Second largest uranium enricher in the world Urenco agrees terms for investment into GUE’s enrichment tech.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,671,018 GUE shares and 500,000 GUE options and the Company’s staff own 35,000 GUE shares at the time of publishing this article. The Company has been engaged by GUE to share our commentary on the progress of our Investment in GUE over time.

We just got news that the world’s second largest producer of enriched uranium has agreed to terms on an investment...

Into GUE’s uranium enrichment technology.

One of the key reasons we Invested in Global Uranium and Enrichment (ASX:GUE) was for its ownership stake in a New uranium enrichment tech company Ubaryon.

Urenco is the biggest non-Russian/Chinese enriched uranium supplier in the world.

It operates facilities in Germany, the Netherlands, the United Kingdom

...and the United States.

It is a private company owned by the UK and Dutch governments as well as two German utilities.

Urenco’s FY24 revenues were €1.8BN ($3.2BN).

Urenco is BIG, and we think the ideal partner to help GUE’s enrichment tech investment further progress the technology.

Today Urenco has signed a non-binding agreement to invest $5M into Ubaryon.

Ubaryon is the name of the enrichment technology company that is 21.9% owned by our Investment GUE.

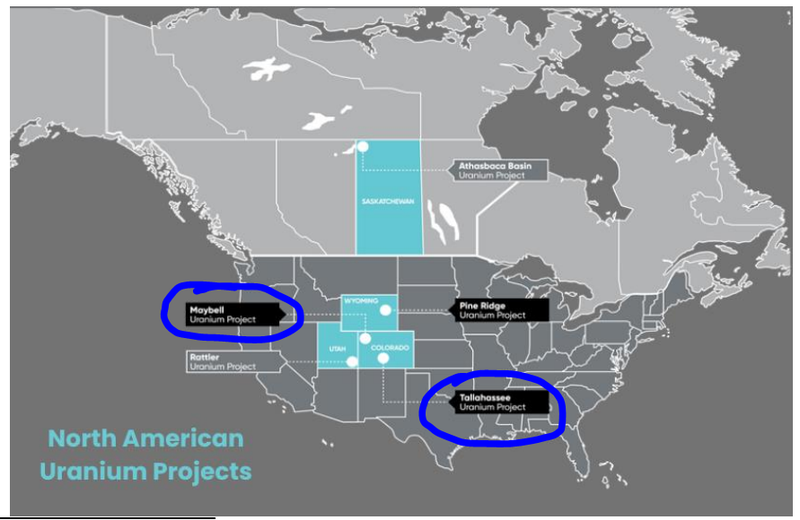

GUE also has a portfolio of uranium assets in the US, including one right next door to Cameco in Wyoming.

(More on those assets later)

Here is a quick-fire overview of the deal:

- Urenco will invest $5M for a 13% shareholding in Ubaryon.

- The investment will be made over 3 years.

- The deal is a non-binding agreement. Urenco and Ubaryon will still need to formalise the deal and convert it into a binding agreement.

Once complete, GUE will still be the single biggest shareholder of Ubaryon...

So GUE will benefit from the capital and expertise injection from Urenco...

We like the deal because for us it is an external validation of the value in Ubaryon’s enrichment tech from an industry giant.

The second biggest enricher of uranium who has actual operating enrichment plants & makes ~$1.8BN euros per year selling enriched uranium has seen enough to take a cornerstone position.

We also think Urenco’s interest has something to do with Ubaryon’s tech being a chemical process for enriching uranium - which if it works, could use less energy, be more environmentally friendly and simplify the enrichment process.

Or maybe because Russia currently controls ~50% of the global enrichment capacity, and Russia and China combined control ~63%.

There is a clear and obvious squeeze going on in the west for enrichment capacity...

