Trump & Xi’s “Truce” Changes Nothing: Why the critical minerals race just accelerated

Published 16-MAY-2026 13:59 P.M.

|

16 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

US president Donald Trump and Chinese President Xi Jinping just spent two days agreeing to "do stuff" together... eventually.

You know the kind of agreement I mean.

When you run into somebody you sort of knew from 15 years ago and you both say “yeah lets definitely catch up soon”

Both knowing it won't happen and both being secretly glad it won’t.

Or like when my kid promises to clean his room "in a minute."

Both of us know nothing's happening after that minute.

Or even in the next 15 minutes.

He's buying time so he can finish whatever he’s doing that's more fun or important (to him).

The "agreement" is the agreement to NOT have the ARGUMENT right now.

Or in this case... the war?

That's what we think the Beijing Trump-Xi meet was.

A two-day "let's not have the argument today" between the world's most consequential pair of frenemies.

“Look at that tree”

Nothing like a rare meeting of the two major world powers to help guide which way the “every commodity” boom we are predicting might go next.

I’m not going to get too much into the geopolitics of it all.

The one sentence summary from Bloomberg: “a swirl of dinners and festivities, generated positive optics for host and guest alike, but brought less apparent progress on some of the biggest bilateral sticking points, from tariffs and trade to US arms sales to Taiwan”

Trump and Xi agreed to meet again in Washington in September.

But let's be frank.

What I really care about is whether or not any of this will make my stocks go up (or down).

How the outcomes of this meeting will shape the minerals supply chains needed for the three global buildouts we think will drive a major “every commodity” boom.

AI data centres.

Robotics.

Military.

And the supply of the critical minerals needed for the West to build them.

It appears that nothing structural got solved last week. Both sides bought time.

The three key global buildouts (AI, robotics, military) still depend on a mineral supply chain that China can choke off at 30 days' notice.

On any whim they choose.

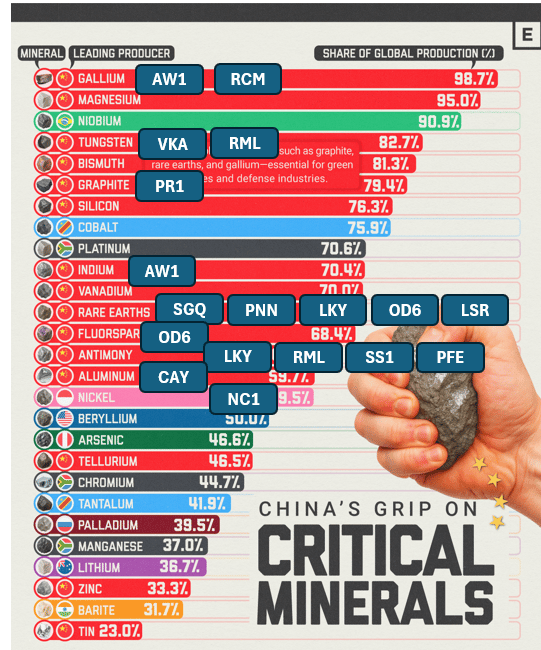

This image is still the same as it was before the meeting - China has way too much control over global supply of critical minerals, and is not afraid to use it:

(source)

In 2010, Japan detained a Chinese fishing trawler captain near some disputed islands.

China abruptly halted rare earth exports to Japan.

At the time China controlled ~97% of global supply and Japan's auto and electronics industries were almost entirely dependent on it.

The squeeze worked fast: within weeks Japan released the captain.

The episode exposed how a single chokepoint commodity could be weaponised to force a diplomatic outcome without firing a shot.

And no one really noticed... or if they did, they didn't do anything about it.

China used this tactic again in 2025 to force Trump to quickly drop his threat of putting huge tariffs onto Chinese exports into the USA.

Only this time the stakes were much higher... and everyone noticed.

Remember when Trump was threatening triple-digit tariffs on everyone back in April last year?

Back then we said he just shook up global financial markets and long standing country relationships like a snow globe:

Trump said “big tariffs on every country, the biggest on China”

China said well in that case we’ll put stringent export controls on various critical minerals and magnets.

Trump said “ok, truce?”

The USA paused its mega tariffs on China threat.

China paused (some of) its export restrictions.

