How high will the gold price go? How big is JBY’s USA gold resource?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,979,167 JBY shares and the Company’s staff own 33,334 JBY shares at the time of publishing this article. The Company has been engaged by JBY to share our commentary on the progress of our Investment in JBY over time.

‘He who has the gold makes the rules’...

Did the US President just tell everyone to buy gold?

Trump posted the following on TruthSocial over the weekend...

After that post, the gold price shot up 6% by ~US$250 per ounce (over just two days).

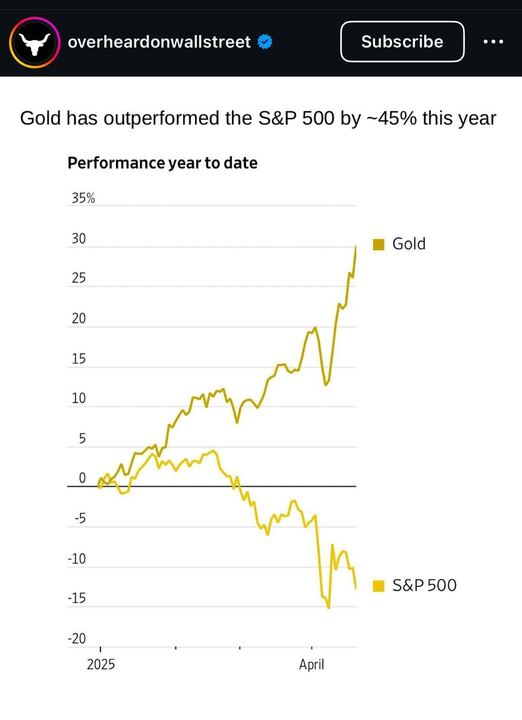

Gold has been inescapable in the media of late, fed by global tariff wars, doubts about US reserve currency status and because gold has been a safe haven asset for thousands of years.

The gold price is currently sitting at US$3,360/ounce. It’s finally taken a healthy little breather overnight, after running up over 30% since the start of the year.

Some pundits are predicting a gold price as high as US$5,000/oz...

Our Investment, the $64M capped James Bay Minerals (ASX: JBY), has a 1.4M ounce gold JORC resource in Nevada USA.

Why has the JBY share price been running on no news over the last two days?

Probably due to the gold price...

Plus we expect expansion drilling to start any day now....

(based on JBY’s March 27th "mobilisation commenced” announcement)

We’ll explain in detail what drill results we are looking for that should move the JBY share price, later in this note (no guarantees of course).

JBY’s edge is specifically where its project is located - and that’s not simply about ease of getting Uber Eats deliveries to site (more on this later).

JBY’s project is right next door (almost surrounded in fact) to one of the world’s biggest gold complexes - “N.G.M” - owned by Barrick and Newmont.

A “complex” in this instance refers to a group of gold mines.

(and N.G.M stands for ‘Nevada Gold Mines’)

This group (or “complex”) of producing mines (circled in green above) has been producing gold for over 40 years - throughout all gold price environments. It must be pretty profitable today...

The N.G.M gold complex that almost surrounds JBY’s project was formed when $55BN Barrick Gold and $96BN Newmont combined all their mines in the area into a joint venture, back in 2019.

Right now, the N.G.M complex is producing ~250k ounces of gold per annum.

(that’s ~A$1.3BN in gold per annum at a A~$5,400 gold price).

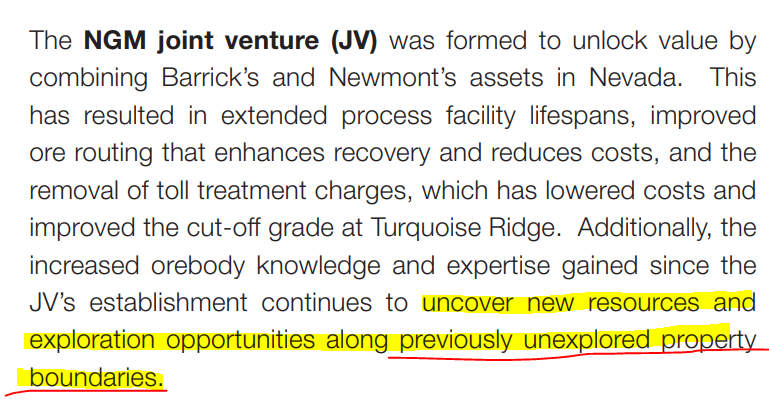

And the N.G.M complex is looking to expand its in-ground gold resource to feed its processing plants:

(Source - Barrick 2024 Annual Report)

In addition to having resource growth plans, Barrick and Newmont already have a large ‘Plan of Operation’ across the entire region that permits gold mining. This area includes JBY’s project - which could save JBY years of time in permitting purgatory...

So how did tiny JBY even get its hands on this 1.4Moz gold project that sits almost inside the N.G.M gold complex?

It was acquired off a distressed private seller back in 2024 before the gold price really started moving.

Two months ago - ex-chief exploration geologist for Barrick and the N.G.M complex - Keith Wood joined JBY as a strategic advisor (more on Keith's CV later).

Keith’s previous job at the N.G.M complex was to find more gold in nearby, unexplored areas...

... which sounds exactly like what JBY is doing right now.

JBY is currently capped at $64M.

Meanwhile for the first time in decades, gold in the US is entering mainstream consciousness...

As we noted above, so far this year gold is up by over 30%, and it looks like it wants to keep running.

Some reputable analysts are saying it will be at US$4,500 per ounce before the end of the year.

We wont mention the lofty gold price predictions of the tinfoil hat crowd.

A high gold price is just the right time for JBY to put capital into drilling and expanding its gold resource, and to be rewarded by the market if successful...

Especially if the N.G.M gold complex is cashed up from high gold prices and in the mood to expand its in-ground gold resources next to all its gold processing plants...

We are sure that JBY’s new strategic advisor Keith Wood (ex-N.G.M complex chief geologist) would know all about this...

The latest presentation from JBY’s Executive Director Matt Hayes tells the JBY story really well in a ‘speed dating’ style of under 15 minutes.

Watch it here to find out the answers to all these burning questions about JBY:

- How similar is JBY’s asset to the giant Barrick / Newmont mine next door?

- Just how cheap is gold production in the USA?

- What kind of grades can be profitably mined in the US?... Western Australian gold investors might be shocked...

- Can Uber Eats be ordered to site? (is it close to civilisation?)

- Plus a crude joke that we can’t repeat here... you’ll have to watch.

We also saw the following video posted by Livewire where Seneca Financial Solutions analyst Ben Richards calls JBY their top gold pick, check that segment out here.

He seemed a bit sheepish talking about a tiny misunderstood stock like JBY, given fund managers usually invest in bigger companies, but we are glad he did.

(Source)

It’s always good to see one of our Investments get picked up by the funds management community.

Over the next 3-4 months, JBY will have catalysts it can deliver in a rising gold price environment that could trigger a re-rate to an index worthy market cap:

- 4,000m RC drill program - JBY should be starting drilling any day now to try and expand its existing shallow gold resource.

- Metwork testing on the deeper Skarn resource - we are hoping to see recoveries that somewhat resemble the ones from N.G.M’s Fortitude pit which has mined ~2.3M ounces of gold from similar geology.

- Re-assaying old cores - JBY recently submitted old diamond cores to be assayed. These were previously untested and should tell us whether or not there is more gold in between the shallow and deeper parts of JBY’s resource.