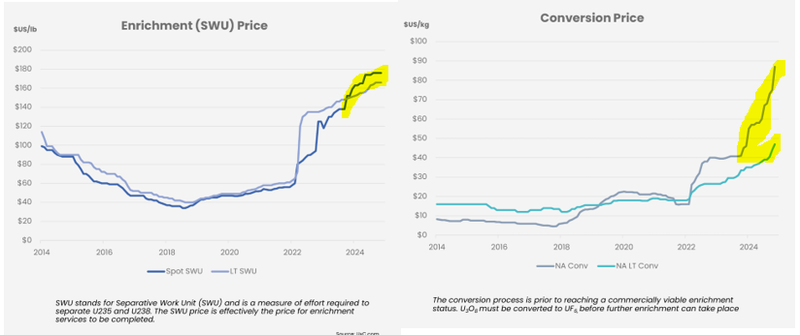

Those restrictions have also pushed conversion & enrichment pricing higher exponentially:

Partnership catalyst to bring more eyeballs to GUE?

We think today’s news is a major catalyst for bringing market attention to GUE (because of its major shareholding in Ubaryon).

It’s very hard to find enrichment exposure on any stock exchange globally...

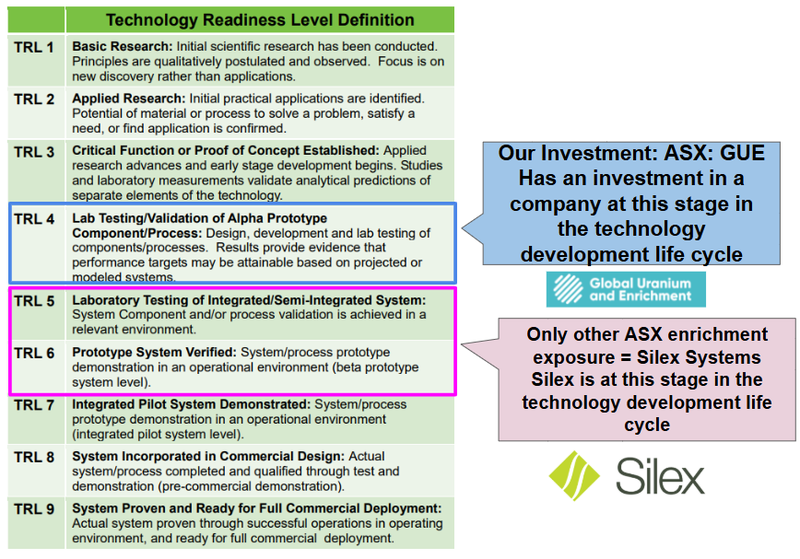

The only other stock in this space on the ASX is $714M capped Silex Systems.

SLX’s tech is more advanced than Ubaryon...

GUE’s tech is at what’s called TRL-4, whereas Silex is about to cross TRL-6.

(TRL stands for Technology Readiness Level and there are 9 stages in this lifecycle of technology development)

GUE’s technology investment has quickly moved from TRL-1 to TRL-4 in the last ~6 years.

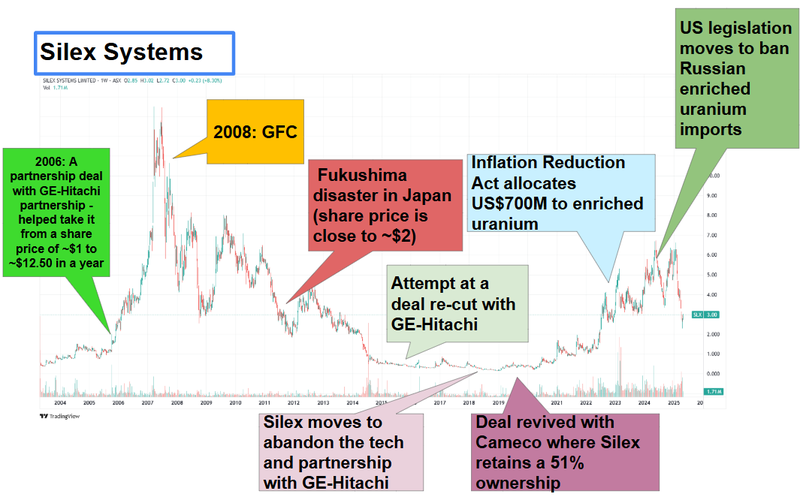

Silex was first listed in 1998 but things really started getting interesting once a partnership deal was signed with General Electric (GE)-Hitachi.

