Silver, Gold and US Critical Metals Macro Themes

Published 09-AUG-2025 16:16 P.M.

|

14 minute read

Commentary: Market still looking good... What’s happening with macro themes silver, gold and US critical metals...

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

We are now in week 6 of the small cap market being “back”...

(we called it in June, finally got one right...hopefully it keeps going?)

We always said the small cap market needed a strong macro theme to bring it back to life.

To bring the sidelined investors back from years of hibernation.

What we did NOT get right was our prediction that gold would be what got things humming again in the small end.

Gold’s 25% price surge from January to April this year got the bigger gold producers going and a handful of small cap investors starting to wake up.

But it has not properly flowed through to small gold stocks... yet.

(we think this will happen when the gold price breaks out of the sideways trading pattern its been in since April)

Then the US critical metals theme came steaming in over the last 2 months as the USA urgently prioritises rebuilding its domestic critical metals supply and advanced manufacturing industries.

We also think silver is just about to swoop in as one of the big themes of the next 12 months.

Three strong macro themes firing at the same time?

Wouldn’t that be great for the small cap sector...

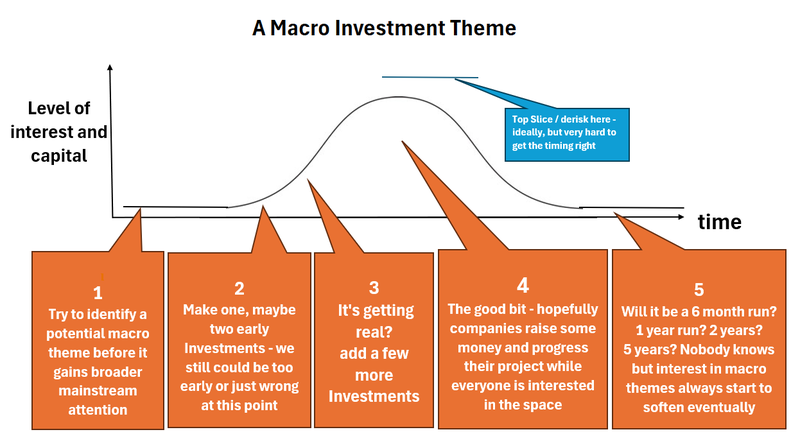

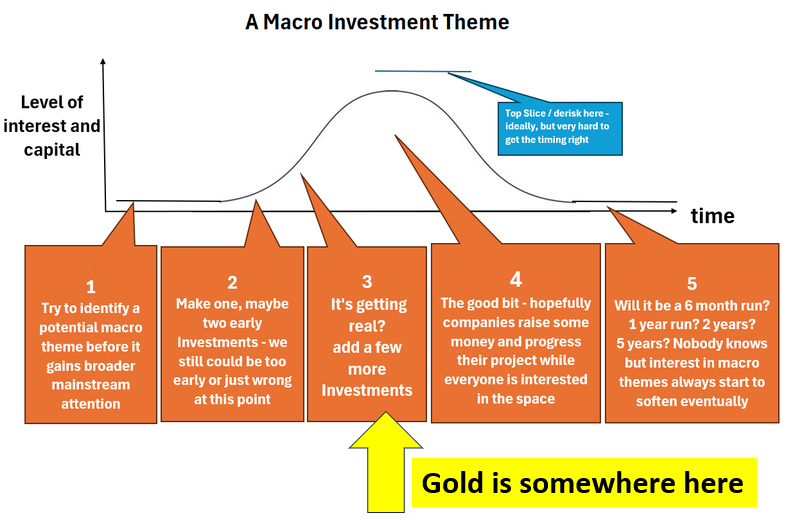

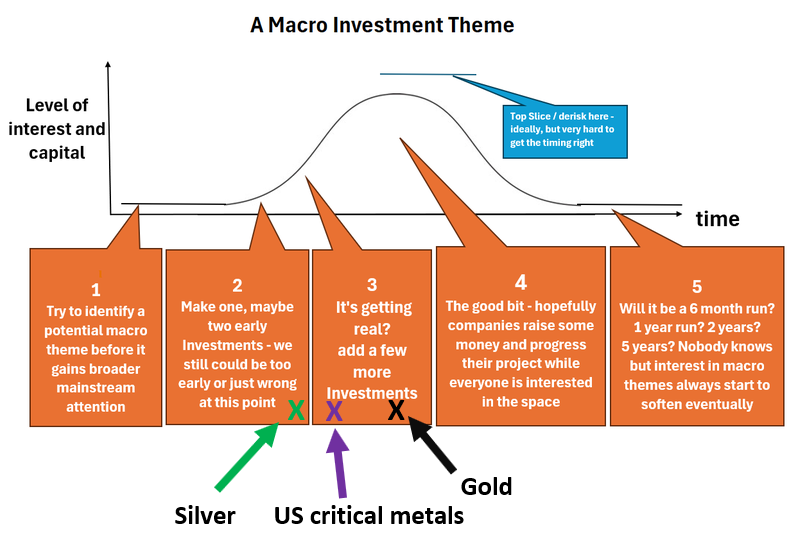

Last Saturday we introduced our idea of how macro thematics evolve into “super thematics” in 5 stages, and our strategy for when to add more new Investments in a macro theme as it evolves:

(read our note where we explain it in more detail here)

This model applies to any macro theme.

The problem is that most macro themes spend 95% of the time stuck in stage 1 - where the market simply doesn't care and stocks struggle to attract attention and capital...

So where are each of silver, gold and US critical metals currently on our model?

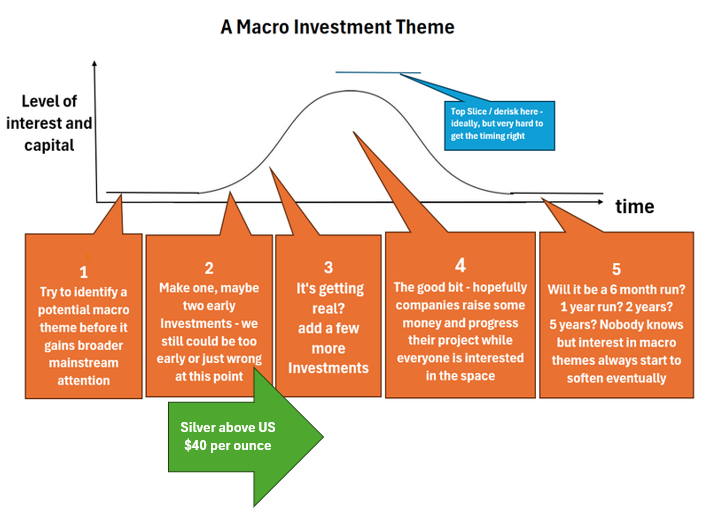

Silver: About to enter stage 3?

We think silver is on the verge of a breakout above US$40 per ounce.

(it finished the week at US$38.4)

And if we see a clean break, we think silver as a macro thematic will go from stage 2 into stage 3:

We think the silver space is right near the end of stage 2 - about to enter stage 3 - which is where we want to start adding new silver names to our Portfolio.

(just before it accelerates into stages 3 and 4)

There are very few silver stocks on the ASX.

(compared to how many gold stocks there are)

We did a quick scan earlier in the week and could only find ~14 silver stocks with market caps between $10M and $250M.

If we had done the same for gold there would be hundreds...

That tells us that IF the silver price DOES do what we think it might and go on a generational price run, there wont be many companies available for investors to get exposure to the running silver price.

And concentration of capital into a few names could mean valuations run beyond where the market could expect.

This week we added West Coast Silver (ASX:WCE) to our Portfolio.

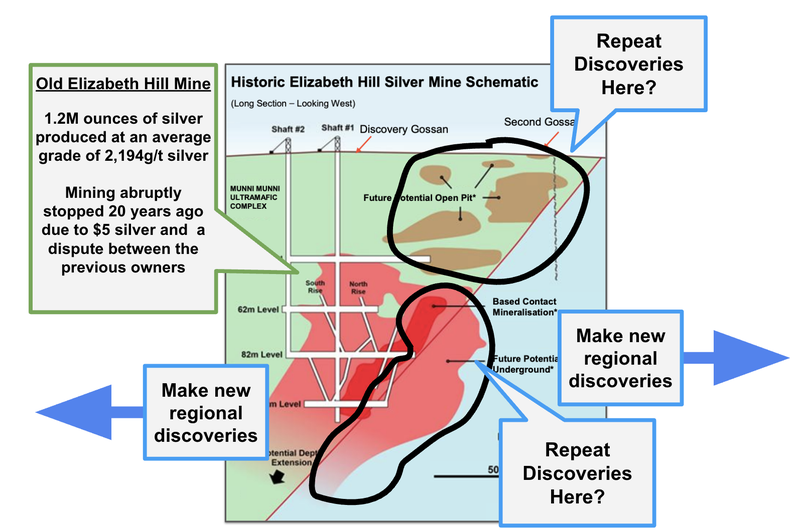

WCE owns 70% of the Elizabeth Hill Mine in WA.

