A $29BN reseller, a mobile product and a billionaire major holder - in ONE company

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,925,333 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

It’s looking remarkably resilient on the charts.

In fact it has just kept going up - 70% since the start of the year.

This is actually quite impressive in a down market for many small caps.

But how and why? And will it keep going up?

Our health tech Investment and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) released its half year results yesterday, which had some clues as to what the next six months could hold.

ONE’s technology connects a patient in a hospital bed to nurses, meal service, medical images and records, educational content, entertainment and other in room systems to help make the hospital run better.

ONE sells its technology to hospitals and other healthcare facilities and has built up a neat recurring revenue model.

Here’s the high level summary of the two most important things ONE has in its corner:

- A Value Added Reseller agreement with ~$29BN capped hospital product supplier Baxter International - NASDAQ listed Baxter has a small army of sales people in the US where ONE operates. It’s opened up a pipeline of “100 opportunities”, and we think major deals could land at any time. Baxter has already delivered two new deals. In recent months ONE has been investing in supporting future Baxter sales, and we think we will continue to see more come in.

- A powerful mobile product - called “MyStay”. Currently being piloted in New York, when fully rolled out, this mobile product should effectively strip out all the difficult hardware supply and installation issues that ONE has diligently worked to overcome over the past few years, and make it way easier for hospitals to adopt the solution.

When these two pieces of the puzzle fall into place and work together, we think ONE’s recurring revenue will rapidly increase - bringing financial and further share price performance with it.

Yesterday, ONE updated the market on how the first half of the year went, which contained a range of important nuggets of information that we talk about today.

Be sure to check out ONE’s latest investor call audio:

Click here to listen to ONE CEO James Fitter speak to the H1 2024 results

Which is best matched up with the latest ONE presentation:

Click here to view ONE’s H1 2024 results presentation

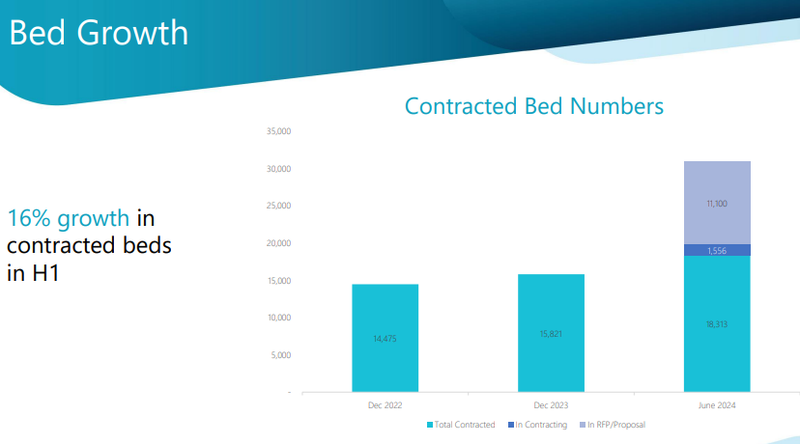

Now, while the financial results for the last half were somewhat disappointing in terms of recurring revenue growth (~7% on the same time last year), we are more interested in ONE’s ability to rapidly expand its “contracted beds” - which is like an active user metric for a tech company.

As of the half year results - ONE had a sales pipeline of ~14,000 new contracted beds to add to its already secured 18,313 contracted beds.

In the investor call above, ONE CEO James Fitter said the company was on track to hit 25% year on year growth rates if the current sales pipeline is converted.

So ONE is in with a shot of nearly doubling its “active user” metric - it just needs some big deals to come in.

Keep on reading for more detailed takeaways from the call.

As we mentioned above, the market seems to agree that ONE is in a good spot right now - the ONE share price is up ~70% since the start of this year.

The market may be pricing in ONE’s traditionally strong finish to the year, which we’ve seen play out before, since we first Invested over three years ago.

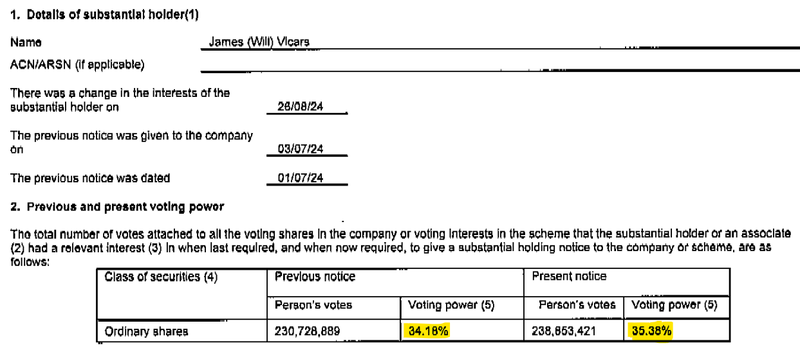

Billionaire hedge fund manager Will Vicars must like how ONE is delivering, recently buying even more ONE shares - increasing his holding from 34.16% to 35.38% in recent days at current market prices.

