TTM: We will tackle the gold, Gina - you get to the copper

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,516,823 TTM shares at the time of publishing this article. The Company has been engaged by TTM to share our commentary on the progress of our Investment in TTM over time.

The gold price just hit new highs overnight.

The highest it has EVER been...

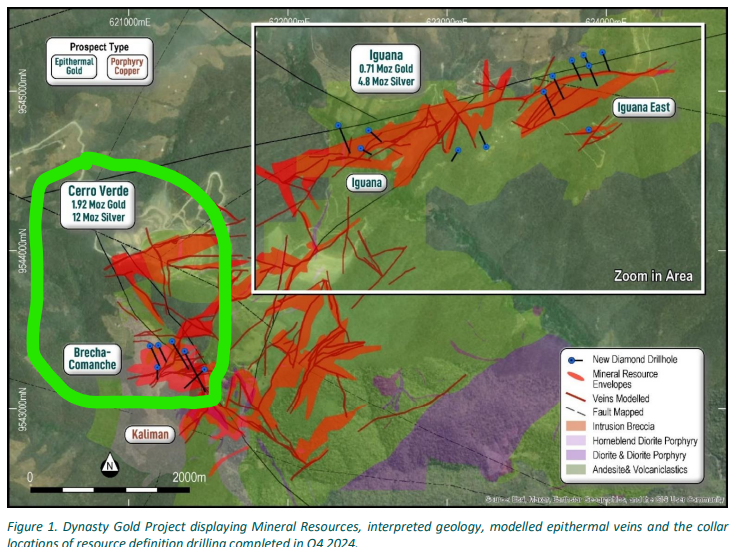

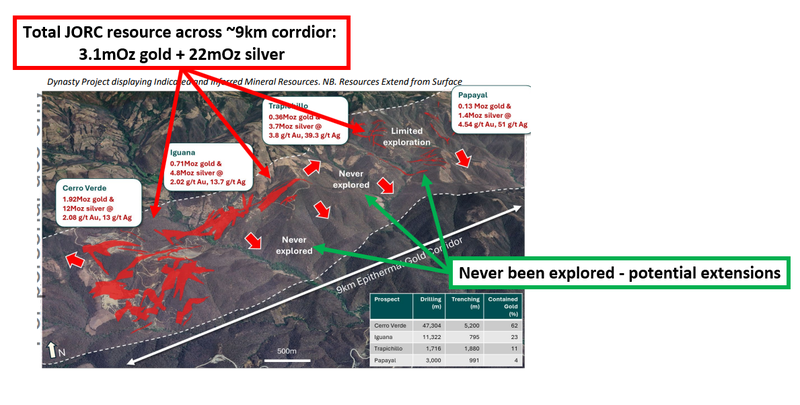

$99M capped Titan Minerals (ASX:TTM) has a 3.1 million ounce gold + 22 million ounce silver resource.

(we’ll explain how such a small company like TTM owns an asset like this later)

Last month TTM raised $20M at 44c per share (above today’s price)

And suddenly there’s THREE drill rigs on site right now beavering away.

TTM is drilling to significantly grow its 3 million ounce resource by the middle of the year - and it now has the funding runway to do it.

The gold price has been on epic run, especially overnight:

Media headlines from the last 24 hours speculate on a number of reasons for last night's gold price surge, but it's really anyone’s guess:

(Source)

(Source)

The key takeaway is that for whatever the reason there is continued interest and price surges in gold...

... which is what TTM needs to attract interest and capital to grow and develop its project.

If TTM delivers more decent drill results AND materially increases their 3Moz gold resource in the coming months, we think it will open the doors for joint venture discussions to develop the gold project... or maybe even takeover interest?

TTM has already proven to the market it can execute joint venture development deals on big projects.

Aside from its 3Moz gold project, TTM also owns a copper porphyry project with some big copper drill hits but needs a lot more drilling to fully develop.

