Big two months coming up - SS1 starts drilling in next few weeks…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,810,000 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

A timeline on drilling is now clear.

Our Next Investors 2024 Small Cap Pick of the year Sun Silver (ASX:SS1) will be drilling its giant Nevada silver project in just a few weeks.

So the next 2 to 3 months should be filled with SS1 drilling announcements and assay results.

Drilling time is always the most interesting for early stage resource companies and their investors - it’s certainly our favourite time.

We are hoping that SS1 will be able to add MORE silver to its already giant 292Moz silver equivalent JORC inferred resource at its project in Nevada, USA.

(We are now in the fourth consecutive week of the silver price trading above its decade long highs)

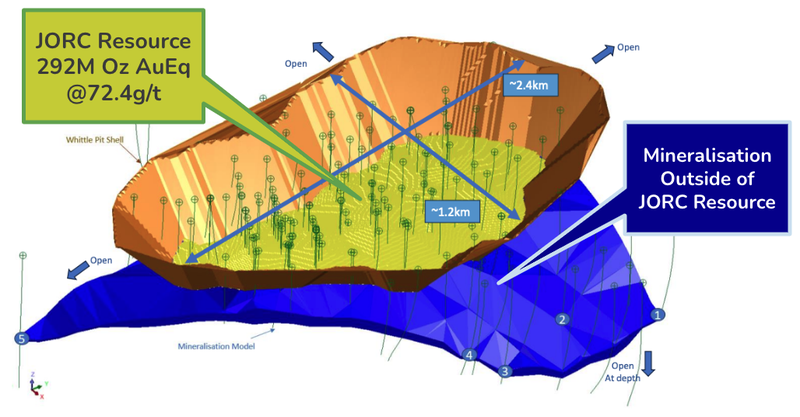

Here is what SS1’s resource currently looks like.

In yellow sits the 292M ounce JORC inferred silver resource, and in blue is the mineralisation outside of the JORC resource:

From the first few rounds of drilling we are hoping to see SS1 do two things:

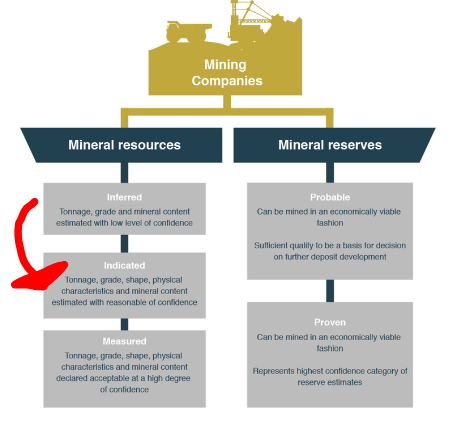

1. Upgrade the size of its JORC resource,

AND

2. Upgrade its resource classification - at the moment, SS1’s resource is mostly inferred, we are hoping to see SS1 move some of the resource into the higher confidence indicated category).

SS1 hasn’t explicitly stated where it will be drilling yet but the company says it has done a fair bit of work in the past few weeks which gives us a good guess of where the drilling could potentially be focused...

Where we want to see SS1 drill:

First of all, mineralisation across SS1’s project is open to the north, south, west and at depth to the east.

This basically means that based on the drilling that has already been done in the past, it appears the silver mineralisation keeps going in all the above mentioned directions, but it hasn’t yet been drilled to confirm what is actually there.

There could be some surprises to come - amazing or disappointing, depending on where SS1 decides to drill and what the results yield.

SS1 could target any one of the above-mentioned areas to expand its resource.

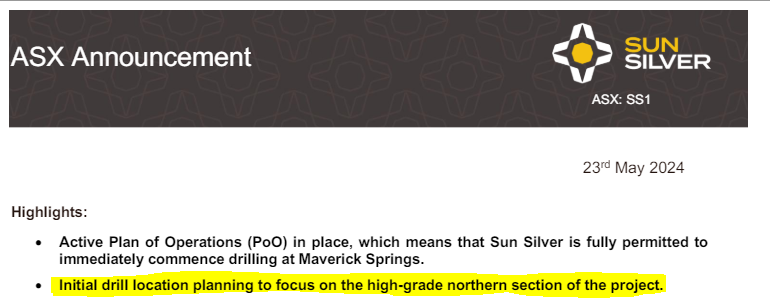

SS1 in an announcement on the 23rd of May did mention that initial drilling would focus on the “high-grade northern section of its project”:

