EMN DFS delivers US$1.34 billion post-tax Net Present Value

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,630,000 EMN shares at the time of publication. S3 Consortium Pty Ltd has been engaged by EMN to share our commentary and opinion on the progress of our Investment in EMN over time.

While other battery metals like nickel and lithium get the limelight, we think there’s a battery metal that could quickly garner more attention.

Today we’re talking about manganese - in particular, high purity manganese.

Our European battery metals Investment Euro Manganese (ASX:EMN) released its long awaited Definitive Feasibility Study (DFS) last week, giving us an in-depth look at the metrics behind EMN’s high purity manganese project in the Czech Republic.

To give you a sense of the scale of the project - its after-tax Net Present Value (NPV) sits at US$1.34B ($1.92B) - more than 16 times EMN’s current market cap (~$118M).

NPV is used to analyse the profitability of a future project - a measure of what today’s capital could bring in terms of future capital.

We first Invested in EMN in 2020 after our success in European based battery metals with Vulcan Energy Resources.

While Vulcan delivered many milestones during 2020 and 2021, leading to a sustained material share price re-rate, EMN was slow to deliver material progress during the strong market.

EMN’s progress over the last 2 years has been a stop-start affair, with a lack of consistent newsflow, difficulties with Demonstration Plant procurement and a change of leadership all playing a role.

EMN’s financial metrics are now out in the market AND their new CEO is 8 months into the role.

This should help the company pick up the pace in the coming months, which is great timing with positive sentiment now seeping back into the market.

We’ve seen the positive effect having a DFS or PFS can have on a share price before.

When our best performing European battery metals Investment Vulcan Energy Resources released its PFS, the share price closed at $6.44 leaving it with a market cap of ~$514M.

Vulcan’s PFS outlined a €2.25B post-tax NPV ($3.29B) and the company’s post tax NPV was roughly six times larger than its market cap on the day.

And we remember well what happened in the wake of those PFS numbers coming out - a procession of offtake deals, a $200M placement and a share price run that took Vulcan shares to an all time high of $16.65.

Will some version of these events play out with EMN? Time will tell. With EMN’s DFS, things are a bit different - the market has taken a savage beating over the last six months and high purity manganese doesn’t have quite the same investment profile as the now glamorous lithium.

And yet, there’s a case to be made for EMN approaching an important inflection point.

After appointing new President and CEO Matthew James in December 2021, we’re now starting to get a good sense for what James is bringing to the position.

We have already seen the pace of progress increase after just a few months.

Our view is that James has a deep understanding of what it takes to bring a resource into production. As EVP of Strategy and Corporate Communications, James helped Australia’s leading rare earth company secure project financing (Lynas Corp, capped at ~$8B).

We’re hoping James can apply the same financing nous from his role at Lynas, this time with EMN - and so far we have been impressed.

The delivery of the DFS is a major part of EMN’s bid to secure financing for its high purity manganese project in the Czech Republic - where EMN will convert an old tailings deposit into new battery metals for the European EV industry.

As such, EMN is not a mining company. It is best understood as a recycling + processing company.

And this makes sense, manganese is a plentiful metal usually used in making steel, but in order to be used in EV batteries it has to be processed to a high purity and this is where the future supply bottleneck exists.

In today’s note, we’ll take a closer look at EMN’s DFS, the products the company will sell, the manganese market and what EMN needs to do to bring the project into reality, including risks.

Here are our six key takeaways following the EMN DFS release:

- Strong numbers (big NPV relative to market cap and higher capex offset by good payback period)

- Excellent ESG credentials backed by recent life cycle assessment (LCA)

- Strong numbers + ESG credentials should make EMN’s project attractive to BOTH project financiers AND offtakers

- EMN likely has a healthy chunk of cash on hand (~$35.8M at 31 March, March quarter’s cash burn was ~$3.6M, 30 June quarterly imminent)

- That cash gives EMN the breathing room it needs to build competitive tension around offtake and project financing

- Europe NEEDS this project more than ever - high purity manganese is essential to the continent’s EV push

On that final point, we’re of the view Europe will need high purity manganese if it is to build out its EV manufacturing capacity.

EMN is ideally situated within EU borders (Czech Republic) and after the recently released life cycle assessment, has the ESG credentials that offtakers need in their supply chain.

The release of the DFS last week means EMN has now ticked off Objective #2 in our EMN Investment Memo:

Here’s what the DFS means for EMN.

