SS1: Giant USA silver resource. NEW: metwork demonstrates conventional processing and excellent recoveries

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,919,142 SS1 Shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our Investment Sun Silver (🇦🇺 SS1, 🇺🇸 SSLVF) already had the largest pre production silver resource on the ASX.

SS1 has a giant 539M oz silver equivalent resource estimate - in Nevada, USA.

Over the last year, the silver price has risen over 150%, and is now trading at US$83 per ounce.

(past performance is not an indicator of future performance)

Making the in-ground estimated value of SS1’s silver $63BN (US$44.7BN).

(inground $ value for illustrative purposes only. Ignoring all costs to dig out and process the ore, along with the time value of money (the silver price varies wildly in any given year). Never take a back of a napkin in ground resource value literally.)

So why is SS1 trading at $1.82/share with a market cap of ~$350M?

Yes, 539M ounces of silver equivalent is huge...

But the market wants to know if the silver can be extracted and processed.

Today, SS1 announced that YES it can - releasing an announcement showing silver recovery rates on the higher end compared to other mines in the region.

Here is what testwork from SS1’s deposit showed:

(read the announcement here)

Silver recoveries reached 78% under early stage heap leach conditions.

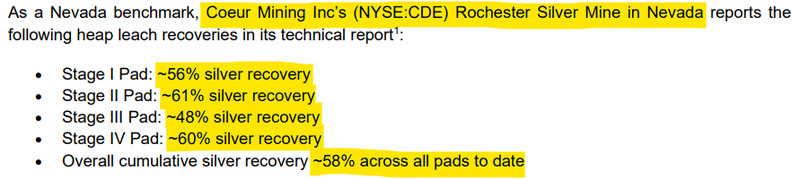

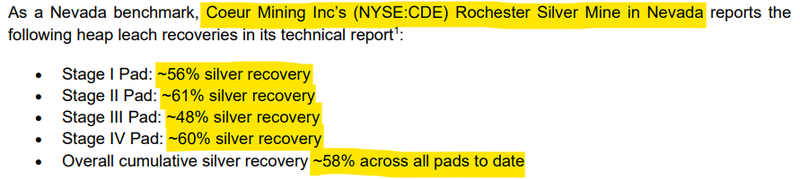

The biggest silver-producing mine in Nevada, $22BN Coeur’s Rochester mine, delivers recovery rates between 48% and 60% from heap leaching.

(source)

We think confirmation that SS1’s silver can be recovered at excellent rates using standard processes was a key de-risking that the market was watching for.

(especially sophisticated resource funds.)

We’ll get into more detail on today's announcement in a second.

Today we’ll also go into detail on one of the key reasons we originally Invested in SS1.

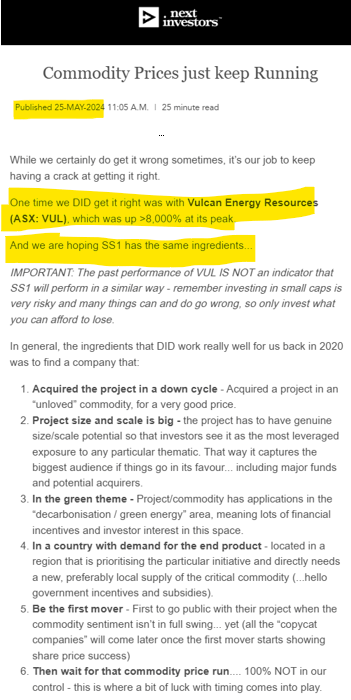

If you have been on our mailing list for more than a few years (you can subscribe here, it’s free), you’ll know that our best ever Investment Vulcan Energy Resources (ASX: VUL) was up over 8,000% at its peak.

And is still up 2,200% from our Initial Entry Price.

(past performance is not an indicator of future performance)

We identified a six ingredient “recipe” that we thought led to the 8,000% run with Vulcan.

We have stated multiple times over the last 18 months that we think SS1 fits all the ingredients.

(read on for full details on the 6 ingredient recipe and where SS1 sits)

The only ingredient (ingredient #6) that SS1 needs that is NOT in its control is for the silver price to run.

The silver price has already delivered a solid leg up, now we are waiting for it to consolidate before what we hope will be ANOTHER run (noting that the silver price can go down as well as up):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our favourite momentum and technical analyst Michael Oliver is calling US$300 to US$500 silver over the next 6 months - check out this recent Sprott Money interview here.

He has correctly predicted silver’s behaviour over the last 2 years.

(Of course he can get things wrong - it’s just one prediction that may not eventuate)

He also says there is going to be a silver price correction on this journey to his price targets - so buckle up for a wild ride if he is right.

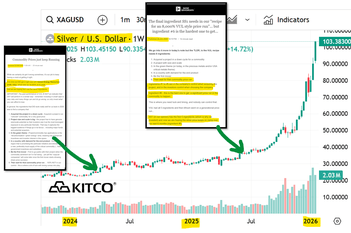

In fact we got a bit of this price turbulence a few weeks ago when silver fell from US$123 to ~US$64 - it's now back to US$85.

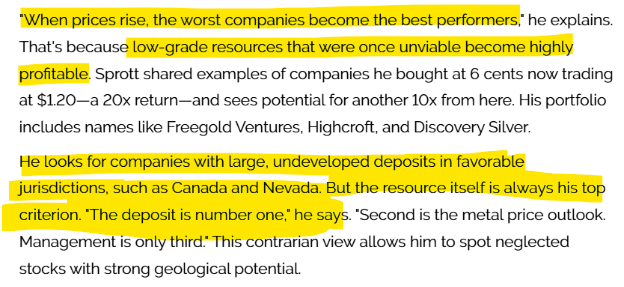

Speaking of silver experts, legendary billionaire silver bull Eric Sprott has a theory that when a commodity price runs, the companies with the largest deposits exposed to that commodity run the hardest.