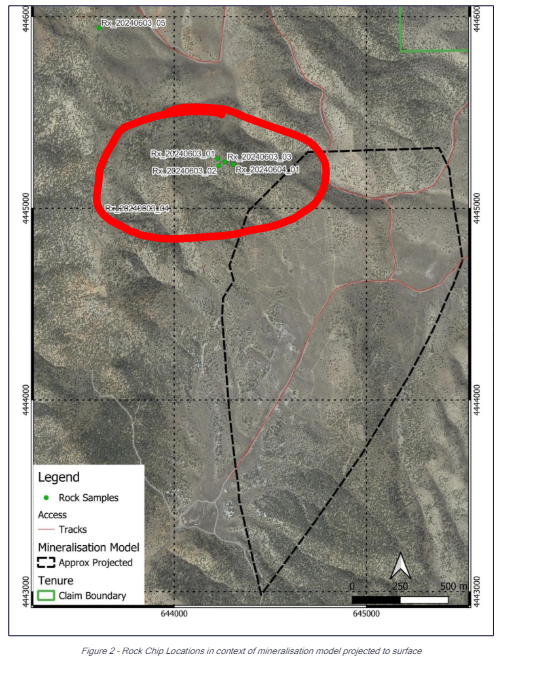

Just a few days ago SS1 also put out an announcement highlighting a target area in that northern section of the project where the geo’s identified ~1.2km of “anomalous outcrop”.

We also noticed in the geo reports in SS1’s which mention the gold-silver mineralisation starts to “flatten out” to the north.

“Flattening out” could be good for SS1 because it might mean shallower mineralisation that is lower cost and easier to mine...

So by drilling to the north, SS1 could hit closer to the surface (shallower) extensions to its existing silver resource - shallow is good because it's easier to mine:

Here is an animation we made overlaying the northern part of SS1’s project:

We also saw SS1 start a review of the old drillcores from the ~60,000m of previous drilling done on the project.

Again in that announcement the focus was on “the high-grade northern section” of SS1’s project.

Usually, we wouldn't place much emphasis on re-logging announcements, but in SS1’s case, we think the work is pretty important.

SS1’s project hasn't been drilled since 2008, and the silver price has been in a bear market ever since, so a lot of the work done on the project hasn't been examined in greater depth and with the latest exploration tools.

At a very high level, the logging work will mean SS1 can update its understanding of the orebody and help plan how best to improve it...

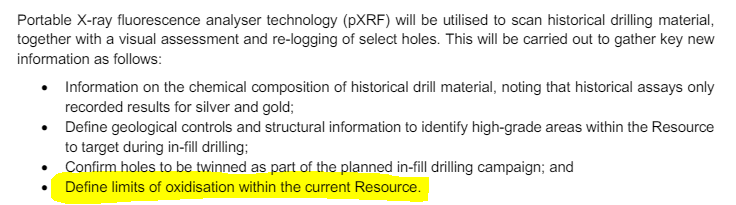

A part of that announcement that we think the market may have missed was the work SS1 is doing on “defining the limits of oxidation” for the project.

Alongside the upcoming drilling results, we think the work being done on metallurgy (working out the type of geology the resource sits in) could be a big catalyst for the company.

With projects like SS1’s where there is already a big JORC resource, the key bit of information that corporates & bigger resource focused investment funds will look for it’s metallurgy.

Metallurgy, at a very high level, shows how the silver & gold from SS1’s resource can be extracted and how well understood/cost effective the extraction process could be.

When it comes to metallurgy, simple and boring is what we want to see - processes that have been tried and tested...

We think the metwork is a big catalyst for SS1 because it would be important information for the majors already operating in Nevada...

These operating mines that are already in production have all of the processing infrastructure already built for their projects - processing resources with specific types of geology.

IF SS1 can show that its resource sits inside geology that is easy to process and shares similarities with some of the mines already in operation then it starts to stack up as a potential target for the bigger companies in the area....

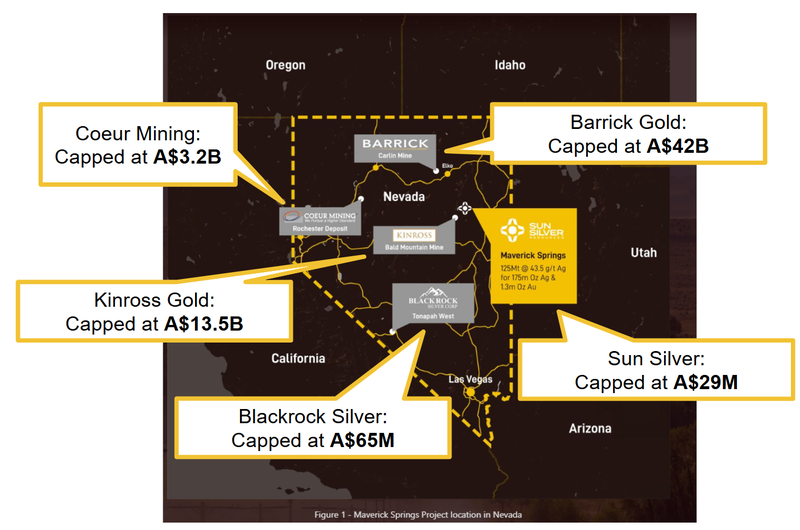

SS1’s project being in Nevada helps make its project all that more interesting to majors...

