ILA: Our New Portfolio Addition

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,766,666 ILA Shares at the time of publishing this article. The Company has been engaged by ILA to share our commentary on the progress of our Investment in ILA over time.

Our newest Investment is Island Pharmaceuticals (ASX:ILA).

ILA is a small cap biotech stock targeting infectious diseases.

ILA’s first focus is developing a drug for dengue fever.

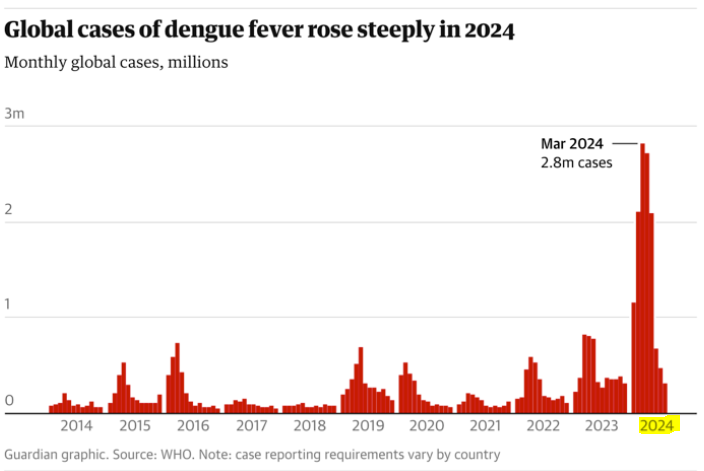

Globally, cases of dengue have doubled each year since 2021.

And seriously spiked upwards last year.

There is currently no specific treatment for dengue...

ILA is weeks away from a Phase 2a/2b trial result for its dengue fever drug.

(meaning its being tested on humans to prove if the treatment actually works)

We have been successful in Investing in biotech stocks in the past by following the lead of experienced doctors, scientists and biotech professionals in the space.

We watched a number of highly credible (and successful) biotech industry experts and seasoned biotech investors increasing their positions in ILA in recent months

(you can see it by watching change in substantial holding notices released via the ASX)

These same people all worked together on a different ASX biotech stock that delivered a 60x return to investors in recent years.

(using the same strategy as ILA, but targeting a different disease)

We can only assume they are chasing a similar kind of success, and understand the science, strategy, the potential of a drug and its commercial viability.

Further down the page we will share who they are, how many ILA shares they have been buying, and the similarities between ILA and their previous 60-bagger.

Aside from dengue fever, ILA is also working on “biodefense technology”...

A separate project developing treatments for weaponised viruses that can potentially be deployed in wars and conflicts...

... For viruses like Ebola, Marburg, Zika, and other RNA viruses - more on this later.

(yes, deploying weaponised viruses in war is a thing - the threat of “germ warfare” leads military/governments to stockpile anti-virals)

So we like the past success of ILA’s major shareholders, we like that they have been building their positions and ILA’s biodefense angle is very interesting.

Most importantly, we are just a few weeks away from finding out if ILA’s drug can prevent or treat dengue fever.

This is the major near term catalyst for ILA.

Dengue fever infects ~100-400 million people each year.

It kills ~40,000 people each year.

Half the world’s population is at risk of getting it.

No specific prevention OR treatment currently exists for this virus... and cases are rising sharply.

Globally, cases of dengue have doubled each year since 2021.

And really surged up last year...

(Source)

and appear to still be rising yet again in 2025 according to recent mainstream media headlines:

(Dengue is spread by mosquitoes, some experts reckon the warming global climate is creating increased livable temperatures for mosquitoes, leading to the recent surge in dengue)

The US government and the US military have acknowledged that dengue fever is a major health crisis too.

The US Department of Defence has supported ILA’s clinical trials through US$625k in grant funding.

With rising global temperatures, dengue cases increasing, and spreading to new parts of the planet, a proven treatment for dengue could save a lot of lives and help millions of people.

It' s also a multi-billion dollar opportunity.

But does ILA’s drug work?