Eric Sprott holds over 40% of the “other” giant undeveloped silver deposit in Nevada, owned by NASDAQ-listed Hycroft Mining - so far so good for him with Hycroft up over 1,000% in the last 12 months.

(past performance is not an indicator of future performance)

Today, we’ll also cover the similarities between Hycroft and SS1, and how Eric’s theory of a running silver price will lift the company with the largest silver deposits the most (like Hycroft and SS1).

A$5.5BN Hycroft is NASDAQ listed, which provides the company access to the giant, deep pools of US capital that are just catching on to silver and gold.

The $350M capped SS1 is planning a US main board listing - which we hope could lead it to become a Hycroft 2.0.

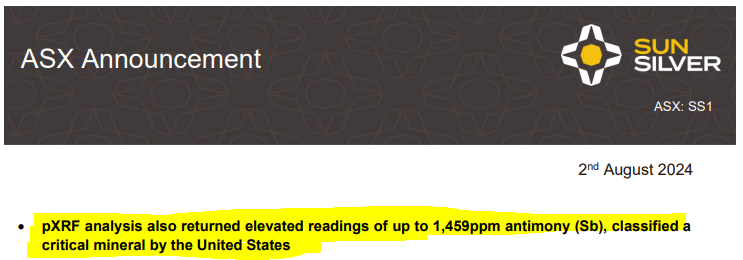

And the final kicker for SS1 - there could be critical military mineral antimony running through its giant silver deposit.

Antimony is a critical military mineral used to make bullets.

The USA has no domestic antimony supply.

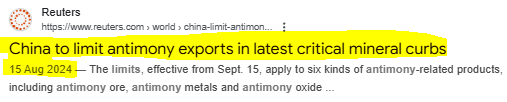

China controls ~85% of antimony processing capacity globally and recently put export controls on the mineral.

(not ideal for if your military is relying on key adversaries for minerals needed to make bullets)

The USA is throwing a lot of capital to bring online domestic supply of antimony.

SS1 (in Nevada, USA) discovered it has antimony running through its deposit after re-testing historical drill cores that were only ever assayed for silver and gold - not for antimony.

If it does turn out that there is a material antimony resource mixed in with SS1’s giant silver deposit, it could lead to US government funding to build SS1’s silver (and antimony) mine.

$6BN Perpetua Resources’ project in Idaho had a similar dynamic.

A giant gold deposit with antimony running throughout.

And a large upfront CAPEX hurdle - US government funding was what started a re-rate in Perpetua’s share price.

Perpetua received commitments for a US$1.8BN loan from US Export-Import Bank and then private capital started pouring into the company in a big way.

Perpetua's market cap has gone from $300M to $6BN.

(past performance is not an indicator of future performance)

JP Morgan says it is better to have military minerals mixed with precious metals - less scope for enemies to crash military minerals prices if it’s a byproduct of producing a precious metal.

We are watching for SS1’s initial antimony resource and then potential US government funding.

What we are watching for next from SS1:

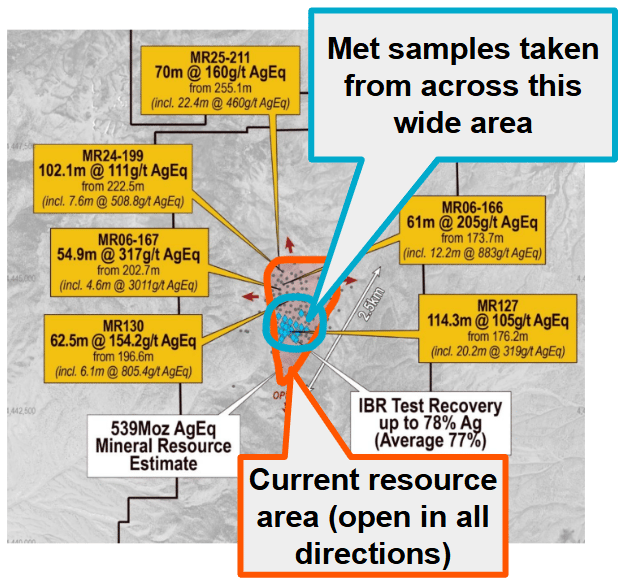

- More drilling results - SS1’s giant silver resource is open in all directions, we are looking for extensional hits and another increase to 539Moz silver equivalent resource estimate.

- Scoping Study - An early look at what the project economics for SS1’s giant deposit might look like. We are expecting this to be released some time in 2026.

- Maiden (first ever) antimony resource estimate - how much of this vital military mineral is running through SS1’s giant silver deposit?

- US government funding - SS1 is “pursuing” Department of Defence (Department of War) funding; we suspect an antimony resource may be what unlocks this one.

- Listing on the US main boards, NYSE or NASDAQ - easy access to US investors to buy, SS1 to become Hycroft 2.0?

- Silver price to continue its next leg up - The silver price run is the most important thing for SS1 in the short term.

In the rest of today’s note we are going to cover off:

- Our key takeaways from SS1’s metwork announcement today - why it's important

- Our recipe of six ingredients for an 8,000% Vulcan Energy sized return - can SS1 repeat it?

- How SS1 could also become a Hycroft Mining 2.0 (Hycroft is A$5.5BN NASDAQ listed beast)

- How SS1 could also define a maiden antimony resource estimate on its deposit.

- How government funding could be what unlocks a mine build.

- 10 reasons we invested in SS1.

- Major updates over our two-year journey (sort of like a greatest hits over the years).

Yes, it’s huge - but can it be extracted and processed?

A big de-risking hurdle has been cleared today.

One the market, and SS1 shareholders (including ourselves) had been waiting a long time for.

SS1 already had the largest pre production silver resource on the ASX - a giant 539M oz silver equivalent resource.

There was a major hurdle for SS1’s asset that large North American project financiers (and others) were likely waiting for - and that was:

Could the valuable silver (and gold) in the SS1’s rocks actually be economically extracted using conventional processing methods?