More on the Definitive Feasibility Study (DFS):

The significance of EMN delivering a DFS is that it has now laid out the full financial picture for the project economics of its manganese project.

A DFS is second only to a bankable feasibility study (BFS) in terms of accuracy for costings and projections, and typically projects that are at the DFS stage can get project funding without having to go a step further and complete a more detailed study.

These studies typically look to put project economics on paper up to a level of accuracy set between +/-5-20%.

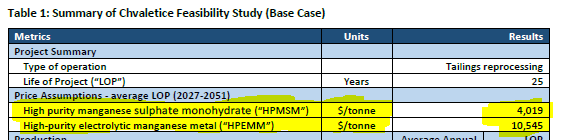

With that in mind, the following were two important numbers from EMN’s DFS:

- After-tax Net Present Value (NPV) of US$1.34 billion ($1.92B)

- Initial CAPEX of US$757.3M (~$1.1B) with an internal rate of return of 21.9% and a 4.1 year pay back period.

First, the after tax Net Present Value (NPV) of US$1.34 billion ($1.92B).

Based on the 25-year mine life that EMN put out, that yields an after tax NPV that is currently 16x more than the company’s current market cap.

This was almost 130% higher than the after-tax NPV released in the company’s preliminary economic assessment released in 2019.

Interestingly, this was done using manganese sale prices of US$4,019 per tonne for (HPMSM) and US$10,545 per tonne for (HPEMM) - we’ve got more on what these two products are later in this note.

The HPMSM pricing was determined using Chinese equivalent prices and adding transport costs into Europe plus a 15-25% premium for the product's ESG credentials.

More importantly though, the base pricing covered products with varying purities which are unable to meet the European EV battery producers specifications.

With so much investment going into downstream battery manufacturing facilities in the European Union we think the DFS estimates are conservative especially given EMN’s project is the largest manganese resource in the EU.

With the critical minerals thematic gaining traction, we think the strategic importance of EMN’s resource will mean it can demand a far bigger premium for its product.

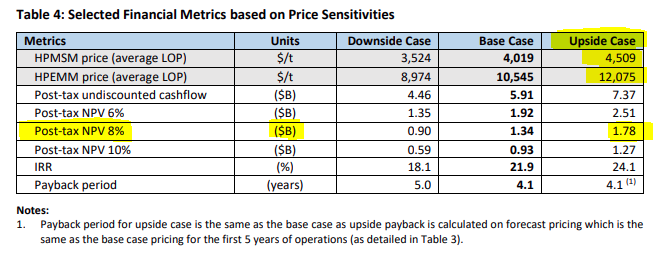

Looking at the “upside case” for pricing in EMN’s DFS, the project’s after-tax NPV increases to US$1.78 billion (~$2.56B).

With the increased adoption of electric vehicles (EVs), demand for HPMSM and HPEMM is expected to increase by almost 30X by 2036.

The market is expected to be in deficit in 2031 by ~475kt of manganese equivalent and if battery demand continues to grow as expected the deficit would increase to 1 million tonnes by 2037.

These factors are likely to contribute to increased prices for EMN’s products and could take the eventual financial outcome for EMN closer to the upside case. Or beyond.

Our second financial metric is project CAPEX.

EMN’s DFS highlighted a US$757.3M total upfront cost (CAPEX) figure which is a ~US$350M increase on the previous preliminary economic assessment put out in 2019.

At first glance the CAPEX looks to have increased substantially, but more importantly, the project economics have stayed relatively strong with a 21.9% internal rate of return.

The high internal rate of return means the project has a low payback period of just 4.1 years on an after-tax basis.

The upfront CAPEX for a project can be the biggest hurdle for any company looking to put its project into production.

Usually financiers will look for as small a payback period as possible - generating a fast return on capital is always a priority.

From experience, with most financing packages being structured in the sweet spot between 3-5 years, EMN’s project fits in well here and offers an AFTER-TAX payback period of 4.1 years.

This in essence means that all of the project financing could be repaid after only four years of operations.

But potential financiers won’t just be looking at the capital return on offer - they also want to know they are backing a project that has the ESG credentials to satisfy an ever growing multi-trillion dollar pool of ESG funds.

Below you can see EMN’s latest ESG disclosure report from Socialsuite ESG, or click here to view it online:

Life cycle assessment paving way for offtake discussions?

