JBY is surrounded by the one of the world’s biggest gold mines - here’s what we saw on site

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,807,167 JBY shares and the Company’s staff own 33,334 JBY shares at the time of publishing this article. The Company has been engaged by JBY to share our commentary on the progress of our Investment in JBY over time.

We’ve now seen it with our own eyes.

And the photos in the announcements and investor deck just don’t do it justice.

Behold...

We just got back from a trip around the USA visiting a few of our Investments in the country.

One of those was a visit to James Bay Minerals (ASX: JBY)’s gold project in Nevada.

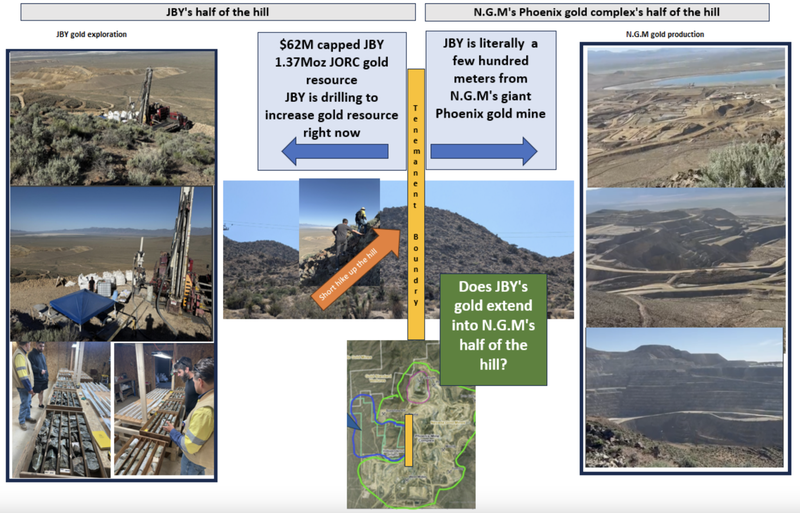

JBY has an existing ~1.37M ounce gold resource and is currently drilling to grow it even further.

It’s currently capped at ~ $62M.

JBY is one of our largest positions, so it was great to finally see it in real life.

(especially witnessing what sits just a few hundred meters away right next door...)

Today we will cover what we saw on site, and all the things we learnt, with plenty of photos.

What we have always liked about JBY is that its ground is practically SURROUNDED by Nevada Gold Mines (N.G.M)’s giant Phoenix mine complex.

That’s what you can see in the video above, filmed just a few hundred meters away from JBY’s drill rig.

(N.G.M. is a joint venture between gold majors $55BN Barrick and $95BN Newmont.)

The Phoenix mine produces ~240k ounces of gold per annum - enough gold to make this single pit alone a top 5 producer on the ASX.

...and it has been producing gold for over 50 years.

We had previously seen how this looks in the JBY announcements and presentations:

(this image is a couple of months old, the market caps of Barrick and Newmont are higher now)

... but we weren’t quite prepared for seeing it all in real life.

JBY’s project doesn't just border N.G.M’s ground... it is essentially a part of the overall mine complex.

The two are so close that when we hiked the hill from where JBY was drilling, right up to JBY’s project boundary (~15 min hike), we were basically staring straight into N.G.M’s pit and operation...

(15 min hike up a hill - no Coke Zeros or nicotine gum vending machines up here)

Here’s that video again that we took from JBY’s ground into the “neighbour’s yard”:

After seeing how close JBY is to the giant Phoenix mine complex in real life, we came up with this rough image to illustrate it:

Taking the photo of the gold mine from JBY’s half of the hill:

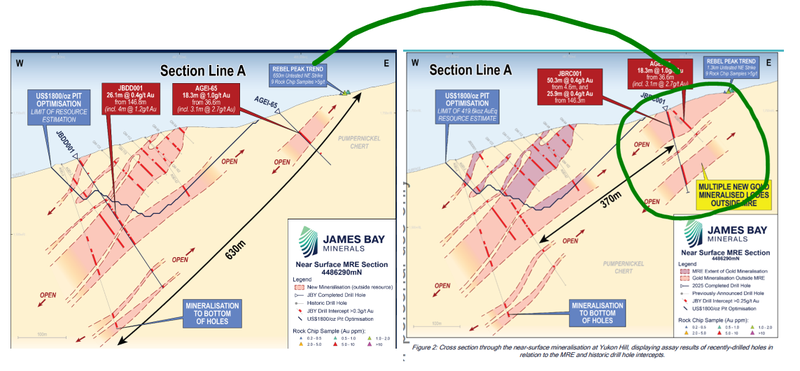

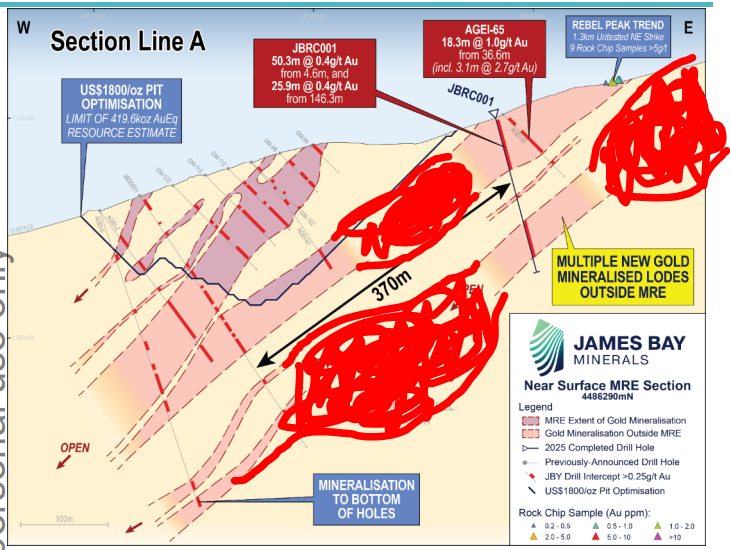

So as we said above, JBY has an existing ~1.37M ounce gold resource and it’s currently drilling to try and grow that resource even further.

JBY released a batch of assay results earlier this week which show that JBY is hitting near surface extensions to its resource.

With the next batch of drilling results we want to see the resource get even bigger.

...and continue edging closer towards the monster, producing, gold mine that encroaches around JBY's space like a round person in an economy plane seat...

(More on the drilling results from earlier in the week later in today’s note).

We were up at the site last week, hosted by JBY’s exploration manager (thanks for showing us around Alex).

Here is a TLDR summary of our key takeaways from our site visit:

- Just how close JBY’s project is to N.G.M (Barrick and Newmont).

- The size/scale of N.G.M’s Phoenix mine (hard to believe without seeing it in person).

- Why we think N.G.M might be interested in oxide ores (like JBY’s)

- JBY’s ground literally borders N.G.M’s open pits...

- How common heap leaching gold operations are in the US (especially in Nevada).

- Why rock chips matter and JBY still hasn't drilled it highest grade targets

- N.G.M’s Sunshine pit is a good analogue to how JBY’s resource could be developed

- How JBY could access its deeper (980k ounces at 6.67g/t gold) skarn resource.

- How close JBY’s project is to mining towns (full of services providers/consultants)

- How the recent land expansion fits into JBY’s overall strategy.

Next we will unpack all of these key takeaways.