Today SS1 has gone a long way to answering that question, delivering early stage metwork results that demonstrate that yes - conventional processing methods are all that is required to process its silver.

The key line was “metallurgical testwork indicates ore is non-refractory and non-preg robbing”.

Which basically means SS1’s silver can be recovered using simple, low-cost gravity or standard CIL/CIP cyanidation without any exotic pre-treatment.

Simple, standard, well-understood processing methods...

Here is Ai’s take on why being non-refractory and non-preg robbing matters:

“When gold ore has preg-robbing, it means the rock steals the gold back after you've dissolved it out; when it's refractory, the gold is locked inside other minerals and won't dissolve easily in the first place. Saying "no preg-robbing, no refractory issues" simply means the gold is easy and cheap to extract using standard processing - the best-case scenario.”

(source)

SS1 recoveries averaged 77% under early stage heap leach test conditions - which is a game changer for project economics.

SS1’s asset sits in the Carlin Trend of Nevada - here recoveries are around the high 50s, low 60s in heap leach conditions.

Coeur Mining Inc’s (NYSE:CDE) Rochester Silver Mine in Nevada is the biggest silver mine in Nevada, with recovery rates between 48% and 60% from heap leaching.

To most, reading the announcement won't make much sense - we had to do some online searches for ourselves to understand some of it.

But for the big mining project financiers waiting to see the orebody get de-risked this is a pretty big moment.

At the end of the day, metallurgy is what can make or break a project.

It’s just the kind of work that the bigger institutional funds look for before cutting big cheques to mid-cap developers.

These are the guys thinking about how the project can get developed and how a resource can be processed into a saleable product.

The next big milestone will be a Scoping Study which SS1 plans to deliver before the end of the year. Here we should get a first look at project economics.

Our Key Takeaways from today’s SS1 metwork announcement

We think SS1’s results today would be looking a lot better to later stage financiers than they could have expected, the key takeaways from us being:

1. SS1’s deposit IS amenable to heap leach processing

SS1 confirmed its orebody was “non-refractory and non-preg robbing” meaning the most common and well understood processing method in Nevada can be applied to SS1’s deposit - Heap leaching.

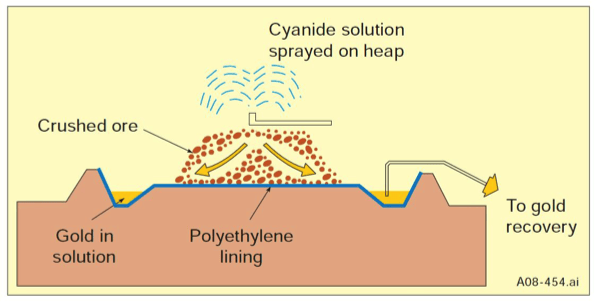

Explainer: What is heap leaching? 🎓

It’s not so common in Western Australia, however heap leaching is a widely used, low-cost processing method suited to bulk-tonnage silver and gold deposits.

We were in Nevada last year - twice on site visits - and everywhere you look its mega mines heap leaching gold, silver and copper out of the ground. (source) (source)

The main benefits of heap leach processing is that its usually lower capital intensity compared to conventional milling and tank leaching, lower operating costs, scalable and far less complex.

The process involves:

- Crushing ore to a defined size;

- Stacking the ore on a lined leach pad;

- Irrigating the heap with a leach solution (typically cyanide for silver and gold);

- Recovering dissolved metals from solution via dewatering, precipitation and smelting processes.

(source)

Here are some pictures from the big heap leach operation $111BN Barrick and $184BN Newmont are running in Nevada.

(notice the pipes running up the hill - that’s where the leaching solution is pumped onto the pads, and if you squint hard you can make out the protective barriers that capture the solution).

(source - from our site visits in Nevada in 2025)

2. SS1’s average recoveries are ~77% (and up to 78.3% in some intervals) - higher than some of the mega deposits in Nevada.

The biggest silver producing mine in Nevada - Coeur Mining’s Rochester project has silver recovery rates between 48% and 60% from heap leaching.

(source)

3. The results were taken from 242 different intervals - so the results are representative of a large chunk of the ore body

... not just cherry picked sections of the “best” parts of the ore body.

(source)

Keep reading to see the rest of our note, which covers:

- Our recipe of six ingredients for an 8,000% Vulcan Energy sized return - can SS1 repeat it?

- How SS1 could also become a Hycroft Mining 2.0 (Hycroft is $5.5BN NASDAQ listed beast)

- How SS1 could also define a maiden antimony resource on its deposit.

- How government funding could be what unlocks a mine build.

- 10 reasons we invested in SS1

- Major updates over our two-year journey (sort of like a greatest hits over the years).

SS1 “The next 8,000% Vulcan”? Ingredient #6 is looking good...

Our job is to identify macro investment themes early and try to find stocks that have the best chance to deliver a 10x return in that theme.

And including the occasional major outsized winner...

(This is what we are all in this game for after all)

It’s not easy - in fact it's very hard. Early stage speculative mining stocks are risky investments and you can lose money easily.

If you have been on our mailing list for more than a few years (you can subscribe here, it’s free), you’ll know that our best ever Investment Vulcan Energy Resources (ASX:VUL) was up over 8,000% at its peak.

(and is still up 2,200% from our Initial Entry Price.)

The past performance is not an indicator of future performance.

That VUL run was back in 2019 to 2022 during the first major lithium bull run.

VUL is still our best Investment to date, so naturally we think a lot about how and why it happened, and how to try to repeat it.

But of course past performance like this is extremely hard to replicate, most Investments don't turn out anywhere near as successful.