That’s a good sign... here’s more on ONE.

For those who are new to ONE - think of ONE’s tech as a single touch screen at your hospital bed where you can:

- Have virtual consultations with relevant medical specialists - local and worldwide.

- Control all aspects of your room - bed, lighting, temperature.

- Order food, watch movies, and get a nurse's attention - like the screen you get in your airline seat when flying.

- Interact with tailored rehab, education and training videos - for a patients specific health situation and;

- Monitor your health outcomes - Doctors and nurses will have better info on you, replacing the clipboards, pen and paper currently used for this.

Here is what Oneview looks like at the patient's bedside:

And here is that the Oneview interface looks like for a patient:

Previously, ONE has had to contend with the logistics of hardware, tablets, and monitor screen arms to physically install its tech in a hospital room.

But the big “blue sky” bet for ONE is to access ONE tech on your own device...

ONE has launched a “bring your own device” (“BYOD”) solution - called “MyStay” where patients can bring their own phone or tablet to a hospital and plug straight into ONE’s platform on arrival.

(Source)

Read more about ONE’s MyStay in this note:

Baxter is Coming... and so is BYOD.

We think that the Baxter Value Added Reseller agreement that ONE has, in combination with MyStay, could unlock the rapid recurring revenue growth that takes ONE further up the charts from its current market cap of ~$276M.

This is the basis of our ONE Big Bet:

Our ONE Big Bet

“ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1BN valuation (based on 5x to 10x forward annual recurring revenue) and be acquired by a large health tech provider.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

Our key takeaways from the ONE H1 2024 results presentation

Earnings calls are always a good listen because they bring together the stream of announcements a company puts out over the course of the year and consolidate it into one cohesive story.

For us, the call gave a really good idea of what will drive ONE forward in the next few years.

It's pretty clear to us the company has been building up to where it is now and ONE CEO James Fitter's comment that the company is “approaching a step change moment” for the business is something that we can see a pathway to ONE achieving.

You can listen to the full recording to via the link below:

Click here to listen to ONE CEO James Fitter speak to the H1 2024 results

which is best matched up with the latest ONE presentation:

Click here to view ONE’s H1 2024 results presentation

Here are our key detailed takeaways from the presentation:

- Market trends - ONE CEO James Fittercommented on the ~350,000 nurse shortfall in the US which is creating problems for hospitals. He mentioned hospitals are looking to embrace tech to take pressure off labour shortages. James highlighted McKinsey research that shows how virtual nursing tech can help reduce costs by over 30-40%.

- Market trends - James talked about consolidation happening in the healthcare industry - he specifically mentioned the takeover’s of two of ONE’s four competitors in 2024...

- M&A in ONE’s sector - in the Q&A section of the call (starting at ~51:00) an MST analyst asked about M&A across ONE’s competitors. James briefly touched on the two takeovers in the sector but also mentioned that the more interesting developments were the acquisitions happening at the Baxter level (the multi-billion dollar market leaders). James discussed the acquisitions by Stryker (one of Baxter’s competitors) in the virtual care/bedside tech space and how it shows the bigger players see value in offerings like ONE’s.

MST Access recently released an excellent research report for ONE with a price target of $0.61 - you check out that full report here: August 8th 2024 ONE MST Report

While that price target does look interesting, we should be clear that analyst price targets are based on a number of assumptions that may be incorrect. Never invest on a price target alone, and always do your own research.

- Baxter partnership - James talked about how the nurse call product was a big part of the Baxter business (25% market share in the US) and how ONE’s products could easily be sold to existing and new clients in the space

- Baxter partnership - James talked about the developments with Baxter over the last two weeks. He mentioned ONE was preparing for joint meetings in the next few weeks with Baxter across five major health systems (Florida, Tennessee, Kentucky and 2x California).

- Baxter partnership - We also found out about the first joint Request For Proposals submitted with Baxter just last week. James mentioned there were 100 different opportunities in Baxter’s pipeline that had the potential to add ONE’s offerings to thousands of beds in the US. ONE also confirmed the hire of a new Vice President of sales in the US, responding to inbound interest through Baxter.

- Revenue growth rates - James mentioned the company was on track to hit 25% year on year growth rates if the current sales pipeline is converted. Anything additional to this would be bonus upside.

- Gross margins improving - There were mentions of gross margins improving as hardware is taken out of the business. ONE also talked about the sunsetting of legacy systems which should lead to improvements in cost structures and increased efficiency across the business.

- Mystay BYOD development costs finished - The company confirmed development of the BYOD device had finished and the product was now out of the development stage. This should mean lower costs going forward for the product.

- Other product launches - ONE launched the second version of the digital door sign during the HY as well as design updates across other products.