Nevada is home to the largest primary silver mine in the US and there are >50 different operating silver/gold mines in the same region as SS1’s project:

Companies like A$42BN Barrick and A$13.5BN Kinross are operating projects not that far away from SS1:

SS1 also going for downstream value add opportunities

In addition to drilling out its giant silver resource SS1 is developing a “downstream value add” for silver paste.

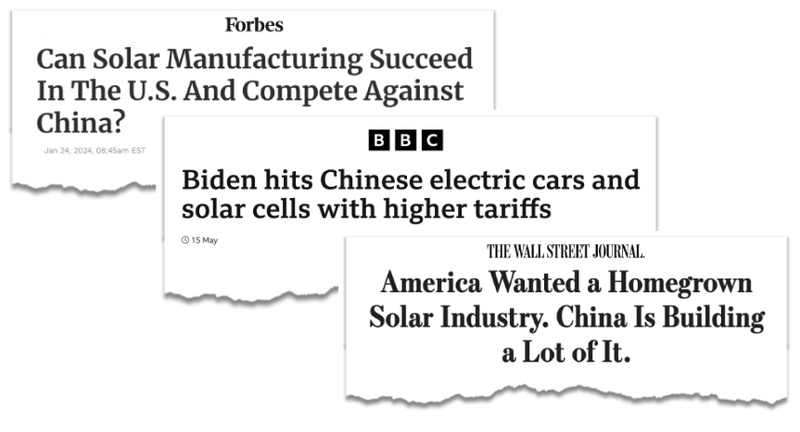

The US and China are in a battle for control over critical minerals.

China currently supplies 90% of the world’s solar panels.

The USA has set a target for solar to reach 30% of U.S. electricity generation by 2030.

In order for the US to meet its sustainability goals under the net zero plans it will need A LOT more solar panels.

The US doesn’t want to be reliant on China for this critical piece of infrastructure, and has recently added a 50% tariff on Chinese solar panels.

The US needs to develop a domestic solar panel supply chain.

And fast.

One of the key components of that supply chain is “silver paste”.

As a downstream value add to the project, SS1 is developing its capabilities to produce silver paste for the US domestic market.

We think this value added product will differentiate SS1 in the market and help the company integrate with the US solar manufacturing industry more closely over the long-term.

The US government has recently slapped a 50% tariff on Chinese solar panels.

Despite the USA’s own target of 30% solar energy as part of its national energy mix by 2030.

We think that SS1’s downstream value added product will become a big part of the story as it moves towards feasibility studies (after drilling out its JORC resource).

SS1 has already appointed a US group Holland & Knight to seek out grant funding from various US government departments to support these endeavours.

If successful, it will provide non-dilutive funding to advance its projects.

(good for existing shareholders, like us).

Ultimately, we want to see SS1 build out its JORC resource and move into development studies.

This brings us to our big bet...

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

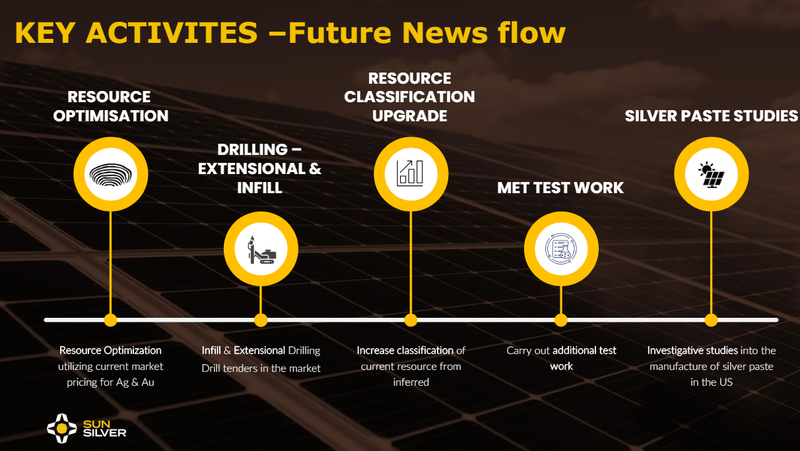

What’s next for SS1?

Drilling Program

SS1 is currently getting set up for its maiden drill program. The next key piece of news that we want to see is some drill targets to follow.

✅ Permitting for drill programme

✅ Drilling contractor secured (today)

🔄 Finalise drill targets + announce a drilling plan

- 🔄 Review historical drill logs and interpret data

- 🔄 Undertake geophysical surveys

🔲 Drilling commenced

🔲 Drilling results

Resource upgrade/update

Off the back of its drill program we want to see SS1:

- Upgrade the size of its JORC resource with exploration drilling, AND

- Upgrade its resource classification with infill drilling - SS1’s resource is mostly inferred, we are hoping to see SS1 move some of the resource into the higher confidence indicated category).

