SS1: The biggest pre-production silver project in the USA also contains antimony?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,374,000 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

Sun Silver (ASX:SS1) has the largest pre-production silver project in the USA.

(and on the ASX)

SS1 has a 480 million ounces of silver equivalent JORC resource in Nevada, USA.

Our bet back in early 2024 was that SS1 would materially rerate if the silver price kept rising.

Last night the silver price was trading above $US37 - it’s up by US$5 per ounce over just the last ~60 days.

And over the last 15 days the silver price looks like, in our opinion, it wants to keep going higher.

A materially rising silver price is the exact scenario we wanted to see start playing out for our Investment in SS1.

You can do the maths on what every US$1 per ounce increase in the silver price means for the estimated in ground value of SS1’s 480 million ounce silver equivalent resource. But of course, there are operational costs and risks associated with removing the silver, which we haven’t considered.

At last traded price of ~83c SS1 is capped at $121M.

What we did NOT predict as part of our SS1 Investment thesis is that SS1 could have antimony running all through its giant, USA silver deposit.

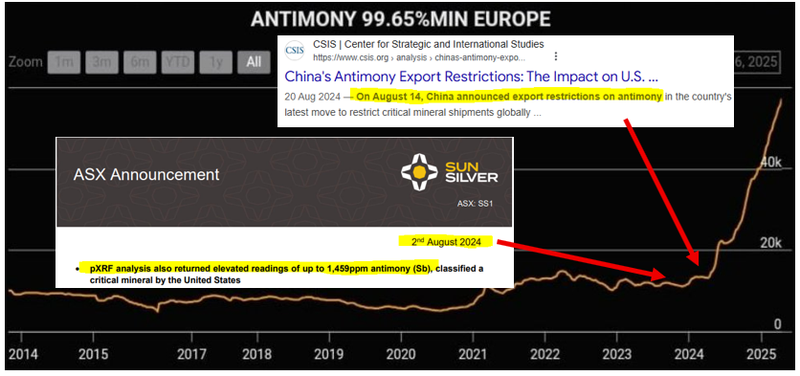

Antimony is a critical defence metal, USA has no domestic supply, the antimony price is up 300% over the last 6 months and ASX stocks with US based antimony projects have been delivering price runs on volume.

We are waiting for the results from SS1’s current drill campaign which could return even more silver hits WITH antimony AND waiting on re-assay results of ~200 historical drill holes that were never assayed for antimony (only for silver and gold).

(SS1 discovered and started work on antimony last year, before anyone cared about antimony, so they have a nice head start)

Here’s the SS1 antimony story and what could happen next:

SS1’s 480 million ounce silver equivalent JORC resource is from ~200 historical drill holes plus some new drilling done by SS1 over the last ~12 months.

Nearly a year ago, back in early August 2024 (before anyone cared about antimony), SS1 reported surprise antimony grades in all their NEW silver drill hits.

SS1’s new drilling back in August 2024 returned antimony - So why didn’t the ~200 historical holes have antimony grades too?

Turns out the ~200 historical holes were never tested for antimony, only for silver and gold:

SS1 is working on a theory that there could be a significant antimony deposit running through their giant silver resource.

To test this theory, SS1 chose FIVE historical drill holes to test for antimony.

To get a sense of how far the antimony might be spread out across their silver deposit, they chose far apart historical holes to test:

In September 2024, SS1 announced that all five of the historical holes tested returned antimony (Source).

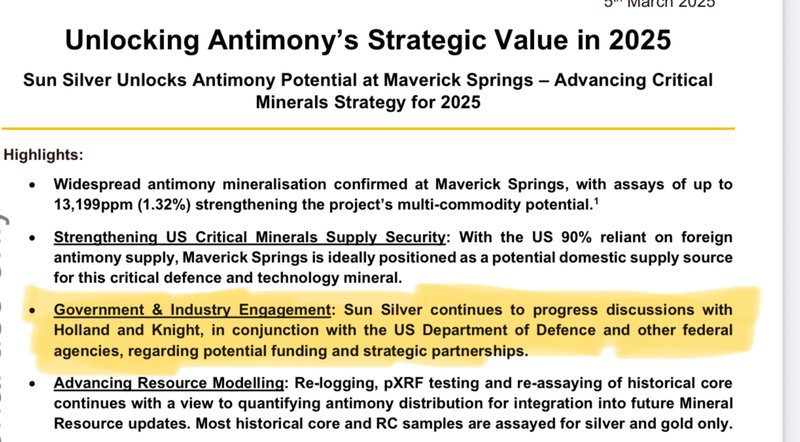

(Source - SS1 Announcement 5th March 2025)

And holes tested were up to 1.3km apart - here is what it looks like from a helicopter view:

SS1 has been working out if antimony runs through its entire giant silver deposit for almost a year now.

