Drilling commencing - does it go deeper? We’ll soon find out…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 49,915,999 PUR shares and the Company’s staff own 1,116,668 PUR shares at the time of publishing. The Company has been engaged by PUR to share our commentary on the progress of our Investment in PUR over time.

Drilling is starting in a couple of weeks time...

Pursuit Minerals (ASX:PUR) will soon be drilling at its Argentine lithium project inside South America’s ‘lithium triangle’

The lithium triangle is home to ~60% of the world’s lithium reserves.

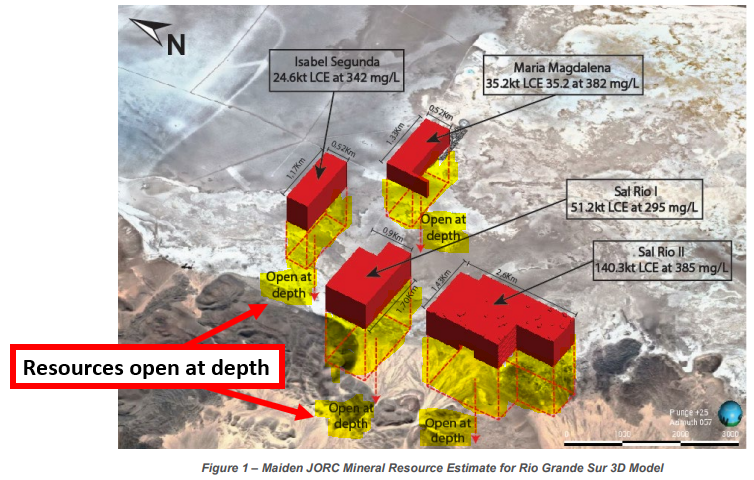

In October PUR announced a maiden 251.3kt lithium carbonate equivalent (LCE) JORC resource based ONLY on shallow 200m deep historical drill holes and recent geophysical surveys.

(without PUR drilling a single hole)

With permits now in hand, the goal for the upcoming drilling is to see if the brine reservoirs extend at depth AND to see if the lithium grades are higher as PUR drills deeper.

Which would mean a material increase to resource size...

Which would mean more to put through PUR’s 100% owned processing plant - which is expected to be production ready by the end of Q1-2023.

Over the last few months, PUR has been running geophysical surveys showing potential for lithium brines all the way down to 500-600m+ depths.

IF PUR hits higher grade lithium at depth AND an upgrade to its existing JORC resource we would hope to finally see a re-rate in the PUR share price which has been churning along at ~1c.

Drilling was supposed to start in December - but it's now officially all happening at the start of 2024.

PUR’s near term plan is to drill four exploration wells and one pumping well down to depths of ~500-600m.

This drilling will test the theory that there is higher concentrate lithium deeper down.

High concentrate lithium would significantly increase the amount of tonnes of lithium carbonate PUR have on their hands.

Once drilling is done, PUR plans to upgrade its existing JORC resource of 251.3kt of lithium carbonate equivalent.

A feasibility study planned for Q4 of this year.

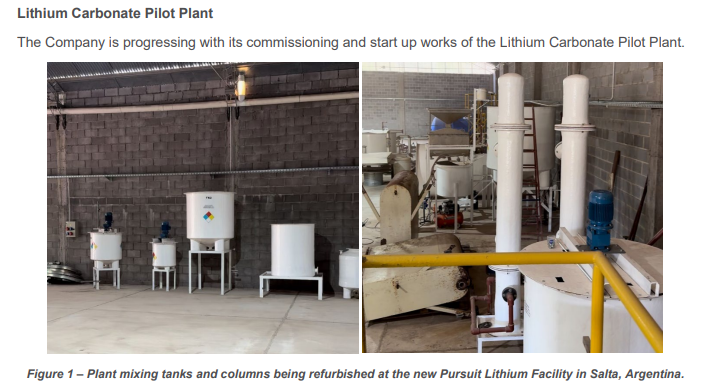

In parallel to drilling, PUR is also about to finish commissioning its 250 tonne per annum processing plant.

This plant could see PUR producing lithium carbonate equivalents at some point this year, which could also deliver a market re-rate for PUR.

Right now, PUR’s existing JORC resource is based only on historical drillholes that go down to depths of ~200m..

No drilling has been done beyond that on PUR’s ground...

PUR’s drill program will be looking to do what other companies have done on salars across Argentina before - drill deeper looking for higher grade, thicker lithium brine reservoirs.

