Early signs of a small cap recovery?

Published 24-MAY-2025 12:24 P.M.

|

11 minute read

Commentary: A share price moving catalyst next week? Uranium stocks running on Trump rumours. More and more resources M&A...

A big share price catalyst coming in the next week?

Uranium stocks running on rumours of a Trump Executive Order to boost the nuclear industry?

More and more acquisitions in the resources space putting cash into the pockets of investors?

Will they cycle it into smaller resource stocks?

(more on all these in a second)

The mood in the small end feels like it's improving.

An interest rate cut this week helped.

And there doesn’t seem to be much “sell in May” selling this year.

After 3 horror years in the small end, anyone who was planning (or needed) to sell... is probably already long gone.

Plus gold is moving back towards its all time highs...

Silver looks great too.

All of this aside, we all just want our stocks to go up.

“Share price catalysts” are a big part of investing in pre-revenue micro-caps.

A “catalyst” is a major news release made by a company that can have significant positive OR negative implications for the company's business and share price.

Depending on if the major news released is good... or bad.

Investing just before a catalyst is expected to be announced can be quite risky...

But in the case of our newest biotech investment Island Pharmaceuticals (ASX:ILA) we are making a calculated “roll of the dice”.

(we have identified and accepted the risks and it fits our risk-reward profile - including the second order risk-reward of looking like geniuses or idiots post the result)

This week, we added ILA to our Next Biotech Portfolio.

ILA is now just days away from Phase 2 clinical trial results for its lead drug for dengue fever.

(meaning we find out if ILA’s treatment is effective or not... pretty important)

Dengue fever impacts ~400M people a year.

And global dengue cases have been doubling every year since 2021.

ILA’s full phase 2a/2b trial results are “due by the end of this month”... which is next week.

In biotechs, exploration and oil & gas drilling, we generally like to Invest in companies with big catalysts coming well in advance of that catalyst becoming due.

Typically months and even years.

With ILA we took a slightly different approach, because we think there is a good chance of a positive result.

There is a risk that we are wrong of course, but here is our reasoning for the bet...

Back in November last year, ILA put out a readout of results from phase 2a of the trial.

Phase 2a of the trial was testing ILA’s drug as a PREVENTATIVE for dengue fever.

The data showed that ILA’s drug was safe, reduced viral load AND showed enough positive data for the Safety Review Committee “SRC” to recommend ILA go ahead with Phase 2b of the trial.

Phase 2b is testing to see if ILA’s drug is EFFECTIVE as a TREATMENT for dengue.

Importantly the SRC found:

- No safety concerns

- Blood levels hit “target concentration” of the drug (important to show that the drug was actually absorbed)

- Reduction in the dengue fever viral load in the phase 2a cohort

The market reacted well to those 2a results news back in November, pushing ILA’s share price up to 28c per share.

(nice share price spike, and looks like any loose stock wanting to come out took the opportunity)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The really important factor here is that phase 2a was actually testing ILA’s drug as a “preventative”.

Basically this means you take the tablets to stop you getting dengue - good for tourists visiting dengue prone countries OR people living in high risk dengue outbreak areas.

Similar to how you might take malaria tablets before traveling to remote locations.

This 2a trial tested if ILA could reduce the chances that a person gets dengue fever.

Phase 2b is trialling ILA’s drug as a “treatment” to see if it can be used on people who already have contracted dengue, to help the recover from it

A treatment could open up both market opportunities for ILA (as a preventative AND a treatment), giving the company optionality when it comes to designing its Phase 3 clinical trial.

(A Phase 3 trial is the final hurdle testing on a larger group of people, before the drug can be approved and sold into market)

On Tuesday, ILA’s CEO David Foster participated in a short interview where he provided an update on the clinical trial results, which are scheduled for the end of this month.

David Foster also mentions that he was roadshowing the product “in Singapore, Hong Kong, Australia and the US”...

And is currently in Brazil taking part in a pharmaceutical partnering conference.

