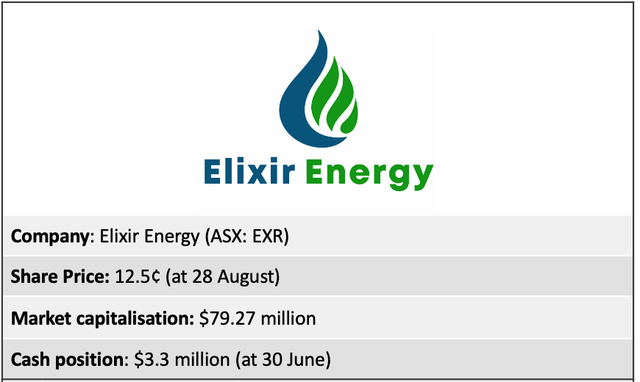

EXR’s Nomgon-2 Gas Well Exceeds Expectations

Elixir Energy (ASX:EXR) has been a recent standout performer in the ASX energy space and it’s run looks set to continue.

The company reported impressive gas content and permeability results from its 100%-owned coal seam gas (CSG) Production Sharing Contract (PSC) on the Mongolia-China border.

After achieving Mongolia’s first ever gas discovery in February at the Nomgon-1 well, EXR rapidly followed up with the Nomgon-2 appraisal well that “exceeded our expectations on multiple fronts”, says EXR managing director Neil Young.

Gas content results came in almost identical to those from the Nomgon-1 well, averaging more than 5 cubic metres per tonne (raw).

Furthermore, down-hole permeability tests produced “significantly better results” at the follow up Nomgon-2 well than at Nomgon-1. Both wells encountered exceptionally thick coals.

The most recent well – the low cost Nomgon-S3 strat-hole has also encountered thick coals in the sub-basin.

Together, the results from the three wells point to an exceptionally thick and gassy coals across a number of square kilometres, while also suggesting a broader areal extent in the broader Nomgon sub-basin.

The data will expand EXR’s contingent resource base at the PSC’s Nomgon sub-basin — targeted for year’s end. This will provide a basis for what could be a very modestly costed pilot production test in 2021.

Initial success in the Nomgon sub-basin also de-risks exploration across the broader PSC area.

We spoke to Neil Young to get his take on the Nomgon-2 results and what they mean for the PSC.

LISTEN NOW:

In the lead up to the Nomgon-2 results, the stock was up three-fold in just a month as shareholders awaited these latest CSG (also known as coalbed methane “CBM”) drilling results.

The share price jumped sharply on news of the CSG discovery at the Nomgon-1 well in February. But it was almost immediately dragged lower as the market dropped in March in response to COVID and a crash in oil prices.

With that backdrop, the current run includes not only anticipation around the exploration results and EXR’s future plans at the PSC — including further exploration and potential offtake and/or farmouts, but the ongoing recognition of the significance of the gas discovery at Nomgon-1.

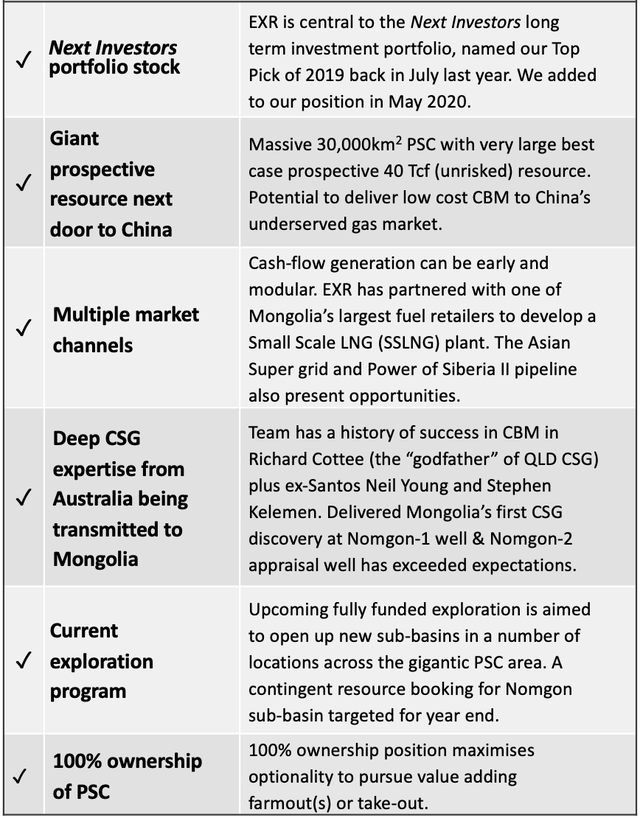

Here at Next Investors we are long term shareholders of EXR, naming it our ‘Pick of the Year’ in July 2019 and doubling down on our investment in May.