A 12 month truce was agreed... (until November 10th 2026)

China was the primary target of the USA tariffs. China ended up casually batting away that threat by saying they will restrict critical mineral exports.

So what changed after yesterday’s Trump-Xi summit?

Not much.

There were some media reports of an expected 6 month extension to the truce, but nothing firm came out of the meeting so far.

So the deadline is still November 10th this year.

A 6 month extension would give each country more time to chip away at the others key points of leverage.

Before they have to have “the argument”.

The key point here is that no broad agreement was announced to upgrade the truce to a long term solution to benefit both parties. Same truce. Same timeframe.

So nothing changed. The great USA reshoring of domestic critical minerals supply rolls on.

Another looming deadline is the US Department of War’s ban on using Chinese rare earth magnets in US defence systems - starting from Jan 1st 2027. (source)

This is a hard legislative deadline that doesn't care about what gets toasted in the banquet room at the Great Hall of the People.

The USA is still in a mad rush to find and build domestic (or friendly) supply of the critical minerals dominated by China.

Here are the critical minerals stocks we are Invested in to find and build new supply of the critical minerals most dominated by China, with projects inside the USA or friendly countries are:

Before we get into where the money is going to come from to build all these mines, here is a bit more on each company (click the link to read our Investment thesis)

Gallium (China 98.7%)

- AW1 - Biggest indium resource in the USA (drilling here also for gallium/germanium right now) in Utah, USA (see Investment Memo)

- RCM - We are in it for the silver, but it also has a gallium/germanium project in Canada (see Investment Memo)

Tungsten (China 82.7%)

- VKA - Tungsten in Nevada, USA (see Investment Memo)

- RML - Gold/antimony/tungsten in Idaho, USA (see Investment Memo)

Graphite (China 79.4%)

- PR1 - We are in it for carbon nanotube fibre thermal management tech, but it also has a graphite project in WA and just announced a Defence Materials Platform Strategy (see Investment Memo)

Indium (China 70.4%)

- AW1 - Biggest indium resource in the USA (drilling here also for gallium/germanium right now) in Utah, USA (see Investment Memo)

Rare Earths (China 69.2%)

- SGQ - Rare earths + niobium, Brazil (see Investment Memo)

- PNN - Rare earths in Brazil (see Investment Memo)

- LKY - Antimony and rare earths in California, USA (see Investment Memo)

- OD6 - in it for the fluorspar, but it also has a rare earths project in WA (see Investment Memo)

- LSR - Gold/copper plus HEAVY rare earths in Arizona, USA (exploration) (see Investment Memo)

Fluorspar (China 68.4%)

- OD6 - Fluorspar in Nevada, USA (see Investment Memo)

Antimony (China 60%)

- LKY - Antimony and rare earths in California, USA (see Investment Memo)

- RML - Gold/antimony/tungsten in Idaho, USA (see Investment Memo)

- SS1 - Giant silver resource with a possible antimony resource, Nevada, USA (see Investment Memo)

- PFE - Antimony/silver in Arkansas, USA (exploration) (see Investment Memo)

Aluminium / Bauxite (China 59.7%)

- CAY - Bauxite in Cameroon (see Investment Memo)

Honourable mention (non-China dominated) Nickel (Indonesia 53.5%)

- NC1 - Giant nickel project, WA (see Investment Memo)

So where is the money coming from to build all these new mines (and make our stocks’ prices rise)?

China’s critical minerals export restrictions quickly evaporated any attempted tariff leverage by the USA.

Unlike Japan in 2010, the USA’s response has been swift and decisive (typical USA style).

The solution: break China’s grip on critical minerals by throwing money at creating its own domestic and friendly critical mineral supply.

An extreme urgency to build new mines and domestic (or friendly) critical minerals supply.

And the money to back it up.

The funding initiatives already deployed and committed in the last 12 months:

- Project Vault - $12 billion strategic critical minerals stockpile (launched Feb 2026). Can include any of the 50+ minerals USGS classifies as critical. (source)

- Pentagon direct deals - Defense Secretary Pete Hegseth confirmed $4.5 billion deployed in five months across six critical minerals deals. That includes a $400M equity stake in MP Materials (source) and a $150M loan for heavy rare earth separation capacity in California (source).

- Defense Production Act financing - $1 billion authorised through September 2027 (source).

