First deal for ONE’s new mobile product. Baxter relationship now "Internet official".

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,569,333 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

Two things we have noticed from our health tech Investment and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) over the last week...

And neither have been announced to the ASX...

First, a very quick background:

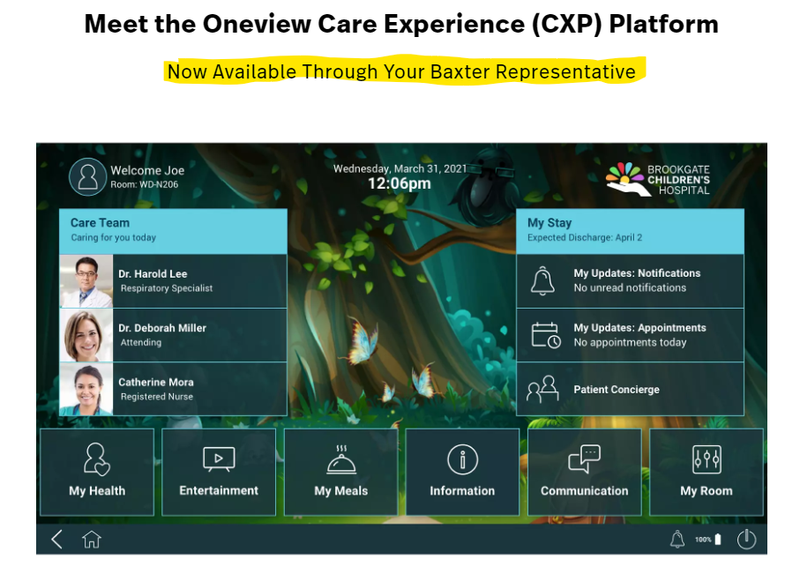

ONE’s technology connects a patient in a hospital bed to nurses, meal service, medical images and records, educational content, entertainment and other in room systems to help make the hospital run better.

ONE sells its technology to hospitals and other healthcare facilities and has built up a recurring annual revenue model.

ONE’s technology is normally delivered via bedside tablet and/or TV screen:

But at the start of the year, ONE launched a “bring your own device” (“BYOD”) solution - called “MyStay Mobile”.

Patients can now use the ONE technology on their own mobile phone during their hospital stay:

And if the patient brings their own device, it makes it easier for hospitals to purchase and roll out ONE’s technology, because they don’t have to buy and install bedside tablets or upgrade their existing in-room TVs.

A great new concept and product launch, it sounds obvious and logical...

But will hospitals adopt and use it?

NEWS ITEM 1: Today we saw a press release from ONE announcing that the first hospital is using MyStay Mobile

This morning we saw a ONE press release announcing that the first hospital will be using MyStay Mobile - this was not released as an ASX announcement, but we think its a significant event:

(Source)

This new signed agreement is with Children's Health of Orange County (CHOC) which is a prestigious 334 bed children’s hospital in Southern California.

The hospital is about to become part of a bigger entity after the parent companies of Children’s Hospital of Orange County (CHOC) and another children’s hospital in San Diego announced an agreement in December to merge under the new banner of Rady Children’s Health. (Source)

While there was no total “contracted bed” count attached to ONE’s press release, we believe there is an opportunity for ONE to sell to a large number of beds into this new, larger entity.

Hospitals are notoriously slow to adopt new tech, so to get MyStay Mobile into such a prominent hospital so soon after launch is a big achievement.

If ONE impresses CHOC with MyStay, it could lead to a post merger opportunity across the combined two hospitals.

Most importantly, this is a valuable case study for other hospitals and a chance to learn and refine the product in a real world situation.

If MyStay Mobile continues to gain traction:

1. Could unlock rapid growth of recurring annual revenue

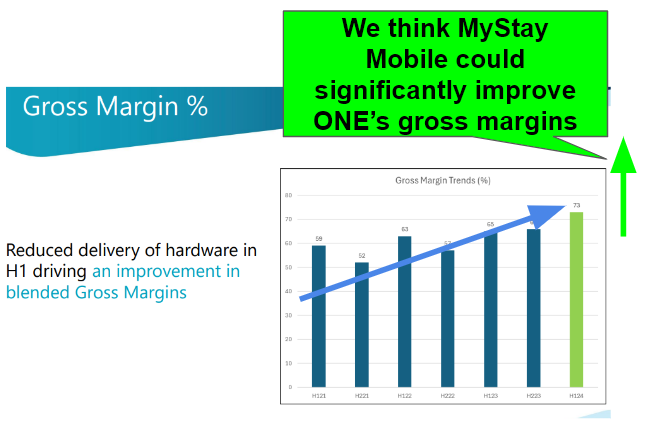

2. Potential to significantly increase gross margins (important for profitability)

(Gross margin is the percentage of a company's revenue that's retained after direct expenses such as labour and materials have been subtracted.)