That decision has paid off: Elixir has more than doubled since we named it our Pick of the Year, while it is up almost 500% since we increased our shareholding.

That investment is clearly paying off given the recent price action, yet we are looking further ahead, eyeing the longer-term potential of Elixir’s 30,000km2 (7 million acre) landholding.

The company is proving up the wider potential in its vast PSC block, with plans to ultimately bring in high quality partners who can help bring a very large potential resource into production.

EXR will first commence a geographically vast exploration program with a low cost strat-hole drilling campaign across its gigantic landholding that lies over the major Permian coal-bearing region.

In addition to the Nomgon sub-basin, the gigantic licence area — the size of “a small European country” — likely hosts numerous coal-bearing sub-basins that are prospective for coal seam gas.

In the short soundclip below, Young explains the overarching opportunity.

Young spent nearly a decade securing the gigantic 30,000km2 (7 million acre) PSC area, which has a giant independently certified un-risked best case prospective resource of 40 Tcf CBM and is likely to host numerous coal-bearing sub-basins.

EXR was the first company to ever secure a coalbed methane PSC in Mongolia and this year made the country’s first ever gas discovery.

It has all the required government approvals and permits to start intensive exploration to increase the resource size and it remains fully funded for exploration, having recently completed a heavily oversubscribed capital raising. The fact that CSG exploration is much less capital intensive than other forms of petroleum exploration also helps project economics.

Nomgon sub-basin discovery

Elixir’s first year exploration program at the Nomgon IX PSC culminated in the February 2020 announcement of Mongolia’s first ever coal seam gas discovery at the Nomgon-1 well.

The current 2020 exploration campaign involves follow up appraisal drilling in the Nomgon sub-basin, plus exploration orientated seismic acquisition and drilling elsewhere in the large PSC area.

The campaign expands on the earlier gas discovery, with the information gleaned to be collated, analysed and corroborated to book an independently verified contingent resource for the Nomgon sub-basin.

After calling total depth of the Nomgon-2 core-hole at 550 metres in July, EXR reported various results from the well — and they have exceeded expectations.

The gas content readings from the main “100 series” seam (measured between 414 to 479 metres) are nearly identical to the strong figures delivered earlier this year from the Nomgon-1 discovery well.

The average gas raw gas content was 5.3 cubic metres per tonne, in an overall range of 3.4 to 7.4 m3/tonne (from 38 desorbed samples).

This compares to the average (raw) gas content from Nomgon-1 of >5m3/t that were measured in a very thick coal seam — which we now know is fully gas saturated.

The average gas content (DAF) figure from Nomgon-1 post well analysis included an of 8.9 m3/t for “100” series coals. By way of comparison, Galilee Energy’s flagship Glenaras gas project in Queensland’s Galilee Basin has a reported DAF gas content of 5.3 m3/t.

The higher final “dry ash free” (DAF) numbers from Nomgon-2 will be advised in due course.

If final figures from Nomgon-2 are anything like Nomgon-1 — which EXR is confident of — its DAF figures will also compare very well with CSG projects globally.

Permeability testing

Six separate down-hole permeability tests have been successfully run at Nomgon-2, with a combination of the company’s Mongolian sub-contractors, on-site expat supervision and on-line oversight from Australia delivering a highly effective process.

The six tests were run using an injectivity fall off test (IFOT) process. Four of these were ran across the main 100 series seam.

These tests have produced significantly better results than Nomgon-1.

Results ranged from 19.7 to 640.3 millidarcy metres (mD.m) — significantly better than those recorded at Nomgon-1. However, the three down-hole permeability tests at Nomgon-1 were successfully conducted and were analogous to that reported from producing fields in certain parts of Queensland’s Bowen and Surat Basins and various basins in China.

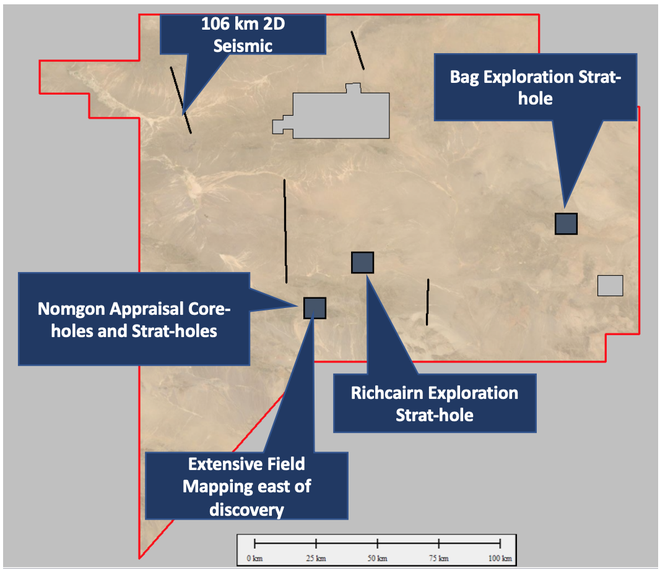

Strat-holes

The Nomgon-S3 appraisal strat-hole recently reached a total depth of 644 metres. Net coals of ~78 metres have been logged.

