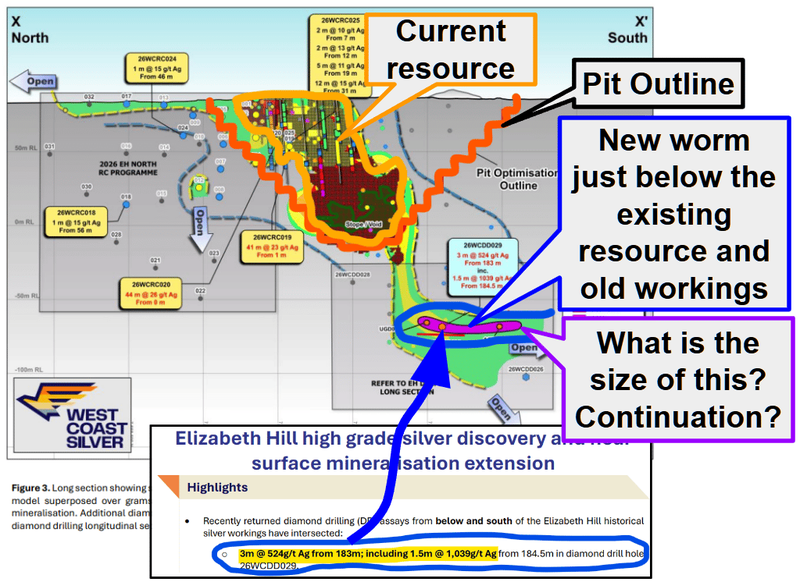

WCE finds new 50m high grade silver zone below historic high grade Elizabeth Mine

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,357,362 WCE Shares at the time of publishing this article. The Company has been engaged by WCE to share our commentary on the progress of our Investment in WCE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

A new discovery at the highest grade silver project on the ASX.

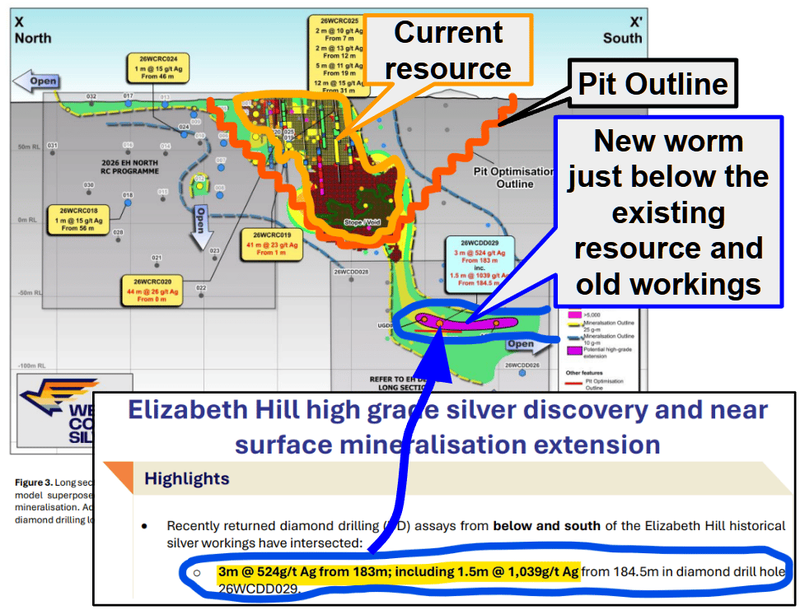

Our silver Investment West Coast Silver (ASX:WCE) just hit a new high grade pocket of silver.

Just below its existing defined resource and already interpreted to be ~50m long.

We call those mineralised zones ‘worms’ in the image below (because they look like worms).

(source)

WCE’s historic Elizabeth Hill mine last produced silver between 1998-2000.

It was the highest grade silver producing mine in Australia - spitting out 16,830t of ore at ~2,194g/t average grade.

From that 16,830t of ore, ~1.2M ounces of silver was produced (~A$101M of silver in today’s money).

WCE owns 70% of the project, which is on a granted Mining Lease, and includes the historic mine plus a land package of 180 square kilometres around it.