We want to see ONE move quickly towards profitability, and higher gross margins due to less need for hardware should feed through to ONE’s bottom line over time as MyStay uptake increases:

3. Dramatically reduce friction in sales pipeline (quicker sales, faster uptake)

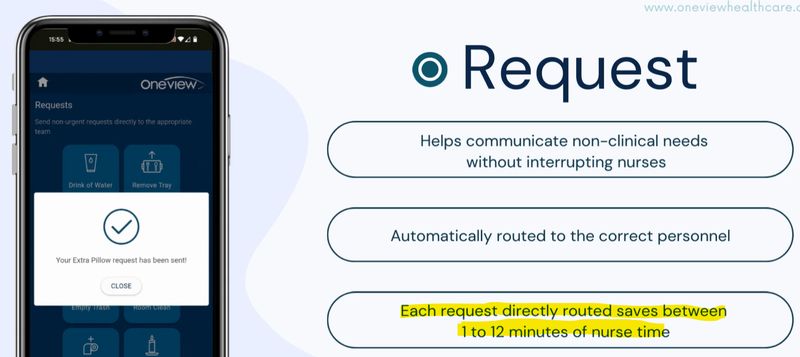

And aside from a dramatically improved patient experience, why do hospitals want to use MyStay Mobile?

Well, each request on MyStay saves nurses anywhere from 1 to 12 minutes:

(Source - MyStay Mobile Demonstration Video)

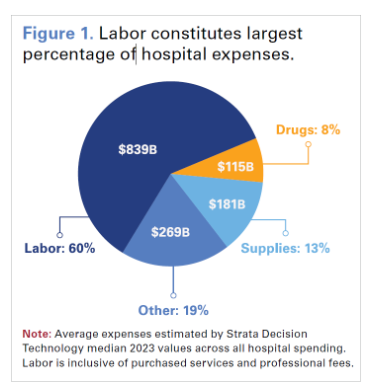

Labour costs now make up 60% of US hospital expenses:

(Source)

US hospitals are under immense financial pressure, and every minute of saved nurse labour cost is, as a result, very important to the ongoing financial viability of these hospitals.

MyStay could prove to be a great quick win for US hospitals, and ONE as well.

If ONE can deliver further traction with MyStay Mobile, it promises to rapidly accelerate ONE’s revenue growth - we are watching for more updates on MyStay Mobile traction.

Read more about ONE’s MyStay in this note:

Baxter is Coming... and so is BYOD.

The second “unannounced” development we noticed is...

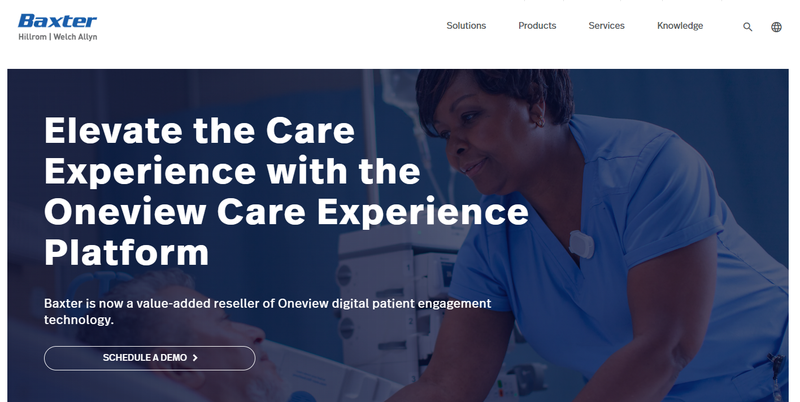

NEWS ITEM 2: US$20BN hospital supplier Baxter is now featuring ONE’s tech offering prominently on its website

NYSE listed Baxter International is a US$20BN capped US (and global) hospital supply giant which sells an enormous range of medical products to hospitals.

