WCE hits extensions to the high grade Elizabeth Hill silver mine

Our silver exploration Investment West Coast Silver (ASX: WCE) just hit extensions to its Elizabeth Hill project in WA.

WCE owns 70% of the project which was one of the highest grade silver mines to ever operate in Australia.

The project last produced ~1.2M ounces of silver at ~2,194g/t from just 16,830 tonnes of ore over a short run between 1998 and 2000.

The mine didn't shut because it ran out of silver - it shut in 2000 because the silver price had collapsed to ~US$5/oz (and the JV partners of the day fell out).

We are Invested in WCE to see it get the project back into production.

In April WCE defined a 2.8M Oz JORC resource on the project with average grades of 617g/t.

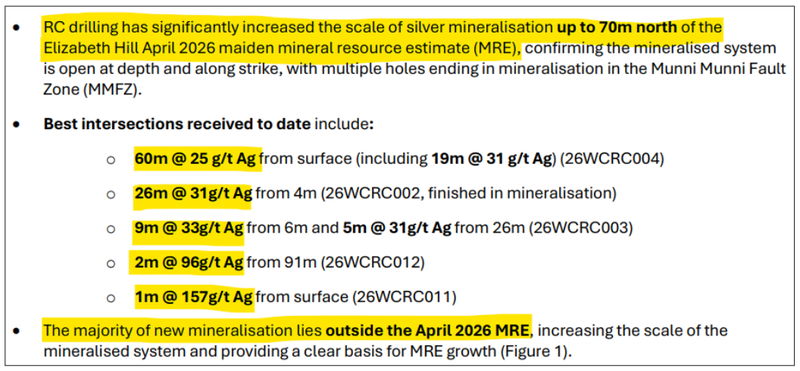

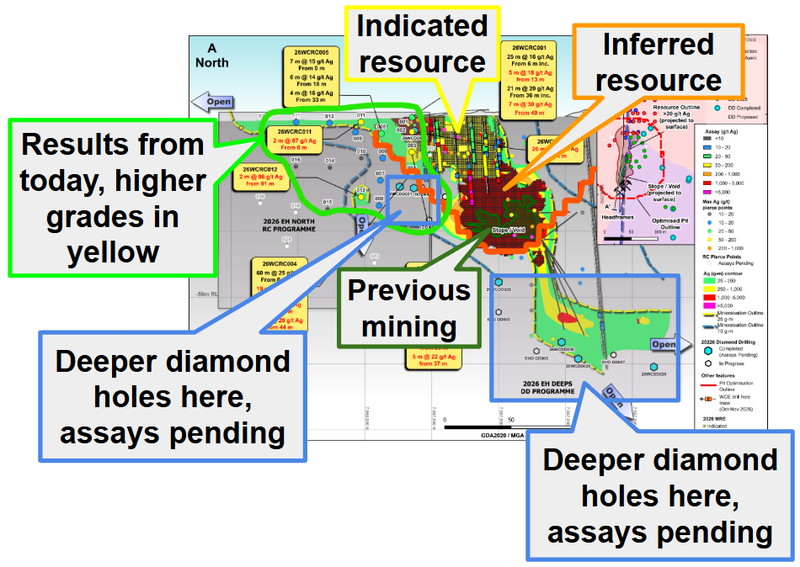

And today, WCE extended that mineralisation ~70m to the north of the existing resource footprint.