- National Defense Stockpile - $2 billion appropriated for FY25 to expand the stockpile, plus an additional $5 billion to the Industrial Base Fund (passed under the One Big Beautiful Bill Act, July 2025) (source).

- FY27 budget request - $48.7 BILLION for critical minerals investments PLUS $47 BILLION for munitions industrial base. That's $95.7 billion in one budget cycle (source).

- 2027 magnet ban - Hard legislative deadline. From January 1, 2027, US defence contractors cannot use Chinese-origin rare earth magnets, tungsten powders, or tantalum in any weapons system. Codified in 10 U.S.C. §4872 / DFARS 252.225-7052 (source).

- JP Morgan’s $1.5 Trillion “security and resilience initiative”. (source)

- FAST-41 permitting fast-track - White House list of priority critical mineral projects that get accelerated federal approvals. The Trump administration added 10 mining projects in April 2025 and has kept expanding the list (source).

By the way - Our Investment RML (Resolution Minerals) secured FAST-41 status for Antimony Ridge in Idaho - one of only three ASX-listed companies on the list (source).

All the tree pointing, banquet toasts and mutual kind words over the last two days doesn’t stop this train.

The USA needs to get out from under the critical minerals leverage that China holds - and fast.

Even world peace. If peace happens - doesn't change it.

Because nobody is going to approve $96 billion in one budget cycle to build a critical minerals supply chain and then say "actually, never mind, let's outsource it back to China, I'm sure they won't use it against us again."

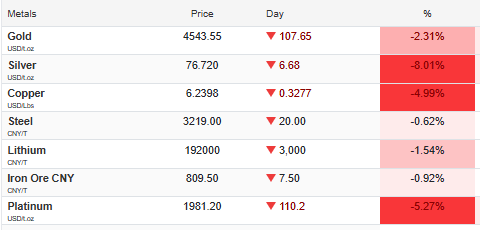

So why did most of the stocks in our Portfolio and watchlist ( and the ASX) get slammed yesterday?

I have my trusty commodity price watchlist open on one of my screens all day.

At ~3:30pm AEST on Friday something happened...

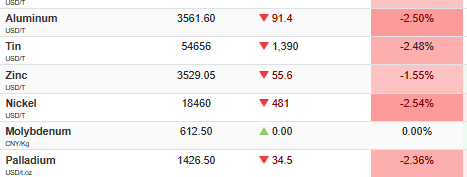

Silver, gold, copper and other commodities all suddenly got smashed.

And it quickly got worse as the day turned to evening:

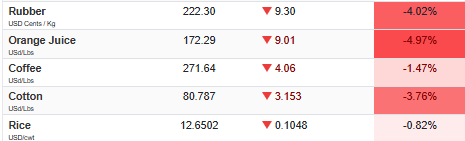

Even rubber, cotton and the humble orange juice got smoked:

So what the hell happened?

Did Xi just agree to keep using the US Dollar as global reserve currency for ever more (commodities are priced in USD)?

Was world peace declared with open shipping waterways and free-flowing commodity supply for all?

Unlikely.

It's been nearly 24 hours now and it’s still not clear why this “every commodity vomit” happened.

(oil and gas were spared)

Bond yields across the board spiked (meaning people were selling bonds too).

When everything's going down at the same time it’s usually a sign investors are moving into cash.

Or maybe the market was pricing in that the Trump-Xi meeting would go worse than it did and unwound the “commodity trade” when Trump didn’t spit the dummy and accelerate the hostilities?

Whatever the outcome of the summit was, we don't think the USA likes having China holding nearly all the supply of critical minerals (and all the processing capabilities).

Using them for leverage.

OR generally withholding or slowing down supply to hobble USA's ability to build out anything that matters.

We think the sudden strategic-ness of the critical minerals to build out AI, robots and military will drive an all commodities boom.

This week's drawdown might just be the algos pricing in "world peace declared, China opens the critical minerals floodgates."

Reality is: China has kept its hand on the floodgate lever the whole time. The gate isn't open.

The gate is just not closing more this minute.

Xi said "Thucydides Trap" to Trump - a veiled dig?

Quick history lesson.

Xi said to Trump ahead of their bilateral meeting that the major question both countries have to answer is whether they can avoid the "Thucydides Trap."

What's the Thucydides Trap?

A Harvard professor named Graham Allison came up with the term back in 2012.