Key takeaways from our JBY site visit

1. How close JBY’s project is to N.G.M (Barrick and Newmont)

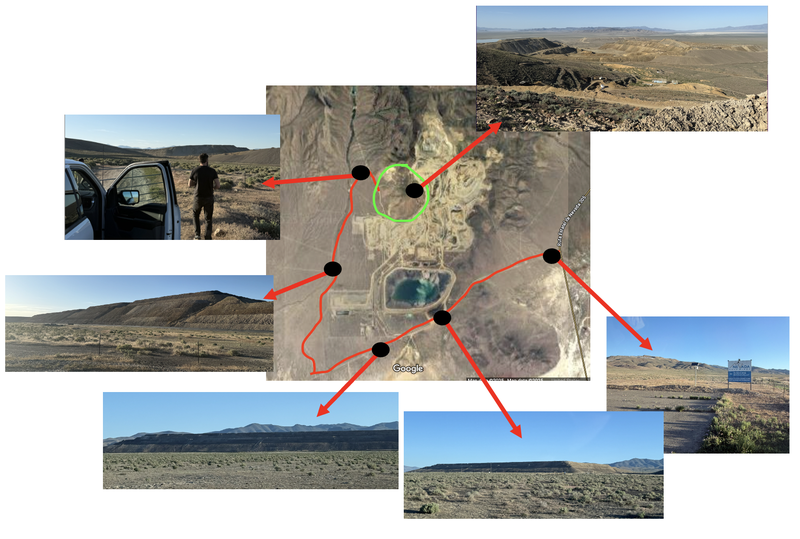

It is hard to appreciate just how close the two projects are without going to site and seeing it.

JBY’s project is basically surrounded by N.G.M.

To get to JBY’s project, we had to drive around N.G.M’s giant leaching pads and the giant pit.

Here are a few pictures from different points on the drive into JBY’s project:

2. Size/scale of N.G.M

The Phoenix pit produces ~240k ounces of gold per annum - enough gold to make this single pit a top 5 producer on the ASX.

The mine has been operating for over 50 years, and getting the project to where it is today would have meant billions and billions of dollars of sunk cost into the mine.

All that sunk cost means N.G.M are heavily incentivised to keep the operation going for as long as possible... which means a nearby ore supply (like JBY’s) could be valuable to them...

3. N.G.M could do with more oxide heap leachable ore

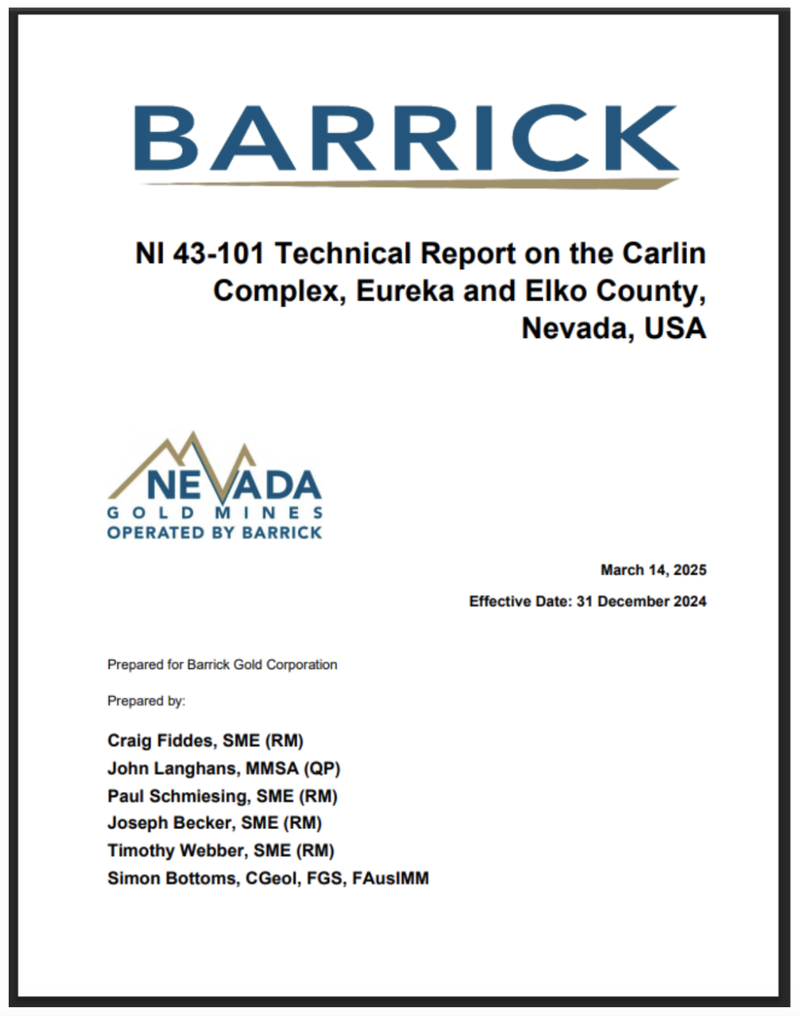

N.G.M is currently trucking concentrates from its Phoenix mine to its Goldstrike processing plant in Carlin.