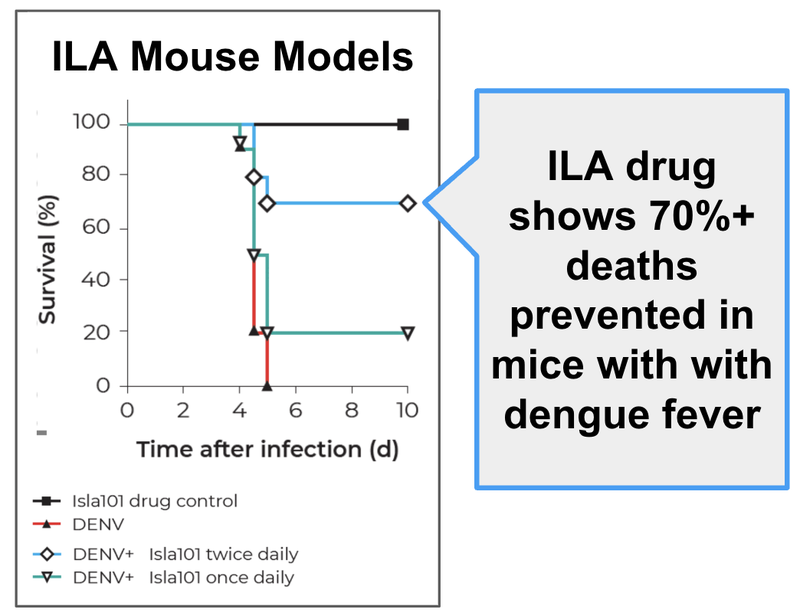

ILA’s pre-clinical data shows that it does...

And ILA’s major investors are betting big that it does...

Here’s the pre clinical trial chart that we think got them really interested in ILA:

ILA’s drug efficacy in humans will be validated in just A FEW WEEKS, with the unblinding of the results of the Phase 2a/b trial.

Is it risky Investing in a stock just weeks away from a “company making”, but potentially binary trial result?

Yes.

BUT

... IF successful, it could mean the ILA moves into a final clinical trial before its drug is ready for FDA approval.

ILA’s drug has already been extensively tested on humans in the past to try and treat other issues including cancer and respiratory diseases.

It’s been in over 40 Phase I, II and III human clinical trials for cancer and respiratory diseases AND has been deemed safe by regulators (see all previous fenretinide trial data here)

(Yes, ILA’s drug has ALREADY been through PHASE III trials and been deemed safe, just not in the context of dengue fever)

So we know it's generally safe, what we don't know (yet) is if it is effective at treating OR preventing dengue fever.

(but we find out in around two weeks, when ILA’s phase 2a/b clinical trial results are announced)

If ILA delivers a success here and eventually achieves FDA approval, ILA may be eligible to obtain a "Priority Review Voucher".

A Priority Review Voucher (PRV) could permit ILA to expedite the FDA approval process for a new drug or alternatively, ILA could sell the PRV in a secondary market.

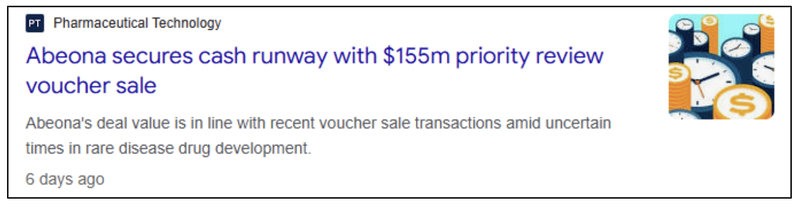

PRV’s are inherently valuable on their own because companies can sell them to other companies... On average they are selling for US$100M (A$156M).

The most recent sale only a week ago was for US$155M (A$241M).

(Source)

ILA is currently capped at $43M (post capital raise on a fully diluted basis).

ILA is our second new Investment for 2025.

And our first new biotech pick for the year.

Some of our best performers have been biotech stocks.

Here are their performances from our Initial Entry Price:

- Arovella Therapeutics, at its peak, has been up as high as 453%.

- Dimerix at its peak has been up as high as 292% - and it's up over 1,000% from its lows 18 months ago.

- Neurotech International at its peak has been up as high as 191%.

(Remember that the past performance of these stocks does not mean future portfolio additions will perform in a similar way. Caution should be exercised in assessing past performance. Stocks are subject to market forces and unpredictable events that may adversely affect future performance.)

A big part of our biotech selection process is following the lead of the right people - who have been there and done it before in the sector.