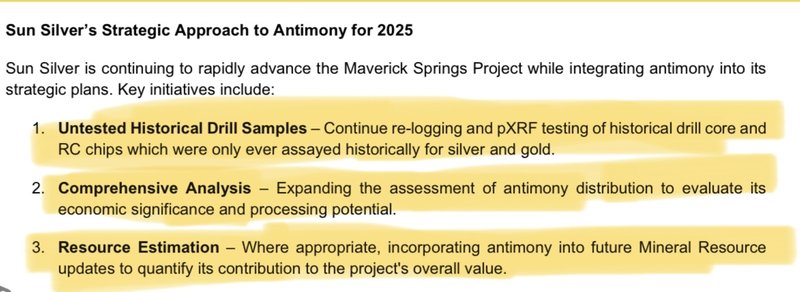

In March this year, SS1 put out an announcement outlining its “antimony strategy for 2025”:

(Source - SS1 Announcement 5th March 2025)

Including trying to secure US Department of Defence funding to progress its project...

More of these historical holes are being tested for antimony right now.

(Source - SS1 Announcement 5th March 2025)

With silver and antimony prices both running, It may be a good time to have a 12 months start on a giant silver project that might contain a significant deposit of a critical defence metal like antimony.

Especially given SS1’s project is located in the USA.

US precious metals exposures with a critical minerals angle have been running of late...

Dateline Resources was up ~56x in 45 days.

And our latest Investment Resolution Minerals (ASX: RML) is up ~300% in 7 days.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

SS1 is currently in the middle of a drill program targeting a resource upgrade later in the year.

SS1 could announce big silver (and antimony) hits from new drilling OR antimony from testing more historical drill holes at any time.

While silver and antimony prices are running:

For a nice 3D visual run through of SS1’s project click here

You can zoom around the historical cores that make up SS1’s giant silver resource and see how many have not yet been tested for antimony.

(Click here to zoom around SS1’s drill holes in 3D - use the buttons circled in red above to navigate)

What could trigger a run in SS1’s share price in 2025?

- Silver price runs - The first is pretty simple, IF the silver price runs, then we would expect SS1’s share price to follow.

- Exploration success - SS1 is drilling right now. Anything that extends the current resource OR adds shallow mineralisation the resource could be a game changer for SS1 (especially a big silver hit or antimony hit, or more mineralisation near surface)

- SS1 silver resource update - SS1 updating its resource from inferred to indicated status could unlock institutional/corporate interest in its project.

- Metallurgical testwork - in an interview this week, SS1 MD Andrer Dornan mentioned hat SS1 would be testing to see if its project is “heap leachable”. IF SS1 can show that its project can be heap leached it would instantly become a well understood mega project that the bigger players would surely want a piece of.

- SS1 hits market cap/trading volume requirements to get into an index - This one is somewhat outside of the company’s control, but as the market cap gets bigger, SS1 becomes more investable for larger institutions. We are hoping SS1 can hit the $150-200M market cap this year and get included in one of the ASX indices.

- Antimony surprise - SS1 could publish an antimony resource by re-assaying historical drill cores that were not tested for antimony. Antimony could signal to the market that SS1’s project is of ‘strategic importance’ to the US Government.

Antimony could unlock government funding for SS1

Perpetua has managed to attract almost US$2BN in government funding support for its gold project (which just so happens to have the biggest antimony resource in the USA).

US funding support is a big part of the reason why Perpetua is up ~1,000% over the last ~18 months.