When it was in production, WCE’s project was one of the highest grade silver producers in Australia.

Mining abruptly ceased in a single day due to a fall out between the project’s JV partners at the time, leaving a potentially untapped resource. (source)

Back then the silver price was just US $5 per ounce - this morning it finished the week at near 14 year highs of US $38.40.

WCE’s project once produced 1.2M ounces of silver from just 16,830 tonnes of ore.

That means average grades during production were ~2,194g/t silver...

(and the high grade nature of the deposit made it a low cost mining and processing operation - we like low cost and fast mining when we think a commodity is about to run)

For some context, most operations these days are happy if grades are north of 50g/t...

A big part of the reason we are Invested in WCE is because we think that the company could make new discoveries similar to what was mined at Elizabeth Hill in the past - both next to its existing mine infrastructure AND regionally:

Read our full WCE initiation note, where you can find:

- 9 key reasons why we are Invested in WCE

- Why we think silver is about to go on a generational price run

- Our deep dive on WCE’s project

And of course our WCE Investment Memo which outlines:

- What does WCE do?

- The macro theme for WCE

- Our WCE Big Bet

- What we want to see WCE achieve

- Why we are Invested in WCE

- The key risks to our Investment Thesis

- Our Investment Plan

We also hold the following as exposure to silver:

- Sun Silver (ASX:SS1) - the biggest pre-production silver project on the ASX and in the USA with a 480M ounce silver equivalent JORC resource. SS1 drilling right now to grow its resource.

- Mithril Silver and Gold (ASX:MTH) - 373Koz gold and 11Moz silver JORC resource in Mexico’s Sierra Madre region (home of Mexican silver). MTH is currently drilling to double that resource.

- Titan Minerals (ASX:TTM) - we mainly Invested in TTM as a gold play with its 3.1M ounce gold resource, but it also has a 22M ounce silver JORC resource in Southern Ecuador. TTM is currently drilling to upgrade its resource.

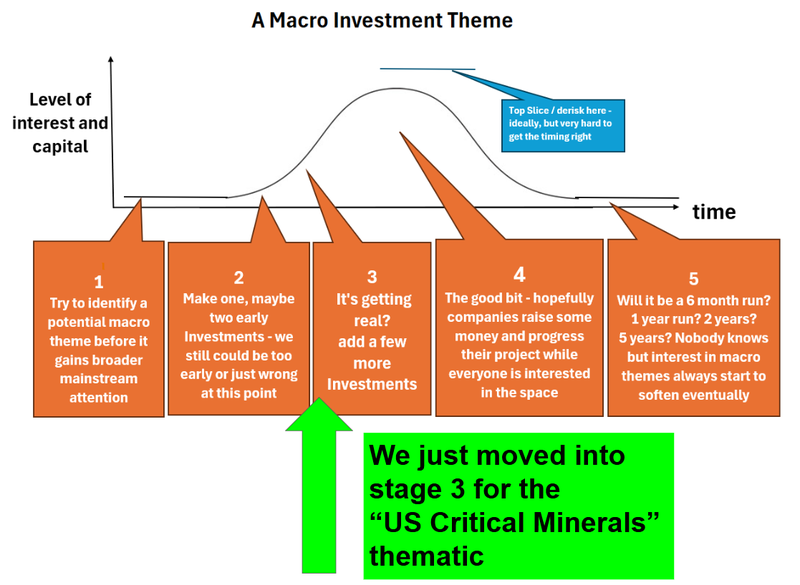

US critical metals just moved into stage 3. More Trump mentions this week... quickly heading toward stage 4?

US critical minerals is currently making the most rapid move through the stages we mentioned earlier.