When it comes to the people backing ILA - it has one of the strongest shareholder registers (major shareholders) we have seen in a while...

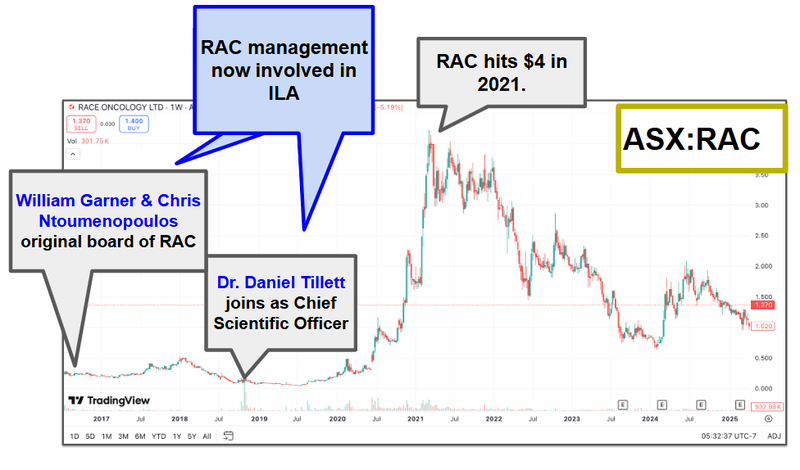

Two of ILA’s biggest shareholders and one of ILA’s directors were part of the Race Oncology team that took the company’s share price from ~6.6c to $4 per share.

(a 60x return from a 6.6c cap raise in 2019)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are basically following the Race team into ILA:

- Dr Daniel Tillet - Tillet holds 6.72% of ILA. He was an early backer of Race Oncology (at 6.6c in 2019) and was Chief Scientific Officer when the company’s share price rallied to $4 per share.

- Dr William Garner -Garner holds 15.79% of ILA. He was one of the founders of Race Oncology.

- Chris Ntoumenopolous - Non-executive director of ILA. Chris was also a director of Race during that rally to $4 per share. Chris participated in the most recent ILA capital raise at 15c.

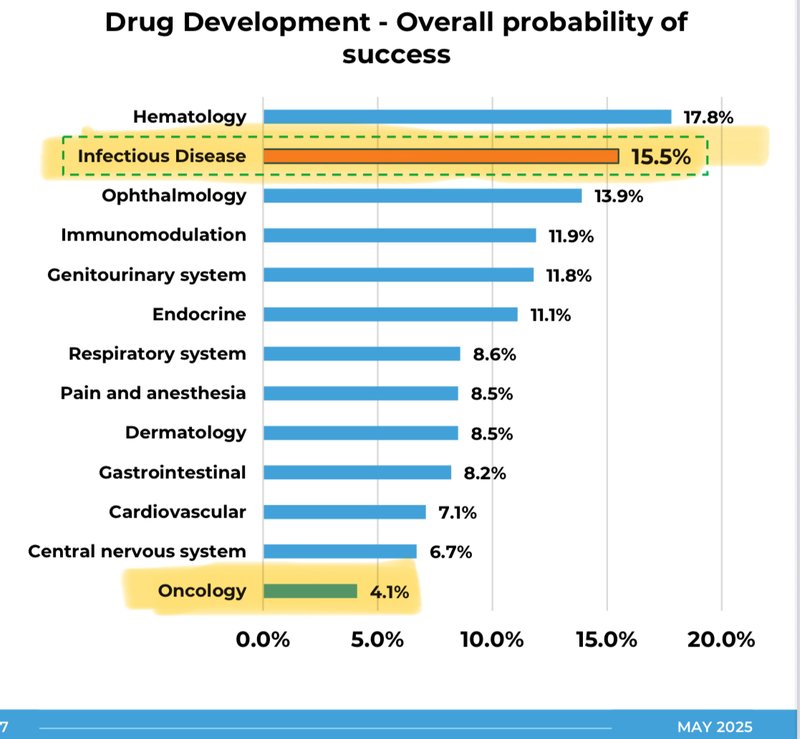

The success of Race Oncology was built on repurposing a drug, just like ILA is planning to do.

Race repurposed drugs for oncology whereas ILA is repurposing drugs for infectious diseases - where clinical trial success rates are almost 3x higher

(also meaning the ‘prize’ on success is smaller to reflect the lower degree of difficulty).

