TrivarX (ASX:TRI) is developing cancer diagnostics IP.

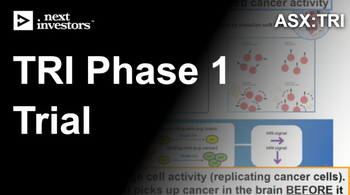

TRI's technology uses stable isotopes to label replicating cells inside the brain (the type of cells that help identify cancer) - detectable via standard MRI.

What is the macro theme?

Finding cancer early.

5-year survival for cancers that move from one part of the body into the brain is 6.1%, compared with 71.5% for cancer patients where the cancer never reaches the brain.

Current standard-of-care MRI imaging can only detect tumours once they reach 2-3mm - by which point the tumour is already structurally established in the brain.

There is no approved non-invasive imaging method capable of identifying tumour cell replication at high levels of sensitivity. (source)

We are Invested in TRI to try and develop a solution.

Our Big Bet for TRI

"TRI re-rates to a $300M+ market cap on successful clinical trial progress for its cancer diagnostics IP, and/or is acquired for multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including clinical trials, commercialisation and regulatory risks - just some of which we list in our TRI Investment Memo (see below).

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Why did we invest in TRI?

Dr Daniel Tillett has delivered in the past for ASX investors - we are backing him again here

Dr Daniel Tillett is the inventor of TRI's new tech (Stabl-Im) and the CEO & Managing Director of ASX-listed Racura Oncology (ASX: RAC) - currently capped at ~A$400M+.

Tillett put $500k of his own money into TRI at 0.8c per share to fund the Stabl-Im acquisition.

He is also signed on as ongoing technical advisor through the clinical program.

Past performance of Racura Oncology is not and should not be taken as an indication of future performance of TRI.

Same backers behind our 2025 Biotech Pick of The Year

TRI shares board members and major shareholders with our 2025 Biotech Pick of the Year - Island Pharmaceuticals (ASX: ILA).

ILA is up 163% from our Initial Entry Price.

Dr Daniel Tillett (ILA’s biggest shareholder) is also a major shareholder in TRI AND vended in TRI’s new tech.

Chris Ntoumenopoulos is director of both TRI and ILA and he was part of the team that sold Resapp to pharma giant Pfizer for $180M.

These two are part of the same team driving ILA, our 2025 biotech Pick of The Year.

Brain-tumour imaging that could be a game changer

TRI’s tech uses stable (non-radioactive) isotopes to label replicating cells in the brain which can then be detected using standard MRI.

5-year survival for cancers that move from one part of the body into the brain is 6.1%, compared with 71.5% for cancer patients where the cancer never reaches the brain.

Current standard-of-care MRI imaging can only detect tumours once they reach 2-3mm - by which point the tumour is already structurally established in the brain.

There is no approved non-invasive imaging method capable of identifying tumour cell replication at high levels of sensitivity. (source)

TRI’s tech (IF it works) will be able to solve that early detection problem.

The ASX understands these stories.

The ASX has a strong history of pricing breakthrough diagnostic / imaging biotechs.

Telix Pharmaceuticals was a favourite amongst small cap investors, IPO’ing at $50M at 65c per share in late 2017 and peaking near $32 in early 2025 at a cap of ~$10.7BN.

Another one was Clarity Pharmaceuticals which IPO’ed at $358M at $1.40 per share in 2021, peaking near $9 in 2024 at a cap of ~$3BN.

So the ASX understands and is willing to re-rate companies that have success in this space.

A peer comp is approaching a ~$5BN market cap

~$5BN Telix Pharmaceuticals has its brain-tumour-imaging product Pixclara which has received both Fast Track and Orphan Drug designations from the FDA

The FDA accepted Telix’s New Drug Application (NDA) and should be making a call on approvals before the end of the 2026

We think that validates the regulatory pathway for TRI.

AND it shows how the market may value a company developing brain tumour imaging tech successfully.

Past performance of Telix is not and should not be taken as an indication of future performance of TRI.

TRI just appointed Telix’s ex- Chief Medical Officer

Dr Danielle Meyrick (PhD, MD) starts as CEO on 1 June 2026.

Previously Chief Medical Officer (APAC) and Global Head of Clinical Science at Telix Pharmaceuticals (ASX: TLX, ~A$5BN).

Before that, CMO at ITM Isotope Technologies Munich (a global leader in isotope therapeutics).

We think Dr Danielle has the right CV to advance TRI’s tech.

We also like that all of her incentives are tied directly to clinical & FDA milestones.

Small market cap relative to addressable opportunity

TRI's market cap is currently ~A$30M.

The neuro-oncology diagnostic market was ~US$650M in 2025. (source)

The bigger market is for treatments when cancer moves from one part of the body into the brain (brain metastases).

That market is forecast to be ~US$8.5BN by 2035.

So an early detection tool could be valuable both in diagnostics and for companies providing treatments.

Free hit on TRI’s AI for detecting Current Major Depressive Episodes.

TRI still has its AI algorithm for detecting current Major Depressive Episodes (cMDE) using sleep data (MEB-001).

