Uranium? Yep, it's happening

Published 13-JAN-2024 12:00 P.M.

|

14 minute read

Anyone looking at uranium?

Wow - look at that spot price rise overnight.

Biotechs in vogue again?

Looks like it.

Battery metals boom over?

We think it’s just a short pause.

...and valuations are becoming very attractive.

We’ve got all this to talk about in today’s weekend edition, our latest articles, quick takes and a quickly expanding Q1 2024 catalyst list.

There's plenty going on.

And it's only the second week of 2024.

Uranium? Yep, it's happening

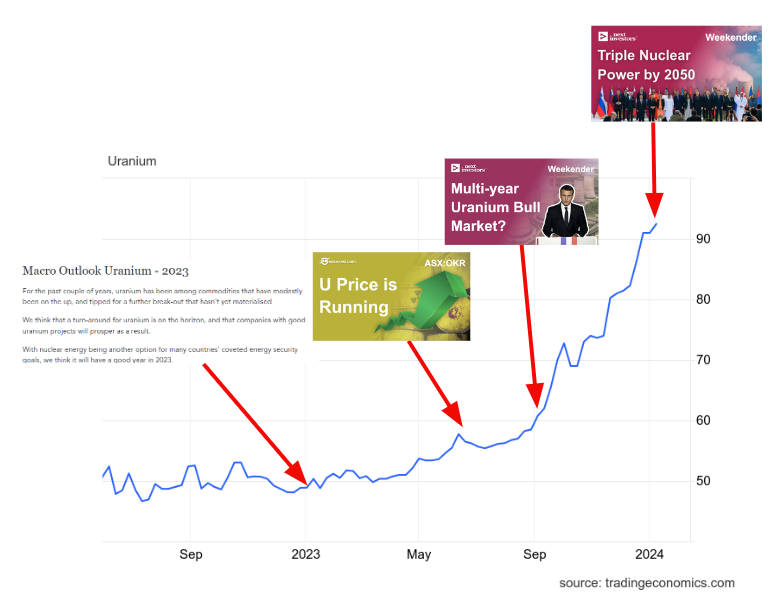

The corner of the market that really has tongues wagging right now is pretty clear - URANIUM.

The U spot price rocketed overnight to hit $104/lb.

The Financial Times called it a “blistering rally”:

With the U spot price now at its highest level in 16 years, this time, we think the uranium bull run is for real.

We said uranium would have a good year in our outlook for the macro theme at the start of 2023.

And that certainly played out - we highlighted that the U price was running in June 2023.

And suggested that we were about to enter a multi year uranium bull market in September 2023.

(during 2023, two of the nine new stocks we added to our portfolio were uranium stocks)

Check out the U spot price:

(Source)

We’ve now got three uranium stocks in our Portfolio (click to see our Investment Memo):

They are:

Global Uranium and Enrichment (ASX: GUE)

previously named Okapi Resources (ASX:OKR)

We’ve spoken about the geopolitical importance of nuclear and secure uranium supply chains in one of our last Weekender editions before the Christmas 2023 break.

In terms of what these companies are up to right now here’s the update:

Haranga Resources (ASX: HAR)

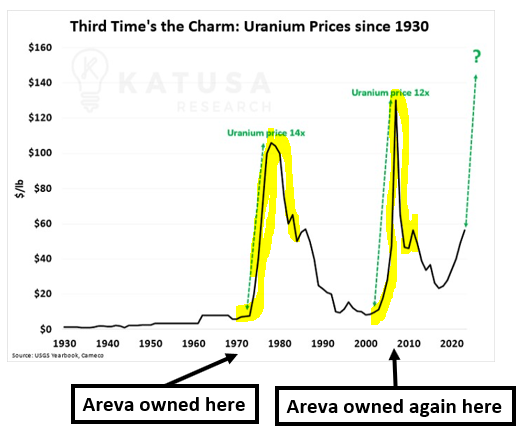

HAR is drilling for uranium right now, seeking to multiply its existing 16.1Mlbs resource in Senegal.

French multinational nuclear power company Areva (now Orano) has owned this project TWICE during the last ~50 years, both times while the uranium price was going parabolic:

Global Uranium and Enrichment (ASX: GUE)

GUE is gearing up to drill its uranium project in Colorado USA

- GUE has a substantial existing JORC resource of ~49.8m lb of uranium. At the end of last year GUE received a Conditional Use Permit (CUP) from the Board of County Commissioners in Fremont County, Colorado, USA.

