ONE strengthening its partnership with Baxter International

Our health tech Investment Oneview Healthcare (ASX: ONE), which has now rebranded as simply Oneview, is making further progress with its partner Baxter International.

ONE has a Value Added Reseller (VAR) agreement with Baxter - the largest supplier of US hospital beds.

We caught a glimpse of this particular picture from Baxter International’s most recent appearance at a trade conference:

Baxter is now co-branding with Oneview, which we think is an important indication that Baxter intends to put Oneview's health tech solutions front and centre of future sales initiatives.

Baxter has already delivered the following deals for ONE:

Read more about why we think the Baxter VAR agreement could be crucial for ONE here:

US$18BN Baxter extends US reseller deal with ONE, expands to Canada.

Our hope is that Baxter is able to dramatically expand ONE’s sales pipeline, and ultimately close enough deals to make ONE the rapidly growing SaaS company that we think it can be.

ONE moving into AI…

We really like this latest bit of news concerning ONE’s latest AI initiative:

(Source)

The product is called Ovie, a “An innovative new GenAI product that provides personalized, real-time support for patients and families throughout their hospital stay.”

The US healthcare system is under immense strain - with well documented things like nurse shortages, high labour costs and overworked clinicians.

We hope that ONE can play a role in improving the customer care experience, and in doing so, secure another sustained re-rate.

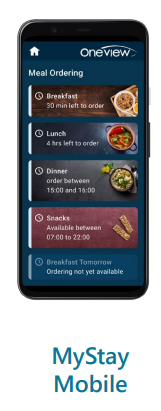

ONE’s move into the AI space, could enhance its ability to become a fast growing SaaS company, in concert with its mobile product, MyStay:

What did we learn in ONE’s latest quarterly?

We reviewed ONE’s latest quarterly, and our overall take is that there have been a few hiccups along the way in the past quarter.

But the overall trajectory remains positive.

ONE noted some impacts from brewing trade tensions between the US and China, and the steps it has taken to mitigate these risks with regards to hardware.

The company also mentioned, “Marginally higher staff and admin costs for the quarter also contribute to the higher outflow as the Company resources the fulfilment of recent new signings and the Baxter pipeline.”

That last bit sounds good to us.

Especially in light of this tidbit from the latest ONE quarterly:

(Source)

We note the following other key points from ONE’s latest quarterly:

- Cash balance of €13.8M (~$23M) as of December 31, 2024

- Successful capital raise of ~$23M, including $20M from institutional investors and $3M from an oversubscribed Security Purchase Plan

- 23% increase in contracted beds during 2024, from 15,821 to 19,429

- 23% increase in live beds during 2024, from 10,151 to 12,514

- Net operating cash outflow of €4.1M for the quarter

What’s next for ONE?

More contracted beds and a transition to the more smoothed out revenue streams of a true SaaS model with MyStay.

We want to see ONE hit 25,000 beds - it’s our number one objective for ONE in our ONE Investment Memo.

We think by hitting all the objectives in that Investment Memo it will move ONE closer to realising our ultimate upside scenario for our ONE Investment, our ONE Big Bet:

Our ONE Big Bet:

ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1Bn valuation (based on 5x to 10x forward ARR multiple) and be acquired by a large health tech provider.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

We’ll be looking out closely for ONE to seal the remaining contracts in late stage negotiations and start to see Baxter’s 100 person strong salesforce deliver results.