We’ve seen it play out before:

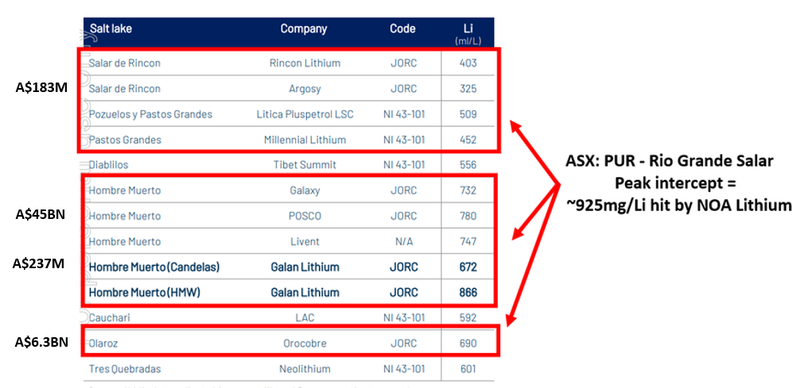

- At the Pastos Grande Salar - where PUR’s CEO has previously had experience. At Pastos Grande, holes drilled down to ~90-180m had average lithium grades of 538 mg/l... Holes drilled down to ~365-620m depths had average lithium grades of ~641 mg/l.

- To the north of PUR - One of PUR’s peers, TSX listed NOA Lithium intercepted lithium grades of ~433mg/li at depths of ~101m then after drilling to depths of ~300-400m started hitting grades of ~773mg/li to ~925mg/li.

At the moment PUR’s inferred resource is based on an average grade of 351mg/li, about half of what peers are finding lower down.

PUR will be drilling deeper and IF higher grade lithium structures are found then it could quickly multiply the size of its JORC resource.

Grades as high as the ones seen by NOA Lithium could put PUR’s project amongst some of the biggest in South America and projects owned by companies with market caps much larger than PUR...

Here is a comparison of grades from Rio Grande with the other Argentinian salars and the peers that own them.

Argentina’s new president wants it to be a mining powerhouse

Argentina’s new president Javier Milei is determined to do things differently.

It’s clear he’s a fan of aggressively cutting red tape:

(Source)

But both the president and the country more generally acknowledge that it will take quite some time to re-establish the country as an economic force in South America.

Part of that ambition is expanding the country’s mining export capacity.

Milei said in a presidential decree outlining reforms in December that, “Mining is another area with great potential in the country that is notably underdeveloped...To that end, we must eliminate costs”.

There have been some positive early signs that red tape for mining companies is getting scaled back, as evidenced by PUR’s relatively quick permitting process which took just 5 months.

Recent media coverage of Argentina’s mining industry, also indicates a new direction for the country:

(Source)

Traditionally Chile has made up the bulk of production and Bolivia’s lithium industry is in its early stages.

But increasingly, Argentina is looking to usurp Chile’s status as the go-to location for lithium carbonate production.

While we are no experts on Argentina’s politics, we think the macro sentiment for lithium production in Argentina is improving - something which could benefit PUR over the long run.

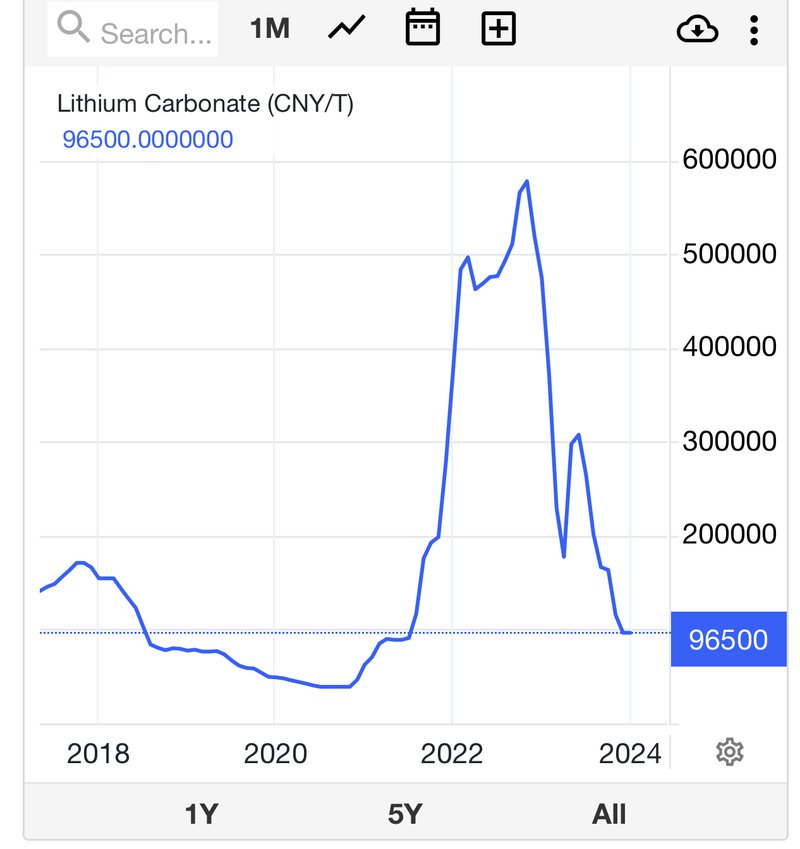

Lithium macro going through a downturn... Again...