Only a week after the DFS announcement, EMN put out the results from its “Life Cycle Assessment” (LCA) study.

The LCA basically looks to review and then measure the carbon footprint of EMN’s project from the start of the project's lifecycle all the way through to the end.

Interestingly, EMN’s LCA was done by the same environmental consultants (Minviro) who completed the study for two of our other European battery metals Investments - Vulcan Energy Resources and European Metals Holdings.

Below are our key takeaways from EMN’s LCA announcement:

- 100% renewable energy to be sourced - EMN plans to secure 100% of the project's energy from wind and solar. This would produce only half the emissions per kg of high purity manganese produced than if EMN were to plug into the existing Czech electricity grid.

- Rehabilitation benefits - The report also touches on the environmental benefits from remediation of the historic tailings areas. This comes about because of the inherent benefits of the project being based around an old tailings deposit.

- Optimisation opportunities - The study also highlighted opportunities to reduce the project's carbon footprint by rethinking its supply chain so as to purchase inputs from companies with strong ESG credentials.

Why do these matter?

The timing of the LCA coincides with the completion of the DFS.

This puts EMN in a position to approach potential offtake partners with all of the financial metrics detailed and the ESG credentials for its project laid out via an independent third party assessment.

EMN actually mentioned this in its LCA announcement on Wednesday, commenting on how this positions the company well as it looks to engage with customers in the EV space who are looking to secure supplies of ESG-centric battery metals right the way down the supply chain.

We’re finding that what the carmakers are saying and doing is consistent. European automaker Stellantis recently let its actions do the talking by investing $76M into our Portfolio company Vulcan Energy Resources.

In short, we genuinely think an equity stake in EMN from an EV manufacturer is a legitimate possibility down the track.

The key differentiator for Vulcan being its Zero-Carbon Lithium project.

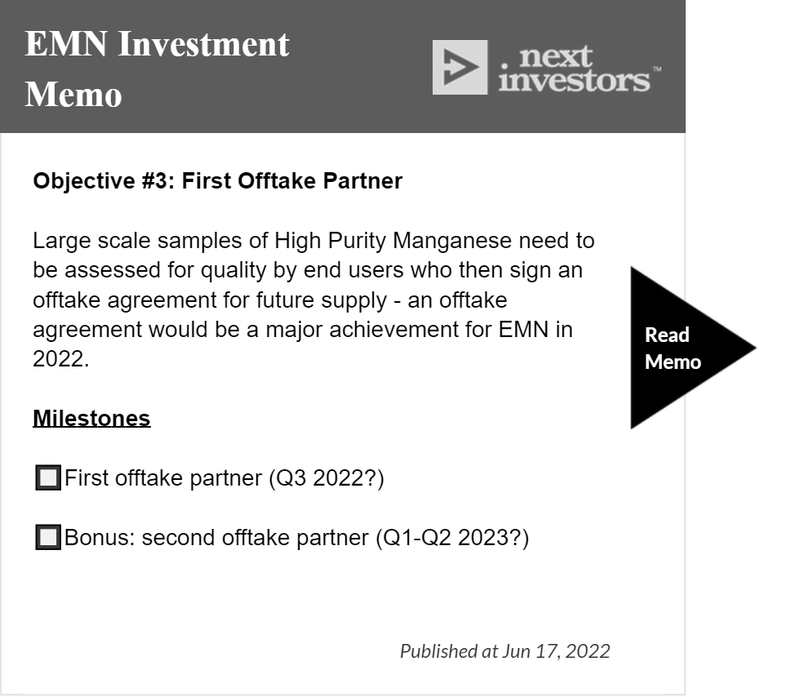

We hope EMN’s focus on proving its project’s ESG credentials will help it secure something similar and position the company to deliver on Objective #3 of our 2022 EMN Investment Memo:

What products will EMN sell?

There are two types of high purity manganese products outlined in EMN’s DFS — high-purity manganese sulphate monohydrate (HPMSM) and high-purity electrolytic manganese metal (HPEMM).

These two high purity manganese products have different use cases and look like this:

As you can see, the HPMSM (sulphate) looks like salt while HPEMM (metal) is a flake. It is the sulphate product that we’re really interested in here as it will make up the bulk of EMN’s output.

Around two thirds of EMN’s output in terms of tonnes will be the sulphate product, with the remaining third the metal product.

