PUR’s Pathway to Lithium Production - Here’s what it needs to do next

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 28,915,999 PUR shares and the Company’s staff own 1,116,668 PUR shares at the time of publishing. The Company has been engaged by PUR to share our commentary on the progress of our Investment in PUR over time.

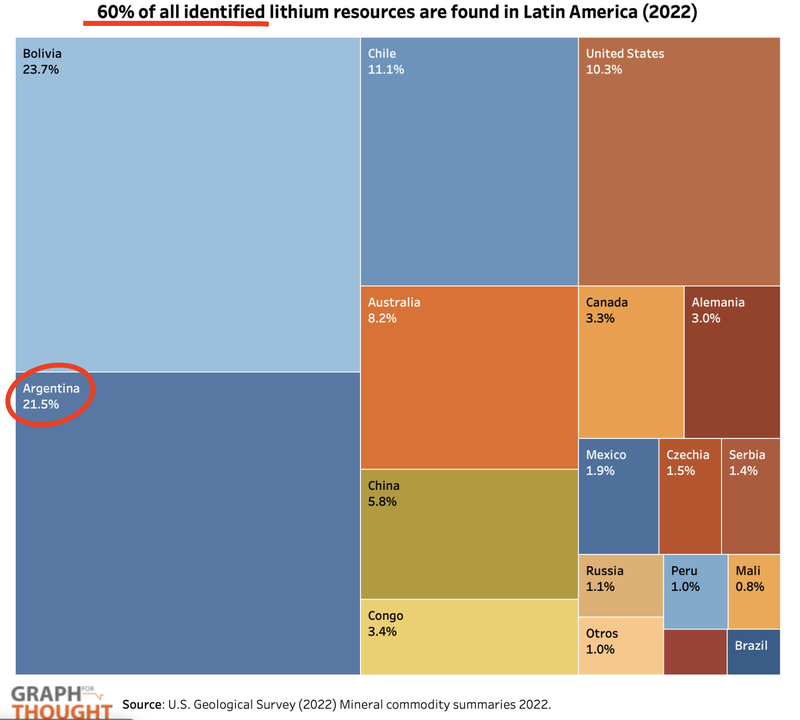

South America’s “lithium triangle” contains 60% of the world's lithium resources and reserves.

The lithium triangle covers Argentina, Chile and Bolivia. The region is soon expected to overtake Australia as the biggest source of lithium production on the planet.

Global lithium giants are pouring capital into the region through existing projects and via acquisitions.

Some recent examples include Rio Tinto spending US$830M on projects - and Korean conglomerate, POSCO, committing over US$4BN in investments.

We have Invested in an emerging developer on a pathway to lithium production in the region.

Our Investment Pursuit Minerals (ASX:PUR) recently settled on the acquisition of an advanced lithium brine project in Argentina.

We first wrote about PUR’s move into Argentinian lithium back in December 2023. Since then, the deal on the project has settled, the new shares related to the transaction have been issued, and it looks like the share price has formed a solid base in recent weeks.

To read our Investment Memo and what we want to see PUR achieve this year - click here.

PUR’s ground spans 9,232ha within a salt lake in Argentina called the Rio Grande Salar.

Inside that salt lake is an already defined foreign NI43-101 lithium resource of 2.1Mt lithium carbonate equivalent (LCE) at an average grade of 370mg/Li.

That resource was based on historical drilling completed over the salt lake by other companies and is based on data from drilling down to depths of only 100m.

As a result, we consider PUR’s project relatively advanced — we know the lithium is there.