TRI is looking to commercialise the tech right now.

IF anything comes from this it will be an added bonus for us.

What do we expect TRI to deliver?

Objective #1: Phase 1 human safety trial

We want to see TRI’s tech tested in patients with confirmed brain tumours, to demonstrate safety, imaging precision, and reliability.

Milestones

Complete trial design

Manufacture stable isotope compounds

Animal efficacy studies & results

First-in-human dose

Phase 1 trial completed

Phase 1 trial results

Objective #2: Phase 2 Imaging Study

Assuming phase 1 is successful we want to see TRI run a phase 2 imaging study.

Milestones

Phase 2 study design

Phase 2 trial commencement

Phase 2 trial completed

Phase 2 results published

Objective #3: FDA Regulatory Pathway

While the trials happen we also want to see TRI go through the regulatory process with the FDA.

Milestones

Pre-IND (Investigational New Drug) meeting with FDA

IND application submitted

FDA approved IND for TRI’s tech

(bonus) FDA Fast Track / Breakthrough / Orphan designation

We don’t really have a timeframe for this one but ultimately, a big win for our Investment in TRI would be to see a re-rate through either a takeover or a licensing/partnership deal.

Milestones

Licensing or partnership discussions with global imaging / pharma majors

Strategic investment from a bigger company or an outright takeover.

What could go wrong?

Clinical trial risk

TRI’s new technology is pre-clinical.

There is no guarantee that Phase 1 delivers safe, well-tolerated dosing - OR that any subsequent Phase 2 trial delivers statistically significant efficacy. Many pre-clinical biotechs fail at first-in-human studies.

Regulatory risk

FDA approvals are not guaranteed. The agency may require additional data, longer studies, or different trial designs. Adverse outcomes from regulators could materially hurt the TRI share price.

Funding & dilution risk

TRI is pre-revenue. Phase 1 / Phase 2 trial costs typically run into millions of dollars per program. Additional capital raises are highly likely and may dilute existing shareholders, potentially at a discount to prevailing share prices.

Market risk

Speculative biotechs are highly sensitive to broader market sentiment. If the biotech sector or small-cap sentiment sells off, TRI's share price could drift regardless of operational progress.

IP / Patent risk

The IP being acquired covers "all intellectual property associated with novel brain imaging technology, the Stabl-Im metastatic brain technology." There is no specific patent number or jurisdiction reference in the announcement - investors should not assume granted patents in all major markets.

Other risks

Like any small-cap healthcare technology company, TRI carries significant risk, here we aim to identify a few more risks.

First, because the newly acquired Stabl-Im technology is entirely pre-clinical, there is an inherent risk that upcoming Phase 1 trials may fail to demonstrate human safety.

Any negative trial data or unexpected toxicity could halt development before the platform ever reaches commercial viability.

The company also faces intense adoption and commercialisation hurdles even if the technology achieves regulatory clearance.

Navigating medical sales cycles and competing against established giants like Telix Pharmaceuticals means capturing commercial market share is far from guaranteed.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our investment plan?

Our Investment Plan for TRI is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the results of the Phase 2 clinical trial results, a commercialisation deal, a macro triggering event or any other reason, we may look to sell up to ~20% of our holding. See our general hold policy for more details.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 23,820,000 TRI Shares at the time of publishing this Investment Memo. The Company has been engaged by TRI to share our commentary on the progress of our Investment in TRI over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Investment Memo:

TrivarX Ltd

(ASX:TRI)

-

LIVE

Opened: 02-May-2024

Shares Held at Open: 18,820,000

What does TRI do?

Trivarx (ASX:TRI) is an AI-driven mental health technology company seeking to commercialise objective measures to aid in the early detection and screening of mental health conditions, such as depression.

What is the macro theme?

We expect technology to play an increasingly important role in mental health care - FDA approvals for medtech algorithms have ramped up dramatically in the last few years. But there are few algorithms for the mental health space. Billions of dollars are being invested in mental health technology companies and startups, and AI is one of the hottest investment thematics right now.

Our Big Bet for TRI

"TRI re-rates to a $300M+ market cap on successful clinical trial progress for its cancer diagnostics IP, and/or is acquired for multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including clinical trials, commercialisation and regulatory risks - just some of which we list in our TRI Investment Memo (see below).

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Why did we invest in TRI?

1. Screening for mental health issues from sleep data

novel solution to a serious problem. Current methods to screen for mental health are subjective and inaccurate, resulting in patients not receiving the right treatment. TRI is using AI to analyse sleep data to provide objective, accurate screening for mental health issues.

2. Genuine AI (Artificial Intelligence) exposure

TRI didn’t just start working with AI once it became a popular investment thematic in recent months. TRI has a Head of AI, Dr Massimiliano Grassi, who has been doing AI for psychiatry for at least 6 years. TRI’s algorithm has advanced to Phase 2 trials and is getting better as time passes and more data is collected.