WCE is currently capped at $35M and held $5M cash at the end of the March quarter. (source)

We Invested in WCE to see the company do two things:

- Discover extensions to the highest grade producing silver mine in Australian history, and

- The big one - find a NEW Elizabeth Hill deposit - something very high grade, modest in size - but that WCE can do a short and very profitable mining run (while the silver price is high).

Today’s hits could be either of those scenarios...

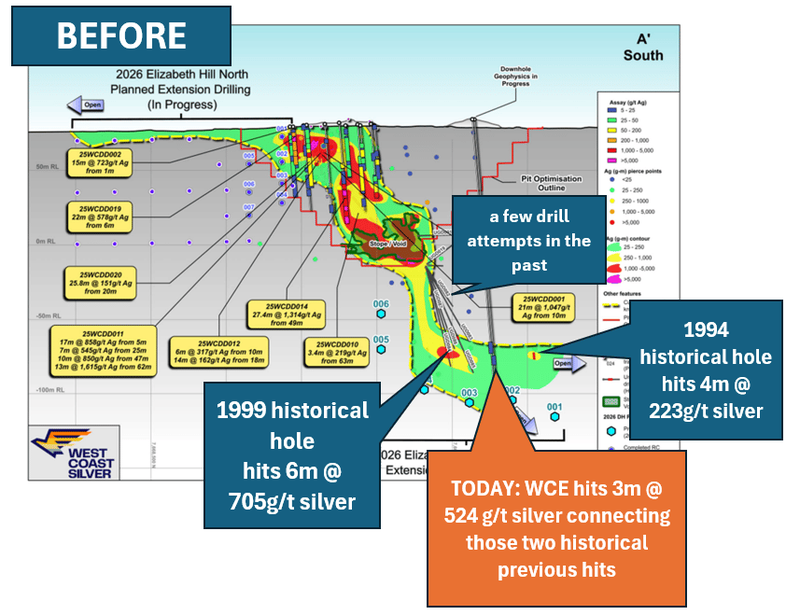