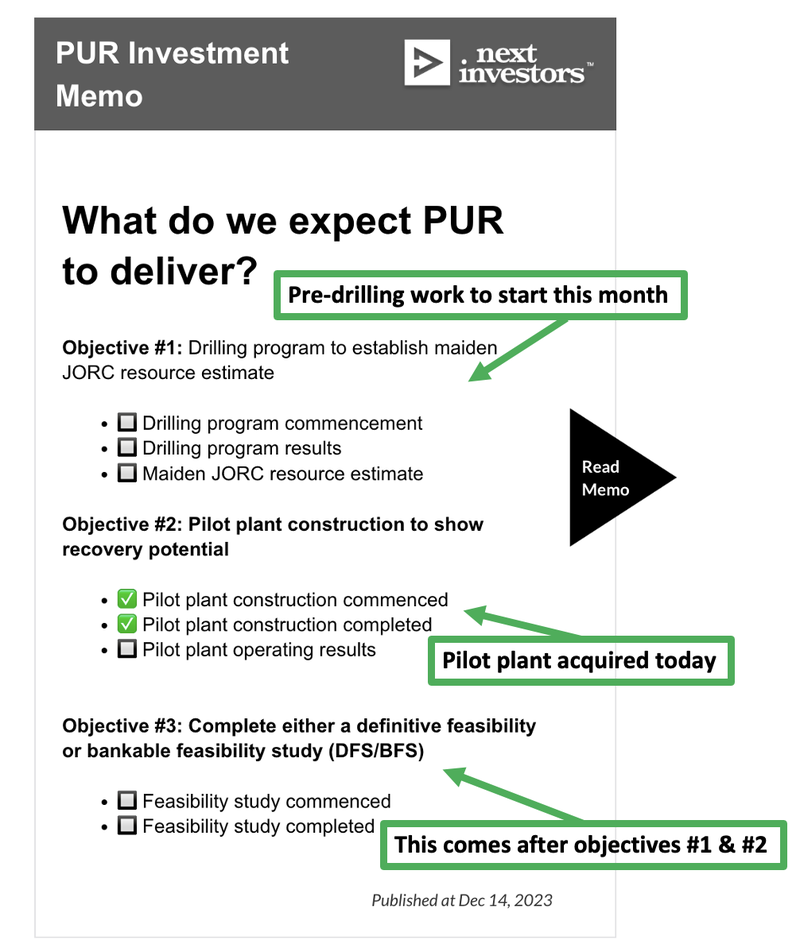

In order for PUR to progress through to a definitive feasibility study the company will need to:

- Update its geological models;

- Do some drilling;

- Define a maiden JORC resource of its own; AND

- Prove that it can produce battery grade lithium carbonate from its brines.

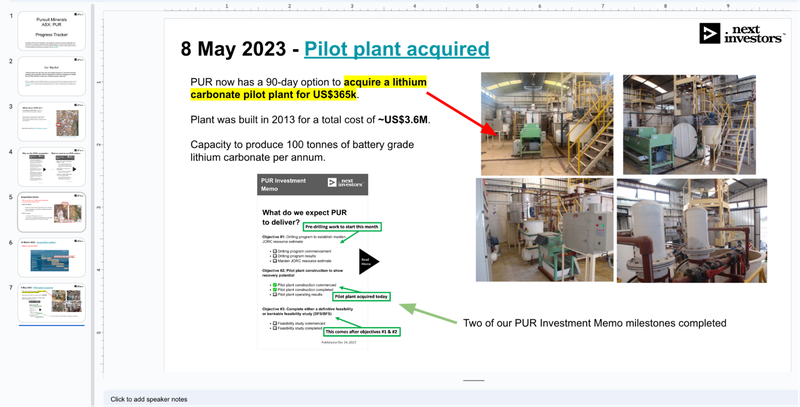

This morning PUR made progress on the last one (producing battery grade lithium carbonate).

On the weekend we wrote that we want to see our early stage lithium investments progress as quickly as possible up the mining company lifecycle. Progressing up the lifecycle increases likelihood of a strategic investor or takeover.

Today PUR fast tracked its progress by entering into an option agreement to buy an existing pilot plant for US$365k.

Without this agreement, it would have taken years to build a pilot plant and millions of dollars to build from scratch - the previous vendor paid US$3.6M for the plant.

The pilot plant has historically produced battery grade (99.5%+ purity) Lithium Carbonate.

PUR will now look to replicate this success with its own lithium brines.

By purchasing this already built lithium brine plant, rather than building it from scratch, PUR can fast-track production of battery grade lithium carbonate.

With inflationary pressures and labour shortages we think that this acquisition puts PUR well ahead of the timeline we expected for the company - particularly because the acquisition cost is ~10% of the value that the vendor paid to build it.

It’s been a few months since we last wrote about PUR, and given today’s news, and other progress being made, it’s time we checked in.