EXR confirm that the prime objective of this well has been met or exceeded, confirming the presence of coals in the Northern limb of the Nomgon syncline.

The well also intersected significant coal seams below the primary target '100 series' — the first time such seams have been intersected in the region.

This data is important for the planned future contingent resource booking.

The Nomgon-S4 appraisal strat-hole will spud shortly. A key objective of this well is to continue to confirm the presence of coal in the Nomgon sub-basin, this time stepping out to the East of Nomgon-2.

Exploration drilling will follow Nomgon-S4 in a number of different locations across the 30,000 km2 PSC, with a view to opening up potential new coal seam gas bearing sub-basins.

Seismic program complete

Elixir’s 2020 2D seismic program has now finished its field acquisition stage with a total of 106 kilometres successfully acquired.

Processing has commenced, with early stage targets already indicated in multiple areas.

Final interpreted results are expected in around early September. These, together with the 2019 seismic results and field mapping work (which is ongoing), will feed into the ultimate well selection process for the exploration drilling campaign.

Work ahead

The Nomgon sub-basin appraisal plan is now moving into a desk-top petroleum engineering phase, with a primary focus on designing a pilot production test for 2021.

EXR is assembling a very positive data set that should not only expand its contingent resource base but also provide a basis what could be a very modestly costed pilot production test in 2021.

Prior to this, EXR has a geographically vast exploration program coming up very shortly, which will target multiple potential new CBM hosting sub-basins with a low cost strat-hole drilling campaign.

New, potentially CSG bearing targets have been identified in various locations across the PSC, supporting the view that the exceptionally large licence area is likely to host numerous coal-bearing sub-basins that are prospective for coal seam gas.

A number of these set to be drilled immediately after the current appraisal program.

Well locations will be determined post the current 2D seismic program and will incorporate the findings of both of the 2019 and 2020 seismic programs and more recent field work.

EXR will remain highly active in the field right through to the end of 2020. This intensive work program is fully funded with a view to a contingent resource booking.

Given the low capital intensive nature of CSG exploration compared to other forms of petroleum exploration, EXR don’t anticipate any issues with funding exploration.

The positive exploration results to date create options over a future farm-out campaign, but given the low cost of exploration, EXR is not reliant on a larger partner to further progress the project.

Even at this early stage, EXR has secured its first offtake partnership with one of Mongolia’s largest fuel retailers — a small scale LNG project targeting the massive coal trucking fleet in the region. Young has also already fielded numerous calls from parties interested in getting involved, including some recognisable multinationals.

Management is aiming to conduct a pilot production testing 2021, where production testing should be characterised by early gas production, and being fully gas saturated coals, a lengthy water producing phase is not required to induce pressure draw-down and gas breakthrough.

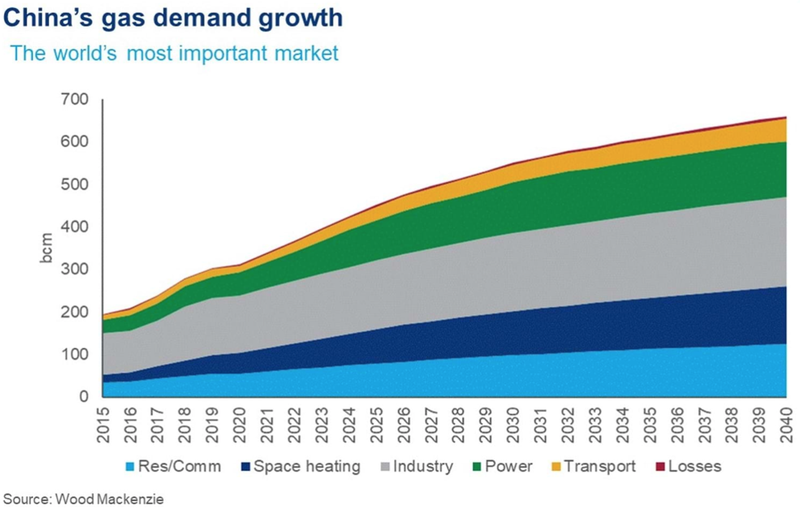

Chinese gas demand

Elixir’s 100% owned Nomgon IX CBM PSC has an independently assessed 40 trillion cubic feet best case estimate, unrisked, recoverable gas resource on China’s doorstep — a country that, according to Wood Mackenzie, is the engine of global gas growth.