Timing wise, PUR’s drill program comes at a tough time for the lithium sector.

Lithium prices are down ~85% from the early 2022 highs AND some of the developers/miners are switching their mines off.

But we have seen all of this happen before...

Back in 2019-2020, the lithium market went through a brief correction where demand was briefly lower than supply.

Then when demand came back it came back even stronger than before and the lithium price peaked in late 2022/early 2023.

The reality is that the lithium market is still in its infancy and suffers from the volatility new markets face.

In the early days of any market, there is typically a small number of buyers and sellers, and decisions to stockpile vs deplete inventories can cause huge fluctuations in prices.

Once markets become more mature, there are hundreds/thousands of buyers, and the price for the underlying products becomes more stable - like the stability we see in oil, copper and iron ore markets today.

Volatility in newly developing markets is not unheard of...

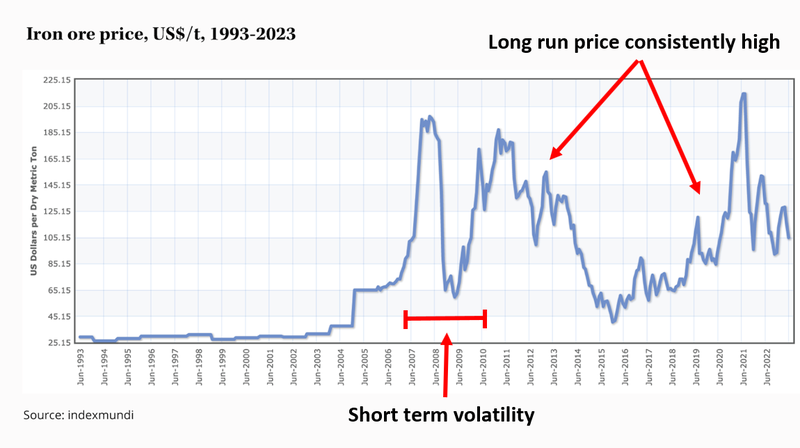

For iron ore, after the Global Financial Crisis (GFC) prices fell from ~US$200 per tonne to ~US$55 per tonne.

Most analysts were calling for a long-term price that would stagnate around those levels.

Some producers went bust, some went into care and maintenance, and others were taken over.

Eventually, demand came roaring back, and iron ore prices have consistently traded over US$100 for most of the last decade - albeit with some volatility.

We think the lithium industry is going through similar cyclical lows.

We think that eventually, demand will grow as the industry is built out.

We also think mine shutdowns and capital flows out of the sector will mean long term prices stabilise at much higher levels than today’s prices.

Cost curve position is everything in the long run

Ultimately, when it comes to mining, where a project sits on the cost curve is everything.

By that we mean how cheap/relatively cheap a company can mine its product.

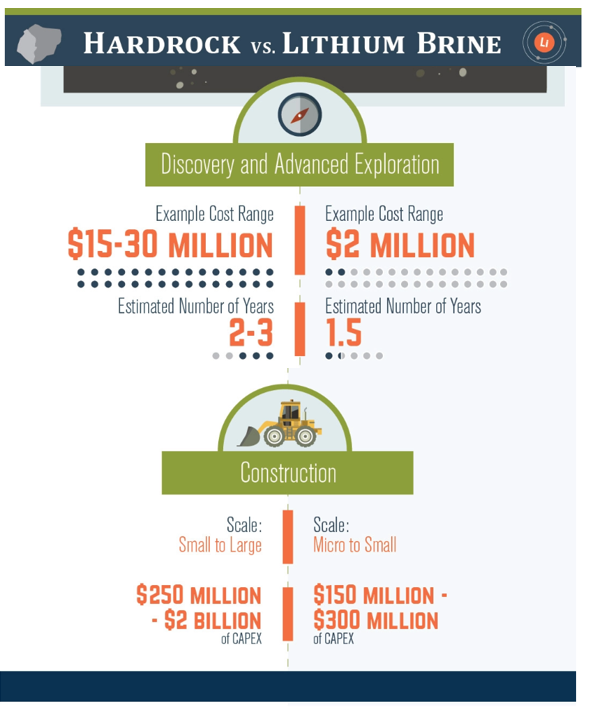

At the moment, most of the world's unprocessed lithium comes from hard rock spodumene hosted mines even though ~60% of the world's reserves are hosted in brines.