3. ~$11M market cap - undervalued and unloved Medtech?

like our successful Investment in Oneview, our view is that TRI is undervalued at ~$11M considering the 9 years of investment into its tech & with a Phase 2 trial being run. We think this is a great entry after years of hard work with the right team to take TRI forward now in place.

4. Imminent Phase 2 clinical trial results

400 patients sleep data is being screened for depression using TRI. IF the trial result is positive, it could open the door to US FDA regulatory approvals and potentially even training the AI algorithm to screen for other types of mental health issues too. The final results are expected in the next couple of months. We think they will be a catalyst for TRI’s share price.

TRI has engaged with the FDA and the De Novo pathway was defined by the regulator, a type of FDA approval which is generally longer and more rigorous but reserved for genuinely new medical devices, which we think TRI’s algorithm is.

TRI has a US-based tech team and is going for the lucrative US healthcare market - which is the huge, clearly trodden pathway for big exits in biotech/medtech.

7. Near term revenue opportunities (Stager) - US$15BN market

Commercial roll-out of TRI’s sleep staging software for sleep clinics - commercialisation is underway with licensing agreements and partnerships anticipated 2024. TRI’s novel products are aimed at sleep research organisations in the US, targeting the US$15 billion sleep medicine market.

8. Proven new management team with key backers

recently appointed board and management team with significant success in US and global healthcare markets, including founding directors/financiers of Race Oncology ($600m+ market cap 2021) and ResApp Health, which Pfizer ended up taking over for ~$180M in 2022.

9. Long term technical team retained (AI experts and human brain experts)

Neurosurgeon Dr Defillo and AI specialist Dr Grassi are the brains behind TRI’s tech - they’ve been involved together since 2019 and both bring a special skill set that we think will drive TRI’s success.

10. Major shareholder is Fidelity Investments

one of the largest fund managers in the U.S, is the #1 shareholder in TRI with a ~10% holding in the company.

11. Potential to screen for other psychiatric disorders

if it turns out that sleep data CAN successfully be analysed by its AI to screen for depression, it is possible that the AI can be trained to screen for OTHER mental health issues too.

12. Potential to integrate TRI’s tech into wearables

TRI’s tech may potentially be integrated into wearables like a Fitbit, Apple Watch or Oura Ring that all track simplified sleep data. That’s a big commercial opportunity in our eyes.

TRI is currently conducting a Phase 2 trial in the US on its algorithm for detecting current Major Depressive Episode (cMDE). Final results are expected in the June quarter (before July 1st 2024).

Objective #2: Regulatory approval - FDA De Novo application

TRI will be engaging with the US health regulator (FDA) to bring its product to market. This involves an De Novo application - which would classify its product as “low-risk” and therefore help speed up the approvals process and get TRI’s product to market quicker.

We want TRI to appoint a Managing Director or CEO with the right skills and experience to take TRI’s product into the market. After that we want to see the company sign commercialisation deals. TRI is currently undertaking an executive search for the role.

Milestones

CEO search starts

CEO appointed

Licensing deal #1 - Stager software

Licensing deal #2 - AI depression screening algorithm

Objective #4: Complete Pivotal Study

Today we are adding a new objective to the TRI Investment Memo. Now that it has completed its Phase 2 trial and published the results, the company will look to complete a Pivotal Study.

We had not yet added it as an objective as it was conditioned on the data collected by the company, however it appears that this Pivotal study will be the best way forward for the company to achieve FDA approval.

Milestones

Complete Pivotal Study Design

Appoint CRO for Pivotal Study

IRB Approval for Pivotal Study

Commence Pivotal Trial

Interim Results

Complete Recruitment

Final Results

What could go wrong?

Regulatory risk

It is possible that health regulators do not approve a new screening product like TRI’s. The regulator could require additional data, or reject the application outright. TRI has previously failed with a “Breakthrough” FDA designation and despite taking a more streamlined approach to regulatory approval - this approval is not guaranteed. An adverse outcome from the regulator could hurt the TRI share price.

Competition risk

AI is accelerating at a significant rate - new market entrants could make TRI’s product for depression screening redundant.

Clinical trial risk

Clinical trial outcomes are never certain - TRI might not be able to generate results good enough for the regulator to approve the product. Clinical trials, even low cost ones, require capital in order to be conducted. A clinical validation study, which TRI may also have to complete could cost additional money.

Small caps often need to raise cash to fund their growth. TRI is not generating any revenue and may need to raise capital, potentially at a discount. Capital raises may dilute existing holders.

Broader market sentiment can get worse and speculative stocks as a whole trade lower, taking TRI’s share price with it. Alternatively, there could be further sector specific pain ahead. For example, the biotech sector sells down.

What is our investment plan?

Our Investment Plan for TRI is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the results of the Phase 2 clinical trial results, a commercialisation deal, a macro triggering event or any other unknown reason, we may look to sell up to ~20% of our holding. See our general hold policy for more details.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 18,820,000 TRI shares at the time of publishing this article. The Company has been engaged by TRI to share our commentary on the progress of our Investment in TRI over time. 14,000,000 shares are subject to shareholder approval.