This tells us that the production coming out of Phoenix right now is not really amenable to being processed on site at Phoenix (using heap leach processes).

We read this in Barrick’s “NI 43-101 Technical Report on the Carlin Complex, Eureka and Elko County, Nevada”.

Here is that reference to the Carlin plants processing “third part ores” from Phoenix.

(Source)

The Phoenix mine site is set up to process oxide ores (via heap leaching).

JBY’s shallow resources (~385k ounces of gold) are all oxide hosted.

We think JBY’s project (IF JBY can prove up a large amount of gold) could start to look attractive to N.G.M for processing on site using the heap leach pads.

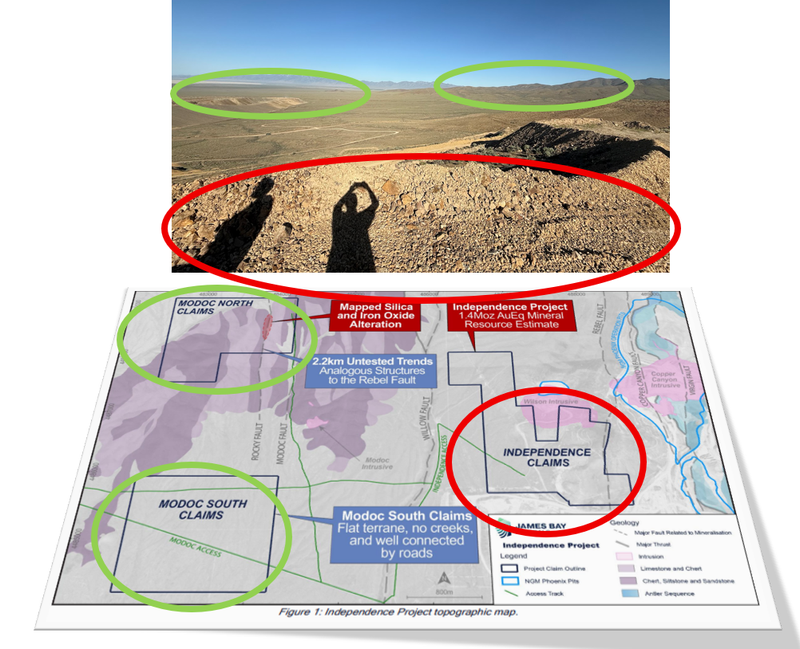

4. JBY holds 50% of a small mineralised hill, N.G.M the other half

We hiked up the hill where JBY’s resource sits and where JBY is currently drilling.

JBY’s highest grade rock chips actually came from right up here near the border with N.G.M’s ground.

We also went up to the “Rebel Peak” targets, where basically half of the mountain is owned by JBY and the other half N.G.M:

Here is our attempt to show it in one image:

(apologies, we are not 3D graphic designers)

Here is another way to look at it:

5. Heap leaching gold operations are common in Nevada

While in Nevada, we learnt a lot about “heap leach” gold processing operations.

Have you ever tuned out when a stockbroker or company CEO starts talking about “the potential of quick and low cost near term production heap leach operation.”

We did too - until we actually saw and understood it, especially in the context of the USA.

Australians generally don’t really understand heap leeching - it's more a USA thing.

Heap leaching is a simple and fast way of extracting gold and is very common in the US (especially in Nevada).

Heap leaching, because of its simplicity, makes 0.3-1 g/t ore bodies economically viable to mine.

Heap leaching operations are very well understood in the US - we many heap leach operations on the our drive, including Round Mountain owned by $29BN Kinross - again it was a huge project, and these photos don't properly do it justice.

How does heap leaching work?

OK bear with us for a quick minerals processing lesson. Skip this if you are already qualified.

Heap leaching is when crushed ore is placed on a “pad” (think of it like a giant tarpaulin to stop chemicals getting into the ground.