For the rest of this note on JBY, we will cover:

- Specific detail of what we are looking for in JBYs upcoming drill results

- JBY’s resource in detail and how we think the company can grow it

- JBY’s exploration upside and what’s next

- Plus the near terms risks we have identified and accepted with our investment in JBY

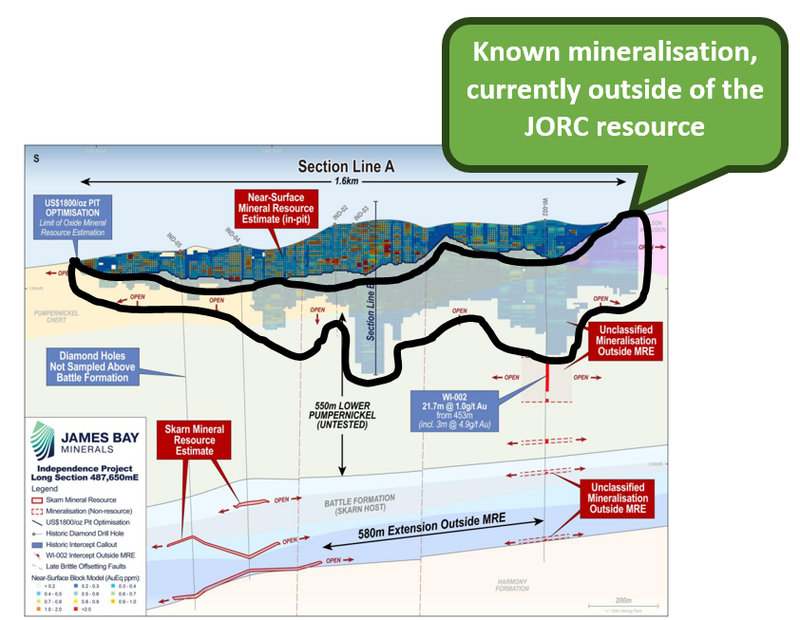

JBY’s 1.4M oz. resource is split into two types - do they join?

JBY’s current JORC resource is divided in two and naturally, has similarities to the N.G.M complex next door (makes sense given they are pretty much the same rocks):

JBY has a ~400k ounce shallow resource with similar grades to N.G.M

The shallow component of JBY’s resource has an average grade of 0.32-0.4g/t.

N.G.M is producing at ~0.32g/t gold grades with all in costs of ~US$670 per ounce - so extremely profitable right now

JBY has a ~1M ounce deeper resource with similar grades to N.G.M

JBY’s deeper skarn hosted resource has an average grade of 6.67g/t.

N.G.M has historically produced ~2.4M ounces of gold from the same host rocks at grades of ~6.68g/t...

(Source)

So N.G.M has shown us that both those deposits can be mined profitably - the deeper high grade and the shallow, relatively lower grade, resources.

JBY is now looking to grow both its shallow and deeper resources.

Drilling should begin any day now and results should come out over the next few months.

At the same time assays are pending from two old holes that could reveal if the two resources connect in the middle...

Here is a visual representation of what JBY is going for with it’s current round of drilling

(We cover the exploration upside in detail later in today’s note)

We are Invested in JBY because we think it can expand its current resource significantly to get scale, then progress into development or get taken over by a bigger gold producer. .

With drilling about to begin and the gold price going almost exponential we think the recent appointment of Keith Wood as a “Strategic Advisor” comes at an excellent time...

Keith was the former Chief Growth Geologist for N.G.M next door and must have played a big role in the development of N.G.M’s growth strategy which is still in practice today...

(Source)

We assume he would know the area extremely well, and will probably have a pretty good grip on what to do with JBY’s project...

Especially considering JBY’s project isn't completely greenfields, and would have been relatively well known to the Barrick/Newmont guys (and Keith’s team)...

We hope that Keith can work in everything he knows about the area in JBY’s upcoming drill programs...

Not to mention bring with him all of the phone numbers and relationships with key management at Newmont and Barrick...

How can JBY grow its ~1.4M ounce gold JORC resource?

With the upcoming drill program the main thing we are watching out for is JBY upgrading its shallow resource.