What success might look like - Here is PUR’s playbook

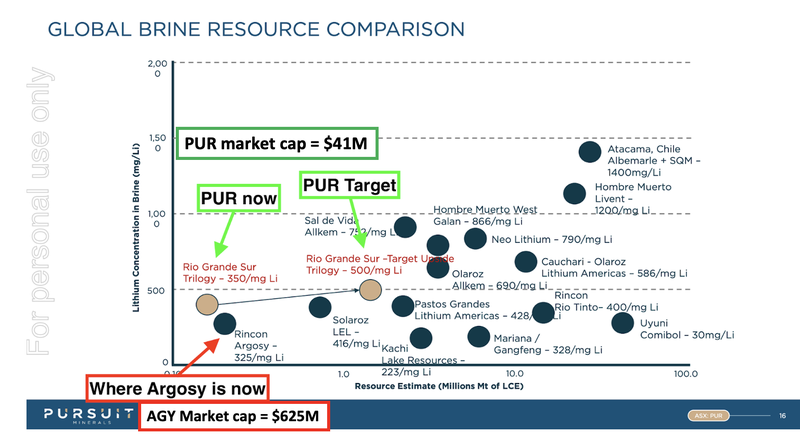

PUR currently trades with a market cap of $41M, and had $4M in cash at the end of the March quarter.

Ultimately PUR is looking to emulate the success of Argosy Minerals.

Over many years, Argosy has taken its lithium brine project from a maiden resource to production in Argentina.

This is exactly what PUR is setting out to do.

Argosy is now valued at many multiples of PUR:

Argosy is currently capped at $624M, however, at its peak, it hit a market cap of $1.1BN.

From first resource (in 2017) through to first production (in 2022), Argosy’s share price rose from ~5c per share to a high of ~80c per share.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think that over the next 12-24 months PUR’s project has the potential to catch up to, and exceed, the size and scale of Argosy’s.

Of course - this is no guarantee - PUR is a high risk small cap stock, and lots can still go wrong. We outline the risks in our Investment in PUR further down the page, and in our Investment Memo.

Argosy is currently ramping up ts 2,000tpa lithium carbonate plant.

PUR’s target is a stage one processing plant capable of producing 2,000tpa LCE - the exact same nameplate capacity.

PUR is planning for its 2,000tpa processing plant to be ready within the next 24 months.

The below chart is a good representation of where PUR is now and where the company is aiming, relative to Argosy - and the other global lithium brine resources.

PUR’s goal is to develop a larger resource estimate and maintain a high concentration of lithium in its brine - which should reflect a higher valuation for the company - ideally getting it closer to or exceeding Argosy.

We are Invested in PUR for the long term to see PUR deliver on its production goals, and that includes continuing to hold the majority of our position through the short-medium term volatility as per our Investment Plan.

Update on our PUR Investment Memo

Back when the deal first got announced, we put together an Investment Memo on PUR, including what we wanted to see the company deliver over the coming 12 months.

Key for us is the following objectives, as kicking these goals will demonstrate to the market that the company is making solid progress - and with that we hope to see the stock re-rate upwards.

How PUR plans to grow its valuation over the coming 12-24 months

The high level answer - through a mixture of fast tracking production and exploration - as we have shown above in the objectives.

1) Lithium processing - demonstrate it can produce high grade lithium carbonate

While PUR runs its exploration programs (set to start this month), the company is also looking to advance a Stage 1 Processing Plant capable of producing ~2,000 tonnes of lithium carbonate per year.

The plan is to be producing ~2,000 tonnes per annum within 24 months and 20,000 tonnes per annum within 36-48 months.

This plan was expedited today, with PUR confirming the purchase of a smaller scale processing plant for just US$365k.

The pilot plant has a nameplate capacity of 100 tonnes per year.

The pilot plant means PUR can start production testing its project a lot quicker than first expected - meaning a condensed timeline to first production.

In the short term though, PUR’s activities will be about exploration, so that it can define its share of the salar’s existing resource estimate.

2) PUR’s exploration drilling - to build and improve confidence in its lithium resource.

Inside the salt lake that contains PUR’s ground, there is an already defined foreign NI43-101 lithium resource of 2.1Mt lithium carbonate equivalent (LCE) at an average grade of 370mg/Li.