Cyanide is sprayed onto the crushed ore, and then the cyanide solution is caught in the channels around the “pad” and sent off for processing into gold.

(Source)

Here was a picture of N.G.M’s heap leach pads (notice the pipes running up the hill - that’s where solution is pumped onto the pads):

And if you squint hard and we draw your eyes to it, you can make out the protective barriers to stop solution leaving the pad’s perimeter:

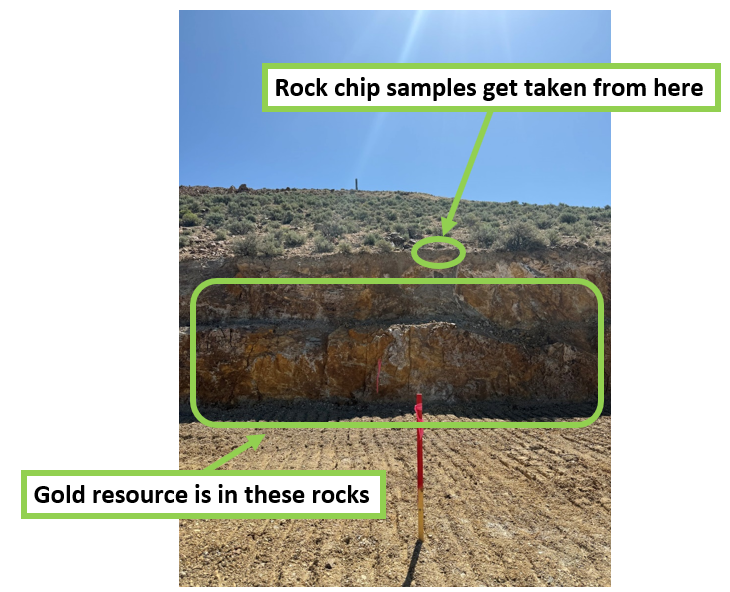

6. JBY’s highest grade rock chips haven’t been drilled yet

Rebel Peak is where JBY picked up gold grades up to 16.6g/t gold.

Rock chips for JBY are important because a lot of its mineralisation starts from surface:

JBY is currently building the road access to get to the Rebel Peak target which hasn't been properly tested with the drill bit YET.

7. Sunshine pit showing how JBY’s project could be mined

Sitting across JBY’s project area is the Sunshine pit that was previously mined by N.G.M.

The reason we think this pit matters is because it gave us a pretty good idea of how JBY’s project could be developed and mined out.

The Sunshine pit sits on very similar topography and so its easy to see how JBY could mine out its resource:

8. Deeper skarn - not actually that difficult to access...

The deeper part of JBY’s resource (980k ounces at 6.67g/t gold) is well below JBY’s shallow ‘at surface’ resource - the thing to note though is that “surface” is actually the top of a mountain - which means that skarn would actually be a lot easier to access.

N.G.M have already mined out a nice big open pit over the border which could make accessing JBY’s skarn resource a lot easier (from either side of the big hill).

It would be a case of just building an underground decline from the bottom of the mountain straight into the guts of the skarn resource:

9. 20 minutes away from mining services town

The night before our site visit, we drove around the towns of Elko and Battle Mountain, trying to get a sense of the place.

Here are some pictures from the drive through Elko, Carlin and into Battle Mountain - notice the theme:

Both towns were full of mining service providers.

In fact every second building was somehow related to the mining industry - either a drilling company, an engineering company, some sort of project consulting business or a mining company itself.

Battle Mountain is ~20 minutes away from JBY’s site and Elko is ~80 minutes away.

That would make building and operating a mine easy relative to a lot of other places in the world.

Drilling and other pre-development work should be even easier - if a piece of drilling equipment is damaged, it's a ~20 minute drive to town on sealed roads to get a replacement part - instead of days and weeks of delays waiting for parts to arrive in a remote location...

While we were hiking up JBY’s hill, we literally saw the drillers drive to town to get a spare part for the drill rig, and they got back while we were coming back down the hill.