(Source)

Today we will be explaining the reasons for our Investment in ILA, and what we think the future might hold.

We will also be launching our ILA Investment Memo which will outline:

- What does ILA do?

- The macro theme for ILA

- Our ILA Big Bet

- What we want to see ILA achieve

- Why we are Invested in ILA

- The key risks to our Investment Thesis

- Our Investment Plan

Before we get to our Memo, here are the 9 reasons why we have Invested in ILA.

(the key risks we have identified and accepted with this Investment are in our Investment memo at the end of this article)

9 key reasons why we are Invested in ILA

1. Big addressable market - dengue infects up to 400M per year, kills ~ 40k

Infectious diseases are usually undertreated. ILA’s current focus is dengue fever which infects ~100-400M people and kills ~40k people per year.

The dengue fever treatment market is worth ~US$2.14BN and expected to grow to US$3.66BN by 20234.

2. Dengue fever cases are growing globally, but no specific treatment or preventative

Globally, cases of dengue have doubled each year since 2021, and nearly tripled in 2024.

In April last year there was an emergency declaration by the CDC about rampant dengue fever in South East Asia and South America.

The US government and the US military have acknowledged that dengue fever is a major health crisis too.

Given there is no treatment or preventative, outbreaks could have disastrous consequences for populations.

3. ILA is backed by the Race Oncology team (went from 6.6c to $4 per share - a 60 bagger)

Founder of Race Dr William Garner holds 15.79% of ILA. Previous Chief Scientific Officer of Race, Dr Daniel Tillet holds 6.72% of ILA and one of the founding directors of Race, Chris Ntoumpelous, is a non-executive director of ILA and participated in the recent placement at 15c

4. Dengue fever clinical trial catalyst due in the next few weeks

Phase 2a/b clinical trials have all been paid for and completed.

Results are due inside the next few weeks, a positive outcome here will de-risk the drug’s efficacy and provide an indication whether ILA’s drug works and if it is better as a preventative or as a treatment.

5. ILA could be eligible for “Priority Review Voucher” (PRV) - worth ~ US$100M

If ILA can get its drug FDA approved it could be eligible for a “Priority Review Voucher”.

A PRV means ILA can get its drug to market quicker. A PRV is transferable and has sold for on average ~US$100M (A$155M) in recent years.

If awarded, this PRV alone could be worth many multiples of ILA’s current market cap of ~$43M (fully diluted), ILA can choose to sell this PRV to raise a substantial amount of non-dilutive capital.

6. The active ingredient in ILA’s drug has already been proven safe in multiple clinical trials

ILA’s main drug candidate ISLA-101 has an active ingredient called fenretinide. There have been multiple clinical trials using this active ingredient for cancer and respiratory conditions in humans - providing a bounty of safety data for ILA.

This means that ILA has been able to ‘skip’ Phase 1 clinical trials as the important ‘safety’ hurdle has been de-risked (source - fenretinide data).

7. The US Government and the US Army both supported ILA’s clinical trials

The US government recently provided US$625k in grant funding for ILA’s clinical trial and the US Army provided clinical support under a CRADA (Cooperative Research and Development Agreement).

8. Possibility to expand drug to other infectious disease indications

IF ILA’s drug works for dengue fever, it could be applied to treat/prevent other infectious diseases like Zika, Yellow Fever and West Nile fever.

9. ILA to enter Biodefense space.

ILA has an exclusive option to acquire a drug that can be repurposed to tackle Ebola, Marburg, Zika - the kind of viruses that can be weaponised in war and conflicts.

This gives ILA potential exposure to the government/military anti-viral stockpiling thematic.

This drug could also be eligible for PRV and has animal data and human phase 1 safety data.

The rest of our Investment Memo is later in today’s email.

Before that, here is a quick overview on what ILA is targeting, what a priority review voucher is and why we think it's important for the ILA story and what we want to see next from ILA.

ILA could also become a biodefense “stockpiling” play

We Invested in ILA for its dengue fever drug.

BUT we also like that ILA is close to securing an exclusive option to acquire a drug called “Galidesivir” that is currently owned by US$2.1BN, NASDAQ listed BioCryst.