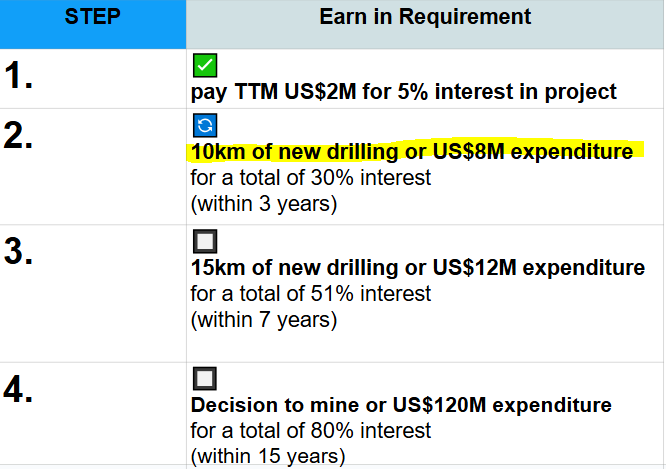

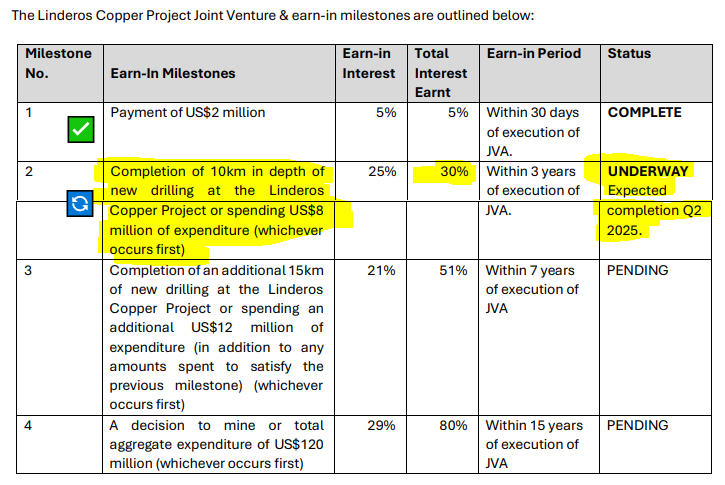

Back in September 2024, TTM finalised a deal with a Gina Rinehart subsidiary where TTM basically gets free carried on US$120M of drilling and development.

In return for spending this US$120M a Gina Rinehart company will earn in 80% of the project.

Here is our simplified explainer of the JV milestones

(full JV deal terms here - Source)

So if all goes well, and Gina develops this massive copper project, TTM could end up with 20% of a potential copper mine.

The next thing we are watching out for on TTM’s copper project is the first assay results from the JV partner’s drilling.

This morning TTM revealed they are in the healthiest financial position they have been in for years.

TTM released its quarterly report, showing the company had US$11.6M ($18.8M AUD) in cash as of December 31st.

(After that $20M capital raise in December, TTM is finally debt free for the first time in many years)

Yesterday it also confirmed that its “in the money” options are being underwritten up to $2.8M.

All this cash is going into drilling to grow its 3Moz gold JORC resource to an even bigger (and more certain) resource.

While Gina Rinehart's team pumps up to US $120M into drilling out and developing TTM’s copper project to earn-in an 80% share.

The bigger the resource, typically the higher the market values your company - especially in a high commodity price environment like gold.

Now armed with a large A$18.8M cash pile, over the coming months we are expecting TTM to:

- More drilling results from its Dynasty Gold project

- An upgrade to its Dynasty JORC resource by mid 2025. (once drilling is complete and the resource models are updated)

- Drilling results from the copper JV with Gina

- A scoping study for Dynasty in the second half of 2025.

Today we will unpack where TTM is and what we are looking forward to over the coming months.

TTM’s December raise attracted some big institutional investors, with Tribeca Partners increasing its position from 5.37% to 14.12% of the company.

Tribeca has billions of dollars in funds under management and are specialist resource investors - so clearly know their way around the resources investing game.

TTM has always had a strong institutional presence on the cap table, and the December raise continued this form.

It's a good sign that the TTM assets are quality assets, and the management team knows what it is doing.

We like to co-invest alongside the bigger sophisticated funds given they have teams of professionals running their due diligence process and have a track record of making money.