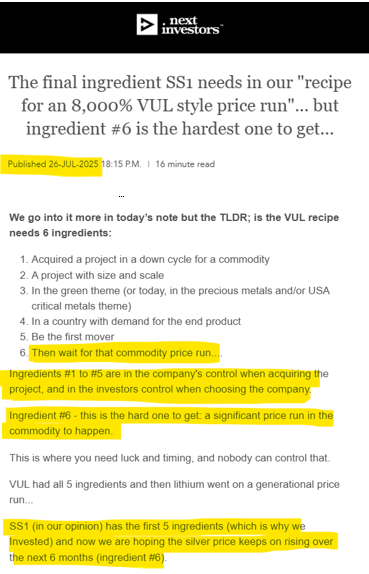

We identified a six ingredient “recipe” that we thought led to the 8,000% run with Vulcan.

The VUL success recipe needs six ingredients:

- Acquire a project in a down cycle for a commodity.

- A project with size and scale.

- In the green theme (or today, in the precious metals and/or USA critical minerals theme).

- In a country with demand for the end product.

- Be the first mover.

- Then wait for that commodity price run....

(read our full 6 ingredient recipe for an 8,000% gain here - remember no guarantees its very hard to pull this off, the planets need to align and a lot of luck is required)

Ingredients #1 to #5 are in the company's control when acquiring the project, and in the investors’ control when choosing the company.

Ingredient #6 - this is the hard one to get: a significant price run in the commodity.

This is where you need luck and timing, and nobody can control that.

VUL had all five ingredients and then lithium went on a generational price run...

SS1 has all 5 ingredients and we were just waiting for silver to go on a generational price run...

Way back in May 2024, when silver was US$38/oz and Sun Silver (ASX:SS1) had just IPO’d at 20c, we first wrote about the “Vulcan recipe” for SS1:

We wrote about the VUL recipe for SS1 again in July 2025:

(again in July 2025 - you can read the full thesis here)

Well, over the last two months, silver has certainly started to deliver ingredient #6 for SS1...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

SS1 is already up over 1,100% (so far) from our Initial Entry Price:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So what’s next for SS1 in the 6-ingredient recipe?

Ingredient #6 looks like it’s coming along nicely.

The big institutional money (that really pushes stocks up when they start buying) doesn’t generally believe in the recent quick price spikes like we have seen in silver.

While the silver price has run hard over the last couple of months, and yes SS1 has tracked along nicely with it...

We think the silver price needs to consolidate the gains (i.e. to stabilise and go sideways for a while to show the price re-rate is real) for the broader market to start believing and the “big boys” to start buying.

(The metallurgical testwork being de-risked today could help make big institutions comfortable buying too)

Once the gains are more consolidated, silver producers will be cashed up from a quarter of selling at high prices and we should see more ‘new silver mine’ CAPEX financiers open their wallets betting on a structural change in the market.

OR

If silver does something silly like go to US$200 or US$300/oz then good old fashioned FOMO will kick in and it will be “game on” for a generalist investor driven rally in silver stocks.

Our favourite momentum and technical analyst Michael Oliver is calling US$300 to US$500 silver over the next 6 months.

He also says there is going to be a silver price correction on this journey to his price targets - so buckle up for a wild ride if he is right (looks like that happened a few weeks ago when silver fell from $123 to $61, now back to $85)

Check out his latest video interview here with Sprott Money - Silver Price Breaks the 50-Year Range, Most Gains By Summer | Michael Oliver:

And as always, as exciting as this US$300 to US$500 silver price prediction sounds for silver investors, keep in mind that analysts do get it wrong all the time.

But if silver DOES do something crazy like go to even US$200 or US$300, this should be what we need for a serious run for SS1 and all our silver stocks.

(yes, even more than the 10x return delivered since SS1’s 20c IPO)

(past performance is not an indicator of future performance)

With silver’s big spike over the last two months, there is already talk that silver could be becoming a “meme-stock” commodity.

(remember the Reddit driven “almost” silver squeeze from 2021?)

Some are even saying that the silver price is starting to behave like “crypto” or an “alt-coin”.

(a lot of salty bitcoin holders are lamenting about silver’s run on social media - attracting some of that hot and fast crypto money?)

Speaking of meme stocks and silver...

Can SS1 grow into the next Hycroft Mining (NASDAQ: HYMC)?

Above, we covered our thesis on why Sun Silver’s (🇦🇺 SS1, 🇺🇸 SSLVF) could have a Vulcan style move (an 8,000%+ re-rate).

But can it also morph into a Hycroft Mining 2.0?

Hycroft Mining is currently capped at ~US$3.8BN (~A$5.5BN), with a US$50 share price.

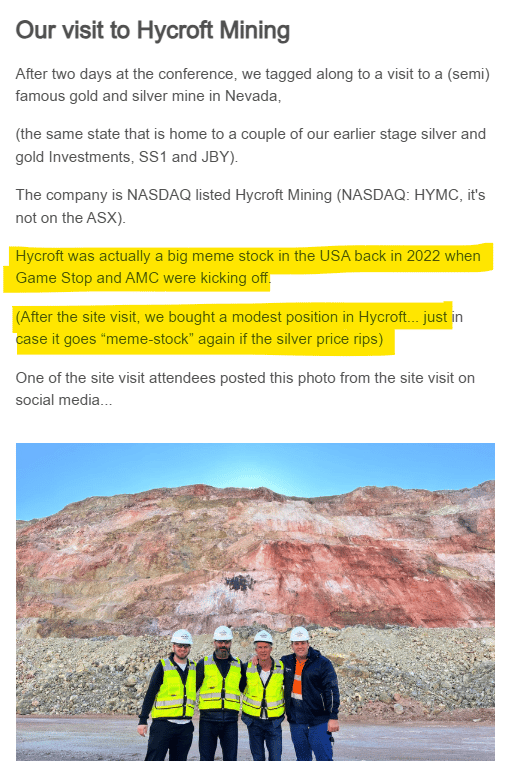

While we don’t cover Hycroft, we bought a modest amount of Hycroft Mining stock at ~US$5/share one hour into our site visit to the Hycroft mine back in September last year.