He wrote the book Destined for War in 2017.

The framework comes from the ancient Greek historian Thucydides, who said of the Peloponnesian War:

"It was the rise of Athens and the fear that this instilled in Sparta that made war inevitable."

The Thucydides Trap: when a rising power challenges a ruling/declining power, war is the historical default.

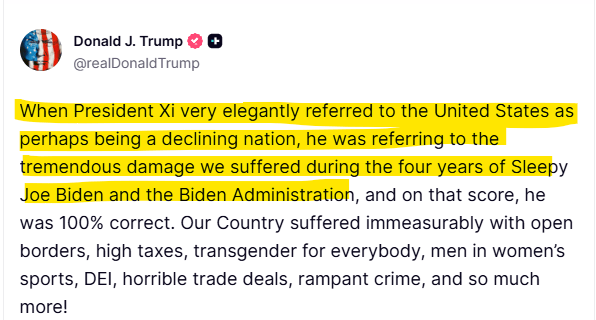

So did Xi just call the USA a declining power to their face?

Here’s what Donald Trump had to say about the USA being indirectly called a declining nation by China (love him or hate him, this is pretty funny):

(source)

But more importantly, does the Thucydides Trap mean the USA and China are going to end up going to war?

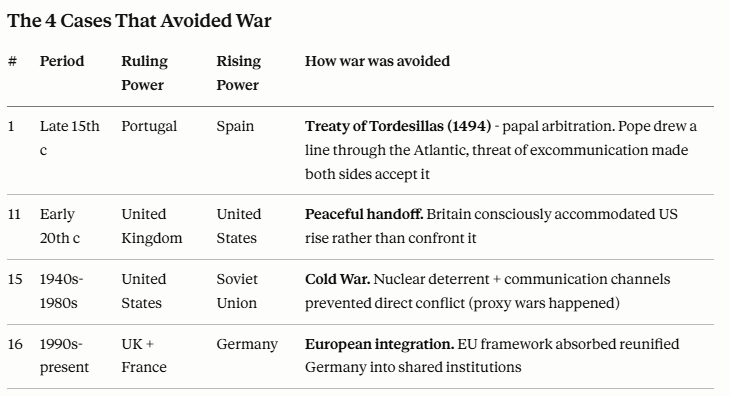

The Harvard boffins that came up with this concept went back over 500 years and identified 16 cases where a rising power challenged a ruling power.

(*excited Ray Dalio noises*)

I love a bit of war history, so I spent some time hassling AI for the specific examples (gotta make hay while the West is still able to build and maintain AI chips and datacentres... before China turns off our critical minerals supply).

Out of the 16 “ruling/declining power meets emerging power” scenarios over the last ~500 years:

12 ended in WAR:

4 did NOT end in War:

The good thing is that the most recent rising-power “baton passes” from the last century did NOT end in war.

(One was a peaceful handoff. One was Cold War nuclear deterrence. One was European integration. Of those three... only the second one really applies to US-China today, and it's the one that currently feels least like a peaceful handoff.)

Whether we DO or DON’T eventually end up with a USA-China war (and I hope we don't)...

...the key point is that regardless, we think the USA does NOT want China having critical mineral supply leverage over it for the great, global race to build out AI, robotics and militaries.

Pulling it out on them every time they get into a disagreement like your wife bringing up that thing you did 10 years ago every time you argue.

So they're scrambling to fix it.

And the scramble is the trade.

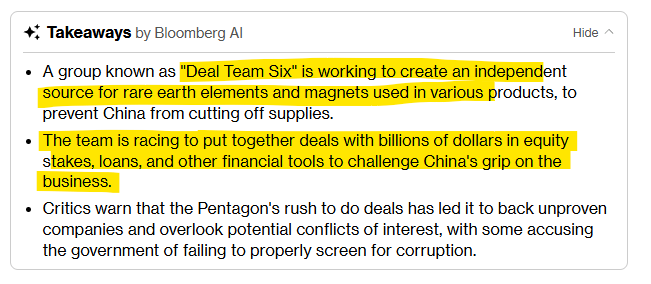

Bloomberg giving rare earths some big airtime in the last 24 hours

Another thing we noticed just after the Trump-Xi meet ended was the sudden interest in rare earths supply chains in the mainstream financial media.