- The significance of the CUP is that it means GUE is a step closer to drilling out the Tallahassee project in 2024.

- Advances have also been made across its other projects and its enrichment technology - something which we think could take it into the big leagues if the right things click into place

GTi Energy (ASX: GTR)

GTR finished up a 26-hole drill program just before Christmas

- This was at one of its uranium projects in Wyoming, USA. GTR has three different projects that sit close to one another in Wyoming.

- Across the three projects, GTR has a total JORC uranium resource of 7.37m lbs. GTR’s Lo Herma project, which holds 5.71m lbs of uranium.

- GTR’s exploration target for the project is for up to ~10m lbs of uranium so we are hoping that any resource upgrade gets GTR closer to that figure.

Got a uranium company that you think we should look at?

Send us a message - we read all of the responses.

Now, the biotech story.

After a long dormant period - small cap biotech sentiment has improved dramatically over the last 6 months.

Case in point: our best performing stock of 2023 - Arovella Therapeutics (ASX: ALA).

The chart over a two year period looks very strong - and it appears the buying continues:

ALA has now re-rated ~685% from our second Investment at 2c - as the company continues to kick goals while biotech tailwinds improve.

ALA has plenty of catalysts to come - find out what they are in our latest ALA note.

Speaking of biotechs with catalysts, one of our other biotech Investments, Neurotech International (ASX: NTI) is ahead of schedule in delivering not one, but two big catalysts this quarter.

NTI is up roughly 150% from a late-June low.

NTI’s first catalyst of three is already tucked away with positive results, these are the next two catalysts we’re looking forward to from NTI:

NTI Catalyst #1: 🔄 Phase I/II Rett Syndrome clinical trial results

A trial on another child neuropsychiatric disorder called Rett Syndrome - Neuren Pharmaceuticals re-rated ~1300% on commercialisation of its treatment for this disorder.

We think NTI could be safer than Neuren’s treatment and if it works better or similar, hopefully, re-rate accordingly. NEU is currently capped at $3BN.

NTI Catalyst #2:🔄 Phase II/III trial results for Autism Spectrum Disorder

After promising Phase I/II trial results, we see this trial as potentially opening more doors when it comes to commercialisation.

Meanwhile, the first Investment in our biotech Portfolio (from 2021), Dimerix (ASX: DXB) is fast approaching the catalyst that we initially Invested for - the Phase 3 trial interim analysis readout.

DXB’s major catalyst is due to hit on or around 15th March 2024, just two months away.

DXB signed a commercialisation deal with Advanz Pharmaceutical for up to $230M - AHEAD of the Phase 3 interim analysis results.

DXB is sitting at a good level on 20c at the moment and at one stage earlier this month had re-rated ~425% from a June 2023 low - further evidence of the marked improvement in biotech sentiment over the last 6 months.

We think DXB would be trading a lot higher if not for the existence of a convertible note from May 2023 (it was tough times and the company was desperate for cash).

This note is being progressively converted to shares and we speculate that the shares are being sold into the market (its possible to track the conversions from the note in 2As such as this one)

The DXB share price has been happily eating all the converted note stock at higher and higher share price levels - it still looks like it wants to run.

We look forward to the note conversions being finished soon and DXB’s major catalyst in March 2024.

Finally, our psychedelic assisted therapy biotech, Emyria (ASX: EMD).

EMD has yet to properly go on a run like our other 3 biotechs, but that we’re hoping that may soon change.

On Wednesday, EMD’s specialist was granted “Authorised Prescriber Status” for its MDMA assisted therapy for PTSD

One of the first in Australia.

Think of this like EMD just got the “commercialisation” tick of approval from the TGA for its therapy.

The treatment is for a condition that as many as 1 in 10 Australians suffer from (PTSD) and has an economic cost stretching into the billions of dollars.

And significantly more globally.

We hope a potentially revolutionary, scalable psychedelic therapy program delivered by EMD brings relief to those suffering from the condition.

EMD was featured in the print news last week:

Got a biotech company that you think we should look at?

Send us a message - we read all of the responses.

Battery metals pause for breath? ...