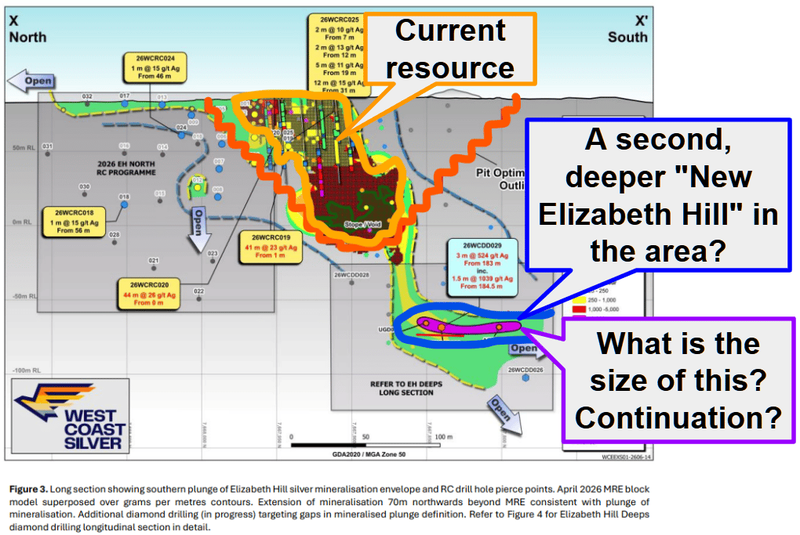

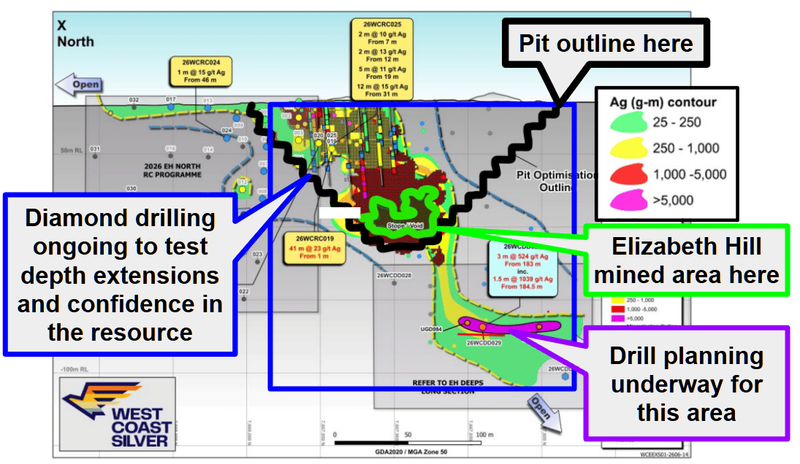

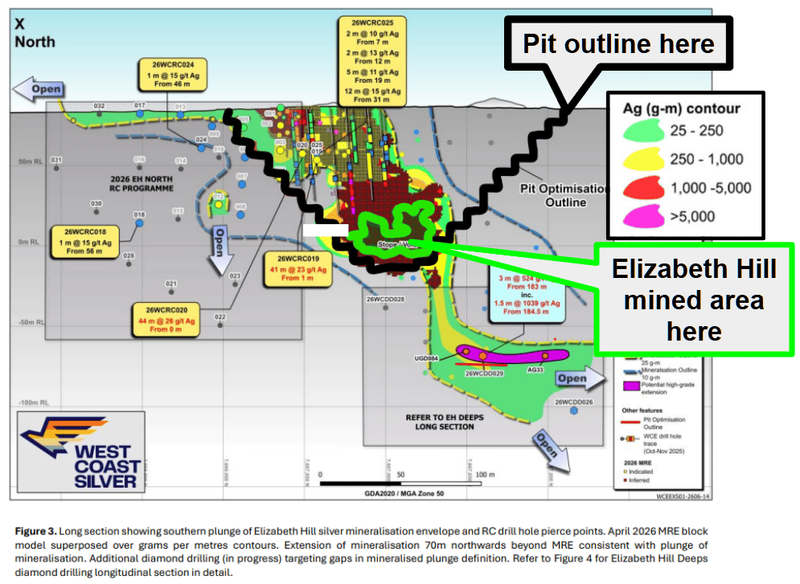

For context, prior to today’s announcement, this is what WCE had (note there is no high grade silver “purple worm” in this image)

Before this drill hit, WCE had two historical high grade drill hits about 50m apart in this area:

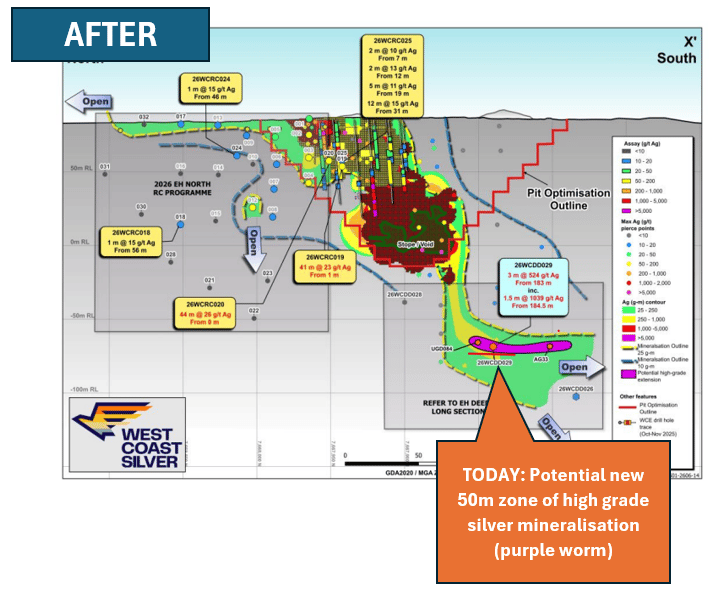

With today's drill result in between those two historical hits the company is inferring a 50m high grade silver zone (the new purple worm in the image):