A big part of the reason why we think antimony could be important for SS1 is because it may unlock similar non-dilutive funding sources...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

SS1’s silver resource on its own is already big enough BUT any hint of antimony potential may be what attracts US government funding to fast track its project into development.

(an almost identical position to where Perpetua was ~24 months ago)

SS1 currently has someone working on potential Department Of Defence funding:

SS1 now finds itself in a position where:

- ● The silver price looks like it wants to breakout (in our opinion)

- US metals projects are in favour and the market is rewarding stocks

- SS1’s project is the single biggest pre-production exposure to both of those thematics...

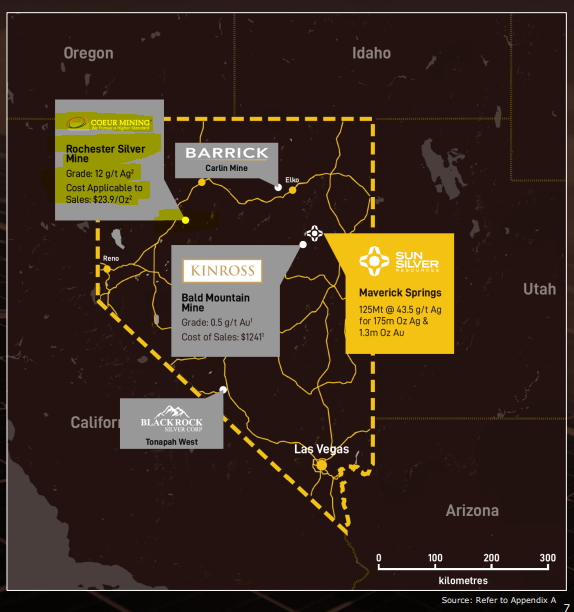

We just got back from a trip around the US - where we drove through Nevada and past a few of those mega mines...

Some of the world’s biggest mines operate in this part of the world - including the Rochester mine which is operated by A$9BN Coeur - the world’s biggest silver miner.

We think there are a lot of parallels that can be drawn between Rochester and SS1’s project - especially around size.

BUT SS1’s project has almost double the grade.

Yesterday, we watched the following interview with SS1’s Chair/MD Andrew Dornan, where he highlighted those parallels (and a lot more):

(Watch the interview here)

The interview gave us a pretty good idea of the key bits of news flow to watch out for over the next few months.

All of which we think could re-rate SS1’s share price higher in a market that is responding really well to silver names and US based mining stocks.

Antimony may signal to the market that SS1’s project is of ‘strategic importance’ to the US Government.

Silver M&A a precursor to a big run in the silver price?

There were a fair few interesting points made in the interview with Andrew on the broader silver macro environment.

There were mentions of silver being used in solid state batteries and in AI data centres.

But the one that stood out to us the most was around M&A being a precursor to a big price run in silver.

The two talked about how M&A is usually a good signal of a coming price run in a commodity.

We tend to agree with that opinion.

We saw the same thing happen in the gold sector ~12-18 months ago where the Newcrest/Newmont deal announced in late 2023 triggered the start of a wave of M&A.

Then, the gold price started taking off:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The silver price has been flirting with a breakout (and looks like it may have finally done the same?).

And the silver M&A wave started in late 2024 and really kicked into gear over the last two months.

And we have just come off the back of a wave of M&A Silver sector is currently going through a period of consolidation...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think the silver price is about to go on a big run...

And so do some well respected technical chart analysts.

A few weeks ago we wrote about what a breakout in silver prices might look like above the US$35 per ounce level.

That level was something that many chartists (including Michael Oliver - a well known technical analysis expert) have been calling a key level to watch....

In a recent webinar we listened to Michael Oliver said “If silver goes above $35, watch out because if it goes above $36 its a triple top breakout”

Oliver also said that if the breakout happens “we are going to get another launch” and when we get it “it will be at a speedier process than what gold is currently doing”.

So far he has been correct - hopefully that gold style run comes next...

(Check out the Silver Slingshot Webinar here - the chart commentary is at ~7 minutes in)

We think that if the Silver price starts running, SS1 will be the main beneficiary of a flow of capital into the sector.

10 Reasons we are Invested in SS1

These reasons are from our latest SS1 Investment Memo (published 26 of March 2025).