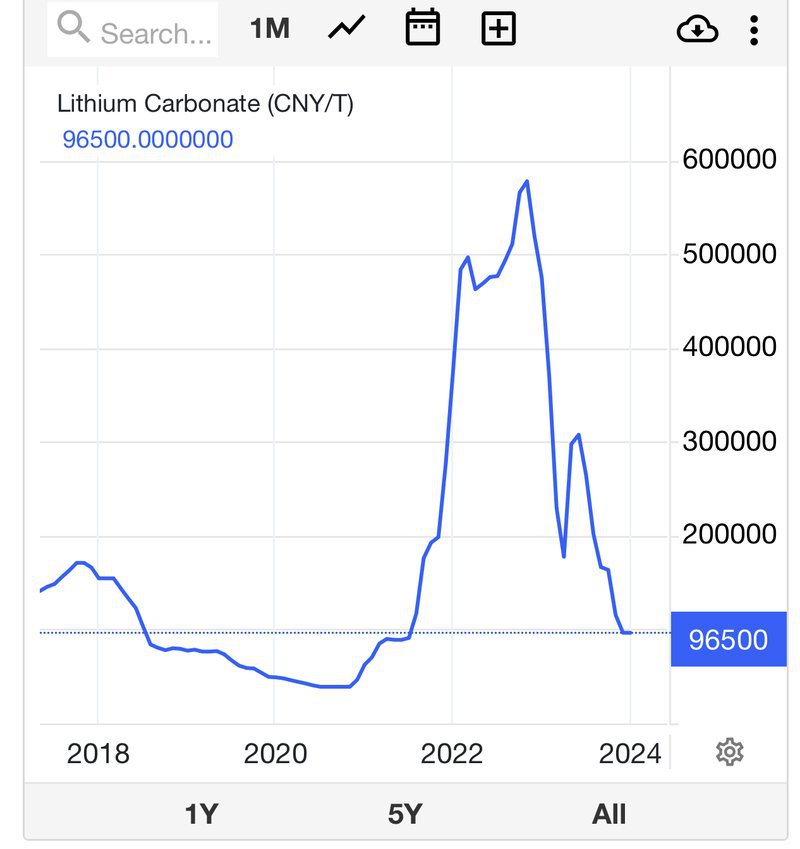

Lithium prices are down ~85% from the early 2022 highs.

(but it hasn’t stopped M&A action in WA)

We have seen short term volatility in the lithium market before...

Back in 2019-2020, the lithium market went through a brief correction where demand was briefly lower than supply.

Then when demand came back, it came back even stronger than before, and the lithium price peaked in late 2022/early 2023.

(Source)

The reality is that the lithium market is still in its infancy and suffers from the volatility new markets face.

In the early days of any market, there is typically a small number of buyers and sellers, and decisions to stockpile vs deplete inventories can cause huge price fluctuations.

Once markets become more mature, and there are hundreds/thousands of buyers, the price for the underlying products becomes more stable.

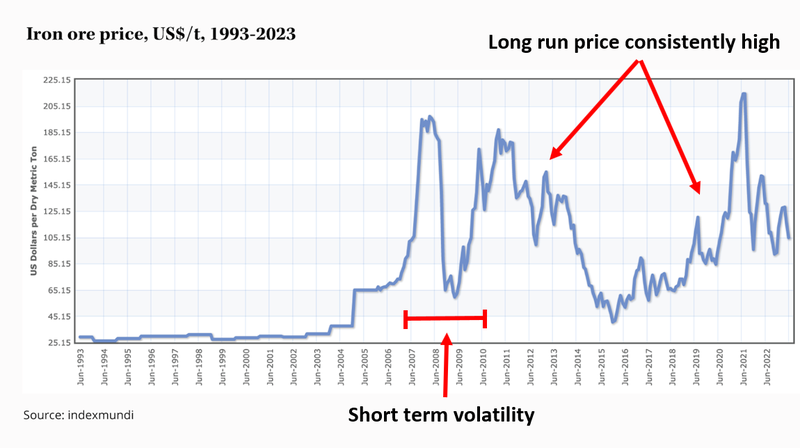

This is what we see with commodities like oil, copper, gold and iron ore.

Volatility in newly developing markets is not unheard of...