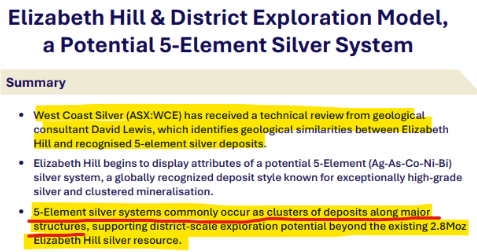

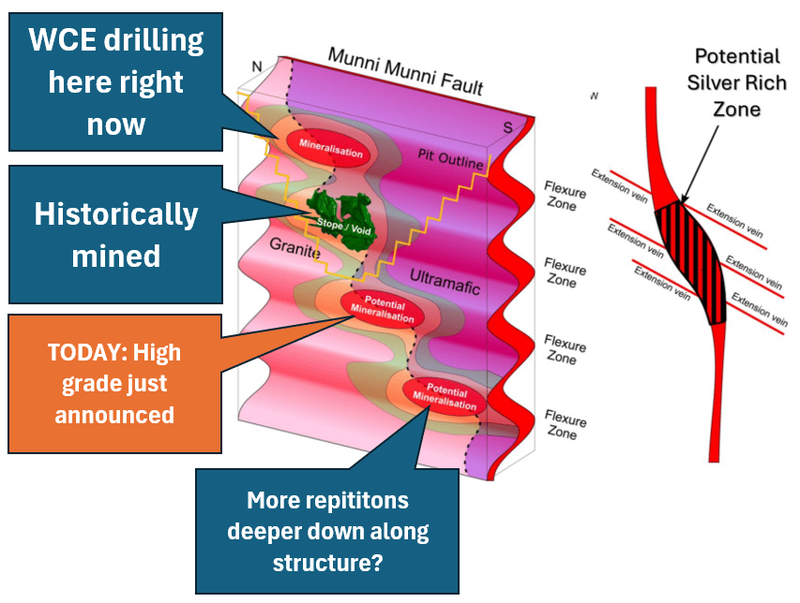

Three weeks ago, WCE revealed analysis by a geological consultant that said this type of system could have repeating extensions, in this way:

(source - read the full theory here)

Today’s announcement is a step towards proving this theory.

Just north enough of the existing resource that IF big enough it could be the starting hits to a “new Elizabeth Hill”.

BUT also, close enough so that if the structure isn’t big enough to be mined as a standalone new discovery - WCE COULD look to get in there with some sort of underground mining setup.

(source)

We are thinking very far ahead here - we are not mining engineers and it's probably too early to make a call on whether or not the structure WCE hit today would make sense to mine.

BUT it's starting to make sense in our head enough to visualise it...

(source)

All we need to see now is more drilling around that area so that “bright purple worm” that represents the inferred high grade silver mineralisation gets longer (and/or fatter) to the point where it becomes too hard to ignore...

(source)

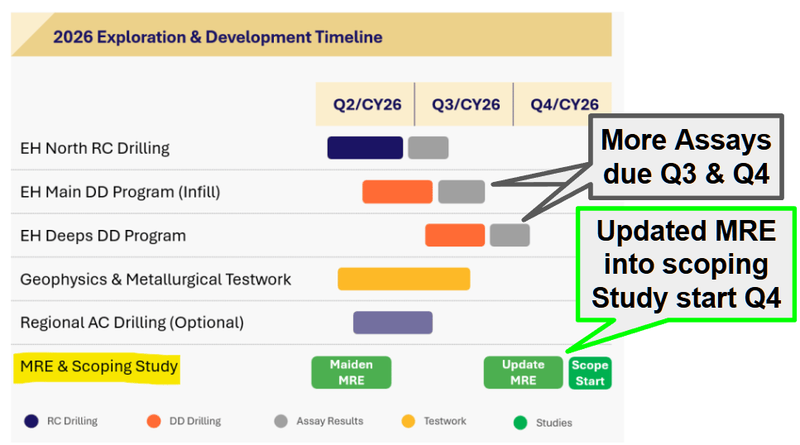

WCE is currently in the middle of its drilling program (with more assays expected through July and August)

So we may not have to wait that long to find out if there is any follow up to today’s hits.