(source)

Get it? Deal Team Six? Like the famous Seal Team Six, the US Navy's premier tier-one special missions unit.

Except it's a crack team of finance-y former Wall St deal makers/bankers and its special mission is doing rare earths deals for the USA.

China had been quietly preparing the rare earth chokehold for a decade.

Through the 2000s Beijing flooded global markets with cheap rare earths, drove Western producers like Mountain Pass out of business by 2002, and then started progressively tightening export quotas from 2006 onwards

This was an explicit industrial policy to capture the higher-value refining, magnet and end-product stages domestically rather than just export raw dirt.

By 2010 they had a ~97% monopoly on the industry.

We also saw the following video in Bloomberg which summaries everything really well - we highly recommend giving it a watch (need a Bloomberg subscription):

(source)

The one thing that stood out from the video was what happened the last time China put in place restrictions on rare earth exports.

That was in 2010 when China put in embargoes against the Japanese.

And forced the Japanese to look for non-China supply.

Which ultimately led to the Japanese bank rolling ASX listed Lynas Rare Earths - the biggest rare earth producer on the ASX, and one of only two in the West.

This New York Times article covers the Japanese embargo era really well:

(source)

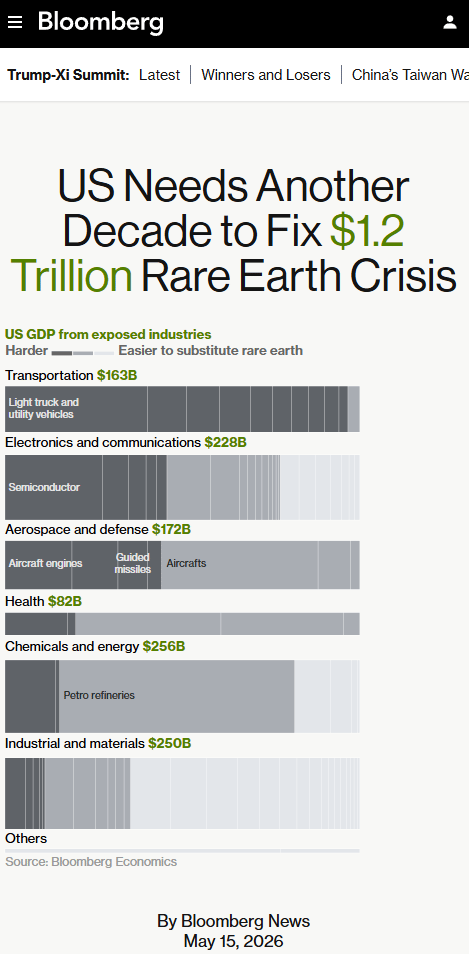

So what (and how much) will the US have to do to build its own ex-China supply chain?

The final article in the 24 hour flurry of Bloomberg rare earths coverage was this “Big Take” on how the US will need a decade and ~US$1.2 trillion to fix its “crisis”:

(source)

Now we just sit back and wait for Deal Team Six to send some of that $1.2 trillion to our rare earths Investments... right?

We are Invested in the following rare earths companies:

- SGQ - Rare earths + niobium, Brazil (see Investment Memo)

- PNN - Rare earths in Brazil (see Investment Memo)

- LKY - Antimony and rare earths in California, USA (see Investment Memo)

- OD6 - in it for the fluorspar, but it also has a rare earths project in WA (see Investment Memo)

- LSR - Gold/copper plus HEAVY rare earths in Arizona, USA (exploration) (see Investment Memo)

(interestingly, the Bloomberg video also talked about how Brazil could be the USA’s rare earths saviour - so maybe we have the geography right on this one...)

How early are we into the capital rotation?

The USA big end of town has spent the last 20 years getting rich on capital-light tech businesses.

The exact opposite of what a mining business looks like - capex-heavy, cyclical, geopolitically tangled, environmentally complicated.

The “muscle memory” just isn't there for US capital to invest in mining.