(Disclosure: 23,000 HYMC shares held and 40 options contracts), no commercial engagement with HYMC)

(we generally only write about ASX listed stocks, and Hycroft is only listed on the NASDAQ)

Our Hycroft Investment has done pretty well for us so far.

SS1 and Hycroft have all 5 ingredients and we were just waiting for silver to go on a generational price run... which is looking pretty good right now.

(read our full 6 ingredient recipe for an 8,000% gain here)

Here is what we said after our site visit to Hycroft’s gold and silver mine in Nevada.

We bought Hycroft Mining because we like giant silver deposits in Nevada, like Sun Silver 🇦🇺 SS1, 🇺🇸 SSLVF),

AND

Also because Hycroft used to be one of the main “meme stocks” during the 2021 GameStop mania era.

And we thought the dormant meme stock crowd could be re-activated on Hycroft in the current gold and silver run.

Here is what we said after that site visit write up:

(source)

Back in 2021, a handful of US stocks delivered eye-watering price runs after hundreds of thousands of retail investors started buying them at the same time, coordinating through Reddit and other social media.

Gamestop was by far the biggest meme stock, followed soon after by AMC Cinemas.

During the middle of its meme stock mania, AMC invested into Hycroft Mining, drawing the attention of meme-stock crowds and turning Hycroft into a meme stock in its own right.

(Why did a cinema company invest into a silver company? Peak meme stock behaviour)

Part of our thesis for Hycroft is that any of the crowd that followed Hycroft during its meme stock phase might be re-energised if the silver price started running...

(and it looks like they have been, if you take a quick look at #HYMC on X)

Hycroft has delivered an incredible 2,400% run over the last 12 months to its recent peak, with most of it over the last 4 months:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

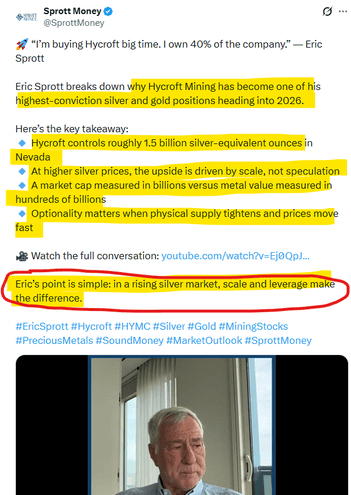

Hycroft’s giant mine in Nevada, USA has a ~2.6BN silver equivalent ounce resource. (source)

Fully diluted Hycroft is now capped at ~US$3.8BN (~$5.5BN AUD).

Sun Silver (🇦🇺 SS1, 🇺🇸 SSLVF) has ~0.539 billion ounces at 72 g/t silver equivalent also in Nevada, USA.

Fully diluted SS1 is capped at ~US$243M... (~$350M AUD)

SS1’s resource is open in all directions; they are drilling to grow it even more, and recently picked up more ground surrounding their silver deposit.

SS1 is already listed in the USA on the OTC market (🇺🇸 SSLVF) but says it is working on a potential listing on a main USA stock exchange - which we are eagerly anticipating given how well $5.67BN Hycroft has been performing recently.

Hycroft’s biggest shareholder is billionaire silver bull Eric Sprott - and we agree with his theory on large precious metals deposits like SS1’s

Eric Sprott owns 40% of Hycroft, and has been buying on market this month (source)

(he actually bought AMC Cinemas’ Hycroft shares from them a couple of months ago... before the massive run)

Eric Sprott is a Canadian billionaire, investor and philanthropist and one of the biggest silver bulls in the world.

We’ve listened to a lot of interviews with Eric over the years, but haven't heard him as excited about a stock as he is when he talks about Hycroft.

and a lot of the reasons given for his excitement are similar to SS1.

Check out the 2 minute video below, he is literally bouncing up and down in his seat when he talks about it:

Here is his same thesis presented in a different article:

(source - read it here)

Sprott's thesis is that over the years, projects with giant resources (like SS1 and Hycroft) may not be commercial while the commodity price is trading lower, so share prices remain very low...

BUT if the commodity price goes up a few hundred per cent, suddenly these projects become extremely profitable, and share prices rise fast from a low base.

(basically talking to the amount of leverage giant deposits offer to a commodity price)

This is a solid thesis for SS1 and HYMC with their giant silver deposits in Nevada (assuming the silver price keeps running of course).

No guarantees of course.

Remember in 2024 when everyone was complaining about how deep SS1’s silver deposit was? And how expensive it would be to dig the hole to get to it?

With the silver price tripling since then, suddenly nobody is talking about that anymore...

(Sun Silver (🇦🇺 SS1, 🇺🇸 SSLVF), if you are listening - please get listed on a USA main exchange like NASDAQ or NYSE asap and try and catch some of the “Hycroft 2.0” tailwinds)

(also if anyone knows Eric Sprott please tell him about SS1)

SS1’s project could also host a giant antimony resource (Critical militiary metal to go with its giant silver deposit)

A big part of the reason why Perpetua received so much government funding support was because its project also hosts the largest antimony resource inside US borders.

Antimony is a critical military metal used for various defence applications like missiles, tanks and ammunition.

Right now, the US has no domestic supply of antimony and China controls ~85% of antimony processing capacity globally.

(The importance of having antimony in a resource just went up over the last few days too.)