That drug has existing non-human data for Marburg disease and two Phase 1 safety studies.

Marburg is a severe disease with a fatality rate of up to 88% - it also has no specific treatment or vaccine at the moment.

The Soviet Union reportedly had a large biological weapons program enhancing the “usefulness” of the Marburg virus.

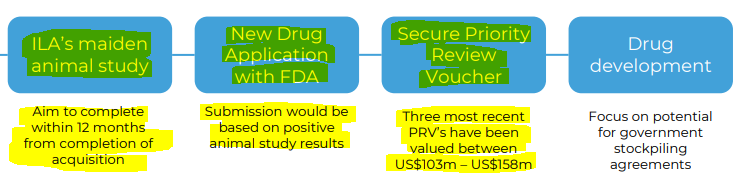

The upside for ILA here is that the drug it would be acquiring could be eligible for the FDA’s “animal rule”.

The animal rule is when drugs are approved by the FDA using animal data alone because running human trials are considered to be unethical OR non feasible.

The only thing that companies need to prove to be eligible is safety in human trials (which has already been shown) and efficacy in animals.

ILA currently has an option on this drug and could in theory acquire the drug, run animal studies and submit a new drug application with the FDA all within ~12 months.

(Source)

The big upside is that Galidesivir could make ILA a “stockpiling play”.

This is where the drug is of such interest and importance to public health that governments have a strong interest in stockpiling a reserve “in case of emergency”.

The best way to think about it is if we could have foreseen a big COVID outbreak in 2020 and the vaccine already existed, governments could have used their stockpile to prevent the spread of the outbreak.

This would have avoided all of the disruptions caused by the lockdowns and vaccine rollout.

OR even worse, in the event a bioweapon is used in war...

Governments wouldn’t be scrambling for a defensive vaccine/treatment.

ILA currently has a 12 month exclusive option to acquire Galidesivir starting in September 2024, so we expect to see some action on this inside the next ~four months.

Priority Review Voucher eligibility could be worth >US$100M

Drug development can take upwards of 10 years from pre-clinical through to FDA approvals and commercialisation.

ILA is in a position where its dengue fever drug could be eligible for something called a “Priority Review Voucher”.

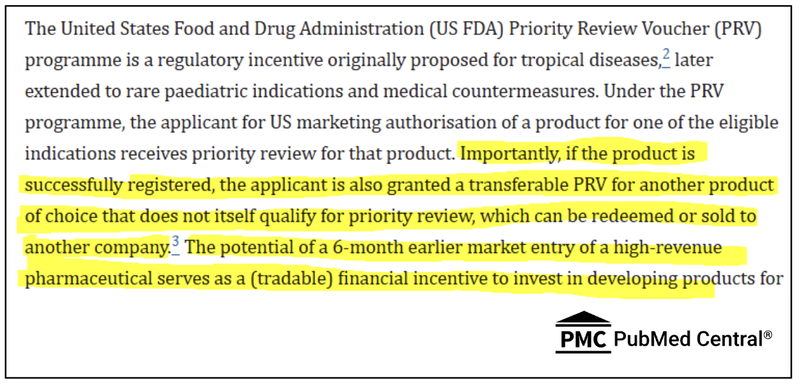

A Priority Review Voucher (PRV) is a regulatory incentive granted by the FDA to encourage the development of treatments for certain serious conditions.

PRV’s are awarded to companies that get FDA approval for drugs targeting:

- Neglected tropical diseases

- Rare pediatric diseases

- Medical countermeasures (e.g. for bioterrorism or pandemics)

Importantly, a PRV is transferable.

This means the PRV can be sold to another biotech company wanting a faster approval.

Some PRVs have sold for as high as $350M (source).

Because ILA is repurposing drugs that have undergone clinical trials, there is already a mountain of safety data... and it can skip most of the early stage works (including manufacturing and scale up).

The active ingredient in ILA’s dengue fever drug has already gone through Phase 1, 2 and 3 clinical trials for cancer and respiratory diseases.

For dengue, ILA just has to run phase 2/3 to test for efficacy and then apply to the FDA for approvals.

FDA approvals would unlock PRV eligibility.

ILA’s other drug, Galidesivir (IF acquired) would ALSO be PRV eligible after a single animal study and FDA approvals.

PRV’s once received, help underpin a company’s valuation.