Silex’s share price has over the years moved up and down based on partnership newsflow and global uranium macro winds...

After that big rally in 2006, the share price came back down to a low of 15c after the deal with GE-Hitachi was abandoned.

Then the deal with Cameco was signed in 2019 and the stock started its run back up to ~$6.75 highs last year

(into a really good macro backdrop for uranium):

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This is what we know GUE has going for it now, after this deal:

- It’s a chemical process and doesn’t require “fancy lasers” (like Silex’s technology does)

- Its enrichment tech partner will be the world’s second biggest uranium enricher, Urenco

- Unlike Silex, GUE hasn’t had to navigate the GFC (2008) and Fukushima (2011), and as far as geopolitics go, the case for nuclear power and uranium is much stronger now than it has been in decades

- GUE’s biggest single shareholder is NASDAQ listed Snow Lake Resources (holding 19.99% of GUE) - giving GUE exposure to US markets...

GUE has the tech partnership and the right type of uranium projects... and all we need now is for the macro sentiment to improve.

Here is what we are expecting next from GUE that could move the share price:

- Completion of the deal with Urenco

- Drilling to start at the newly acquired uranium project in Wyoming, USA.

And of course... a rally in the uranium price could also be good for GUE’s share price.

Why we think the uranium macro will get stronger from here...

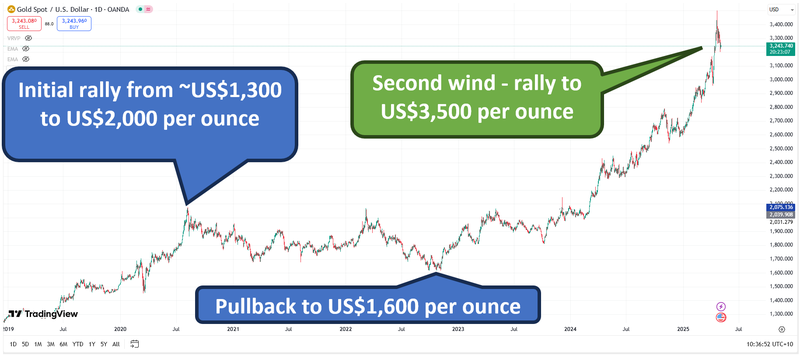

The uranium spot price had its initial run at the end of 2023 into the start of 2024.

It went as high as US$107/lb.

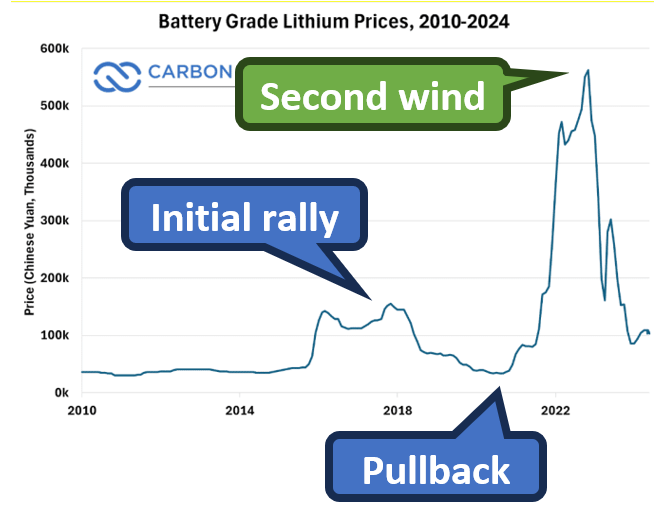

We think something similar to gold & lithium is playing out with uranium.

Lithium first ran in 2017-18, then came off in 2019-2020 only to go to all time highs in 2021-2022...

Gold did the same - a small run in 2020-2021 then a pullback in 2022-2023.