SS1 first hit antimony in one of its new drillholes in August 2024 - BEFORE the China export ban on antimony came into place:

(Source)

(Source)

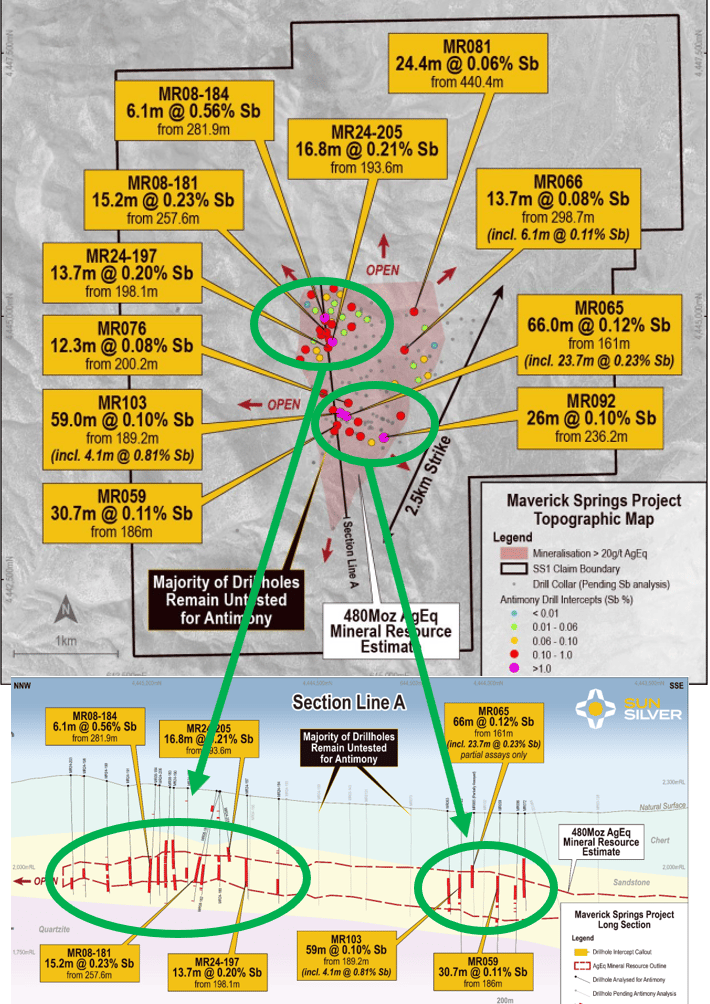

So far, almost all of the holes SS1 has re-assayed have had antimony in them.

Here is where SS1 has found antimony across its resource so far:

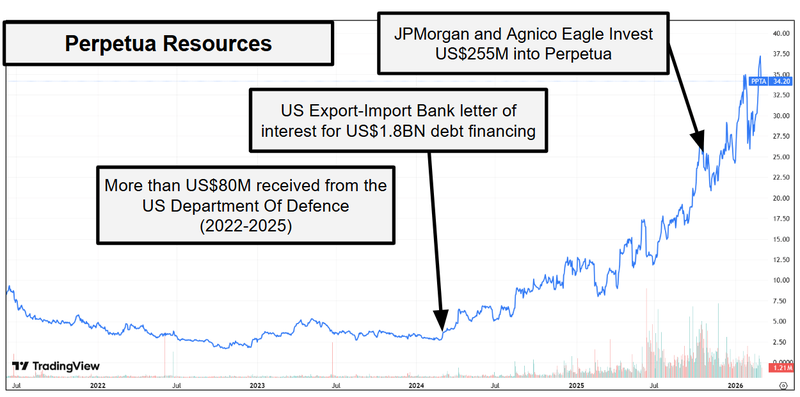

Given antimony’s use in critical military applications, the US government has been scrambling to secure its domestic supply, and has deployed ~US$1.8BN in funding on a US based precious metals project owned by Perpetua Resources.

Perpetua Resources’ project, like SS1’s, is primarily a precious metals project (in Perpetua’s case its gold).

BUT its project also has an antimony resource, and if the mine moves into production, could produce ~30% of the USA’s domestic needs.

That’s why the US government has deployed ~US$1.8BN in funding at bringing its project online and seen Perpetua’s share price re-rate by over 1,000% over the last ~12 months.

We are primarily Invested in SS1 as an exposure to its giant silver resource estimate.

BUT we think the antimony is an increasingly important side story (especially IF SS1 can define a large antimony resource to go with its giant silver deposit).

We think it could be what SS1 unlocks government funding and support for SS1’s project...

Government funding could also be what unlocks SS1’s project

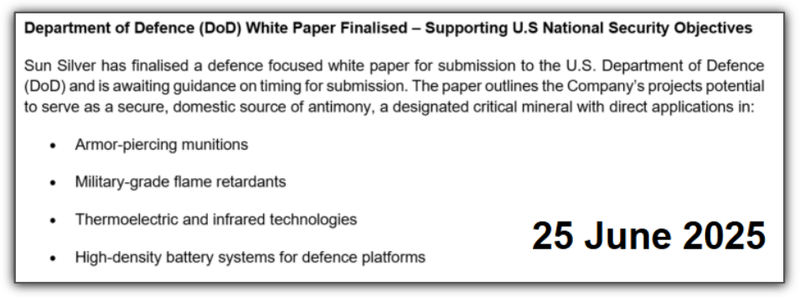

Back in June 2025, SS1 finalised a white paper to submit to the Department of Defence (DoD) for funding.

(Source)

Than in July 2025 explicitly said that it was pursuing US DoD funding.

(Source)

We think government funding could ultimately be what unlocks SS1’s giant silver resource.

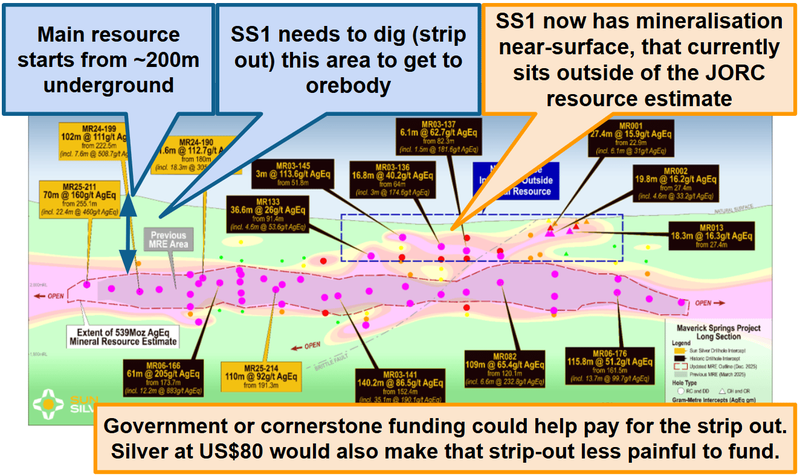

SS1’s silver deposit starts from ~200m underground - which is considered relatively deep.