(source)

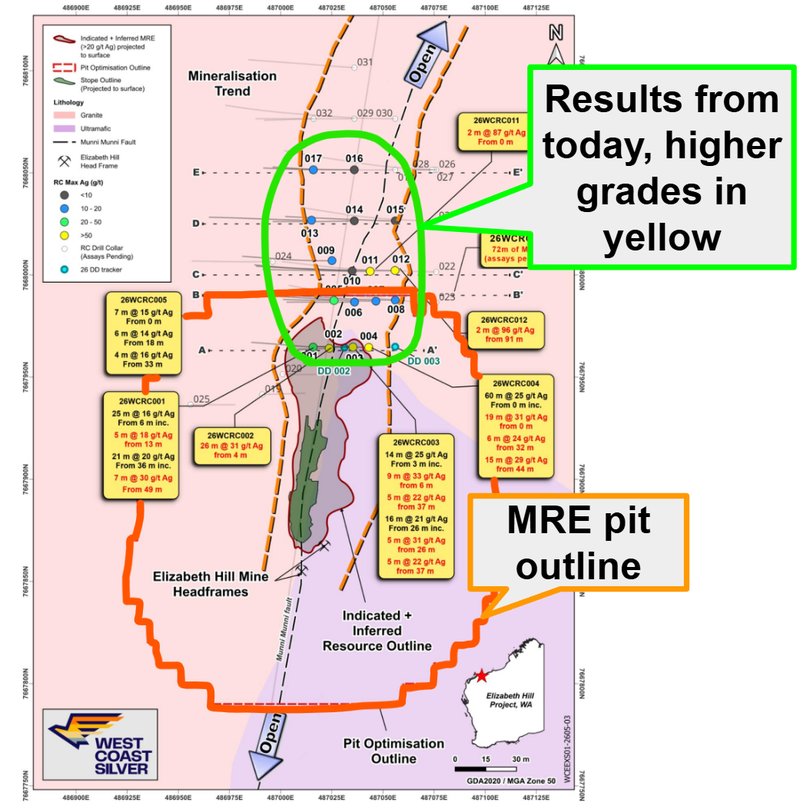

Here is where those extensions sit relative to WCE’s existing JORC resource:

(source)

WCE also had a few holes that ended in mineralisation - which could mean there is more silver at depth.

WCE has a diamond rig drilling those deeper targets right now.

Here is a side on look at the extensions too:

(source)

Back in May, WCE laid out a Growth & Development Plan for bringing Elizabeth Hill back online - we covered it here: WCE lays out growth and development plan for the old Elizabeth Hill silver mine.

That plan runs the project toward an updated JORC resource and a scoping study from around the December 2026 quarter.

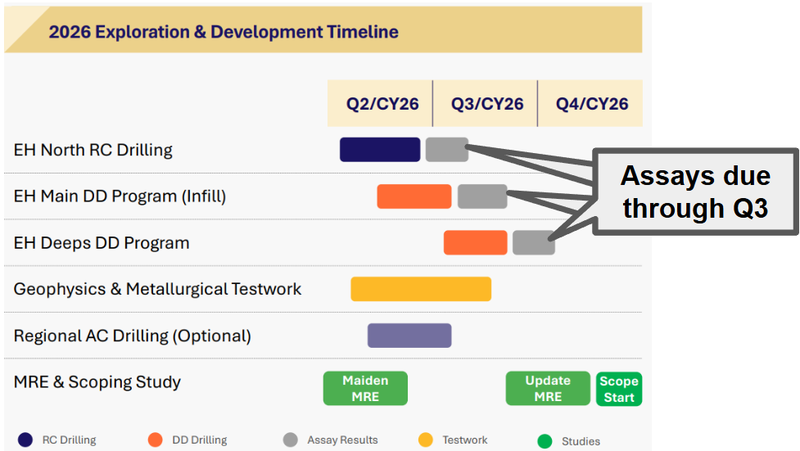

Today's announcement says economic studies of the near-surface mineralisation are progressing in parallel with the drilling - which is exactly the resource-growth step that feeds into that updated resource and scoping study.