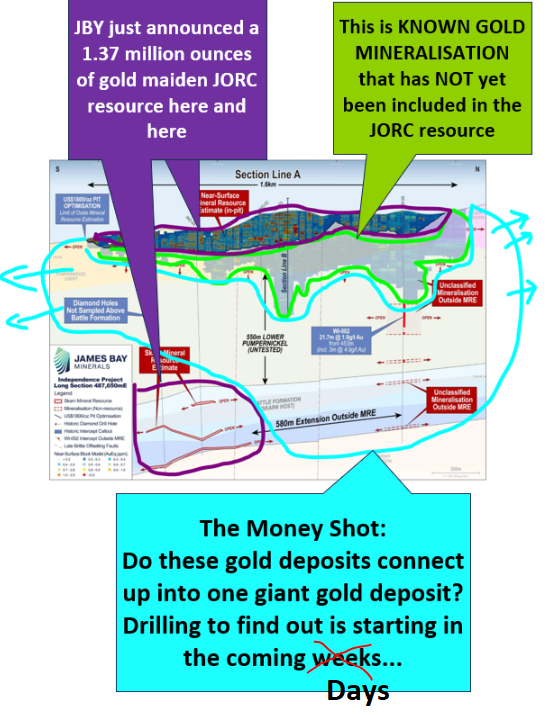

We already know that there is known gold mineralisation that sits outside of the current resource model.

With some drilling, JBY can bring some of this into the current resource estimate for that shallow portion of its project:

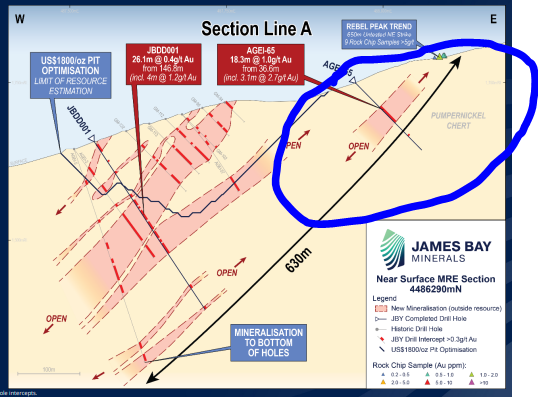

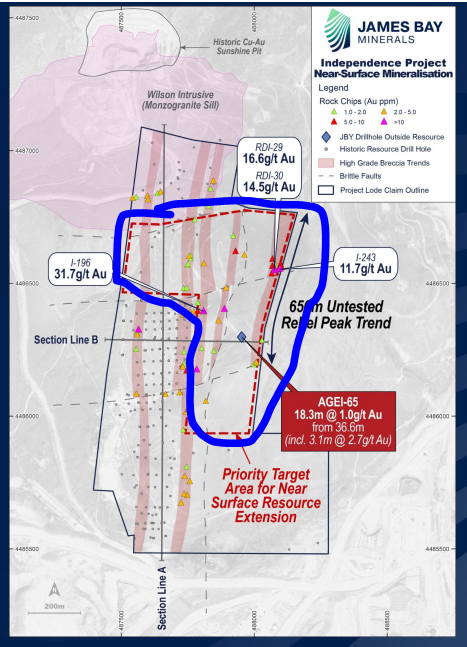

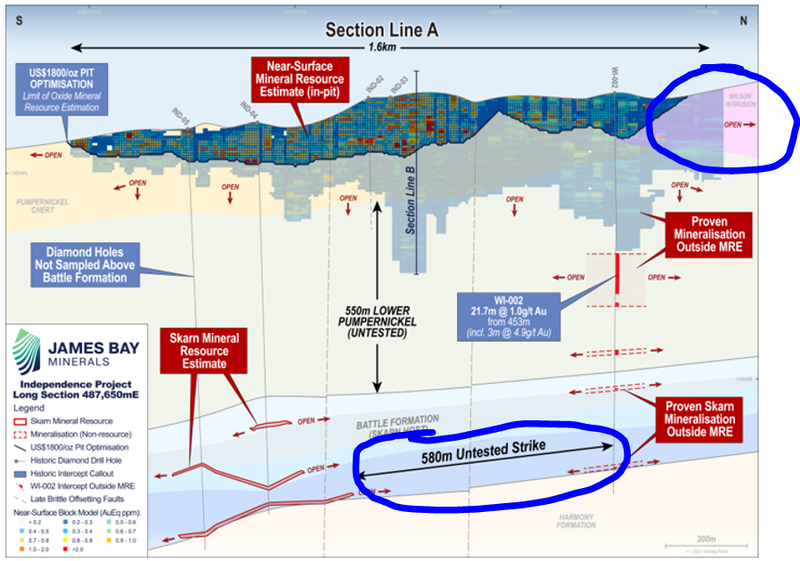

We think the bigger blue sky upside will be from the untested targets to the north/east of JBY’s current resource area.