Post capital raise, ILA’s market cap is ~$43M (including in the money options).

The average value of a PRV is estimated at ~US$100M, but some have sold for up to ~US$350M.

Just this week, we saw one PRV get sold for US$155M (A$241M).

(Source)

The reason PRVs are so valuable is because:

- A drug can get put into market a lot quicker than the traditional commercialisation strategy.

- Once a company is granted PRV status for a drug, that status can be transferred to another product of choice without having to qualify for a priority review.

That time saving is obviously valuable for companies who can get into market ~6 months earlier (versus going through the priority review process).

(Source)

At our Initial Entry Price - ILA’s market cap is ~$43M (fully diluted basis).

IF ILA were to get PRV status granted for one of its drugs, ILA could have a transferable asset worth (on average) US$100M (A$155M) and up to US$350M.

Many multiples of where we are Investing.

What are the key catalysts for ILA in the short term

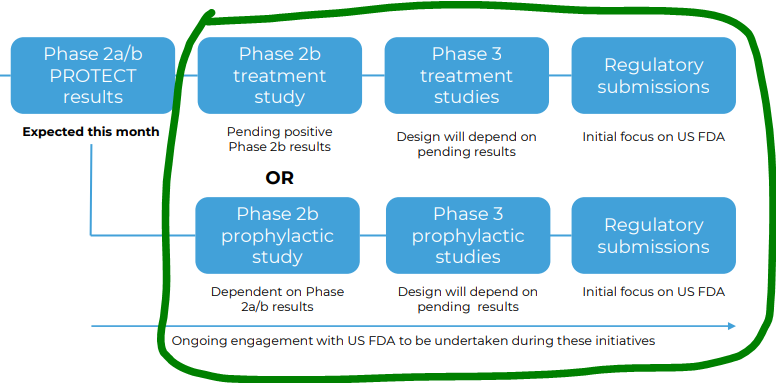

🔄 Phase 2a/2b trial results (DUE THIS MONTH)

The most obvious catalyst are the results from the 2a/b trials for dengue fever.

The results should be out in the coming weeks.

The main thing we want to see from the result are:

1. That the drug efficacy is high enough to move into phase 2/3 trials

AND

2. Whether or not it works best as a preventative (pre-infection) or treatment (post-infection).

The ideal scenario will be ILA having started phase 2/3 trials before the end of this year.

(Source)

🔲 Partnership for phase 2/3 clinical trials...(unexpected surprise catalyst)

The big unexpected catalyst we are hoping drops inside the next few months is a partnership to take the phase 2/3 clinical trials forward.

This is a complete unknown, but we think ILA will have all of the key ingredients needed to be able to attract a partner before or right after the company starts phase 2/3 trials:

- ILA knows its drug is safe in humans (has had over 40+ Phase I, II and III human clinical trials completed and is recognised by the FDA as safe).

- Phase 2a/2b data will be known - (assuming the upcoming results are good) ILA will be able to show potential partners that its drug is effective against dengue fever.

- Animal models show the drug works against otherwise lethal doses of dengue - animal data shows both safety and efficacy in animals that are injected with a lethal dose of dengue.

We think a combination of these will be enough for ILA to at the very least start discussions with a big partner...

Investment Memo: Island Pharmaceuticals (ASX:ILA)

Investment Memo Date: 21-May-2025

Shares Owned at Open: 3,766,666

What does ILA do?

Island Pharmaceuticals (ASX:ILA) is a drug repurposing company focused on antiviral therapeutics for infectious diseases.

ILA is currently repurposing an old cancer drug for prevention and treatment of dengue fever and other mosquito borne diseases.

What is the macro theme?

Dengue fever affects ~400m people and causes ~40k deaths a year and currently has no treatment or preventative.

Dengue is predicted to become a major and growing problem as the world warms and mosquitos become more prevalent in latitudes further away from the equator.

It could apply to other infectious diseases.

Our Big Bet for

“ILA re-rates to a $500M+ market cap by developing its dengue fever or Galidsiver drug”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our ILA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we Invest in ILA?