HPEMM can be converted into sulphate by other high purity manganese producers. But EMN will retain some optionality here and can adjust output according to market needs.

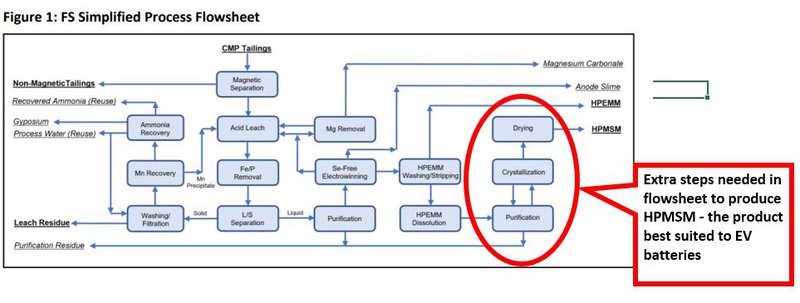

HPMSM requires a bit more work to produce, as you can see in the flowsheet from the DFS:

Remembering that this is a tailings deposit (leftovers from an old mine operation in the 1930s), the flow sheet has the added benefit of getting rid of the environmental mess that the old mine left behind.

Key point: EMN is not a “mining company” - it is best understood as a “recycling + processing company”.

EMN’s flowsheet is based on a crucial built-in assumption - there are likely to be only six non-Chinese HPMSM projects that could come online by 2030.

That’s the upside assumption.

It also assumes supply coming from recycling batteries and an increase in Chinese supply.

Those are the downside assumptions.

Which brings us to why location is such an important part of EMN’s future prospects.

Here’s why Europe needs EMN’s manganese

Over the coming decades manganese-containing battery chemistries are expected to dominate the battery market amid the widespread commercialisation of high-manganese batteries.

Manganese is currently largely used by the steel industry, but in the years ahead it is expected to feature in the cathodes of most lithium-ion batteries.

High-purity manganese suitable for the battery market currently makes up less than 0.5% of the 22 million tonne global manganese market... but the EV revolution is radically transforming this market.

Leading independent commodities market research firm, CPM Group, which has expertise in high-purity manganese, expects 8 million battery EVs to be built in 2022 and a projected 150 million to be built every year by 2030.

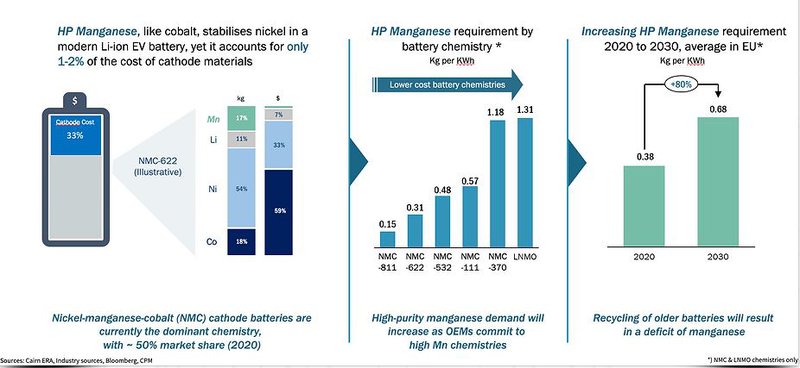

Some of these battery packs weigh up to 500kg, with 100kg of that being manganese and in the coming years, battery producers will likely look to reduce their cobalt and nickel content and increase manganese consumption. This may be due in part to cobalt’s association with less than stellar ESG mining practices and nickel’s persistently elevated price.

We are particularly drawn to this chart from EMN that shows how the move to higher manganese content could strip out some of the costs for EV manufacturers:

CPM Group forecast a 30-fold increase in the use of manganese in EV batteries in the 15 years from 2021 to 2036. This translates to a forecast deficit in 2031 of 475kt Mn equivalent.

But if battery demand keeps growing as expected and no additional projects come to the market, that deficit could reach 1 million tonnes by 2037. This is not unrealistic as global car makers including Tesla, Volkswagen, Stellantis, and Renault have each announced moves to batteries with high manganese content.