(source)

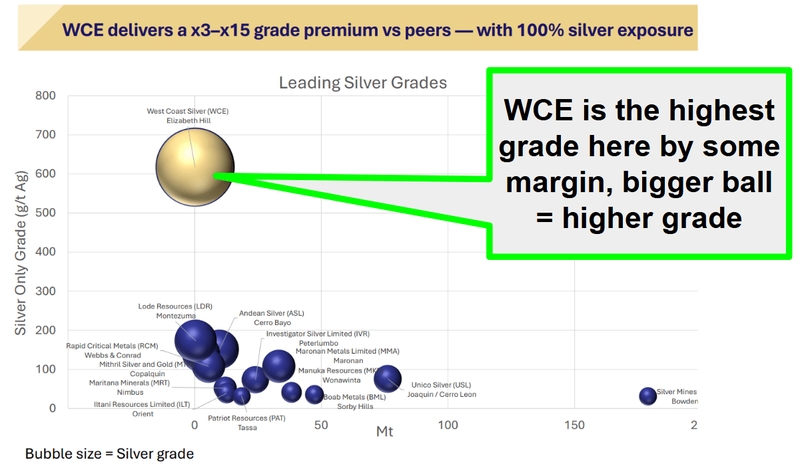

WCE’s project is already the highest grade on the ASX

Up until now, most of WCE’s drilling has gone into defining its maiden JORC resource estimate of 2.8M ounces of silver at ~617g/t. (announced back in April).

A solid start - making it the highest grade pure silver resource on the ASX by a big margin.

(source)

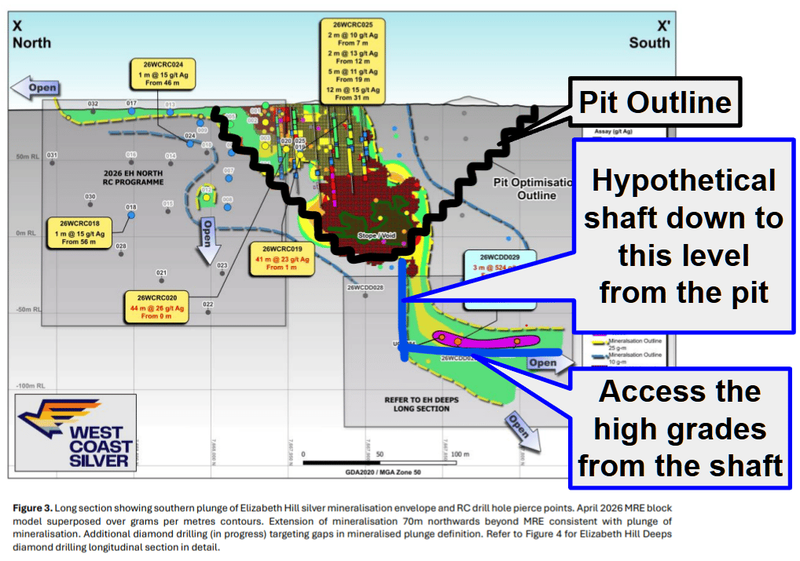

So far all of WCE’s ultra-high grade silver sits inside one optimised open-pit shell.

Meaning hypothetically WCE could just start digging out the current resource from surface.

(source)

The last time this project was mined back in the early 2000s it was done using underground mining methods.

So changing the nature of the deposit from underground to open-pit COULD be a big win for WCE.

WCE could have the highest grade deposit on the ASX that could be mined using well understood, low cost open-pit mining methods.

High grades = More silver comes out of each tonne of material mined.

Open-pit = cheaper and faster to run (literally just digging and blasting rock).

As mentioned earlier, IF that new purple worm starts to grow with more drilling, then underground mining could be back on for the project.

Maybe as a plug in into a development plan for AFTER all the near surface stuff gets mined.

Again we are not mining engineers and going underground will have costs, the new discovery will have to make sense economically to add into WCE’s resource/mine plan - there is no guarantee it makes that cut-off...

We should know more pretty soon though - WCE expects to have another updated resource estimate out between now and the end of the year, leading into a scoping study (expected to start in Q4-2026):

(source)

Here is everything we know about WCE’s project right now:

- WCE’s project sits on a granted Mining Lease (reducing permitting timelines)

- There is historic mine infrastructure on site (the project was last mined in 2000)

- The project is ~30km away from the Radio Hill processing plant (WCE has an MoU in place with the owners of that plant).