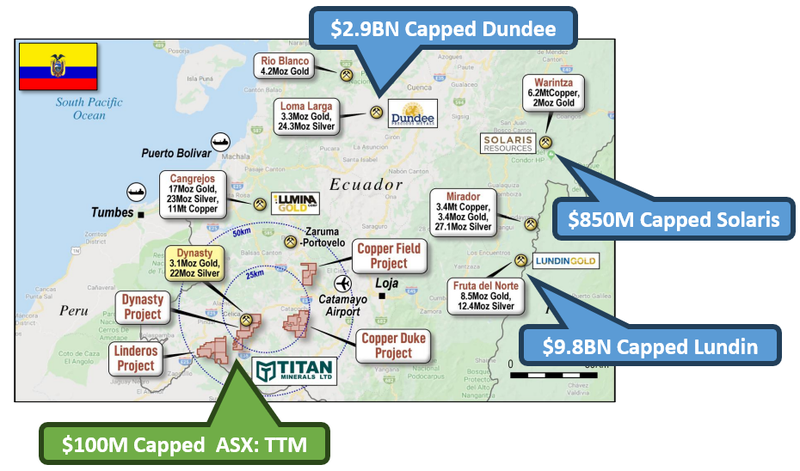

The part of Ecuador where TTM’s assets sit is jam-packed with multi million ounce mega assets - almost all of which are owned by majors like $2.9BN Dundee Precious Metals and $9.8BN Lundin Gold.

(another reason why we think TTM, assuming the geology stacks up, could be considered a future M&A target)

TTM has already managed to bring in Gina Rinehart's Hancock Prosecting (via subsidiary Hanrine) for one of its assets in a US$120M farm-in deal where TTM is free carried to a decision to mine.

(Gina's Hancock Prospecting is one of the biggest private mining conglomerates in the world.)

If TTM can drill out and upgrade its 3M ounce Dynasty project then there is a chance that project starts to pop up on the majors radars too.

A running gold price is when interest in these mega projects will be highest too.

A quick history lesson - where TTM was and where it could go...

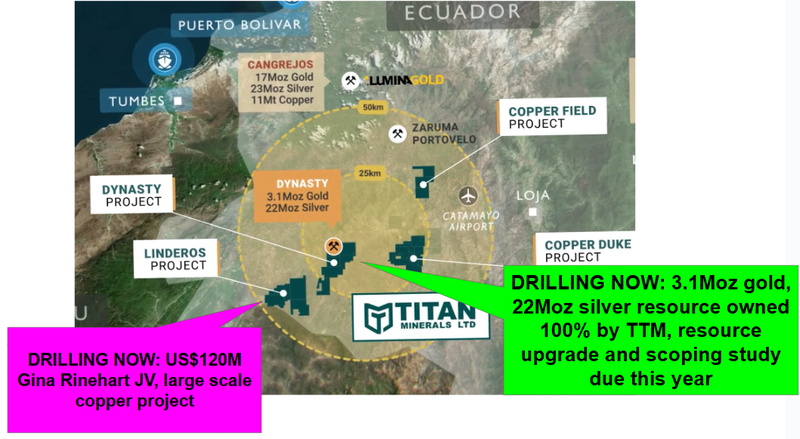

So how did a $99M capped company get hold of such big and valuable copper, silver and gold assets?

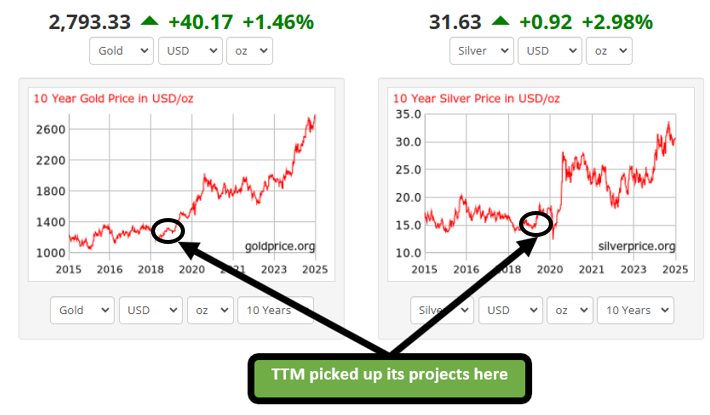

TTM picked up these assets when the market didn't really care too much about gold, silver or copper...