The global research group report that amidst the chaos of the pandemic, China’s gas demand has exceeded expectations.

The country’s economy has proven surprisingly resilient and energy demand remains high, but the impressive growth of the Chinese gas market can in part be explained by the previous relatively low share of gas in the overall energy mix.

As part of President Xi Jinping’s pledge to protect the environment, China has moved millions of homes and businesses from coal to cleaner-burning natural gas. Additionally, China’s vehicle fleet now includes more than eight million gas fired vehicles — a figure that is still growing rapidly.

Even amidst the chaos of the COVID-19 pandemic, the country’s gas demand exceeded expectations, with demand particularly strong from the industrial sector.

Largely driven by environmental concerns around the burning of coal, forecast growth in Chinese gas demand plays well for EXR.

Along with rising gas demand from China helping EXR’s project economics, so is higher gas prices, as discussed in the following video...

Regional pipeline development

China’s transition to gas has been hampered at times by a lack of infrastructure — gas supplies still run short, especially in winter when demand peaks.

To help meet its growing energy needs and clear its dirty air, Xi is taking steps to expand the country’s gas network and diversify energy supply.

Under his leadership, China has spun off the tens of thousands of miles of pipelines held by state-owned oil and gas giants, including US$56 billion of PetroChina and Sinopec assets, consolidating them into a new state-owned company, PipeChina.

In the West, the consolidation of assets and state ownership doesn’t often point to efficiencies. However, the creation of PipeChina is part of Xi’s strategy to enhance the efficiency of China’s oil and gas resources and ensure safe and stable energy supply.

This makes sense if you are aware that PetroChina, which accounted for 60% of China's natural gas production last year, has historically prioritised its own pipeline needs ahead of those of its rivals, especially those that do not own pipelines.

Splitting up vertically integrated structures and providing open access occurred in the likes of the USA and Australia a few decades ago and is considered a key enabler of more efficient markets and increased gas demand.

By ensuring open access to pipeline transport to fully utilise its transmission capacity, China will encourage local gas exploration and multiple sources of supply by improving third-party access to infrastructure that’s essential to serve customers.

The idea behind placing its pipelines under one umbrella company is to raise the allocation efficiency of China’s oil and gas resources and ensure safe and stable energy supply.

This development could prove particularly beneficial for EXR.

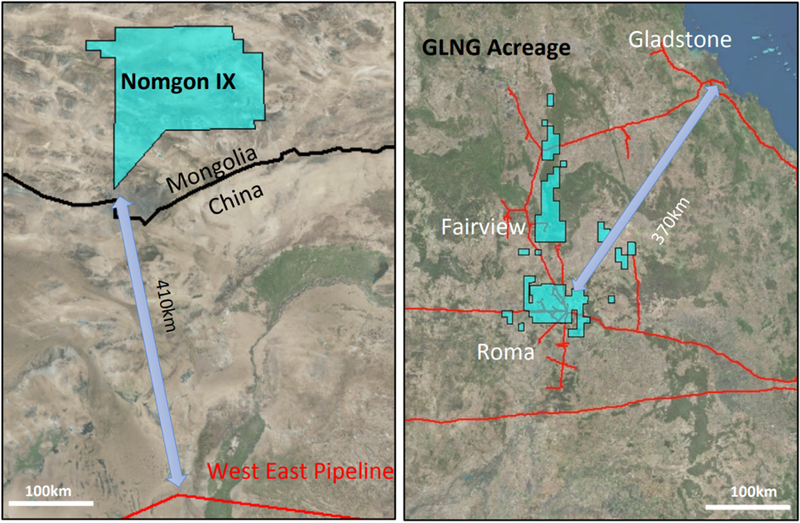

Given that EXR’s 30,000km2 Nomgon IX PSC is located on the Mongolia-China border, the company is well placed to help meet this demand — as highlighted in the following articles:

Santos chief executive Kevin Gallagher has also recently recognised that developing gas closer to where it's needed by users “is always going to be a lower-cost option”.

Located on the Chinese-Mongolian border, Elixir’s Nomgon IX PSC is just 410km from China’s existing East-West Pipeline.