So we should expect assays to continue next quarter and perhaps an update on the Scoping Study, as clearly some of the works here are quite advanced:

(source)

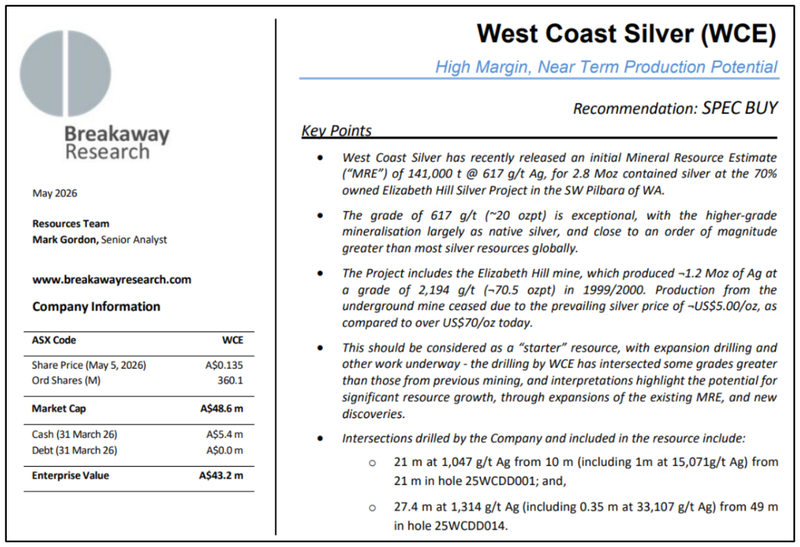

Alongside that Growth & Development Plan, a research house (Breakaway Research) published a report on WCE putting some indicative numbers around the starter-pit idea.

It sketched indicative free cash flow of ~A$168M for a full pit and ~A$17.6M for a smaller, shallow starter pit, on operating margins of ~A$55-70/oz - using a silver price of A$85.71/oz (US$60/oz), which is below the current spot price.

Breakaway also described WCE as the highest grade, pure-silver, near-term development project on the ASX (at an enterprise value of ~A$43M at the time of the report).

Here is a link to the full report:

Next Investors is not a research house and does not provide price targets. The research report mentioned in this article was produced by a third party. We are sharing it for informational purposes only. We have not independently verified the data or the assumptions used in that report.

Those are third-party, indicative figures only - a directional sense-check on the high-grade thesis, not our forecast - and the real economics will come from WCE's own scoping study later this year.

We also noticed another report from Red Cloud that can be viewed from WCE’s website: West Coast Silver Releases Maiden Mineral Resource Estimate and Launches Dual Value Creation Plan

What we want to see next from WCE

Recently, WCE released an updated presentation here.

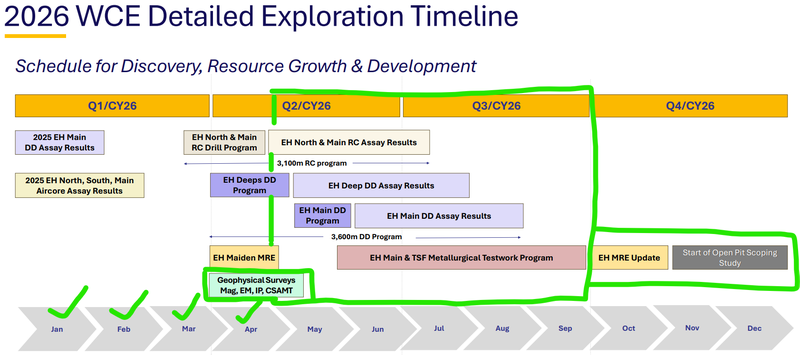

It’s always good to see a Gantt chart showing what’s ahead in these presentations - a one pager on what to expect next.

(source)

The three things we are most looking out for are:

- The RC drill campaign on the targets to the north of the Elizabeth Hill Mine (happening now).

- The diamond drilling going for at depth extensions to the Elizabeth Hill mine (also underway).

- Geophysics across the broader project area

And then all of that data rolling into what we expect to be an updated JORC resource before the Scoping Study before the end of the year, expected to get underway in Q4.