Since then a fair bit has changed in the markets - it feels like we are in the early stages of a bull market...

Silver looks like it wants to breakout in our opinion AND US metals are in favour with the market.

As a result we have included updates below each reason:

1. SS1 has the largest primary silver resource on the ASX

SS1 has an estimated 480M ounce silver equivalent JORC Resource.

This is the largest pre-production primary resource on the ASX.

There is a premium attached to being the “biggest” of any commodity in a particular market and funds or investors wanting leverage to silver (without buying the commodity itself) will ideally look to SS1 first.

2. SS1 is extremely leveraged to movements in the price of silver

Silver is generally produced as a by-product from producing base metals. But because SS1 is a primary silver producer, it means that for every US$1 per ounce that silver increases, it can have a material increase on the in-ground value of SS1’s project.

This has the effect of SS1’s share price generally tracking very closely to the price of silver.

If silver goes up (and goes up in a big way) then so too may SS1.

Update:

Silver is already up US$4 per ounce (~11%) from when we published our last SS1 Investment Memo.

Based on SS1’s 480M silver equivalent JORC resource that is >US$1.6BN increase in the in-ground value of the resource.

Note* These are high level calculations, in-ground values don’t consider the cost of extracting and processing that resource. It’s hard to say how much of that in-ground value converts into above ground value.

3. We are bullish on silver and the price is reaching decade highs

The silver price is re-testing a 12 year high at the time of writing (around US$34/oz) as silver demand is fast outstripping supply.

We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

Update:

Silver is up over 11% since we launched our latest SS1 Investment Memo.

Silver is also up over 68% since SS1 first picked up its project:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Check out our last note here where we launched our latest Investment Memo: SS1: Increases to 480M ounces of silver equivalent resource... and identifies at surface and near surface mineralisation.

4. SS1 is reaching a size where it could potentially be included in index funds

SS1 is currently capped at ~$103M. It is reaching a size and liquidity profile where it could qualify for inclusion in the ASX indices.

Getting into an index opens up SS1 to a whole new pool of capital and it makes the company a potential investment opportunity for institutional investment funds.

If SS1 gets into an index like the ASX All Ords it could become the de-facto ASX Silver ETF and the only way for passive funds to get leveraged silver pre-production silver exposure on the ASX.

Update:

At yesterday’s close price (83c) SS1’s market cap is now ~$121M.

We have said previously that the $150-200M range is where SS1’s project will start to enter that “index inclusion territory”.

The perfect storm would come in a scenario where the silver price is testing new all time highs and index buying has started in SS1.

See our index inclusion thesis here: SS1 index inclusion upside - the only way to get silver exposure on the ASX...

5. The US Department of Defence wants antimony, SS1 may have it

The US imports 90% of its antimony which all come from potentially hostile countries (China, Russia and Tajikistan) and it has no antimony production of its own.

Antimony is a critical mineral for various military applications including as a hardening agent for ammunition.

SS1 has identified antimony across its project from xPRF analysis and drilling data collected in 2024.

Update:

The US government just proposed the “2025 Budget Reconciliation Bill” which includes ~US$2.5BN in funding support for U.S production of critical minerals.

There is also ~US$500M allocated to the Department Of Defence aimed at developing critical minerals supply chains.

That bill is expected to pass in July.

Earlier this week the G7 also called for "immediate and scaled investment" to secure critical mineral supply chains.

(Source)

We think the government funding available for critical mineral resources just keeps growing.

6. Can SS1 be the next $1.1BN capped Perpetua Resources?

Perpetua Resources has a gold-antimony resource in Idaho, USA.

The US Government, through the Department of Defence, has provided over $50M in grants as well as a $1.8BN loan to help fund the development of the mine.

The US Government was particularly interested in the antimony potential of that project.

We think that if SS1 is able to develop a US-based antimony resource it could also be supported by the US Government - like Perpetua Resources.

Update:

Perpetua is now capped at ~$1.9BN and was just added to the “FAST-41 program” for fast tracked permitting of its project.

The US wants projects to come online.

IF SS1 can define an antimony resource across its project we think it could become a sort of Perpetua 2.0.

Interestingly SS1’s biggest shareholder Nokomis Capital (owns 8.9% of SS1) was also an investor in Perpetua...