Helped along by the number of mentions, urgency and funding from major US companies and the US government in the last few weeks.

It feels like Stage 1 was in 2023/2024.

Then Stage 2 earlier this year.

And just inside the last two months we are moving through stage 3 approaching stage 4 pretty quickly...

Inside the last 45 days we have seen rapidly evolve and gain mainstream attention:

- JUNE 18th: NEWS: Battery makers say antimony ban is starting to bite and antimony prices hit all time highs at US$60,400/tonne (Source: Reuters)

- JUNE 20th: Tungsten prices close at record highs (Source)

- JULY 4th: President Trump’s Big Beautiful Bill passes, allocating US$7.5BN to "Enhancement of Department of Defense Resources for Munitions and Defense Supply Chain Resiliency", US$1BN for the "identification, leasing, development, production, processing, transportation, transmission, refining, and generation" of critical minerals projects and US$1BN for the Defense Production Act (Source)

- JULY 10th: The Pentagon makes a direct US$400M investment into US critical minerals producer MP Materials. (Source)

- JULY 15th: Tech giant Apple cuts a US$500M offtake deal with MP Materials. (Source)

- JULY 16th: US Department Of Defence officials say that the Pentagon will keep investing in US critical minerals projects. (Source)

- JULY 16th: US government guarantees a rare earth's price floor for MP Materials. (Source)

- AUGUST 1st: Trump administration says “we want Operation Warp Speed levels of urgency to develop US critical metals” (Source)

- AUGUST 1st: US government officials urge more tech companies to invest in rare earths space directly, either through seed investing or by making buyouts. (Source)

- BREAKING NEWS this week - Apple increased its commitment to US manufactured products to US$600M (increase by another US$100M) and specifically mentioned US made rare earth magnets in its press conference.

That Apple news from this week added another ~$2-3BN in market cap to MP Materials market cap ...

Here is a video of Apple CEO Tim Cook and US president Donald Trump lovingly talking about the US based rare earths miner MP Materials:

(Watch it here - Source)

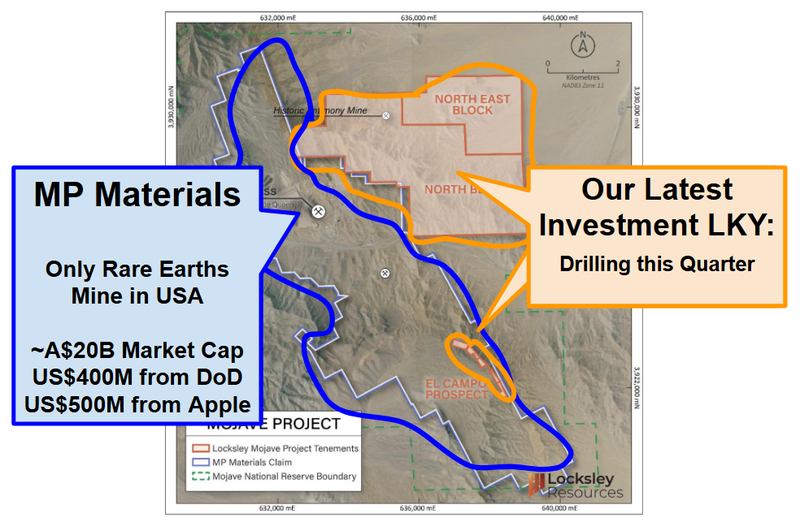

Our Investment Locksley Resources (ASX:LKY) sits right next door to MP materials

LKY had been working on getting drill permits for 18 months...

Earlier this year (post Trump coming into office) LKY got its drill permits.

LKY lodged another application to upsize its drill program and expects to be drilling in September.

MP Materials was up again overnight.

Daily 5-8% moves upwards for a company with a market cap of ~$20BN are significant...

There is suddenly a LOT of attention and capital flowing towards MP materials...

A rising share price and big US attention on MP Materials so close to LKY’s drilling program can only be good for LKY.

If the next door neighbour is capped at $20BN - then the risk/reward on offer for a company drilling next door becomes a lot more attractive.

We covered LKY in a note on the day of that Apple news here: LKY: Apple’s CEO Tim Cook’s X post sends MP Materials’ share price up. Neighbour LKY appoints Tribeca Capital for US critical metals growth strategy

Rare earths and antimony are first off the rank to get the attention of US investors.