- We know that the project was previously mined using a very simple processing flowsheet (conventional gravity circuits only).

- Access to mine support services, infrastructure, port, rail, power and skilled labour in the major coastal iron ore mining hub city of Karratha, Western Australia (~45km by road).

So far WCE has made it relatively clear that its intention is to get the project back online with a high margin starter pit that is one single ~130m deep open pit. (source)

A low tonnage, high grade mine where WCE has already proven up to 90% silver recovery rates (so should be able to process with a relatively simple flowsheet).

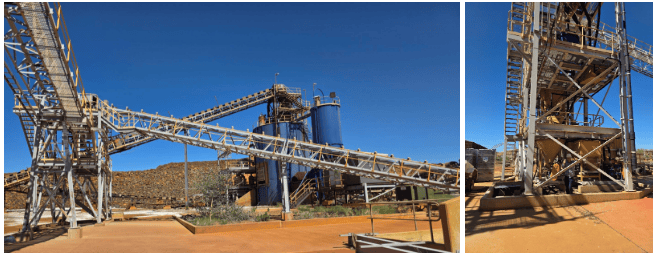

WCE also made it clear that one of the processing options it's considering for the mine would be from the Radio Hill processing plant ~30km away (WCE already has an MoU in place with the owners of that plant).

Here are some photos of that plant:

(source)

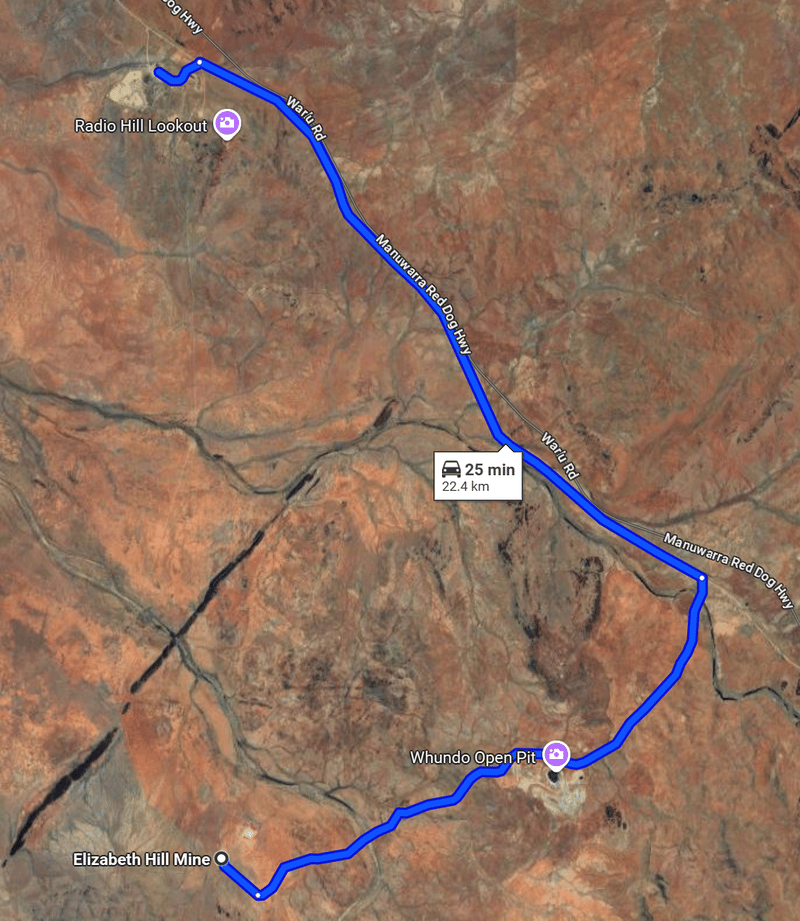

And here is where it sits relative to WCE’s project:

(source)

Ultimately, we are Invested in WCE to see it drill out and bring back online its silver project - repeating the types of mining runs done in the past (high grade, low tonnage) BUT this time into a silver market where prices are high.