Check out our side by side comparisons of SS1 and Perpetua here: Is antimony going to be the dark horse for SS1 in 2025?

7. SS1 has a Carlin-Style deposit, cheap and easy to mine.

SS1’s project is located in the “Carlin Trend”, an area that is home to some of the biggest gold and silver mines in the world.

In the mid-1980s Barrick made a Carlin-Type discovery at its “Goldstrike” project in Nevada (not too far from SS1).

This was the project that put the company on the map and produced around 200,000 ounces at 1.2g/t of gold and 200,000 ounces of silver in the mid-1990s.

What made this project so successful was that it was a low cost mining production.

If SS1 can prove that it can extract the gold and silver from its resource with a similar process used by Barick on its Goldstrike Project it could have a material impact on the feasibility of SS1's project.

Update:

In our last SS1 note we did a deep dive on carlin style deposits and why they are able to operate profitably with low costs.

Check out our deep dive into how SS1’s project compares to $9BN Couer Mining’s Rochester project.

See that deep dive here: How does SS1’s project rank against some of the other mines in the region?

8. SS1 is in Nevada USA, near some of the best gold and silver mines in the world.

Nevada is a big mining state and the area of Nevada that SS1 is working in is called Elko County.

There are major gold and silver mines scattered throughout this area of Nevada, and Elko County is very familiar with the mining industry.

$45BN Barrick and $14BN Kinross both own projects in the region.

This means that there is a high level of skilled labour in the area and permitting processes are well known.

Update:

We just got back from the US and got to see these giant deposits in the flesh.

This whole region is full of mining towns and it's easy to see how a giant resource like SS1’s could be developed.

9. JORC resource includes ~2.16M ounces of gold

Included inside SS1’s 480m ounce silver equivalent JORC resource is a ~2.16M ounce gold resource.

With the gold price also at record highs, the in-ground value of SS1’s project is also leveraged to the increase in the price of gold.

10. Downstream value add: “Silver paste” production (for solar) could improve economics

SS1 has a giant silver resource within the US. Silver is a key material used in solar panels in the form of silver paste.

SS1 is evaluating the merits of developing downstream silver paste processing.

The world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could add to the merits of the project.

Update:

A big part of the long term bet for SS1 is that its silver would be used downstream to produce silver paste that goes into solar panels.

Check out our deep dive on SS1’s silver paste angle here: Silver Squeeze coming?

What could go wrong?

In the short term we think there are two key risks for SS1.

First is “Commodity price risk” and second is “Funding/dilution risk”.

Commodity price risk, because SS1’s share price moves up and down with the silver price.

IF the silver price was to fall, we would expect to see weakness in SS1’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

Funding/dilution risk, because there is always a chance SS1 looks to raise some cash off the back of momentum in its share price.

Raising cash is always a good thing in the long run because it gives the company cash to do things.

In the short term it creates some selling pressure from the investors who may look to flip their shares for a quick profit.

Funding risk/dilution risk

As a small cap, SS1 is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, SS1 could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

Other Risk

Investing in Sun Silver Limited (ASX:SS1) carries other risks which may affect the value of the company. The Company’s primary asset is a pre-production silver and potential antimony project in Nevada, USA, and its prospects are inherently speculative. As mentioned the value of SS1 is highly sensitive to fluctuations in commodity prices—particularly silver, amd maybe antimony. A sustained downturn in these prices could materially impact the project’s economic viability.

There is also exploration and development risk. The Company is currently re-assaying historical drill holes and undertaking new drilling to confirm the presence and extent of antimony, which remains unproven at commercial scale. Metallurgical test work is ongoing, and the project’s ability to proceed to heap leach production has not yet been demonstrated.

Additionally, there is no guarantee SS1 will receive government funding or support, including from the US Department of Defence, despite strategic interest in antimony. The Company is as mentioned reliant on capital markets to fund development, and any capital raise may dilute existing shareholders.

Finally, regulatory, environmental, and permitting risks in the US jurisdiction—while generally stable—may delay or adversely affect development.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SS1 Investment Memo:

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our SS1 Investment Memo where you will find:

- What does SS1 do?

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.