The reality is that it is a lot cheaper to mine lithium from brines than it is hard rock.

Instead of having to dig a big hole in the ground, brine operators just drill wells into the ground and pump their lithium brines up to surface.

Brine operations typically cost a lot less to discover and develop too...

In terms of discovery and exploration costs, hard rock projects can cost upwards of $30M, whereas lithium brine projects can cost as low as $2M.

In addition, exploration timelines are typically almost half as long for lithium brine projects.

When it comes to development, brine projects can cost almost one-tenth of the cost of hard rock projects.

Source: A Cost Comparison: Lithium Brine vs. Hard Rock Exploration

Of course, there will always be hard rock mines that are cost competitive but in the long run, we expect to see the brine operations with scale sitting in a strong position when it comes to long run operating costs...

Ultimately, those who produce lithium at the cheapest price will benefit the most no matter what the lithium price is doing...

The fact PUR’s lithium project is based on brines is one of many reasons we are Invested in PUR.

🎓 See our educational article on the differences between hard rock and lithium brine projects here: The different types of lithium projects explained

Why we are Invested in PUR:

- PUR’s project already has an existing JORC resource - PUR has managed to define a JORC resource of 251.3kt of lithium carbonate equivalent before any drilling.

- Exploration upside - Most of the drilling in the Rio Grande salar (salt lake) has been down to depths of ~200m. Lithium mineralisation is interpreted to extend down to depths of ~500m in depth, leaving plenty of exploration upside for PUR to chase.

- Processing plant being commissioned - PUR has fast tracked its pathway to first production by purchasing a processing plant. The plant is currently being commissioned and will be able to produce ~250 tonnes of lithium carbonate equivalent per annum.

- Strong management team - Team includes the founding chairman of $402M Syrah Resources - Tom Eadie, and Kyle Stevenson was also the founder of Millennial Lithium which was eventually sold for CAD$491M.

- Located inside Argentina’s “lithium triangle” - PUR’s project sits in a region home to ~50% of global lithium supply, dubbed the “lithium triangle” of Argentina. The region also hosts majors like Allkem (capped at $6.3BN), Albemarle (capped at $24BN), SQM (capped at $24BN) and Rio Tinto ($182BN) hold lithium projects. This brings with it potential future consolidation opportunities.

- Low market cap relative to advanced peers - PUR currently has a market cap of ~$24M, which is low compared to other lithium brine players Argosy Minerals (~$190M).

Ultimately we hope that a combination of these reasons helps take PUR to a market cap >$1BN which forms the basis for our PUR “Big Bet” which is as follows:

Our PUR ‘Big Bet’

“PUR increases the size and scale of its lithium project to a level that warrants putting it into production. We are hoping this re-rates the company to a market cap of >$1bn (similar to what peer company Argosy achieved)”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PUR Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

More on PUR’s drill program:

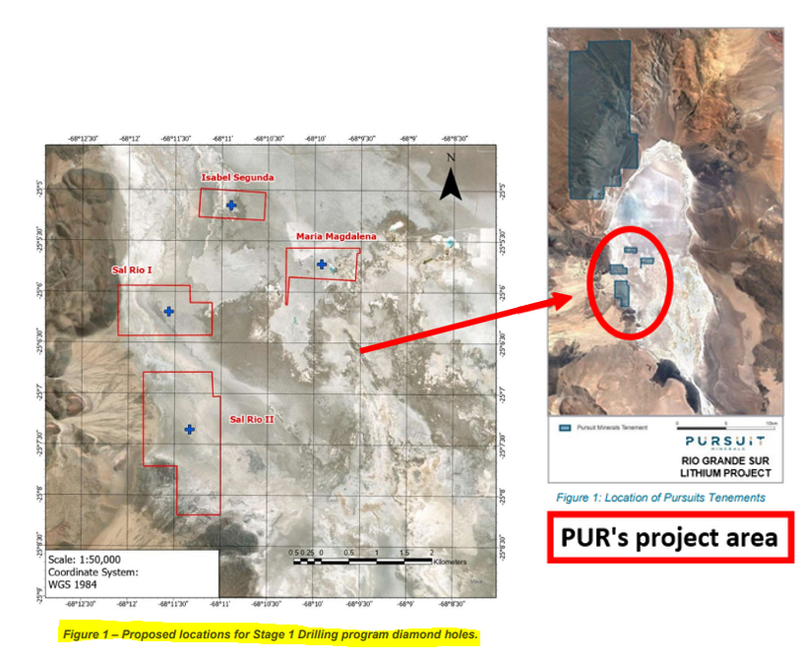

PUR plans to drill four exploration holes down to ~500m-600m depths.