Yes, an estimated 539M ounces is a LOT of silver, but SS1 needs to dig a big expensive hole (pit) to reach it before they can extract and sell it.

That pre-strip (digging down to the juicy, valuable bits of the project) means a lot of upfront capital spend, which is typically where project financiers get scared off from a project.

Conventional project financiers (and equity investors) want as fast a payback as possible with mining projects. Big upfront CAPEX can scare off these investors.

However, as the silver price goes higher, the pre-strip cost matters less and less, as the value of the in ground silver goes higher and higher.

BUT government funding or some sort of government-backed loan could be what really unlocks SS1’s project.

(Source)

Perpetua Resources’ project had a similar dynamic - a large upfront CAPEX hurdle - and government funding was what started a re-rate in Perpetua’s share price.

Perpetua received commitments for a US$1.8BN loan from US Export-Import Bank and then private capital started pouring into the company in a big way.

As mentioned earlier - Perpetua's market cap has gone from $300M to $6BN.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think a similar re-rate could happen to SS1 if the government was to backstop its project with some sort of funding deal.

SS1 listed in the US in November - which might help with government engagement

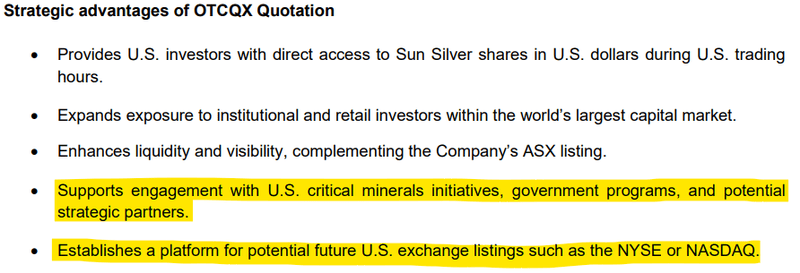

SS1 trades in the US under an OTC listing... which is the first step ahead of a potential future listing on a bigger exchange like the NYSE.

The listing is on the OTCQX which is the highest tier of the OTC, with stricter and higher standards than other OTC exchanges.

Being on a US exchange allows direct access to capital from US based investors and will allow SS1 to gain a more prominent presence within the US.

The aim of this will be to leverage off this to seek out opportunities (government or strategic partners) to help progress the project into development and production.

It was also stated in an announcement back in November last year the intention to list on other US exchanges such as the NYSE or NASDAQ.

(Source)

A US listing could also boost SS1’s chances of getting US government funding/support.

US public support for a company with a US listing could be stronger as opposed to SS1 only being listed in Australia.

That could also mean there is public support for the project from shareholders who buy over there.

See our deep dive on why we think a US listing would be good for SS1 here.

Sun Silver

10 Reasons we are Invested in SS1

The below reasons are from our latest SS1 Investment Memo (published 26 March 2025).

Since then, a fair bit has changed in the markets, so we have included updates below each reason:

1. SS1 has the largest primary silver resource on the ASX

SS1 has a 480M ounce silver equivalent JORC resource estimate.

This is the largest pre-production primary resource on the ASX.

There is a premium attached to being the “biggest” of any commodity in a particular market and funds or investors wanting leverage to silver (without buying the commodity itself) will ideally look to SS1 first.

🚨Update:

SS1’s resource estimate now sits at 539M ounces of silver equivalent.

2. SS1 is extremely leveraged to movements in the price of silver

Silver is generally produced as a by-product from producing base metals. But because SS1 is a primary silver producer, it means that for every US$1 per ounce that silver increases, it has a material increase on the in-ground value of SS1’s project.

This has the effect of SS1’s share price generally tracking very closely to the price of silver.

If silver goes up (and goes up in a big way) then so too should SS1.

🚨Update:

Silver recently hit all time highs at ~$120/oz and has been hovering near US$83/oz, currently up by around 185% from when we published our latest SS1 Investment Memo.

Every time the silver price goes up, the in-ground value of SS1’s 539M silver equivalent JORC resource estimate increases.

3. We are bullish on silver and the price is reaching decade highs

The silver price is re-testing a 12 year high at the time of writing (around US$34/oz) as silver demand is fast outstripping supply.

We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

🚨 Update:

Silver is also up over 250% since SS1 first picked up its project:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

4. SS1 is reaching a size where it could potentially be included in index funds

SS1 is currently capped at ~$103M. It is reaching a size and liquidity profile where it could qualify for inclusion in the ASX indices.

Getting into an index opens up SS1 to a whole new pool of capital and it makes the company a potential investment opportunity for institutional investment funds.

If SS1 gets into an index like the ASX All Ords it could become the de-facto ASX Silver ETF and the only way for passive funds to get leveraged silver pre-production silver exposure on the ASX.

🚨 Update:

We have said previously that the $150-200M range is where SS1’s project will start to enter that “index inclusion territory”.

SS1’s market cap is hovering around ~A$350M.

And now, since the middle of 2025, we have seen the Sprott Silver ETF start buying SS1 shares... (hopefully the first of many indexes/ETF’s).

See our index inclusion thesis here: SS1 index inclusion upside - the only way to get silver exposure on the ASX...