We wonder what could be next? (uranium? lithium? Other metals with non obvious tangential uses in AI, data centres or robotics?)

Our two other US critical metals in rare earths and antimony exposures are:

- Resolution Minerals (ASX:RML) - gold-antimony-tungsten and silver in Idaho - next door to another major US critical metals company - Perpetua Resources. RML actually announced that it had received an A$225M unsolicited non-binding indicative offer for its project earlier this week. That sort of offer pre-drilling on an exploration asset is another sign for us that the thematic is starting to heat up...

- Sun Silver (ASX:SS1) - as mentioned earlier, its project is mostly silver BUT after re-assaying the old drillcore on the project SS1 has been finding that most of the holes also have antimony too - SS1 has exposure to both the silver macro theme AND the US critical metals theme and is currently our biggest position.

(other US critical metals investments we have are GUE and GTR in uranium, PFE in lithium - just waiting for themes to move out of stage 2 in our macro theme model...)

Gold producers on the move... gold about to break out of its April to August trading range?

With gold we think we are somewhere in the middle of stage 3.

Capital has well and truly flowed into the bigger producers and the mid caps.

But we haven’t quite seen it flow into the junior explorers just yet - which is why we think it isn’t quite at stage 4 just yet.

Here is where we think the gold macro theme is sitting:

Gold delivered a great run to new all time highs at the start of this year, but has been moving sideways for the last 4 months (at all time highs, strong consolidation which is good):

If gold breaks out of this range and starts marching upwards again, we think this will firm up gold's position in stage 3 and potentially into stage 4 of our macro theme model, depending on how sharp the price rise is.

(keeping in mind that commodity prices can go up OR down, so gold continuing a leg up is no guarantee)

And finally smaller gold developers and explorers to start getting some of that attention and capital.

A fair few of the big gold producers have been reporting quarterly earnings over the last few weeks.

And the numbers have mostly surprised the market to the upside.

Gold producers printing cash.

(not surprising because gold has basically spent the last 4 months at all time highs, of course gold producers were going to deliver strong quarterly prints)

Newmont is a good example of this.

Newmont produced ~1.5M ounces of gold in Q2-2025 and recorded free cash flow of $US1.7 billion (A$2.58 billion) thanks to the persistent all time high gold prices of the last few months.

Newmont’s share price is up ~15% inside the last month in response to those numbers - and it's now capped at ~A$116BN.

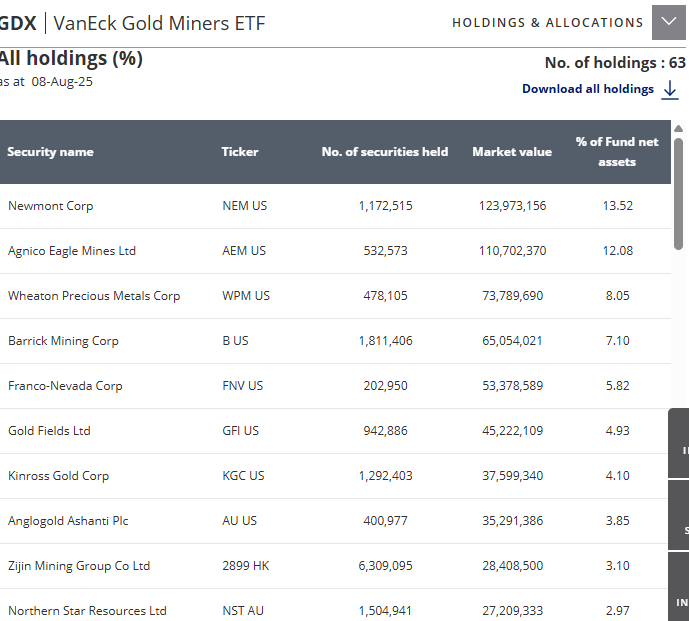

You can get a broader view of the sudden attention and capital flowing into gold producers this week by looking at the Van Eck Gold Miners ETF - ASX: GDX.

GDX is an exchange traded fund made up of large gold producing companies, here are its top 10 holdings of major gold producers:

(source)

And here you can see capital flowing into GDX this week:

We are even seeing seeing fund flows into GDXJ (the fund made up of SMALLER gold producers)

GDXJ is up ~70% for the year and just started another small rally from the mid 60’s to $72.

