market risk played out for EMN, with the share price sliding over a sustained period.

Financing risk - while today’s news is a welcome de-risking event in terms of financing risk, EMN will need to secure additional capital to fund its two projects.

To see all of our risks in detail for EMN read our EMN Investment Memo.

Our EMN Investment Memo

Click this link to access our 2022 investment memo for EMN which includes:

- Key objectives for EMN in 2022 (shown above)

- Why we invested in EMN

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.