(securing commercial partners to help sell your drug helped our biotech Investment DXB’s share price run over 1,000% - more detail on this here)

Over the past 12-months Brazil has had significant issues with dengue fever, so we think it is a good time for ILA to be preparing the pharmaceutical industry to pay attention to its trial results.

(Source)

If ILA announces some promising results from its Phase 2a/2b trial, we think that the stage is set for the company to surprise the market with a partnering/licensing deal for a larger Phase 3 trial.

(like DXB did)

Particularly due to rapidly rising dengue cases in some countries... like Brazil.

It all depends on the data, results and ILA’s ability to execute on a commercial deal.

No one can control the upcoming results of the 2a\2b trials, but in terms of getting a commercial deal done, we are backing the team behind ILA to deliver.

Two of ILA’s biggest shareholders and one of ILA’s directors were part of the Race Oncology team that took the company’s share price from ~6.6c to $4 per share:

- Dr Daniel Tillet -Tillet holds 6.72% of ILA. He was an early backer of Race Oncology (at 6.6c in 2019) and was Chief Scientific Officer when the company’s share price rallied to $4 per share.

- Dr William Garner - Garner holds 15.79% of ILA. He was one of the founders of Race Oncology.

- Chris Ntoumenopolous - Non-executive director of ILA. Chris was also a director of Race during that rally to $4 per share. Chris participated in the most recent ILA capital raise at 15c.

We also like that another biotech expert is a big backer here - Jason Carroll.

Carrol is currently the CEO of another ASX listed biotech company but he likes ILA enough to be talking about it in interviews and buying ILA shares on and off market...

He currently holds ~14.73% of ILA.

Read our ILA initiation note for the full 9 reasons why we are Invested in ILA

Uranium set for a big week with Trump executive order on the horizon?

On Friday the rumour mill was working in overdrive with whispers that Trump is set to announce a big executive order to boost the US nuclear industry.

(Source 1, Source 2, Source 3)

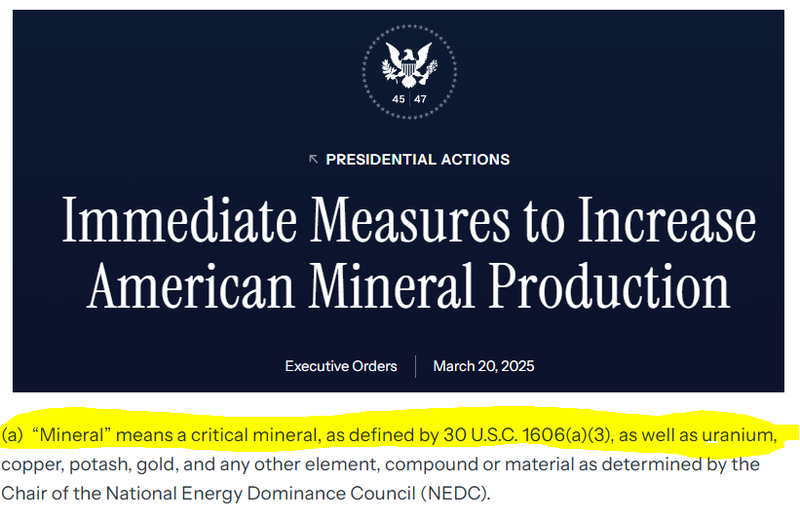

Despite being technically classified as a ‘fuel’, Trump has inserted “uranium” into the list of critical minerals needed for national security.

This was done in an Executive Order was signed in March, specifically mentioned uranium:

(Source)

Now, it looks like the Trump administration is targeting the nuclear fuel supply chain (uranium and uranium enrichment).

On Friday uranium stocks across the board started running...

(the Fin Rev reckons it might be a short squeeze?)

Five of the top 20 shorted stocks on the ASX are uranium stocks.

With Boss Energy and Paladin Energy being two of the most shorted stocks on the ASX:

IF Trump's Executive Order triggers a big run in the uranium price, we expect there to be a scramble to cover these shorts, pushing the price up for these large cap uranium stocks.

This could spark a much bigger short squeeze across the sector, the AFR cover this very well here:

(Source)

We have two US-based uranium Investments that we will be watching very closely next week...