For iron ore, after the Global Financial Crisis (GFC) prices fell from ~US$200 per tonne to ~US$55 per tonne.

Most analysts were calling for a long-term price that would stagnate around those levels.

Some producers went bust, some went into care and maintenance, and others were taken over.

Eventually, demand came roaring back, and iron ore prices have consistently traded over US$100 for most of the last decade - albeit with some volatility.

(Source)

We think the lithium industry is going through similar cyclical lows.

Some of the best selling cars in Australia and some parts of Europe are EV’s and we expect demand to continue rising over the next 5-10 year period.

We also think mine shutdowns and capital flows out of the sector will mean long term prices stabilise at much higher levels than today’s prices.

After all, mines going offline mean less supply and once those mines go offline, they are relatively difficult to get back into production.

Commodities work in cycles.

And just because the lithium price has cooled doesn’t mean it will stay that way.

We think that the key is to find a good project, with good management that will be ready to take advantage of undersupply / new demand for a commodity when the time comes.

It also provides some great valuations to enter high quality, advanced battery metals stocks at low valuations.

We are still keen on lithium, especially at the current lower macro sentiment valuations.

We are also still VERY keen on WA lithium exploration - the softness in the lithium price hasn’t slowed down M&A activity and consolidation in the WA lithium space.

(check out TG1 which is our favourite in the WA lithium exploration space - they are drilling in the coming months)

Know any advanced battery metals stocks that are way undervalued that you think we should look at?

Send us a message at [email protected] - we read all of the responses.

Bottom Drawer

Today we will be moving two more stocks to our Bottom Drawer Portfolio.

Our “Bottom Draw Portfolio” is our list of Investments that were unable to make meaningful progress towards our “Big Bet”.

This is generally due to a key risk materialising.

We still hold/watch our Bottom Drawer stocks closely, in the hope that they pull a rabbit out of the hat and return to the main Portfolio.

But, to make room for new investments and new opportunities we may look to sell some or all of our position in these stocks.

If we sell out of a stock entirely, it will be moved to our “Past Investments”.

Vonex (ASX:VN8)

Our VN8 Big Bet: VN8 grows to a size that attracts a takeover bid from a larger telco (at multiples of our Initial Entry Price) by acquiring and consolidating smaller telco businesses.

What Happened?

VN8’s strategy was to grow through acquisitions and debt, making four acquisitions in under two years to grow its top-line revenue.

This strategy worked well for Unity Group who was taken over for $3.6BN in 2022.

However, VN8 was too slow to integrate the new business and it could not grow fast enough before interest rate hikes put a strain on the heavily leveraged strategy.

A writedown of $19M last year was a tough re-set of the balance sheet, and the company has not made meaningful progress since.

We are hoping to see the company recover from its position but it has been slow moving.

We still think VN8 could successfully deliver the turnaround and eventually pay down the debt from its acquisition spree

VN8 recons they will do ~$50M in revenue with $5M EBITDA, but it’s going to be a slow grind to pay down the ~$21M debt.

As such we have moved VN8 to the Bottom Drawer for now.

Ragusa (ASX: RAS)

Our RAS Big Bet: That RAS will return 10x by discovering and defining a significant enough deposit to move into development studies for one of its projects.

What Happened?

We first Invested in RAS for its suite of exploration projects.

During the time we have held RAS, the most interesting project for the company was its NT Lithium project next door to lithium producer Core Lithium.

After its drilling campaign the company did not deliver material lithium results and the “exploration risk” materialised.

As such, we have moved RAS to the bottom drawer.

2024 ramping up

It’s been a good holiday break and had been a slowish start to 2024, but this week felt like things in the markets started moving again.

The U price ripping last night will certainly get a few more investors out of their poolside deck chairs a little earlier than they probably planned.

We also expect more companies to start announcing news again over the next couple of weeks as boards and management return from their breaks.

What we wrote about this week 🧬 🦉 🏹

Oneview Healthcare (ASX: ONE)

Bring Your Own Device (BYOD) and a recently activated value added reseller agreement with $30BN capped NYSE listed Baxter International have got ONE Investors like ourselves enthused about ONE’s future trajectory.

We’ve tried the BYOD tech and we rate it - it’s as easy as opening up your web browser on your phone.

ONE released its quarterly report last week which we think provided some excellent insights into its future trajectory.