In early 2019 TTM and Core Gold (then a TSX listed company) came together to form what TTM is today.

(Source)

The pro-forma market cap of the combined company was over $180M at the time of the merger - remember today TTM is actually capped at circa $100M with $18M in cash, despite advancing the assets in recent years.

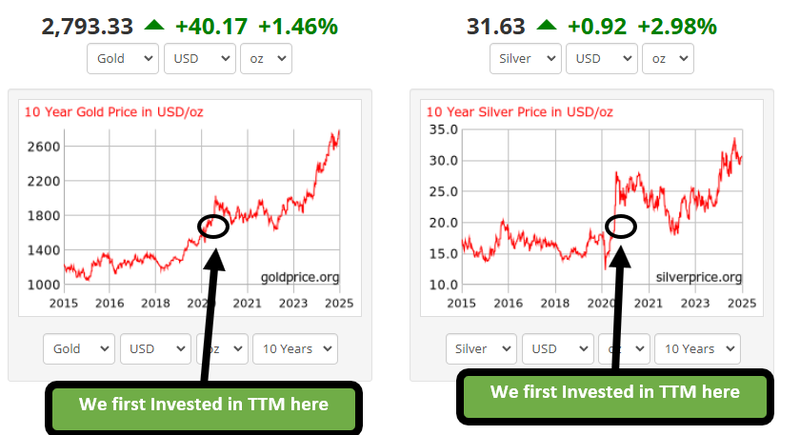

When that 2019 deal was done, the gold price was US$1,300 per ounce (now ~US $2,800) and the silver price close to decade lows at ~US$15 per ounce (now ~US $31.5).

(if only we could go back in time and load up on gold and silver then)

Since the 2019 deal, gold and silver prices have almost doubled.

The copper asset that Gina is now farming into was just an early stage exploration asset.

TTM has managed to put out a maiden JORC resource AND attract the likes of Gina to its copper asset with a US $120M deal to earn-in to 80% of this project.

So with 3m ounces of gold and 22m ounces of silver we think there is a good chance TTM could surpass that $180M valuation from 2019 when gold and silver were half where they are today.

(which would almost double its share price from current levels)

Gold had a huge 2024, and is having an even stronger start to 2025.

Usually when a commodity like gold runs, gold companies share prices respond upwards in this order:

- Companies producing and selling gold first,

- Companies with JORC defined gold resources second;

- And those exploring for gold third.

Most of the profitable producers are trading near all time highs.

As long as gold prices stay where they are, we think companies like TTM (with defined in the ground resources) will be the ones to run to new highs next.

We first Invested in TTM ~4 years ago and ever since (partially because of a lack of investor interest in gold stocks) the company had been scraping through by the skin of its teeth...

TTM never had more than $5M in the bank account at any given time but now after a strong $20M raise the company has cash to drill out its 3.1M ounce gold + 22M ounce silver resource in Ecuador.

(and a cashed up partner on its copper asset).

TTM is drilling right now, and for the first time in 4 years we get to see the company “aggressively drill” its projects with the cash runway to support it.

Drilling and progressing its projects forms the basis for our TTM Big Bet which is as follows:

Our TTM Big Bet:

“We want to see TTM prove up a $1BN plus copper or gold discovery in Ecuador which is so attractive that a mining major acquires the company.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our TTM Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