We think this will mean more cash starts flowing into the smaller producers out there.

Our gold producing Investment Kaiser Reef (ASX:KAU) put out its quarterly last week where we got to see its first gold production numbers after acquiring the producing Henty gold mine in Tasmania.

KAU ended the quarter with $30.7M in cash and gold bullion on hand - before a $500K debt repayment in July and a $2.5M payment of final royalty payment of approximately $2.5 million.

KAU also clarified a bunch of one-off costs paid during the quarter which totalled ~$3.8M.

(Source)

We sort of expected a lot of one-off costs this quarter with the whole Henty acquisition and associated capital raise being done.

For us, the bet with KAU is that we see the gold price stay at today’s levels (or go higher) for at least another few quarters.

After which the Henty acquisition could have basically self funded its own cost of acquisition.

KAU spending more time with the asset will also hopefully lean up operations and deliver more cash to KAU.

We are also looking forward to seeing KAU use this cash for more drilling at its Victorian assets A1 and Maldon.

(And finally ramp the A1 mine’s gold production in Victoria which is why we first Invested in KAU)

A great time to do more exploration drilling with gold at all time highs and looking like it wants to start a new move higher.

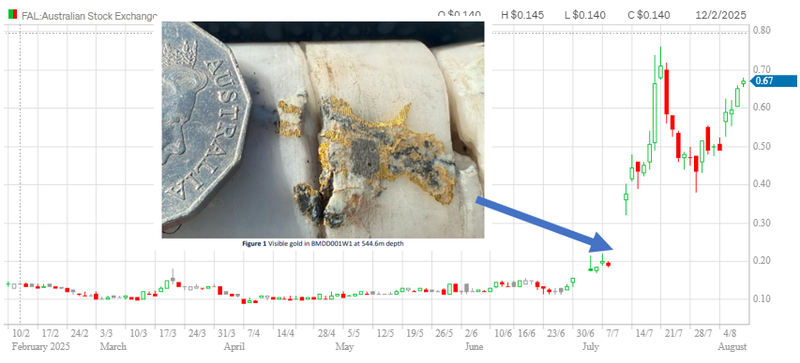

And especially after seeing the move from Victorian explorer Falcon Metals (we don’t hold shares in Falcon Metals), which is up over 600% after hitting visible gold on its ground in Bendigo - not that far from KAU’s ground...

Hopefully KAU can finally get some of that exploration luck while the market is rewarding gold discoveries...

We hold the following in our Portfolio as exposure to gold:

- James Bay Minerals (ASX: JBY) - 1.37M ounce gold JORC resource in Nevada, USA - Next door to Nevada Gold Mines (Joint Venture between Barrick and Newmont)

- Haranga Resources (ASX:HAR) - Holds the centre of the Motherlode region in California which was the centre of the Californian gold rush.

- Mithril Silver and Gold (ASX:MTH) - We mentioned this in the silver section earlier but MTH also has gold in its resource. MTH’s project has a current 373k ounce gold, 11m ounce silver JORC resource estimate.

- Resolution Minerals (ASX:RML) - Mentioning this one again. RML’s project is next door to Perpetua Resources’ 6M ounce gold project. RML is looking to make an analogous discovery...

- Titan Minerals (ASX:TTM) - 3.1m ounce gold, 22m ounce silver JORC resource in Southern Ecuador. TTM is currently drilling to upgrade its resource.

- BPM Minerals (ASX:BPM) - Early stage explorer with ground in the same region as the >8M ounce Tropicana gold deposit owned in a joint venture between majors Regis Resources and AngloGold.

- Lightning Minerals (ASX:L1M) - Early stage explorer with a newly acquired gold-copper project in QLD.

In Summary...

The US critical metals theme definitely has the most momentum right now...

Silver is threatening a breakout and we think it will be next.

And gold has been trading sideways at all time highs, stage 3, if it breaks higher again it could potentially be angling towards a move into stage 4 now that the mega capped gold producers are moving again.

US critical metals, silver and gold are our top themes for the next 12 to 18 months.

But of course, commodity prices (and interest in macro themes) can go up OR down - acting on predictions that may not eventuate is risky.

It’s very possible to be too early... or even just flat out wrong.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.