Global Uranium and Enrichment (ASX:GUE)

GUE has a number of advanced stage uranium assets based in the US and Canada.

GUE is also the single biggest shareholder of Ubaryon - a private company working on uranium enrichment technology.

GUE has been busy recently, announcing:

- Acquisition of an asset in Wyoming on a 50-50 basis with JV partner (and now biggest shareholder of GUE) - NASDAQ listed Snow Lake Resources (read our full take on the deal).

- Scoping Study on its Tallahassee project with a US$280M NPV at a uranium price of $100 (read our take here).

- Investment in GUE uranium enrichment tech (via stake in Ubaryon) from Urenco (the second largest uranium enrichment company in the world) read our full take on the deal.

With US-based uranium in the spotlight, we think that GUE has set itself up nicely to take advantage of this increased attention on the sector.

GUE’s JV partner Snow Lake Resources has made big moves in the past day since rumours of Trump’s executive order began:

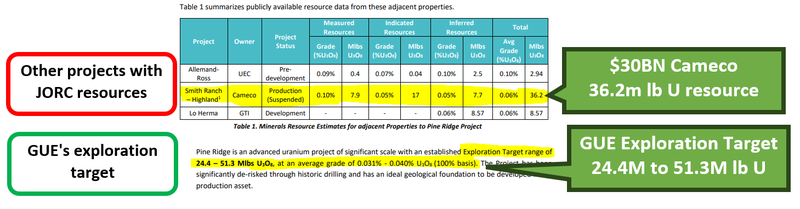

The project that GUE acquired in that deal sits just ~15km away from $35BN Cameco’s Smith Ranch asset.

Smith Ranch is where the USA’s largest permitted ISR uranium processing facility is located.

GUE’s asset right now, has an exploration target that IF converted into a JORC resource, could be bigger than Cameco’s...

(Source)

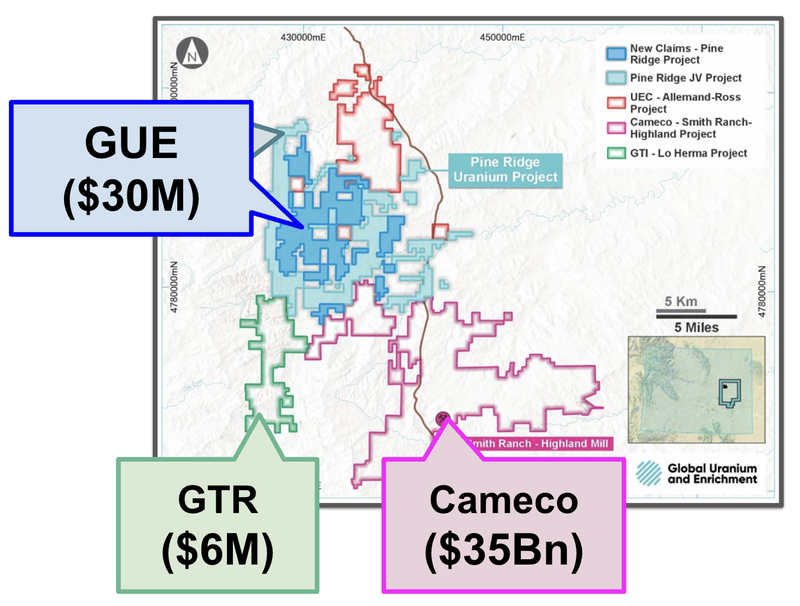

GTI Energy (ASX: GTR)

GTR has a 7.53Mt uranium JORC resource.

GTR is on track to complete a Scoping Study this quarter, which will give us an idea of the economic viability of its project.

GTR is also an ISR uranium play next door to both GUE and Cameco.

Here is where the three projects sit:

Both GTR and GUE are currently trading near their all time lows.

We think that any big spike in the uranium price and the positive momentum in the US could be what triggers a rally in both of their valuations.

More M&A is happening in the late-stage resource space

Another week, another big M&A deal in the midcap mining space.