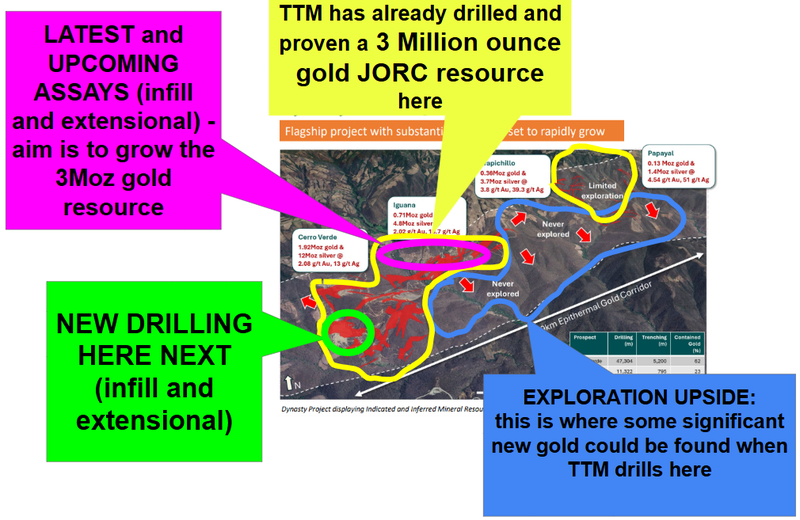

How TTM can upgrade its 3moz gold + 22moz silver Resource

Yesterday TTM put out a batch of drill results from the drilling the company has been doing over the past few months.

TTM is currently 4,600m through a 10,000m drill program.

Most of those results came from parts of TTM’s project where the existing 3m ounce gold + 22m ounce silver sits.

Next, TTM is moving west to the outer limits of its resource (Cerro Verde), with some focus on extensional drilling as well as some more infill drilling.

Cerro Verde hosts the majority of Dynasty’s existing resource - so it’s a fertile area to go drilling in. This drilling will likely focus on resource classification upgrade in addition to resource growth:

Off the back of current drilling, TTM expects to upgrade its resource in mid 2025 before a scoping study in the second half of this year.

Where we think the big resource upgrades could come from

Most of the drilling to date has been infill/extensional across TTM’s existing JORC resource.

But we think the big exploration upside is from the areas that sit between the JORC resource.

At the moment, TTM is doing a round of trenching trying to pick which parts of this area to drill.

After the trenching results we are looking forward to seeing TTM drill these areas.

The latest from TTM’s Copper JV with Gina Rinehart

We also got an update on where the copper JV with Gina is at in today’s quarterly.

So far the JV has started a 10,000m of drilling program which TTM said they expect to be completed by Q2-2025.

This drilling formed part of the earn-in agreement with TTM’s Joint Venture partner Hanrine (a wholly owned subsidiary of Gina Rinehart’s Hancock Prospecting).

Results from the first 10,000m should come in progressively over the coming months (hopefully we see some strong results).

If the results are good, we expect Hanrine to continue to drill another 15,000m to earn in a further 21% of the project.

Here’s what we think interested Gina and the Hancock team to TTM’s asset:

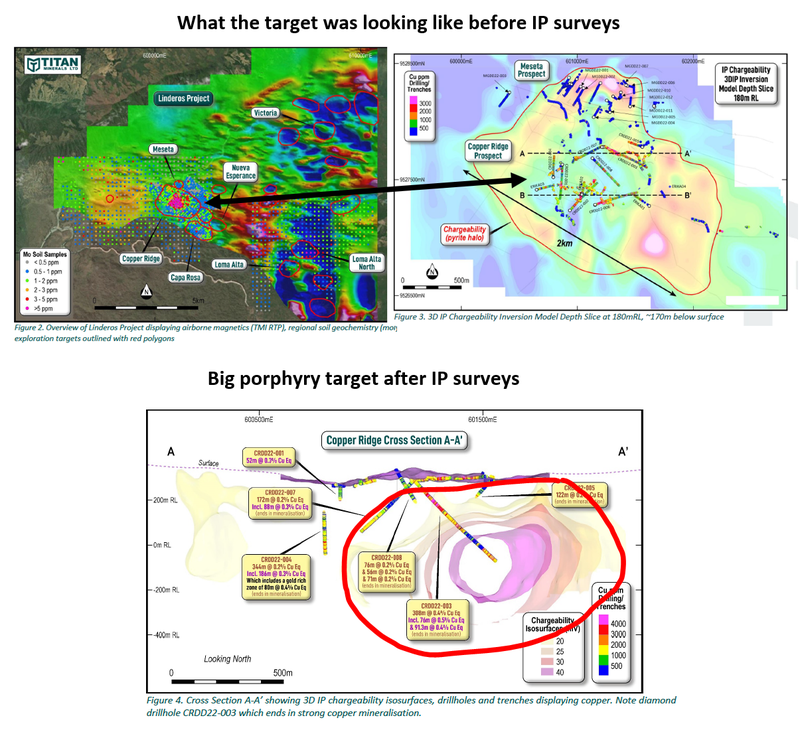

Back in 2022 TTM made some significant copper hits over the project.