However, this is not yet a JORC classified resource.

PUR plans to drill out its project based on two theories, with a view of establishing a maiden JORC resource by the end of this year.

3) Drill deeper (relatively lower risk)

PUR wants to drill out the areas that sit inside the existing (foreign) resource.

The existing lithium resource currently extends down to depths of ~100m from the surface.

PUR wants to drill deeper drillholes (down to >300m), in order to see how much of this resource sits inside its ground.

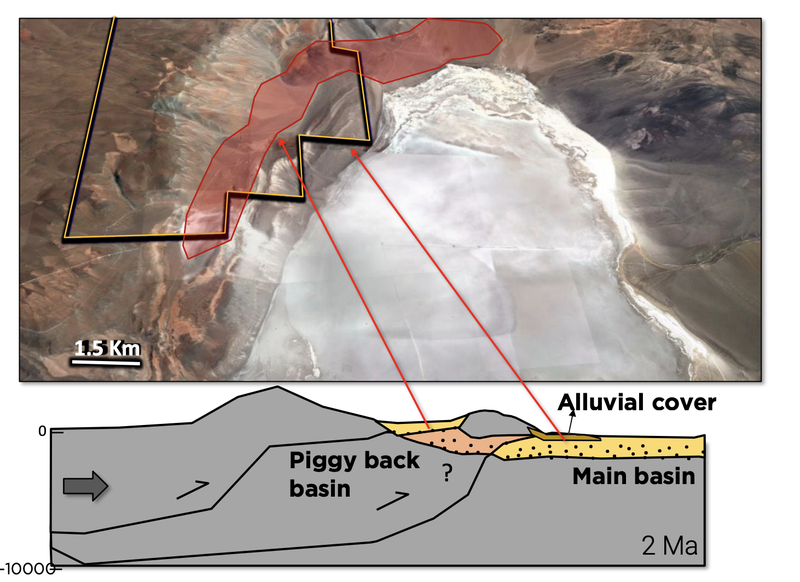

4) Drill further away - (Blue sky exploration potential)

PUR wants to drill test a “sub-basin” theory on its ground at the margins of the salt lake.

This theory has been tried and tested across other salt lakes in South America’s lithium triangle, delivering additional lithium resources for those successful.

It involves drilling on the edges of a salt lake to see if the lithium aquifers extend deep underground.

Both theories could significantly increase the size and scale of PUR’s project.

We view the “sub-basin theory” as the unexpected blue sky exploration equivalent for PUR.

To get an idea of the ground, below is an image from the PUR team on site in Argentina ahead of its exploration programs (set to commence in May).

Ultimately the exploration program and work on processing are the first steps toward what we hope will eventuate in our PUR Big Bet materialising:

Our PUR ‘Big Bet’

“PUR increases the size and scale of its lithium project to a level that warrants putting it into production.

We are hoping this re-rates the company to a market cap of >$1bn (similar to what peer company Argosy achieved)”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PUR Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

For a high level update on PUR’s progress, check out our Progress Tracker for PUR:

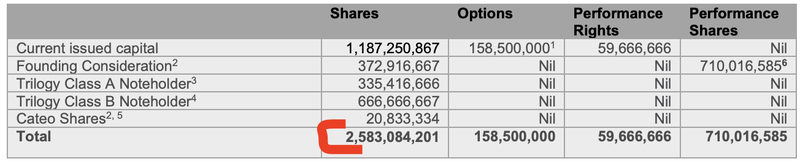

Capital structure update

PUR settled the acquisition of its Argentinian lithium project in full on the 29th of March.

As part of the settlement, PUR issued ~1.4 billion new shares, most of them at 1.2c per share.

Of that ~ 1.4 billion new shares, 625 million are under mandatory escrow, while ~ 750 million are tradeable on the market.