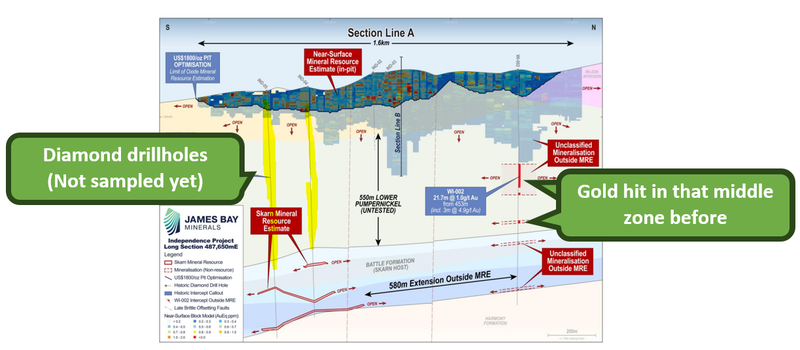

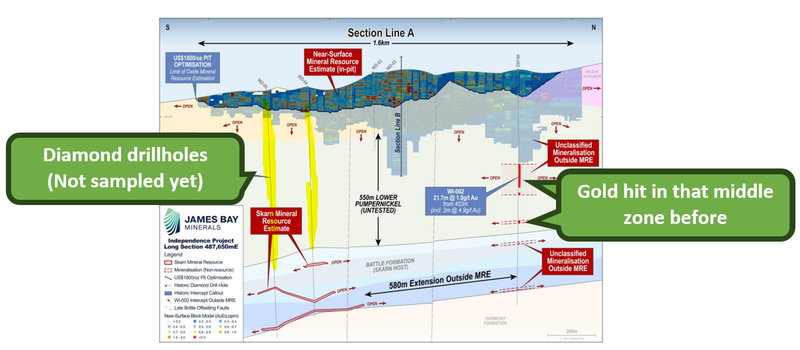

Here JBY will be testing a ~1.3km strike zone, Here is how it looks on a cross section:

And here is how it looks on a 2D map:

Beyond the upcoming drill program there are two other ways that JBY can increase its resource.

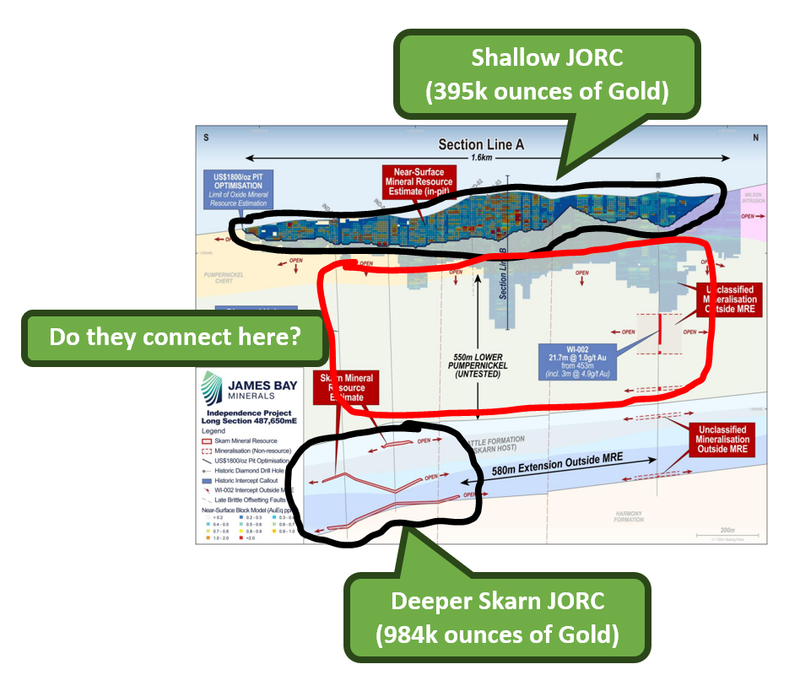

The second idea is a bit more conceptual, but there seems to be some precedent for it.