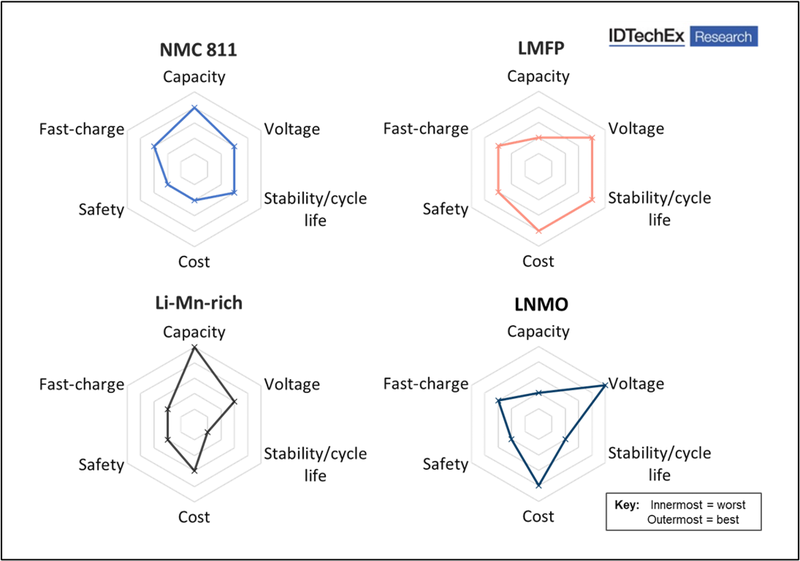

Below are the various performance metrics for high manganese EV batteries — NMC (nickel-manganese-cobalt), LMFP (lithium-manganese-iron phosphate), Li-Mn-rich (lithium-manganese rich NMC), LNMO (lithium-nickel-manganese oxide):

There’s plenty of manganese in the world (around 300 years worth) - just not much capacity to get it up to scratch for EV batteries.

The supply constraint ultimately comes down to high-purity refining capacity.

With its Pilot Plant, EMN was able to demonstrate that reprocessing the tailings can produce battery-grade manganese products that meet the specifications of the most demanding battery customers.

The trick is now to scale up that process with the Demonstration Plant.

Once again, the company’s location in Europe also can not be overstated. EMN stands to become the only significant primary producer of battery grade manganese products in Europe, helping to improve the security of Europe’s battery raw material supply.

This comes in the context that Europe currently imports 100% of its manganese requirements with China supplying over 90% of the global high purity manganese market.

What’s next for EMN?

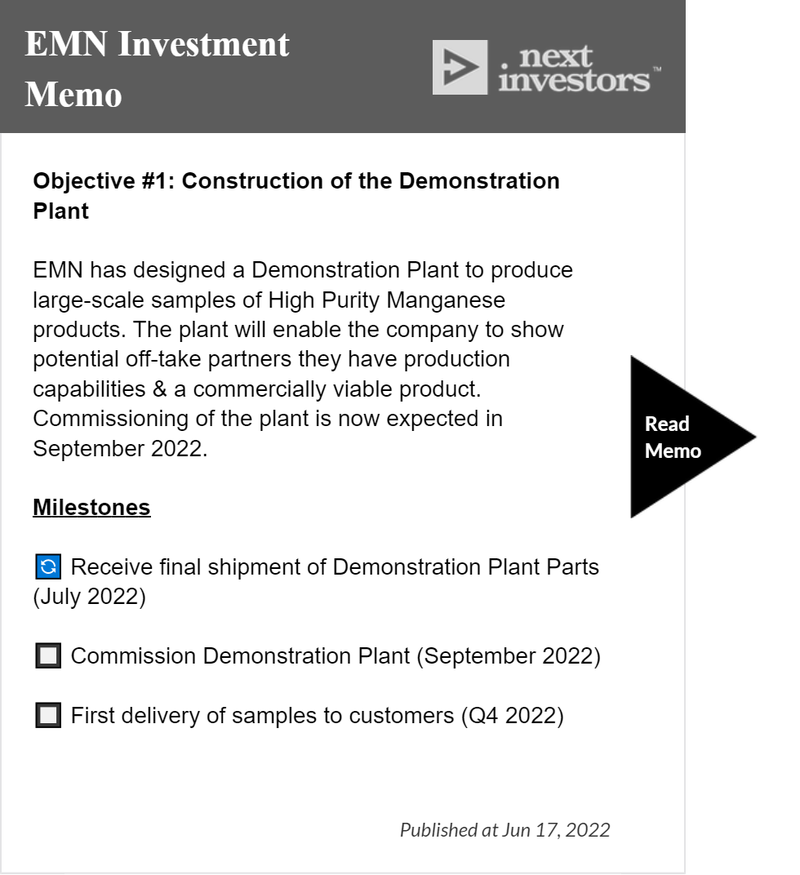

Our eyes are firmly fixed on the construction of the Demonstration Plant our #1 Objective for EMN:

The product qualification work that stems from the commissioning of the Demonstration Plant should prove crucial in offtake discussions as it would prove out the viability of EMN’s product at scale - a 7X scale-up of EMN’s successful existing Pilot Plant.