Now gold is ripping to new all time highs every week and the market is re-rating gold stocks again...

After decades of watching commodities markets, we know a small pullback almost always happens after a big rally following years of trading sideways.

We think the uranium spot price could be doing something similar.

An initial run in 2023, small pullback, then it could start a more sustained move up...

The uranium spot price looks to be at the very early stages of another move up:

(Source)

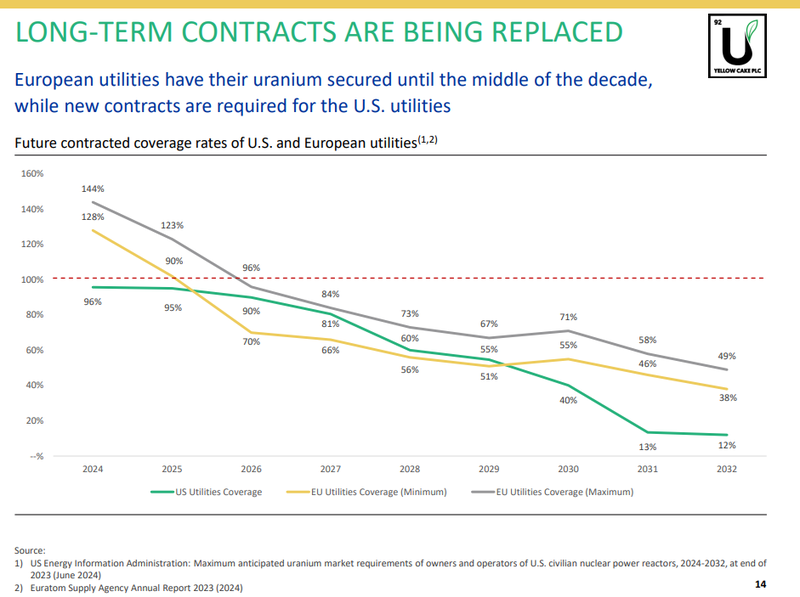

Uranium is slightly different to other commodity markets because it has a long on/off contracting cycle from utilities.

These buyers aren't actively buying in spot markets, instead, they are contracting supply decades into the future.

Spurred on by recent climate commitments, countries around the world are moving to grow their nuclear fleets.

Which is putting pressure on supply in the medium term.

AND long term contracted rates are declining... starting in 2026 all major utilities across the EU and US will be below 100% coverage for the first time in years.

By 2032 the utilities will have <50% of supply contracted.

This could trigger the start of a contracting cycle where these utilities are back in the market looking for new supply...

(Source)

Our view is simple, we think GUE has the right assets to be re-rated in a market where sentiment for uranium companies is a lot more positive than it is now.

All we need now is for the uranium price to start running again...

Why enrichment matters:

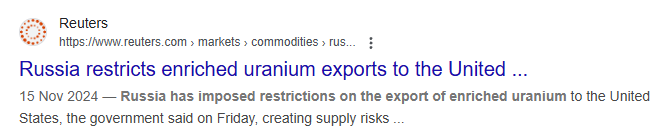

We think the sudden movement on this has a lot to do with the recent export restrictions Russia put on enriched uranium...

(Source)

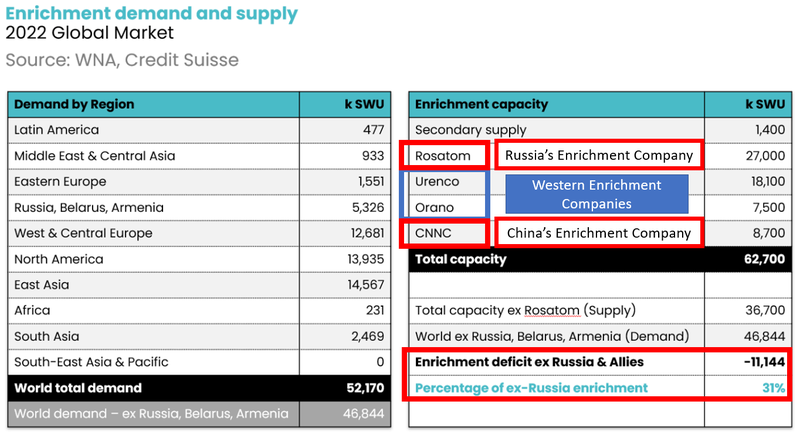

Russia currently controls ~50% of the global enrichment capacity, and Russia and China combined control ~63%.