In total, there are over 2.5 billion PUR shares on issue - here’s the full capital structure post settlement of the deal:

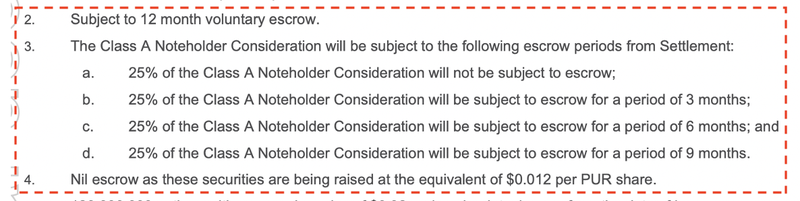

Here are the escrow periods for the different share types:

🎓 We keep track of our Portfolio companies' capital structures in the following spreadsheet - to access the spreadsheet click here.

PUR’s share price since the acquisition was first announced and even after the settlement occurred has consistently traded well above 1.2c per share.

At last close, PUR was trading at 1.6c per share.

Typically investors in new acquisitions like PUR’s will hold shares for longer but investor psychology plays a big role in bearish markets like we are currently in.

As a result, we expected some of the ~750 million shares that are non-escrowed to come to market.

Since the acquisition was first announced we have seen ~814M shares traded, ~342M of these shares were traded after the settlement occurred.

Our view is that a large chunk of the post-deal churn has already happened and PUR’s share price has started forming a base off which to build.

With the register now fully diluted (post-transaction), PUR’s shareholder register can turn over, leaving room for the share price to (hopefully) re-rate if/when the company delivers fundamental progress at a project level.

Why we like the lithium triangle - and Argentina in particular

So why did PUR move into a lithium project in Argentina? The macro thematic plays a big role.

The International Energy Agency (IEA) anticipates a 40x increase in lithium demand by 2040.

This means the world needs much more lithium over the next two decades.

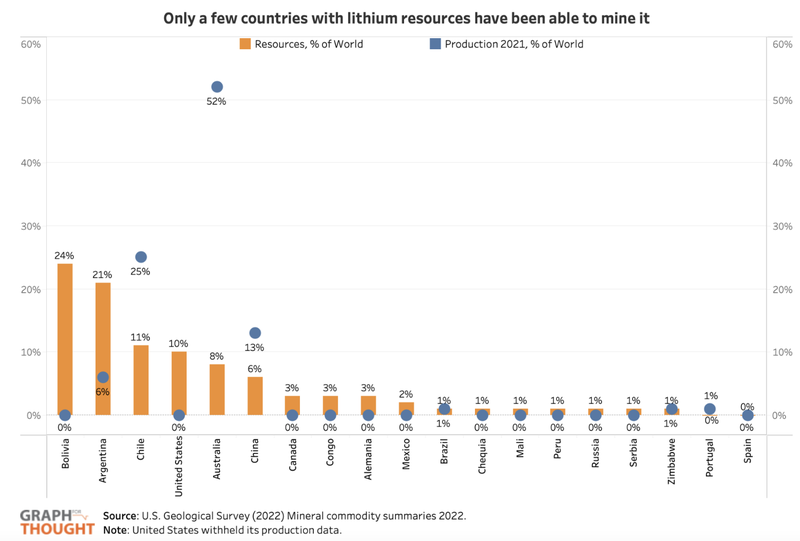

Most of the world's lithium is currently produced in Australia (~52%), despite Australia only holding ~8% of the world's known lithium resource.

This is where the lithium triangle comes into play — ~60% of the world's known lithium resources sit in this region that sits across Bolivia, Chile and Argentina.

Argentina — which is the location of PUR’s project — holds ~21% of the world's resources but only accounts for ~6% of the world's lithium production.

Our view is that in order to meet the coming lithium demand over the next 20-30 years, the world needs to commit capital to regions where lithium resources exist that need to be developed and put into production - like Argentina.

Head of Metals Research at Bank of America, Michael Widmer, agrees with this view saying, “if Argentina didn’t come through, it’d be almost impossible for the lithium market to stay well-supplied".

Thanks Argentina.

Senior Analyst from Benchmark Mineral Intelligence (Daisy Jennings-Gray) also agrees with our view and anticipates Argentina will overtake Chile in lithium production by 2027.

Chile currently produces ~25% of the world's lithium, or around 4.5x as much as Argentina.

However - Chile has recently started making foreign investors nervous.

A few weeks ago, Chile’s President announced that it would nationalise a large chunk of its lithium industry. This is a move that could see capital pour out of Chile and look for homes in other countries capable of producing significant volumes of lithium.