Our WCE Big Bet:

“WCE re-rates to a market cap of $300M by bringing the Elizabeth Hill mine back online OR making a new discovery that is as big (if not bigger) than Elizabeth Hill into a strong macro silver theme.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our WCE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s going on with the silver price right now?

We think silver is currently going through that big washout that happens after a first big rally.

We think that fundamentally, nothing has changed with silver.

Forecasts are for a sixth year in a row the world uses more silver than it produces. (source)

It could start next week or in three years time, no one knows - but we think that at some point inside the next 2-3 years silver will go on a big run again.

If some of the chart gurus are to be believed then the moves in recent months were the first stage of the breakout, the current move lower is the retest of that move - and whatever happens next will be the real decisive move...

No guarantees of course. Commodity prices are very hard to forecast.

A few weeks ago on one of the biggest podcasts in the world (the All-In Podcast) - fund manager Dan Dreyfus laid out the bull case well saying:

- The world uses ~1.2 billion ounces of silver a year

- It only produces ~1 billion ounces a year

- That leaves a ~200M ounce hole every year - pulled from above-ground stocks

- And he reckons there’s only ~600M ounces of accessible above-ground inventory left

So Dan’s call is for an “above-ground” shortage at some point within the next three years.

On silver, he also said:

1. The China export cutoff list:

"Samarium, gadolinium, terbium, dysprosium, lutetium, scandium, yttrium, erbium, silver, just cut it off ."

2. The main silver block (one continuous passage, late in the talk):

"We're going to be short silver, for example, to build these solar panels, especially if we start launching data centers in space, right? These are going to consume incredible amounts of silver. But right now the silver supply demand dynamic is we consume 1.2 billion ounces a year. We supply a billion ounces a year. So there's a 200 million ounce deficit per year and we only have 600 million of above ground inventory left. So the clock's ticking. We got three years left guys before we just stock out. And then the solar story is where do you get the silver for the photovoltaic cells?"

3. His closing allocation comment:

"So for our kids and for the country generation tool belt for us allocating, get some exposure to copper, silver, minerals and then there's a bunch of service providers in and around that area that we should be investigating over the next year."

Check out Dan’s full pitch here: Dan Dreyfus: America’s Critical Minerals Crisis is Here

Dan’s thesis is pretty simple and based on above ground inventories being run down due to that deficit between production and demand.

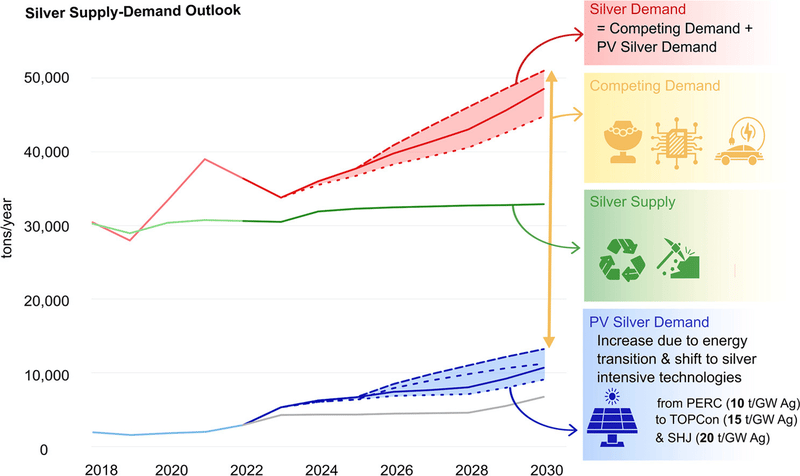

We think there is pressure on the demand side too...

- Solar panels alone now eat 200M+ ounces a year - roughly one-fifth of global mine supply (source)

- EVs, power grids, semiconductors and AI data centres all need silver (source)

So demand could be a lot stronger than even Dan is expecting:

(source)

As mentioned earlier, our favourite silver analyst, Michael Oliver is still calling for US$500 silver:

Silver Supercycle Begins Now! Massive Acceleration To $500 Silver Coming | Michael Oliver Silver

And billionaire Eric Sprott thinks silver “should be at US$300” and can “easily” get there.