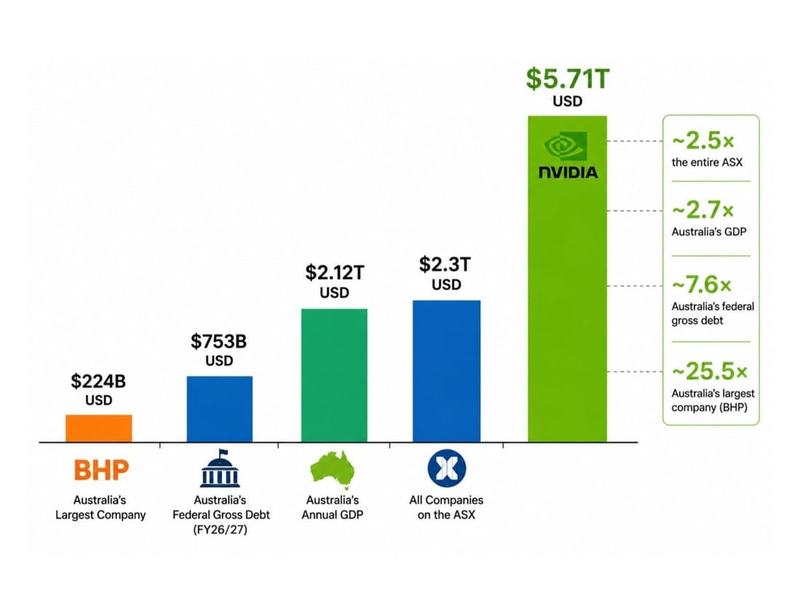

We get it - when NVIDIA has a market cap bigger than the entire mining industry it makes sense for them to stick to what they know.

A "small cap" in the US is a company under US$2 billion.

A "small cap" in Australia is more like under AU$200 million.

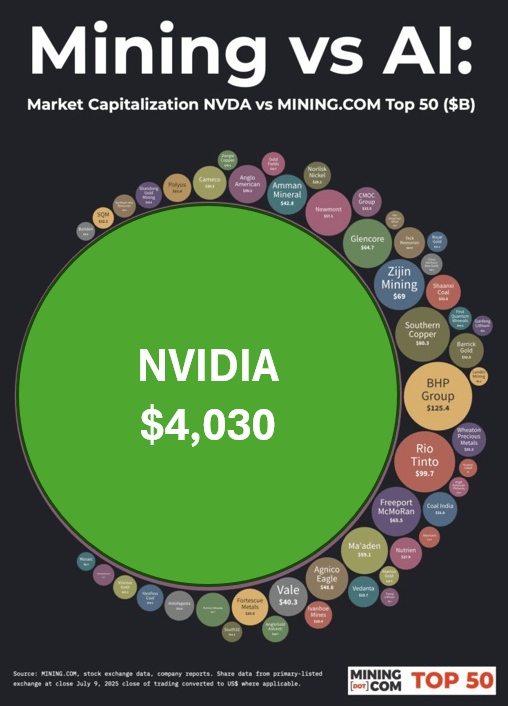

And then there's the chart we keep coming back to:

NVIDIA's market cap, on its own, is bigger than the top 50 mining companies on the planet... combined.

Here is NVIDIA compared to BHP... and even the entire ASX:

(source)

So it makes sense why the big US capital allocators aren't sniffing around ASX small cap mining stocks.

(yet)

In 1957, when the S&P 500 launched, energy and materials made up roughly 47% of the entire index.

During the 1970s commodity supercycle peak, they hit 30%+.

Today energy and materials make up about 6% of the S&P 500.

We think that over the next 5-10 years that will have to revert back to historic averages.

And today, all of the funding commitments we mentioned earlier in today’s note are like the start of a wave, one that we expect to get bigger and bigger.

We are here now:

When the retail-investor and tech-VC end of the US markets start cutting big cheques into the metals and mining space we will get to here:

(Imagine instead of Gamestop, the retail meme stock of the year is a mining company?)

The first wave of capital floods into the major producers - BHP, Rio, Glencore, Freeport, Cameco etc.

The safest place to deploy the first big tranches.

Then comes the second wave - the more interesting one (to us).

The wave that moves into mid-tier developers and ambitious nimble explorers.

The ones with US-relevant projects, technical management, drill-ready ground, and the ability to move from drill program to offtake in 12 months instead of 36.

(this is the wave we sit in. This is the wave we are Invested in.)

Now we just wait for our underinvested little mining balls to grow relative to that giant green NVIDIA ball:

(source - from 11 July 2025, so the numbers could look different today)

See you next week, and have a great weekend.

Next Investors

Did someone forward this to you? Subscribe Here

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.