Specifically a 308m at ~0.4% copper equivalent hit.

At the time of drilling, TTM managed to confirm big zones of copper porphyry mineralisation - but the market at the time overlooked the results.

Then, in 2023 TTM ran an IP geophysical survey and found what it thinks could be “a much larger porphyry system than previously recognised in surface mapping, geochemistry, and drilling”.

Here’s what it looks like in “colourful blob” form:

(Note* that monster 308m hit ended in mineralisation and has barely crossed halfway mark of that giant target)

These results were good, but generally it is a major mining company with deep pockets that develops these types of projects.

(Think BHP, Rio Tinto, etc...)

However, copper resources are depleting around the world and larger companies have had to get creative to make new copper discoveries.

Enter Gina Rinehart, who also happens to have pretty deep pockets.

The geology is stacking up and there is strong demand for new copper assets.

Two big reasons why we think Gina Rinehart's Hanrine has invested in TTM's copper project, farming in for (up to) US$120M.

Here’s some more on the global copper thematic that we are witnessing...

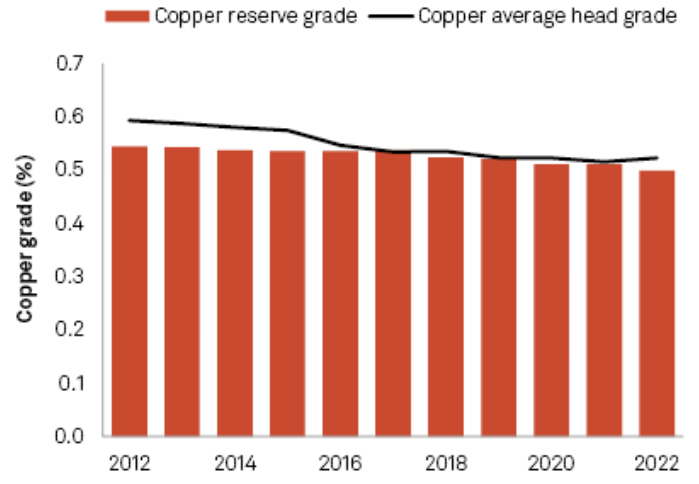

Quick summary: Depleting supplies of copper, new projects more valuable?

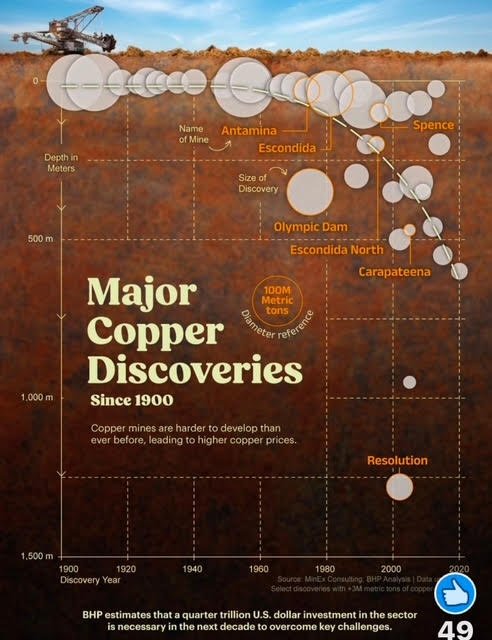

Over the last decade the resources from existing copper assets are depleting:

(Source)