Eric Sprott's CRITICAL Mid-Year 2026 Warning | Sprott Money

Hopefully, they are right and silver finds a new base around these current levels and starts to turn.

No one knows where prices go next though, in the short term the silver price will have an effect on how WCE’s share price trades.

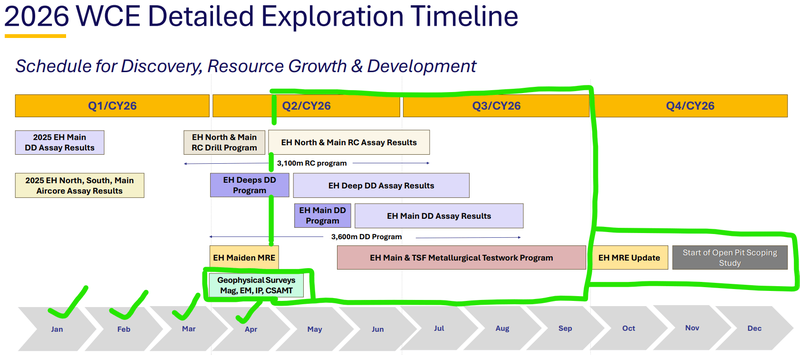

What’s next for WCE?

Here is WCE’s latest Gantt chart with everything we can expect to see over the coming months:

(source - WCE’s latest investor presentation)

In terms of exploration the three things we are looking out for are:

- The RC drill campaign on the targets to the north of the Elizabeth Hill Mine (happening now).

- The diamond drilling is going for at depth extensions to the Elizabeth Hill mine (started Mid April).

- Geophysics across the broader project area

And then all of that data rolling into what we expect to be an updated JORC resource being fed into a Scoping Study, expected to get underway in Q4.

Here are the milestones we are tracking right now:

- 🔄 Drilling results

- 🔲 Updated mineral resource estimate

- 🔲 Scoping study starts

- 🔲 Scoping study results

What could go wrong?

In the short term the key risk is around “exploration risk” and “commodity price risk”.

WCE is currently drilling surrounding the historical mine.

There is a risk WCE does not find enough economically viable mineralisation and the company’s share price re-rates lower.

Exploration risk

There is no guarantee that WCE’s upcoming drill programs are successful. WCE may fail to find economic deposits of silver.

Source: What could go wrong? - WCE Investment Memo 8 August 2025.

Right now, the silver price has pulled back significantly from its all time highs earlier in the year.

WCE’s primary commodity exposure is silver, so any further falls in the silver price could mean WCE’s share price moves lower.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver prices fall, this could hurt the WCE share price.

Source: What could go wrong? - WCE Investment Memo 8 August 2025.

Other risks

Like any early-stage exploration company, WCE carries significant risk, here we aim to identify a few more risks.

WCE's development strategy currently relies on a non-binding Memorandum of Understanding (MoU) to process its ore at the nearby Radio Hill plant. If the company is unable to secure a final, legally binding commercial agreement on favorable terms, it could face major project delays or the heavy capital burden of building its own processing infrastructure.

While near-surface silver can be extracted via a low-cost open pit, any future development targeting deeper high-grade structures will likely require underground mining. Shifting underground introduces much higher operational costs and engineering complexities, and there is no guarantee that these deep zones will meet the economic cut-off requirements to justify mining.

Funding an active drilling campaign alongside a scoping study scheduled for Q4 2026 requires substantial ongoing capital. WCE will likely need to execute further capital raises to fund these operational milestones, which introduces an imminent risk of equity dilution for existing shareholders.

The company is working toward delivering an updated mineral resource estimate before the end of the year. Any unforeseen delays in receiving assay results or completing these technical studies could stall development momentum and negatively impact the stock price.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our WCE Investment Memo

In our WCE Investment Memo, you can find the following:

- What does WCE do?

- The macro theme for WCE

- Our WCE Big Bet

- What we want to see WCE achieve

- Why we are Invested in WCE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.