🎓 Learn more about JORC resources here: What is a JORC resource? How does a company define a resource?

Metallurgical test work updates

We talked about this in today’s note but we think the results from metwork testing will also be important for SS1.

SS1 already has a giant existing JORC resource, the met test work will give us a good idea of how simple/cost effective it will be to process out the silver and gold from the resource.

We think this is a catalyst that the technical part of the market (and the major miners already in Nevada) will be watching for...

Silver Paste Program

At the same time, SS1 will be working on its downstream processing solutions for silver paste, which will provide a potential offtake solution once the company moves through to the feasibility and development stage of the project.

🔲 Silver paste studies

🔲 Silver paste grant funding

If all goes well, we want to see SS1 move through to feasibility studies with strong project economics.

🔲 Commence feasibility studies

Reminder: Why we Invested in SS1...

- Second largest silver resource on the ASX - $25M capped SS1 already has a ~292M ounce silver equivalent JORC resource (which is the second largest on the ASX). The most comparable peer is $294M capped Silver Mines with a ~400M silver equivalent resource. Currently Silver Mines market cap is more than 10 times SS1, with a resource only ~ 25% bigger. Based on this, we think there is upside in SS1’s market cap.

- Potential to increase an already large JORC resource - Only ~20% of SS1’s project has been explored to date. With its first round of drilling, SS1 will be looking for extensions to its current JORC resource and potential nearby targets.

- Silver price is hitting decade highs - Silver demand is fast outstripping supply. The silver price is re-testing an 11 year high at the time of writing. We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

- Project acquired and IPO priced while silver was “unloved” - SS1 acquired its 292M ounce silver equivalent JORC resource project while silver was boring and trading sideways. The ~$25M IPO market cap was set before silver's current price run.

- SS1’s tight, clean capital structure supports share price re-rates - ~55M of the ~125M shares on issue are escrowed for at least ~12 months. The top 20 hold ~65%. Most importantly there are no options on issue, meaning there is no extra “weight” being carried when the share price is responding to news. Current shareholders can NOT use a strategy to sell head stock while retaining upside via an option.

- The US solar industry will need a lot more silver - Silver is a key material used in solar panels. Silver demand from solar energy is forecast to “go exponential”. In the next six years, the US government is aiming for more than 6x current solar capacity. And to satisfy US solar energy targets for 2050, the world would need to dig up nearly EVERY single known ounce of silver EVER found in current reserves (98%).

- US push to “onshore” solar industry away from China- SS1 has a giant supply of silver for solar panels on US soil (Nevada). The US has just applied a 50% tariff to solar cells that are imported from China into the US, up from 25% previously. We expect this to provide additional economic incentives and support to domestic US solar manufacturers while also creating further demand for domestically sourced silver and silver paste both of which SS1 is pursuing production of.

- SS1 is based in a mining county in the top silver producing state in the US - the area of Nevada that SS1 is working in is called Elko County. There are major gold and silver mines scattered throughout this area of Nevada and Elko County is very familiar with the mining industry. $45BN Barrick and $14BN Kinross both own projects in the region.

- Downstream value add: “Silver paste” production (for solar) could improve economics - silver paste is made from silver and improves the efficiency of solar panels. Currently most of the world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could improve the overall economics of its project.

- US Government to support domestic solar industry and help bring strategic projects online - SS1’s project may be seen as having strategic value to US onshoring of solar panel manufacturing. We think SS1 could benefit from US government tax incentives included in the Inflation Reduction Act, tariffs on Chinese solar panels and potential government grants for strategic projects and manufacturing initiatives.

- JORC resource includes ~1.37M ounces of gold - the gold price is also at record highs. Included inside SS1’s 292m ounce silver equivalent JORC resource is a ~1.37m ounce gold resource. We think this gold has appeal as an inflation hedge/precious metal, which could pair nicely with the rapidly growing industrial use of silver from solar panels.

What could go wrong?

The three risks we are most focussed on at the moment are “Exploration risk” “Commodity price risk” and “Market risk”.

Namely, drill results could disappoint the market, the price of silver could fall, and with major indices around the world around all time highs - there could be a pull back that impacts the market more broadly that filters through to SS1’s share price:

Exploration risk

There is no guarantee that SS1’s upcoming drill programs in Nevada are successful and SS1 may fail to materially increase their JORC resource.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 sentiment and share price.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking SS1’s share price with it. Alternatively, there is always the risk of further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Our SS1 Investment Memo

For a full rundown of our investment thesis, read our SS1 Investment Memo, where we share:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.