There is a clear and obvious squeeze going on in the west for enrichment capacity...

Below is a quick summary of the companies that have enrichment capacity in the world matched up against sources of demand:

Those restrictions have also pushed conversion & enrichment pricing higher exponentially:

Why does this matter for the west?

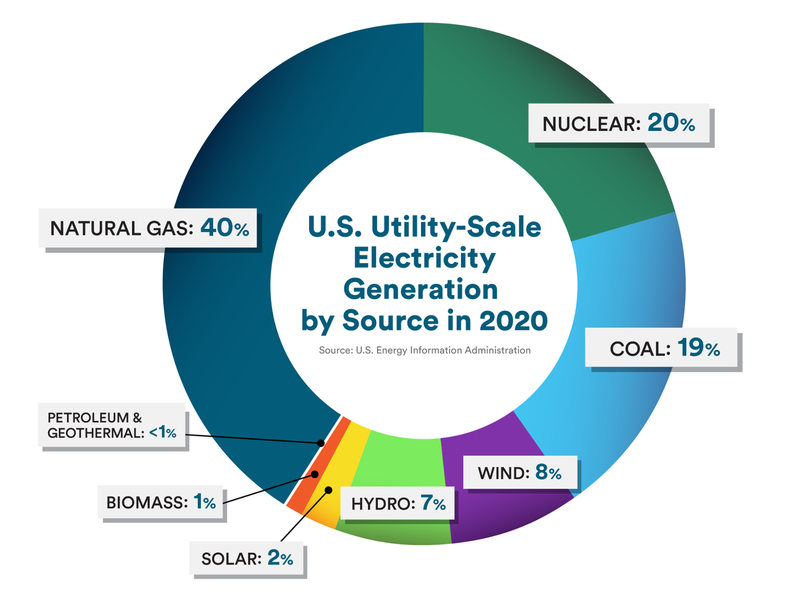

Because the West is reliant on nuclear power (and enriched uranium) for a big portion of its electricity generation capacity.

The USA is home to the world’s largest fleet of nuclear reactors AND ~20% of all US electricity generation relies on nuclear power.

The problem is even worse in France.

France relies on nuclear power for ~70% of its electricity generation capacity...

(Source)

Global Uranium and Enrichment

ASX:GUE

GUE’s new US uranium project: 8 things we like about it.

We mentioned earlier we thought GUE also had the right assets to do really well in a strong uranium macro environment.

GUE recently acquired a 50% stake in a uranium project in Wyoming.

The project is right next door to the USA’s biggest permitted ISR uranium processing plant owned by $30BN Cameco.

We think Wyoming and the type of project GUE has (ISR uranium) will be the first to come back into production inside the US...

Check out our previous note here for a deep dive on the project.

Here is a quick summary of the 8 reasons why we like the project:

- Located in the uranium capital of the US - GUE’s new project is in the old capital for uranium production in the USA - Wyoming was once producing most of the world’s uranium.

- Domestic uranium is crucial for the US - ~20% of US electricity generation relies on nuclear power. The USA is also home to the world’s largest fleet of nuclear reactors. Despite this, the country is reliant on imports for ~95% of its nuclear fuel consumption, much of which still comes from Russia and Kazakhstan... We think the US will need to bring domestic supply back online - which is good for GUE.

- US Government is already allocating significant funding for the domestic uranium industry - The US government has committed upwards of US$10BN in funding to encourage new supply to come to market. More specifically, the US Department Of Energy started signing purchase orders with Wyoming based companies...