- Big addressable market - dengue infects up to 400M per year, kills ~ 40k

- Dengue fever cases are growing globally, but no specific treatment or preventative

- ILA is backed by the Race Oncology team (went from 6.6c to $4 per share - a 60 bagger)

- Dengue fever clinical trial catalyst due in the next few weeks

- ILA could be eligible for “Priority Review Voucher” (PRV) - worth ~ US$100M

- The active ingredient in ILA’s drug has already been proven safe in multiple clinical trials

- The US Government and the US Army both supported ILA’s clinical trials

- Possibility to expand drug to other infectious disease indications

- ILA to enter Biodefense space.

What do we expect ILA to deliver?

Objective #1: Phase 2a/b study results:

We want to see ILA’s results from the Dengue Fever phase 2a/b study. We want to see ILA show that its drug is effective enough to move into a phase 2/3 trial.

We also want to see whether or not ILA will be doing a phase 3 trial as a preventative (pre-infection) to Dengue OR as a therapeutic (post-infection).

Milestones

🔲 Phase 2a/b clinical trial results

🔲 ILA makes a decision to move into phase 3 trials

Objective #2: Phase 2/3 clinical trial design and completion

Based on the results from the phase 2a/b study, we want to see ILA set up a trial design and eventually start phase 2/3 trials.

Milestones

🔲 FDA meetings to determine endpoints for the trial

🔲 Clinical trial design completed

🔲 Clinical trial starts

🔲 Clinical trial completed

🔲 Clinical trial results

Objective #3: Partnership for Phase 2/3 trials.

Pending the results of Objective #2, we want to see ILA lock in some sort of partnership deal to help fund its phase 2/3 trials.

Milestones:

🔲 Partnership deal

(Bonus) Objective #4: Galidesivir acquisition

We want to see ILA make a decision on the Galidesivir acquisition option.

Milestones:

🔲 Option exercise

🔲 Forward plan

What could go wrong?

Development purgatory risk

With a big catalyst coming, any positive news may become a liquidity event that existing holders use to sell into.

ILA will likely have to run an additional Phase 2 or 3 trial(s), which will take time and cost money (see funding risk).

This could result in a quiet period while the company recruits new patients for the trial and may mean the ILA share price trades sideways or sells down on a lack of material newsflow.

Cap structure risk

Shares were issued inside the last 12 months at 6c and 7c. Both of those capital raises happened to have one-for-one options attached to them. This could create some short term selling pressure, which could take some time to churn through.

We also recognise there are ~50m 7c options in the money which could get converted and create more supply.

Clinical trial risk

It is important to be aware that clinical trials can be unsuccessful.

Here are some of the standard risks that are associated with biotechs that are undertaking clinical research:

- Patient recruitment is delayed or fails

- Ethics approval is delayed or fails

- Clinical trial cost blowouts

- The drug or treatment is ineffective at treating the particular disease (usually determined by clinical trial results in Phase II and Phase III)

The design of the trial is such that the regulatory body does not approve the drug/treatment.

There is a chance that one or more of ILA’s clinical trials fail to meet their primary or secondary endpoints, meaning the treatments fail to satisfy the criteria of the studies.

Any clinical trial results, if negative, could hurt the ILA share price.

Funding risk

Pre revenue biotech companies regularly need to raise capital to fund their growth ambitions. Capital raises can cause dilution to existing shareholders.

As a pre-revenue company, ILA will likely need to raise capital at some stage in the future, potentially at a discount to the prevailing market prices to secure funding.

This will be contingent on clinical trial results and broader market sentiment (see next risk).

Phase 3 funding risk

If ILA’s Phase 2a/b trial is successful, it will need to conduct a larger Phase 3 trial.

This trial will likely need to be much bigger with human patients with dengue fever around the world, which could get expensive if setting up clinics in remote overseas locations.

If ILA is not able to find an institutional partner or fund willing to pay for the trials it may need to raise the money from the retail market.

Market risk

Broader market sentiment for small pre-revenue biotechs could deteriorate and the sector as a whole trades lower, taking ILA’s share price with it.

Alternatively, the entire equities market could sell down as well.

What is our Investment Plan?

We plan to hold a position in ILA for the next 3-5 years (and beyond) as it takes its dengue fever drug into phase 2/3 clinical trials.

We eventually may look to take some profits by selling up to ~20% of our holding (in line with our holding policy and escrow conditions) if the share price materially rerates on the company successfully delivering on the key objectives listed above.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.