By way of comparision, transporting gas from the PSC to China’s East-West Pipeline is almost exactly the distance that gas from Santos’s GLNG licences in Queensland travels to reach the Gladstone LNG port.

It’s a “very simple exercise” says Young, who was formerly part of the Santos Business Development team that assembled the assets that now supply Gladstone LNG.

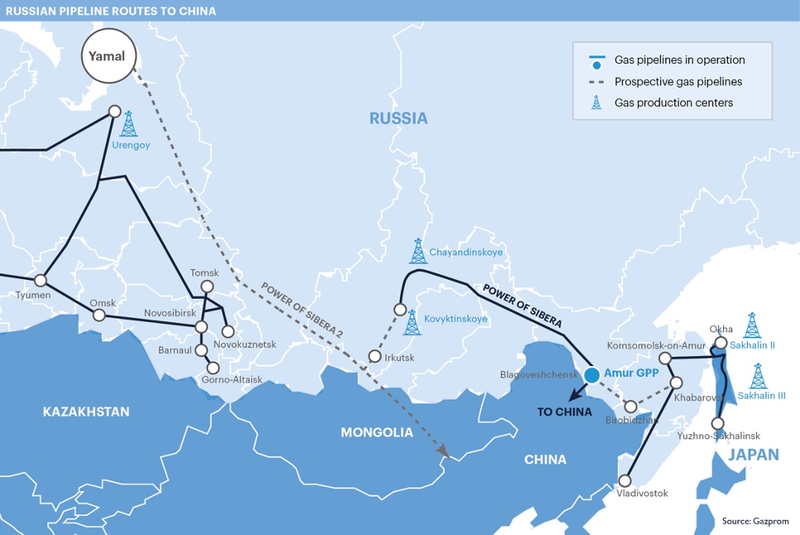

Power of Siberia 2

Following a March meeting between Gazprom Chair Alexei Miller and Russian President Vladimir Putin, design and survey work on the Power of Siberia-2 gas pipeline has begun.

The pipeline could become the basis of a new gas export channel through Mongolia to China with preliminary technical and economic analysis suggesting a capacity of up to 50 billion cubic meters (~1,750 PJ) of gas per year.

Fast economic recovery in China post COVID-19 and the country’s growing appetite for natural gas might in fact speed up the realisation of Power of Siberia 2.

Here’s you can see the proposed pipeline path running past EXR’s PSC in Mongolia:

Market opportunities

Multiple market opportunities exist for Nomgon PSC gas, in addition to the clear need for gas supply to China.

Existing large-scale electricity transmission runs through the PSC area that has large spare capacity, while Mongolia’s grid needs new power sources particularly to power local mining operations.

Inside the PSC’s borders, but excluded from the agreement, is one of the largest coal deposits in the world, the government owned Tavan Tolgoi coal mine. Also within the PSC is the Rio Tinto operated Oyu Tolgoi copper/gold mine, the largest user of power in Mongolia that is seeking new local power generation to replace Chinese imports.

Further, numerous Small Scale LNG (SSLNG) plants could be established to supply the region’s large coal trucking fleets.

EXR has already signed an MoU with MT Group, one of Mongolia’s largest fuel retailers, over the possible development of a Small Scale LNG (SSLNG) plant.

Mongolia itself is another major market for EXR’s gas. The country relies on coal for 90% of its electricity production and air pollution is a significant public health problem particularly in the capital, Ulaanbaatar.

The country has been extremely supportive of the proposed Asian Super Grid — a massive system of proposed interconnected electricity grids across north-eastern Asia and through the Gobi region that allows for the exchange of power from renewable and other clean energy resources like solar, wind, and hydro (and gas) across the continent.

EXR: looking ahead

Elixir Energy is a company that first came onto our radar in November 2018, after which we named it our Pick of the Year in July 2019.

Here at Next Investors, we conduct a significant amount of due diligence prior to us making an investment.

What initially attracted us to Elixir was the exceptional potential of its prospective CSG assets and its proximity to the fast-growing Chinese gas market.

Getting to know the management team — particularly managing director Neil Young, who has been operating in Mongolia since 2011 — has been a major source of confidence for us and our decision to make a large investment in the company, which we doubled down on in May.

Now, after many discussions with Young and seeing the company’s progress to date, we are increasingly impressed with EXR and its prospects going forward.

The current appraisal process works to de-risk the project, providing comfort to parties interested in subsequent farm-out negotiations with EXR. The company plan to book an independent contingent resource by the year end will greatly enhance its farm-out options.

The project’s scale, its proximity to a gas hungry China, plus EXR’s exploration results to date and its 100% ownership, suggests that the company has what it takes to attract high quality farm out partners and /or acquirer in the future.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.