In fact, the flight of capital out of Chilean lithium has already begun:

That news just strengthens the macro thematic for PUR with Argentine lithium projects likely to benefit from Chile’s nationalisation plan.

The lithium heavyweights are already putting their money behind the Argentinian lithium industry:

- Posco Holdings (capped at ~$36BN) - Investing US$830M into a lithium hydroxide plant and committing up to US$4BN in investments in Argentina.

- Rio Tinto (capped at $156BN) - Paid US$830M for lithium projects in Argentina.

- Gangfeng Lithium (capped at ~$26BN) - China's largest lithium producer paid US$962M for its projects in Argentina.

And this headline from Bloomberg summarises the region's potential perfectly:

PUR is at the right place at the right time, in a region where lithium resources are known to exist, but the lithium industry is still in its infancy.

We hope that by de-risking its project and bringing it closer to development, PUR re-rates to a company with a market cap in excess of $1BN and attracts the attention of major players in the region.

What’s next?

Permitting for the upcoming exploration program 🔄

In its March quarterly PUR confirmed permitting for the TEM (transient electromagnetic) surveys had been approved.

Permitting for the company’s drill program is still ongoing.

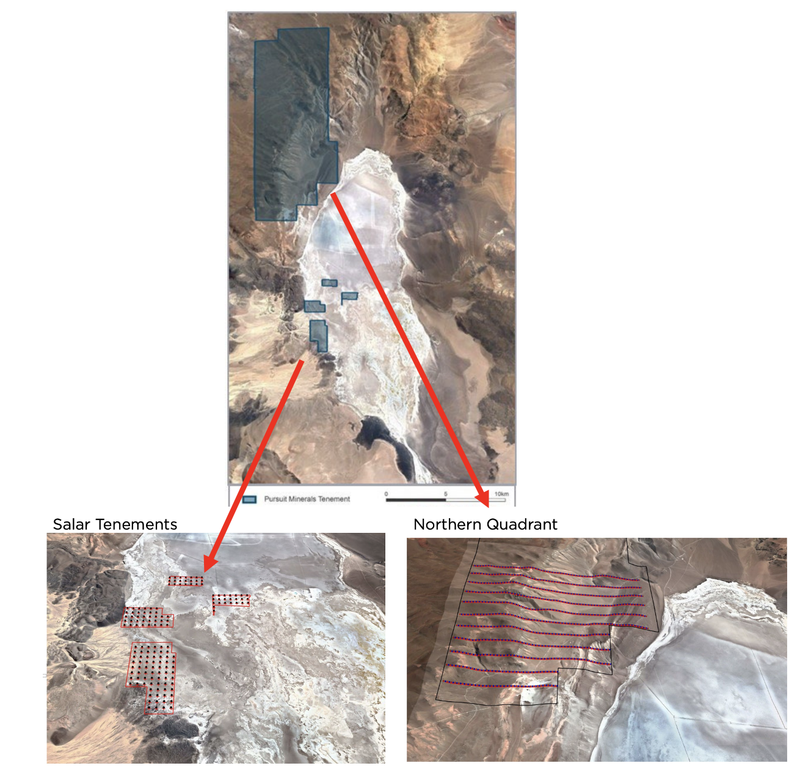

TEM/CSAMT surveys 🔄

PUR is looking to start geophysical surveys across its ground in May.

CSAMT stands for “Controlled source Audio-frequency Magnetotellurics” - a type of geophysical survey.

Ultimately the geophysical data will be used to identify the highest priority drill targets that PUR plans to drill test later this year.

Below is where PUR plans on running this program:

What are the risks?

In the short term, the main risks involve “market risk” and “commodity pricing risk”.

Recent turbulence in the lithium price coupled with negative market sentiment may put pressure on PUR’s share price.

In the long run, exploration and commercialisation risks will be more relevant.

You can see more on the key risks in our Investment Memo:

Our PUR Investment Memo

Along with the key risks, our PUR Investment Memo provides a short, high-level summary of our reasons for Investing.

The Investment Memo details:

- Key objectives we want to see PUR achieve

- Why we Invested in PUR

- What are the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.