KAU completes acquisition of 30k ounce per annum Henty Mine

Our gold producing Investment Kaiser Reef (ASX: KAU) just completed the acquisition of the Henty gold mine in Tasmania.

So right now, KAU has 100% ownership over a project that is producing ~30k ounces of gold per annum.

For the first three months of the year, Henty produced 6,064 ounces at an All In Sustaining Cost (AISC) of A$3,283/ounce.

(Source - Catalyst Metals quarterly report)

Based on current gold prices (~A$5,000 per ounce) that level of production at those costs would net the owner of the mine ~$10M in three months.

That is $10M after all costs are considered in just three months, annualised that would mean $40M for the owner of the project.

KAU’s upfront consideration is ~$31.6M for the project, and if we see a few more quarters similar to the last one, KAU could technically self-fund its acquisition in under 12 months of owning the mine.

KAU today is capped at ~$98M.

Lets not forget KAU is also producing gold from its A1 gold mine in Victoria which for the first time in ~X years is mining never before touched virgin parts of that project.

We think there is scope for KAU to deliver a surprise big quarter from this project and surprise the market with even more production than is being priced into KAU’s share price right now.

KAU keeps talking about becoming a 50k ounce+ per annum producer, we think A1 is part of that plan…

(Source)

We did a deep dive on what KAU is taking over in our last KAU note here: KAU’s new Henty gold mine acquisition produces 6,064 ounces over 3 months. KAU takes ownership in 18 days…?

9 Reasons why we like KAU’s Henty acquisition:

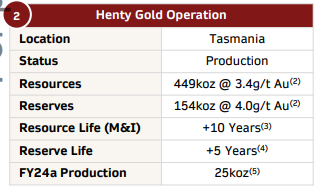

1. Producing mine with existing resources + reserves base

The Henty gold operation is currently producing ~5,000 to 6,000 ounces of gold per quarter. The project also has 5+ years of mine life in reserves and over 10 years of mine life in resources.

(Source)

2. The project could generate ~$120M in revenues per annum at today’s gold price

Henty produced 25k ounces in 2024 (KAU is looking to grow this number in 2025). At current gold prices, that would be ~$120M in revenues per annum. With all in costs averaging ~A$2,500/oz for Henty in 2024, KAU should be able to turn those revenues into free cashflows in the current gold environment.

(Source)

3. Henty has $100M+ of existing infrastructure

The Henty Gold Operations has an existing 300ktpa processing plant, a mining fleet/inventory and tailings storage/underground declines with replacement value greater than $100M. KAU gets to benefit from all the capital that’s gone into the asset to date.

(Source)

4. Exploration potential untapped to date

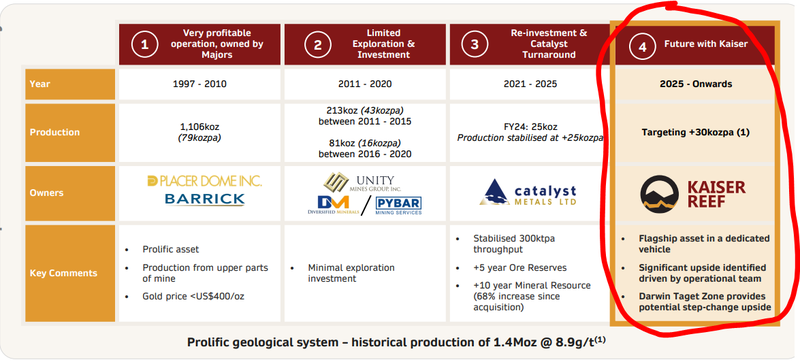

KAU is taking over the project after previous operators focused on ironing out production efficiencies. With the cashflow from operations at record gold prices, KAU can drill out the project to extend the project's mine life.

5. Acquiring a big gold asset has worked for other ASX companies

Northern Star was capped at $7M when it made its first big acquisition for $40M. 25 years later and several other acquisitions later Northern Star is capped at $20BN.

$1.7BN Bellevue Gold also started with a market cap of ~$2M before making acquisitions to become what it is today. There is a precedent for gold M&A to work in the long run.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

6. KAU’s Exec director Brad Valiukas has experience maximising value from assets like these and is now working full time on Henty and A1

Brad was Manager for Technical Services at Northern Star during 2015-2019. His role was spread across the entire Northern Star portfolio and he helped set up the foundations for assets like Jundee to be the cornerstone of the $20BN producers project portfolio.

Certainly a good guy to have on the KAU team, extracting the most profits from Henty and its Victorian assets.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

7. KAU now has two operating mines

KAU will now have a diversified production profile. Once the A1 mine production lifts to closer to Henty’s production, if one mine has a bad quarter, the other one could fill in the gaps temporarily. A smoother, more predictable production profile may attract institutional investors who want less volatile gold production exposure.

8. KAU market cap can grow to a size where institutional money can come in

The ASX gold space has had a lot of M&A deals get done over the last 12-18 months. Most of those deals are to grow in size/scale as quickly as possible so that the producers can attract investment from institutional/passive funds. KAU post-deal will have a market cap of $83M, which is approaching a level where these funds may be able to invest.

9. KAU is acquiring a non-core asset from $1BN company

Vendor of the asset Catalyst looks like it wants to focus all of its time and effort on its WA assets. KAU can now take Henty and give it the time & capital it needs to be a big part of a company’s portfolio. What might not be core for a $1BN company, can be a great foundational asset for a <$100M producer like KAU.