After the four holes are drilled, PUR is planning to drill ONE pumping well to determine flow rates for the project.

Below are the drillhole locations for the first phase of drilling:

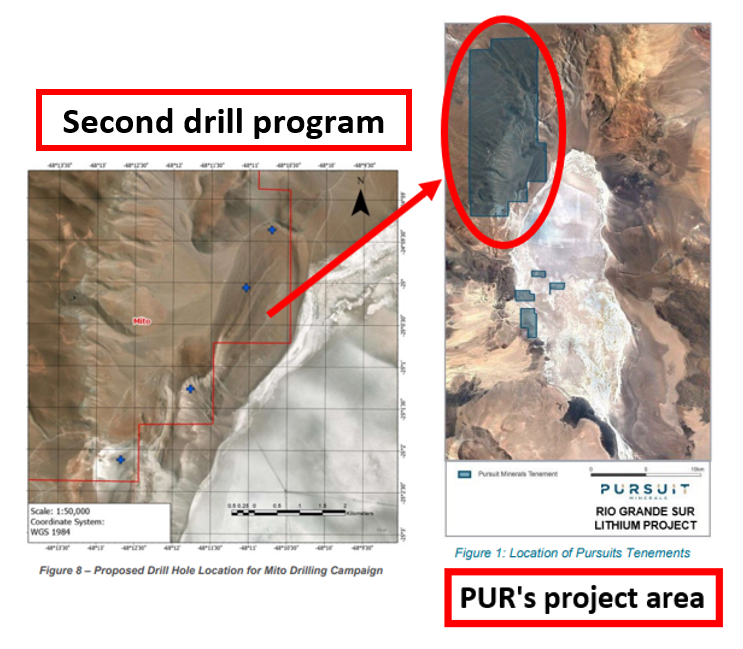

After its first phase of drilling, PUR will move onto its larger Mito tenement to the north.

Mito is PUR’s biggest landholding and sits right on the margins of the Salar.

Here PUR will be testing to see if the brine reservoirs inside the Salar extend out onto the margins - a theory that PUR’s neighbour NOA Lithium has been testing and successfully proving.

What’s next for PUR?

Phase 1 drill program 🔄

PUR expects drilling to start in a few weeks' time and the drilling to run through to the end of Q2-2024.

Pilot plant commissioning 🔄

In a recent update, PUR confirmed that its processing plant had been relocated to a new facility where commissioning works had started.

PUR expects the plant to be commissioned and ready to start producing in Q1-2024.

Once fully assembled PUR expects to be producing both battery and technical grade Lithium Carbonate - which it can send off to potential buyers/offtake partners.

PUR has mentioned that the company had received “several expressions of interest for the development of the project inclusive of off-take agreements”...

What are the risks?

Now that PUR has defined its own JORC resource, the key risk for the company is around “commercialisation”.

PUR is looking to produce battery-grade lithium carbonate from its pilot processing plant.

There is a risk that PUR experiences technical issues trying to get the plant back online OR that adjustments need to be made to its plant to make it suitable for the brines at its project.

There is still an element of exploration risk too considering PUR will be looking to expand its existing JORC resource with its 2024 drill program.

Drilling is always risky and there is a chance PUR fails to find higher grade lithium brines at depth which would impact any future resource upgrades.

Finally, as PUR is a small cap it is subject to future capital requirements - the company may need to raise more capital to continue to fund its operations. We note its September 30 cash balance of $3.6M. With pilot plant commissioning and drilling to pay for, these costs may precipitate a capital raise.

Capital raises can incur dilution for shareholders and may take place at a discounted share price.

Future capital requirements - The availability of equity or debt funding is subject to market risk at the time and there is no guarantee that PUR will be able to secure future funding on terms acceptable to the Company.

Dilution & issue of further securities – PUR may issue future securities which may rank ahead of or pari passu with existing shares, or dilute existing shareholders.

You can see more on the key risks in our PUR Investment Memo.

Our PUR Investment Memo

Along with the key risks, our PUR Investment Memo provides a short, high-level summary of our reasons for Investing.

The Investment Memo details:

- Our PUR Big Bet

- Why we Invested in PUR

- Key objectives we want to see PUR achieve

- What are the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.