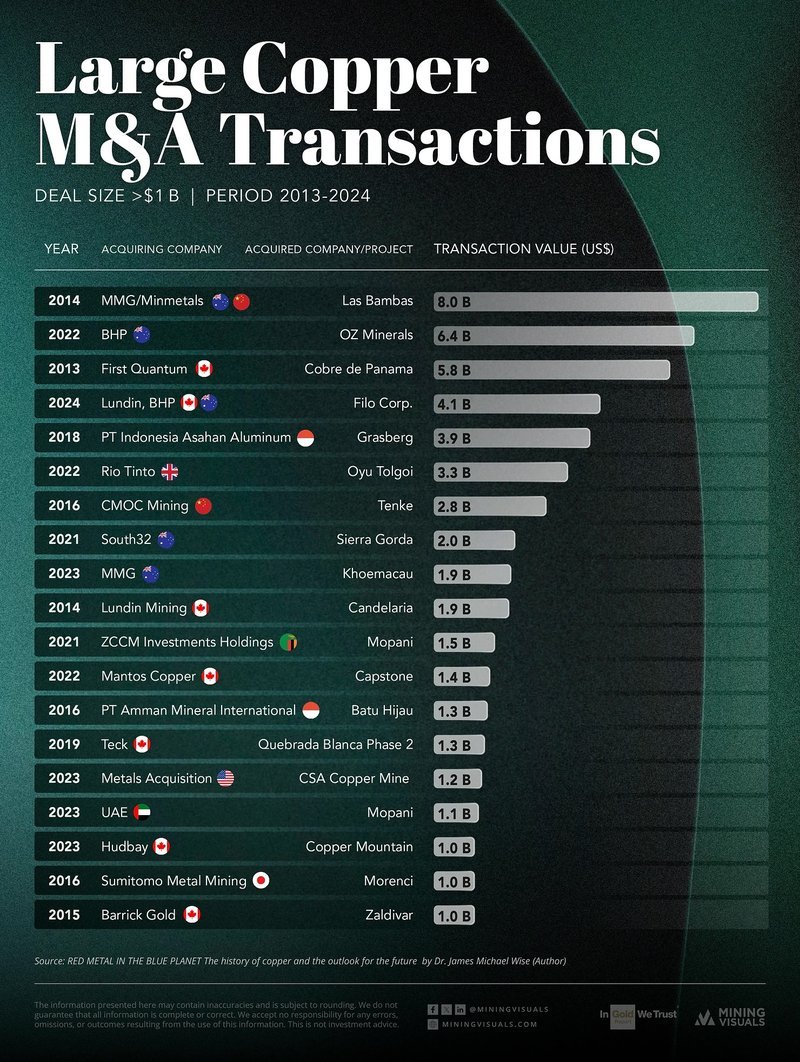

This has led to a wave of consolidation across copper projects with billions of $ spent since 2013.

Last year this peaked with the BHP/Lundin Mining $4.1B acquisition of Filo Corp’s copper project:

(Source)

This consolidation is because it is becoming harder and harder to make new copper discoveries and there are less juniors out there conducting copper exploration.

Companies are going deeper and deeper to find new copper discoveries, they are much smaller and becoming less frequent:

All of this points to sustained market interest in copper, which we think should only improve the appeal of TTM’s copper exposure in its portfolio of assets in Ecuador.

The copper price continues to push upwards over the long term, but the supply side of the equation for copper is looking more drastic.

(Source)

We think that this is a big reason that Harine has farmed-in to TTM’s project, and if they like what they see (with more copper hits from the completed drilling program) then we expect the company to continue to fund exploration.

What’s next for TTM?

More drilling at Dynasty gold project 🔄

TTM has 5,400m left to drill at its Dynasty gold project.

We expect the company to complete this drilling over the coming months and set itself up for a resource upgrade.

Resource upgrade/update at Dynasty 🔲

By mid-year we expect TTM to publish a resource upgrade over its Dynasty Project.

Drilling results from the Linderos Copper project 🔄

10,000m of drilling has been completed.

We should expect the results of this project to be announced over the next couple of months.

What could go wrong?

With the balance sheet healthy in the medium term, the key risk for now is “exploration risk”.

If TTM is unable to discover more gold over its Dynasty project and publish a resource upgrade lower than market expectations, it could have a negative impact on the share price.

In addition, if the 10,000m at Linderos does not identify the copper hits that Hanrine needs to continue to fund exploration, it could also jeopardize further development and investment over this project.

Exploration / Drilling risk

There is no guarantee that TTM’s extensional drilling programs will be successful and TTM may fail to uncover enough economic mineralisation to justify the expense.

Source: 29 May 2024 TTM Investment Memo

Our TTM Investment Memo:

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our TTM Investment Memo where you will find:

- What does TTM do?

- The macro theme for TTM

- Our TTM Big Bet

- What we want to see TTM achieve

- Why we are Invested in TTM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.