5. The US Department of Defence wants antimony, SS1 may have it

The US imports 90% of its antimony which all come from potentially hostile countries (China, Russia and Tajikistan) and it has no antimony production of its own.

Antimony is a critical mineral for various military applications including as a hardening agent for ammunition.

SS1 has identified antimony across its project from xPRF analysis and drilling data collected in 2024.

🚨 Update:

The US government has started Investing directly into critical minerals projects inside the US.

We have seen the Pentagon take a direct stake in MP Materials.

The US government also took a 5% stake in Lithium Americas.

In December 2025 we saw the following news piece which reads as though the government is not done investing in new projects just yet. (Source)

6. Can SS1 be the next $4.5BN capped Perpetua Resources?

Perpetua Resources has a gold-antimony resource in Idaho, USA.

The US Government, through the Department of Defence, has provided over $50M in grants as well as a $1.8BN loan to help fund the development of the mine.

The US Government was particularly interested in the antimony potential of that project.

We think that if SS1 is able to develop a US-based antimony resource it could also be supported by the US Government - like Perpetua Resources

🚨 Update:

IF SS1 can define an economic antimony resource across its project we think it could become a sort of Perpetua 2.0.

SS1 is currently capped at ~$350M, Perpetua is capped at A$6BN.

Perpetua was also the first company to get investment from JP Morgan as part of its US$1.5 trillion push into critical US industries AND it attracted a strategic investment from Agnico Eagle - the world’s 3rd biggest gold miner.

Check out our side by side comparisons of SS1 and Perpetua here: Is antimony going to be the dark horse for SS1 in 2025?

7. SS1 has a Carlin-Style deposit, cheap and easy to mine.

SS1’s project is located in the “Carlin Trend”, an area that is home to some of the biggest gold and silver mines in the world.

In the mid-1980s Barrick made a Carlin-Type discovery at its “Goldstrike” project in Nevada (not too far from SS1).

This was the project that put the company on the map and produced around 200,000 ounces at 1.2g/t of gold and 200,000 ounces of silver in the mid-1990s.

What made this project so successful was that it was a low cost mining production.

If SS1 can prove that it can extract the gold and silver from its resource with a similar process used by Barrick on its Goldstrike Project it could have a material impact on the feasibility of SS1's project.

🚨 Update:

In a previous SS1 note we did a deep dive on Carlin style deposits and why they are able to operate profitably with low costs.

Check out our deep dive into how SS1’s project compares to $22BN Coeur Mining’s Rochester project here: How does SS1’s project rank against some of the other mines in the region?

8. SS1 is in Nevada USA, near some of the best gold and silver mines in the world.

Nevada is a big mining state and the area of Nevada that SS1 is working in is called Elko County.

There are major gold and silver mines scattered throughout this area of Nevada, and Elko County is very familiar with the mining industry.

$45BN Barrick and $14BN Kinross both own projects in the region.

This means that there is a high level of skilled labour in the area and permitting processes are well known.

9. JORC resource includes ~2.16M ounces of gold

Included inside SS1’s 480m ounce silver equivalent JORC resource is a ~2.16M ounce gold resource.

With the gold price also at record highs, the in-ground value of SS1’s project is also leveraged to the increase in the price of gold.

🚨Update:

After the most recent resource upgrade, SS1’s resource has 2.25M ounces of gold.

Gold is also trading near its all time high at US$5,133 per ounce.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

10. Downstream value add: “Silver paste” production (for solar) could improve economics

SS1 has a giant silver resource within the US. Silver is a key material used in solar panels in the form of silver paste.

SS1 is evaluating the merits of developing downstream silver paste processing.

The world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could add to the merits of the project.

Ultimately, we are hoping a combination of the above reasons help SS1 achieve our Big Bet which is as follows:

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SS1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Other major updates from SS1 since we first Invested

We have been Invested in SS1 for over two years now.

Since then, we have followed and written about SS1 as the company’s story has evolved.

Here is a list of some of the biggest developments for SS1 over that period - basically, this is an archive of SS1’s “best hits” and our take on them:

- SS1 is now the biggest primary silver resource on the ASX

- SS1 is leveraged to the silver price

- Silver to be classified as a critical mineral in the USA?

- Nevada is the “Silver State”, with mines everywhere

- How does SS1’s project rank against some of the other mines in the region?

- From a technical/charting perspective, the momentum is in silver’s favour as well...

- Silver M&A a precursor to a big run in the silver price?

- Silver Squeeze coming?

- Eric Sprott’s silver Exchange Traded Fund (ETF) is buying SS1

- SS1 is also going for downstream value-add opportunities

- SS1’s project could also host a giant antimony resource

- Why an antimony resource could be a game-changer for SS1

- Perpetua Resources - Can one company deliver the US all its antimony needs?

- SS1’s giant silver deposit could be mineralised from surface...

- SS1 is headed for a US stock exchange

- SS1 just raised $30M - led by global institutions

What are the risks?

In the short term we think the key risk for SS1 is “Commodity price risk”.

There is commodity price risk, because SS1’s share price tends to move up and down with the silver price.

IF the silver price was to fall, we would expect to see weakness in SS1’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

Other risks

Like any stock market investment, investing in SS1 carries a range of risks which may affect the value of the company, some of which cannot be predicted (this is the nature of risks).

Here we aim to identify a few more risks.

SS1’s project in Nevada is a large pre-development silver project that is not yet producing.

There is a risk that the project does not progress to production or that development takes longer and costs more than expected.

SS1 remains reliant on the capital markets to fund exploration and development activities. Any future equity raisings could dilute existing shareholders, while debt funding may not be available on favourable terms.

Although SS1’s project is located in a stable jurisdiction, permitting, environmental approvals, and local regulatory processes can still present delays or uncertainties.

Finally, while US government support or funding could act as a major catalyst, there is no certainty that such assistance will be provided.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SS1 Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our SS1 Investment Memo where you will find:

- What does SS1 do?

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.