The idea is that the shallow near surface gold extends at depth and connects to the higher grade, deeper skarn section:

We’ve already seen JBY demonstrate this with one drillhole, and there are existing diamond holes that haven’t been sampled in that middle section that could prove this theory even further:

JBY recently confirmed that these holes had been resubmitted to the assay labs to be tested for gold so we should get some news on this front soon.

The final and most obvious way JBY can grow it’s resource is by drilling extensional holes to both it’s shallow and deeper resources.

(which is partially what the next round of drilling will be doing)

A big part of our JBY Big Bet is based on JBY being able to grow its resource and re-rate in valuation - as follows:

Our JBY Big Bet:

“JBY re-rates to a +$300M market cap by expanding its large US gold resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our JBY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for JBY?

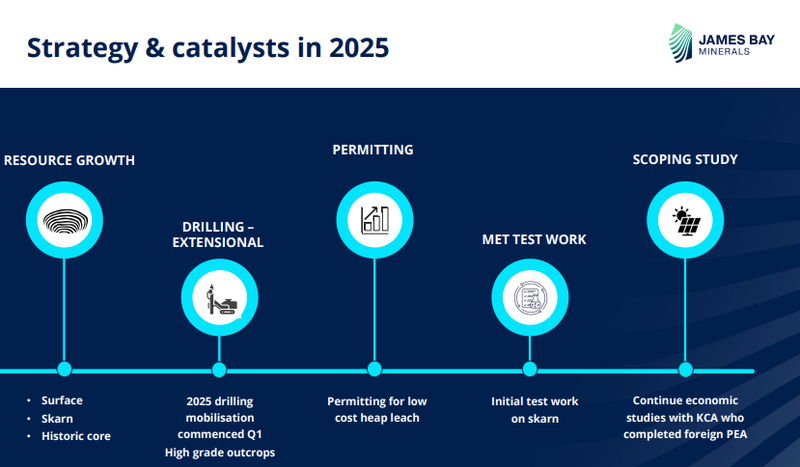

The following slide from JBY’s most recent investor presentation gave a good overview of what to expect next from JBY:

4,000m RC drill program 🔄

JBY should be starting drilling any day now to try and expand its existing shallow gold resource.

JBY’s plan is to drill a 4,000m program testing ~1.3km of strike that could extend the resource from surface to the north/east:

Metwork testing on the deeper Skarn resource 🔄

JBY has also flagged it would look to do some metwork testing on it’s deeper skarn resource.

From that program we are hoping to see recoveries that somewhat resemble the ones from N.G.M’s Fortitude pit which has mined ~2.3M ounces of gold from similar geology.

If the metwork is similar, the look through for us will be that JBY’s resource might also be feasible to mine.

Re-assaying old cores 🔄

JBY has flagged potential assay results from old deep diamond drillcores that were never tested for gold.

These should give us some more information on whether or not there is gold in between JBY’s shallow and deep resources:

What are the risks?

In the short term the key risk for our JBY Investment Thesis is exploration risk.

JBY still has assays pending from its last drill program AND plans to start drilling again later this quarter.

There is no guarantee that any of that drilling delivers any economically viable drill results.

If that were to happen we would expect the market to react negatively and move the JBY share price lower.

Exploration risk

There is no guarantee that JBY can increase its existing resource estimate through exploration drilling. There is always a chance that drill programs fail to find any economic mineralisation that may not add to the project’s overall resource estimate.

Source: “What could go wrong” - JBY Investment Memo 25 November 2024

To see other risks to our Investment Thesis, check out our JBY Investment Memo here.

Our JBY Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our JBY Investment Memo where you will find:

- What does JBY do?

- The macro theme for JBY

- Our JBY Big Bet

- What we want to see JBY achieve

- Why we are Invested in JBY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.