- ONE’s Artificial Intelligence (AI) Strategy - ONE confirmed the company had made investments into “the foundations for the AI strategy”. Target areas for AI adoption could be things like predictive analytics, displaying of relevant information and AI to increase care team productivity. ONE also talked about the long term potential for one to one AI nursing for patients.

- ONE’s Artificial Intelligence (AI) Strategy - ONE interviewed all major customers and shortlisted problems mentioned by customers. Expecting to launch a pilot AI product in Q4 of this year (another catalyst to look forward to).

For us, after listening to the call, it's pretty clear there is potential for ONE to put out news that genuinely changes the company’s fundamentals in a big way over the next 6-12 months.

It's no surprise to us that ONE’s share price is holding up relatively well in an otherwise tough market AND the company’s biggest shareholders keeps increasing his position with on-market buying.

Major shareholder keeps buying on market

Two days ago, billionaire hedge fund manager Will Vicars increased his holdings in ONE - going from 34.19% owner to 35.28% owner.

(Source)

This wasn't Vicar’s first increase in holding... he has been progressively increasing his holding for over two years:

It’s always a good sign when a highly successful billionaire hedge fund substantial shareholder continues to buy on market, at market prices.

How does ONE’s half year results impact our ONE Investment Memo?

Objective #1: Repeat sales success and hit 25,000 beds

Building on ONE’s previous 15,000 bed achievement, we want to see ONE hit a total of 25,000 in CY2024, primarily out of the USA.

Source: “What do we expect ONE to deliver?” -ONE Investment Memo 2024

August 2024 update:

ONE looks to be on track to hit Objective #1 from our Investment Memo - it just needs to close more deals in the sales pipeline - the chart below shows 11,100 beds that are at the RFP/Proposal stage

(Source)

With 18,313 contracted beds currently, ONE could finish the year strongly if sales risk doesn’t materialise (see risks below).

Objective #2: More deals with major hospital networks through Baxter agreement

We want to see ONE sign more deals with more hospitals. The Baxter value added reseller agreement has started and the market launch is expected in Q3 CY2023, and we are hoping to see sales traction from this agreement in Q1 CY2024.

Source: “What do we expect ONE to deliver?” -ONE Investment Memo 2024

August 2024 update:

We noticed two new Baxter deals flagged in ONE’s HY results - while we were hoping for more traction with Baxter sooner, we think this could be just the start of many more to come:

(Source)

What are the risks for ONE right now?

Every speculative technology investment carries risk. ONE is no different.

Here are some of the more obvious risks that we can see at the moment (of course there’s always risks no one can imagine).

Sales risk

Despite a strong customer retention rate and the endorsement of the product by prestigious hospitals, ONE could lose key clients or not seal as many deals, hurting their revenue and share price.

Large institutions like hospitals don’t tend to adopt new technology very often and the sales cycle can be long. This feature of ONE’s customer base can cause delays in sales that drag out over a long time.

Marco factors in the market including a recession can cause a reduction in spending on new technology, affecting ONE’s ability to make sales.

August 2024 update: this risk materialised for ONE due to factors outside of its control. Notably, the postponement of projects by a large customer due to corporate activity which is set to re-commence in September 2024, as well as construction delays at a hospital in Ireland.

Distribution partner risk

A key part of ONE’s strategy is to sell its products through a distribution partner like Baxter, Microsoft or Samsung.

Although ONE has a strong relationship with these companies, if they move slowly - or don’t prioritise ONE’s products when making a sale - then it could reduce the sales outcomes for ONE.

August 2024 update: Baxter has helped ONE seal two new deals, but we want to see more from the Baxter channel - delays on Baxter’s end could hurt ONE’s performance.

Funding risk

Although ONE raised $22.8M in July 2023, growth companies need cash to achieve their goals. If ONE doesn’t use the money from this raise wisely, then share price pain could follow. This was ONE’s fourth capital raise since it listed in 2016.

August 2024 update: As of the latest half yearly results, ONE has a cash balance of ~€6.0M (~$9.8M). If this continues to fall as ONE can’t make quick enough progress to breakeven, then a capital raise may be required at some point in the future.

Technology risk

ONE will need to add functionality to its products over time as the health tech industry advances. The BYOD rollout may not go as planned.

Also, ONE has flagged that a range of additional features are in the pipeline, and the successful roll out of these features could help it reduce this particular risk as hospitals become more advanced.

August 2024 update: It appears that the MyStay rollout is going well based on the latest half yearly presentation, but it is always possible that it may prove harder to build the functionality of the product on schedule, on budget.

Market risk

Tech stocks could fall in value again. Even if ONE does everything right from an operational standpoint, the market could always sell off or favour different sectors.

August 2024 update: While tech stocks are performing well in the market, this trend could reverse and take ONE’s share price with it.

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE

- Why we Invested in ONE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.