(remember the horrors when IVZ needed to replace a broken drilling part in remote Zimbabwe, and drilling was delayed by weeks while the part was found and flown in? None of that here)

Here is where JBY’s project sits on the map relative to the three major mining towns nearby:

10. JBY’s recent land expansion setting up the company for long term

We also got to look at JBY’s new ground that was picked up only a few weeks ago.

Here is where that ground sits relative to our position on top of JBY’s existing resource:

One of the key questions we had before going to site was where JBY could set up its processing/leaching operations IF it took its project into production itself.

The new ground answers that question.

The flat bit of ground would definitely be suitable to set up all of the project infrastructure, relaxing the space on the hill for mining and the flat ground for processing.

That ground on the left in the photo is literally a 5 minute drive from where JBY’s resource sits.

The ground on the right in the photo, is JBY’s exploration upside.

Once JBY is done drilling out and bringing its current project area closer to development, it could also switch focus to greenfields exploration on this ground.

The aim there would be to try and replicate what JBY has right now on that area:

JBY is set up now for a scenario where it can develop its existing resource and then use cashflows to explore the ground to the north.

What’s Next: Key things to watch out for:

Post site visit, we always walk away with a whole different perspective of what the real needle movers for a project could be.

For JBY we think the following are the key things to watch going forward:

1. Expanding the shallow resource is key 🔄

As mentioned earlier, the type of geology and relevance to N.G.M’s operation next door means this is where JBY can have the easiest wins.

A big win from this would be if JBY can grow the resource from surface, to the north - which is exactly what we saw from the drill results earlier this week.

Here is what we are hoping to see from the next batch of drilling:

JBY is still only in the middle of its drill program so we should know whether or not the resource is getting bigger to the north fairly soon...

2. Assays pending on deeper skarn + Metwork 🔄

JBY has also flagged it would do some metwork testing on its deeper skarn resource which is ~984k ounces of gold at 6.64g/t.

From that work we are hoping to see recoveries that somewhat resemble the ones from N.G.M’s Fortitude pit which has mined ~2.3M ounces of gold from similar geology.

If the metwork is similar, the look through for us will be that JBY’s resource might also be feasible to mine.

Well understood recoveries could also pique the interest of N.G.M who are likely keeping a close eye on everything JBY is doing given the proximity of its ground to N.G.M’s operations.

3. Re-assaying old cores 🔄

We are also watching out for re-assaying results from the old deep diamond drillcores that were never tested for gold.

These should give us some more information on whether or not there is gold in between JBY’s shallow and deep resources:

We think that any major unexpected surprises across any of the three above could contribute to JBY achieving our Big Bet which is as follows:

Our JBY Big Bet:

“JBY re-rates to a +$300M market cap by expanding its large US gold resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our JBY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What are the risks?

In the short term the key risk for our JBY Investment Thesis is exploration risk.

JBY still has assays pending from its last drill program AND plans to start drilling again later this quarter.

There is no guarantee that any of that drilling delivers any economically viable drill results.

If that were to happen we would expect the market to react negatively and move the JBY share price lower.

Exploration risk

There is no guarantee that JBY can increase its existing resource estimate through exploration drilling. There is always a chance that drill programs fail to find any economic mineralisation that may not add to the project’s overall resource estimate.

Source: “What could go wrong” - JBY Investment Memo 25 November 2024

Another risk is “funding risk”.

JBY had $6.2M cash in the bank at 31 March 2025 but given the company is actively drilling it could look to up its cash balance with a capital raise inside the next 6 months.

A capital raise could put some short term pressure on the company’s share price.

Funding risk/dilution risk

JBY is a small cap that is not generating any revenues at the moment. As a result, the company is reliant on access to financing from the market. If there is any negative news (macro or fundamental) then JBY may be forced to raise capital at lower share prices. Capital raises at lower valuations could dilute the ownership of existing shareholders and cap the upside potential of the company’s share price

Source: “What could go wrong” - JBY Investment Memo 25 November 2024

To see other risks to our Investment Thesis, check out our JBY Investment Memo here.

Our JBY Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our JBY Investment Memo where you will find:

- What does JBY do?

- The macro theme for JBY

- Our JBY Big Bet

- What we want to see JBY achieve

- Why we are Invested in JBY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.