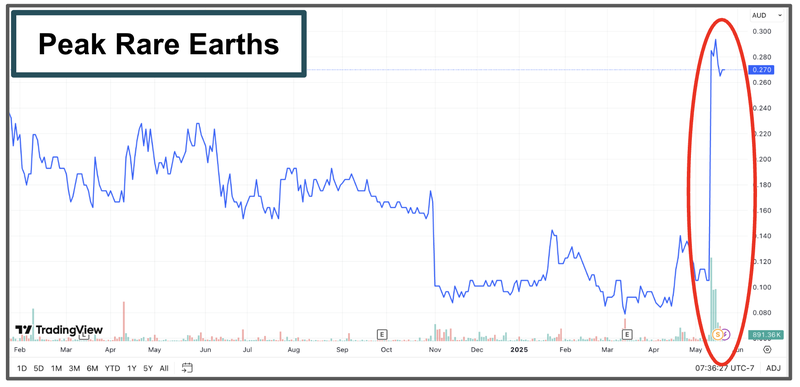

Last week, it was Peak Rare Earths.

(with an offer over 170% above the last traded price).

This week it was New World Resources, a US based copper developer which was trading at 1.6 cents per share a few months ago, but recently got a takeover offer of 5 cents per share.

And Xanadu Mines, which got a takeover offer at a 57% premium to the last traded price.

Here is how each of the shares traded for those companies before and after the takeover offers:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Consolidation in the mining space is important.

It gives institutional investors a way to exit positions without needing to develop the mine themselves.

These liquidity events then mean that there is more capital to roll back into the sector and chase the next big mine or discovery.

(not to mention money into the hands of any retail and high net worth individuals holding the stock too)

Right now we are in M&A season, as the valuation for advanced resources projects are currently at depressed levels.

While producers (particularly in the gold sector) are currently printing money and have excess capital to spend.

We think that the projects most ripe for M&A are those where the company is going through a “newsflow light” development stage.

The development stage can be a bit boring for some investors

Development takes a long time and there isn’t much scope for “blue sky” announcements to move the share price.

More likely you will get “development delays” or “cost overrun” announcements.

Many short term investors who were there for the “exciting” exploration and resource definition stage will eventually get bored and move on to the next stock.

And the share price drifts down.

For these reasons later stage development projects that are building a mine often trade at lower share prices.

UNTIL...

They either get taken over by a bigger company at a premium as we are seeing start happening.

OR

get close enough to completing their mine construction that the upcoming mine revenues attract new investors.

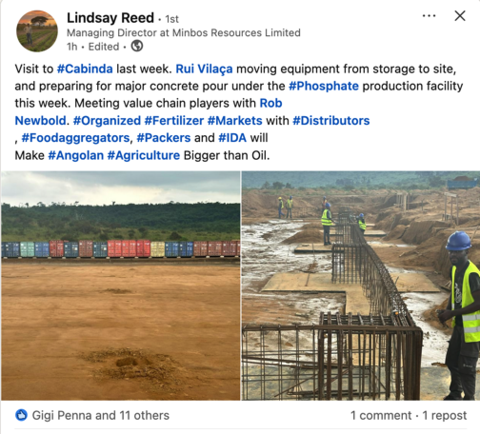

One company that fits the development stage description is our Investment Minbos Resources (ASX:MNB).

MNB is currently building its phosphate fertiliser project in Angola.

(Source)

(Source)

MNB has already sunk tens of millions of dollars into its project and is now in the early construction phase.

BUT the share price is at lows of ~4c.

Once MNB’s project is in production it is forecast to deliver ~US$55M in EBITDA per year, over a 20 year mine life (based on the company’s definitive feasibility study in 2022)

Despite being in construction, potentially only a year or two away from that scenario AND having made a lot of progress financing the project...

... MNB is only capped at ~$38M with $12.5M cash in the bank at 31 March 2025 and no debt drawn at the moment.

This sort of selling in advanced stage resource companies isn’t unique to MNB though which makes the sell offs a little more bearable...

We think there is definitely value in these advanced stage companies and are actively looking at new opportunities that fit that bill.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.