Here’s what we really liked about ONE’s quarterly report:

- Baxter progress

- BYOD progress

- Minimal cash burn

- Healthy cash balance

It all adds up to another strong quarter for ONE.

Most importantly, ONE has now activated a partnership with Baxter - meaning potentially more than 500,000 hospital beds in Baxter's network are now available for ONE to sell to.

Read: Baxter is Coming... and so is BYOD.

Emyria (ASX: EMD)

On Wednesday, EMD’s specialist was granted “Authorised Prescriber Status” for its MDMA assisted therapy for PTSD

One of the first in Australia.

This is a major milestone for the company and for the industry as a whole.

Authorised Prescriber Status allows EMD’s specialist to provide MDMA-assisted therapies in its clinic in Perth as a treatment and not just in a clinical trial.

Think of this like EMD just got the “commercialisation” tick of approval from the TGA for its therapy.

We think there’s plenty to look forward to as EMD Investors.

Read: APPROVED: EMD Receives Authorisation to Prescribe MDMA for Therapy

Pursuit Minerals (ASX: PUR)

On Monday, PUR received its drilling permits, meaning PUR will soon be drilling at its Argentine lithium project inside South America’s ‘lithium triangle’

The lithium triangle is home to ~60% of the world’s lithium reserves.

In October PUR announced a maiden 251.3kt lithium carbonate equivalent (LCE) JORC resource based ONLY on shallow 200m deep historical drill holes and recent geophysical surveys.

(without PUR drilling a single hole)

With permits now in hand, the goal for the upcoming drilling is to see if the brine reservoirs extend at depth AND to see if the lithium grades are higher as PUR drills deeper.

Which would mean a material increase to resource size...

Read: Drilling commencing - does it go deeper? We’ll soon find out...

Quick Takes 🗣️

88E: 88E to flow test Hickory-1 discovery in mid February

PFE: PFE gets even more land in USA lithium hotspot

Q1 2024 Catalysts List

Things to watch out for in the coming weeks

Every new year starts off the same...

Most investors don't make it back to their desks until after Australia Day (26 January), and companies continue working on major catalysts that didn't get delivered before the end of the previous year.

Here are some companies across our portfolio that we are expecting material news in the next couple of months.

- Dimerix (ASX: DXB) - Interim results from its Phase 3 clinical trial on FSGS (March 2024)

- Neurotech International (ASX: NTI) - NTI has TWO catalysts coming up., results from a Phase II/III trial for Autism Spectrum Disorder and a Phase I/II Rett Syndrome clinical trial (positive Rett Syndrome results laid the foundation for Neuren Pharmaceuticals now +2,000% re-rate).

- 88 Energy (ASX: 88E) - Flow test of its Hickory-1 oil & gas discovery in the North Slope of Alaska in the US.

- Noble Helium (ASX: NHE) - final independent lab analysis on samples from its two wells.

- TechGen Metals (ASX: TG1) - Rock chip/soil sampling results from its lithium project in WA ahead of the company’s first drill program.

- Haranga Resources (ASX: HAR) - Assay results from its uranium project in Senegal.

- Grand Gulf Energy (ASX: GGE) - Sidetrack well at its Jesse-1A well. GGE will be looking to isolate and then stimulate its helium discovery - the goal being a commercially viable helium flow test.

- Tyranna Resources (ASX: TYX) - Assay results from its Angolan lithium project. TYX has hit plenty of visual spodumene in its drill cores so the assay results should be interesting.

- Solis Minerals (ASX: SLM) - Assay results from its Brazilian lithium project.

- Lanthanein Resources (ASX: LNR) - Drilling to start in February/March at its Lady Grey lithium project, next door to SQM/Wesfarmers giant Early Grey lithium mine.

- Galileo Mining (ASX: GAL) - Assay results from its nickel/palladium project in WA.

- Kuniko (ASX: KNI) - Maiden JORC resource from its nickel project in Norway.

- Arovella Therapeutics (ASX: ALA) - We’re looking for a finalised Phase 1 clinical trial plan from ALA, which could drop this quarter or the next. We’re also looking for data on animal studies from the ALA + Imugene partnership for solid tumours.

Bite sized summaries of the latest mainstream news in battery metals, biotechs, uranium etc: The Future Money: https://future-money.co/

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.