This includes hospital beds, after Baxter closed an acquisition of hospital bed maker Hillrom for US$10.5BN in 2021.

In November 2023 ONE signed a value-added reseller (VAR) agreement with Baxter, allowing Baxter to sell ONE's products to its vast hospital customer base.

We want to see ONE increase its market share in the US and Baxter controls up to ~75% of the hospital bed market in the USA.

But a value reseller agreement is only impactful if the reseller is engaged and starts “moving units”.

This week we saw the strong signs of Baxter’s commitment to promote ONE products as a value add to their large existing product range.

Baxter now features ONE’s technology offering on its website:

(it’s like somebody with a lot of social media followers finally posting a photo of their new boyfriend/girlfriend... only happens once things are starting to get serious...)

(Source)

We believe this partnership will significantly increase ONE's sales velocity and market penetration, potentially reaching some of the ~500,000 hospital beds in Baxter's network.

The Baxter website saw a strong sign of ONE’s products nicely, and directs visitors to contact their Baxter representative:

(Source)

Baxter's USA sales team consists of over 50 members, who have all been trained on how to sell ONE’s products, so we think Baxter has the necessary resources to sell ONE’s product effectively.

Baxter has already delivered two deals:

(Source)

And we want to see more material deals come through ONE’s Baxter value added reseller agreement in the near term.

Our ONE Big Bet

“ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1BN valuation (based on 5x to 10x forward annual recurring revenue) and be acquired by a large health tech provider.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

OneView Healthcare

ASX:ONE

How does this impact our ONE Investment Memo?

We see today’s signed agreement with Children’s Hospital of Orange County as reducing technology risk for ONE slightly, as the product is now about to generate its first revenues.

The fact a prestigious children’s hospital is willing to commit funds to the technology validates its value, and shows ONE’s strategy to develop this product was the right idea.

Technology risk

ONE will need to add functionality to its products over time as the health tech industry advances. The BYOD rollout may not go as planned.

Also, ONE has flagged that a range of additional features are in the pipeline, and the successful roll out of these features could help it reduce this particular risk as hospitals become more advanced.

Source: 22 September 2023 ONE Investment Memo

While no bed count was mentioned in the agreement, the hospital has 334 beds and we expect this agreement to eventually result in a material contribution to our #1 Objective for ONE:

Objective #1: Repeat sales success and hit 25,000 beds

For ONE, ‘contracted beds’ is like an ‘active user’ metric for a tech company. We think this is the basis for judging ONE’s success.

More contracted beds = more revenue.

Building on ONE’s previous 15,000 bed achievement, we want to see ONE hit a total of 25,000 in CY2024, primarily out of the USA.

ONE is projecting growth of 20-25% across this metric in FY23 excluding the potential beds from the Baxter agreement and BYOD solution.

Source: 22 September 2023 ONE Investment Memo

What are the risks for ONE right now?

The three risks we are most conscious of right now are sales risk, distribution partner risk and funding risk.

Sales Risk

Despite a strong customer retention rate and the endorsement of the product by prestigious hospitals, ONE could lose key clients or not seal as many deals, hurting their revenue and share price.

Large institutions like hospitals don’t tend to adopt new technology very often and the sales cycle can be long. This feature of ONE’s customer base can cause delays in sales that drag out over a long time.

Macro factors in the market including a recession can cause a reduction in spending on new technology, affecting ONE’s ability to make sales.

Source: 22 September 2023 ONE Investment Memo

Distribution partner risk

A key part of ONE’s strategy is to sell its products through a distribution partner like Baxter, Microsoft or Samsung.

Although ONE has a strong relationship with these companies, if they move slowly - or don’t prioritise ONE’s products when making a sale - then it could reduce the sales outcomes for ONE.

Source: 22 September 2023 ONE Investment Memo

We’re awaiting a new major Baxter deal, but this may take longer to materialise than expected.

Funding Risk

Although ONE raised $22.8M in July 2023, growth companies need cash to achieve their goals. If ONE doesn’t use the money from this raise wisely, then share price pain could follow. This was ONE’s fourth capital raise since it listed in 2016.

Source: 22 September 2023 ONE Investment Memo

As of the latest half yearly results, ONE has a cash balance of ~€6.0M (~$9.8M). If this continues to fall as ONE can’t make quick enough progress to breakeven, then a capital raise may be required at some point in the future.

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE

- Why we Invested in ONE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.