The Demonstration Plant had to be shipped via sea freight from China because the rail option was impacted by the ongoing conflict in Ukraine.

The shipment is coming via the port of Hamburg, which is currently facing a strike by port workers - which may explain the delay in EMN receiving the parts for the Demonstration Plant.

Below is a video of what the Demonstration Plant looks like:

Despite the potential for delays in the Demonstration Plant’s commissioning, EMN can still advance offtake discussions using their Pilot Plant, and these potential offtake agreements are Objective #3 in our EMN Investment Memo:

We note that EMN should have a healthy cash position, ~$35.8M at 31 March, last quarter’s cash burn was ~$3.6M. While we are still waiting for the latest quarterly figures, we think the cash buffer should allow EMN to enter offtake negotiations with a strong hand.

Offtake discussions are closely tied up with project financing, Objective #4:

On this Objective we note that in late June EMN appointed US financial services company Stifel (market cap ~US$6B) as Project Finance Advisor for its Czech Republic high-purity manganese project.

Stifel is very experienced in the project financing space, and we expect Stifel to help EMN move towards a final investment decision in 2023.

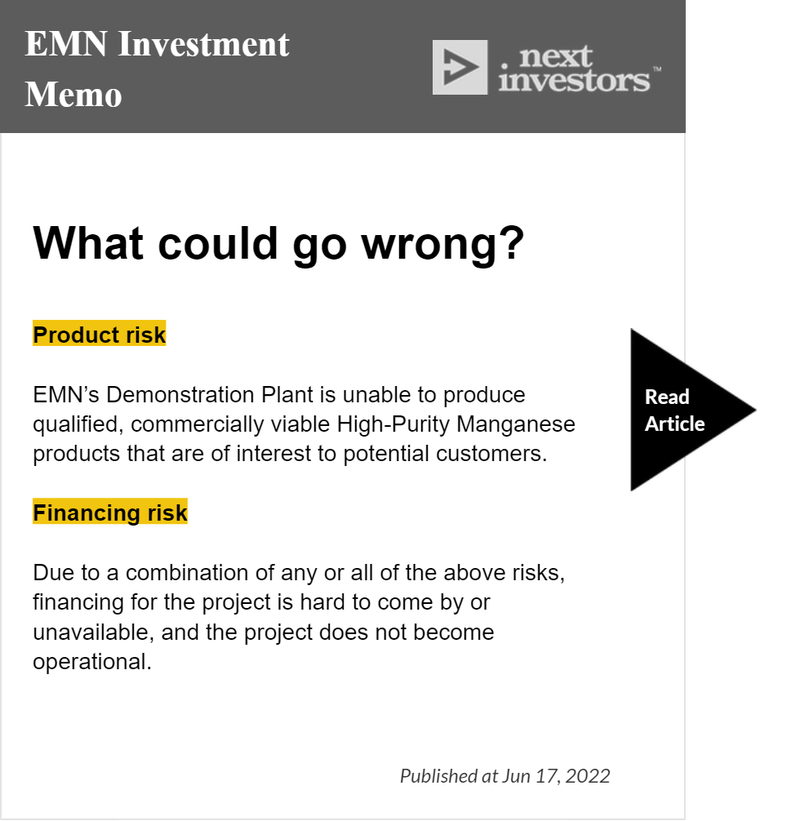

Risks for EMN after DFS

Below we’ve highlighted the two risks we are most focussed on after last week’s EMN DFS (for full risk summary, click the image below):

As before, the commissioning of the Demonstration Plant could be impacted by logistics challenges, or the products do not meet end user requirements.

Meanwhile, the DFS partially de-risks EMN’s project as financiers now have a much better picture of the project economics.

Our EMN Investment Memo

Below is our 2022 investment memo for EMN including:

- Key objectives for EMN in 2022 (shown above)

- Why we invested in EMN

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.