- GUE’s new project is the lowest cost style of uranium - ISR uranium has the lowest opex, lowest CAPEX and is the easiest type of uranium to get into production. Most of the world’s uranium supply comes from ISR deposits in Kazakhstan.

- GUE’s project is right next to Cameco’s fully permitted ISR processing facility - GUE’s new project sits within ~80km of 5 permitted ISR uranium facilities, including Cameco’s Smith Ranch-Highland plant (the USA’s biggest ISR uranium production facility). Plants are owned by the likes of $30BN Cameco & $3.4BN Uranium Energy Corp.

- Neighbours with plants have been doing M&A over the years - Wyoming neighbours Uranium Energy Corp have been talking about “Hub and Spoke” operating models for years now and have always said they are open to bringing new projects into their portfolio. $3.4BN Uranium Energy Corp has also been trigger happy on deals paying US$134M for a junior back in 2021 when the uranium price was only US$42/lb.

- GUE’s project could host more uranium than $30BN Cameco’s project next door - The project has a 24.4-51.3Mlbs exploration target. IF GUE is able to define a JORC resource at the upper end of that target it could become comparable to $30BN Cameco’s project next door. So far the project has had ~1,200 holes drilled so the target is estimated with a pretty big data set of drillholes.

- We really like the uranium macro thematic - Once they get moving, the uranium price tends to rip. It’s happened twice since 1970. This time we think the structural demand & forecast supply issues from decades of stalled new projects could come together to trigger a big run in uranium prices.

What’s next for GUE?

🔄 Drilling & exploration plans for Pine Ridge

GUE has previously said that "preparations for initial drilling” at Pine Ridge were advanced.

Within the next few weeks we want to see GUE lay out a clear exploration plan and put some timelines around the drill program.

(Source)

🔄 Enrichment Technology (GUE owns 21.9% of private company Ubaryon)

We want to see the deal with Urenco be converted from a non-binding agreement into a binding agreement.

Key Milestones we are tracking:

🔄 Secure strategic/commercial partner for uranium enrichment technology

🔄 Further validation and extend the enrichment performance (show how well it works)

🔲 Achieve continuous operation at bench scale (scale up process)

🔄 Regulatory approvals

GUE’s other mining projects

GUE has a number of other North American uranium exploration & development assets.

Here is what we are looking out for across these projects:

🔄 Project 1: ~52 Mlb Resource Scoping study at Tallahassee (coming months)

A Scoping Study is due shortly at GUE’s advanced ~52Mlb JORC resource in Colorado.

GUE indicated in September 2024 that the scoping study is due in the “coming months”.

🔄 Project 2: maiden JORC Resource at Maybell (coming months)

GUE completed its drill program in October last year, now it is preparing a maiden mineral resource estimate for Maybell in another part of Colorado.

Depending on the resource size and economics, next steps could potentially include additional drilling in 2025 and a scoping study to evaluate development options.

What are the risks?

The two main risks for GUE right now are “Commodity Price Risk” and “Market Risk (Macro)”.

Uranium small caps tend to be bid up or sold off in line with the uranium price.

If macro sentiment is weak, small cap companies share prices can suffer pretty aggressively.

If the uranium price falls or trades sideways then we would expect GUE’s share price to trade sideways or be sold off.

Commodity price risk

The uranium price could fall, or fail to rise enough to make GUE’s US assets viable.

Source: “What could go wrong”? - GUE Investment Memo 20 Feb 2023

Market risk (macro)

The broader market could sell down or crash, impacting the risk appetite of market participants and hurt the GUE share price.

Source: “What could go wrong”? - GUE Investment Memo 20 Feb 2023

We list more risks to our GUE Investment Thesis in our Investment Memo here.

Our GUE Investment Memo:

You can read our GUE Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our GUE Investment Memo covers:

- What does GUE do?

- The macro theme for GUE

- Our GUE Big Bet

- What we want to see GUE achieve

- Why we are Invested in GUE

- The key risks to our Investment Thesis

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.