TTM - Gold, Silver and… Copper with a Gina JV?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 12,152,769 TTM shares at the time of publishing this article. The Company has been engaged by TTM to share our commentary on the progress of our Investment in TTM over time.

Gold is at all time highs...

Copper is also trading at all time highs....

The silver price just hit decade highs again - touching over US$32/oz overnight.

And our Investment Titan Minerals (ASX:TTM) is leveraged to all of them.

Commodity price runs tend to happen first.

Then capital starts to look for homes in companies with the most exposure to those particular metals.

We think that our Investment TTM could benefit from this.

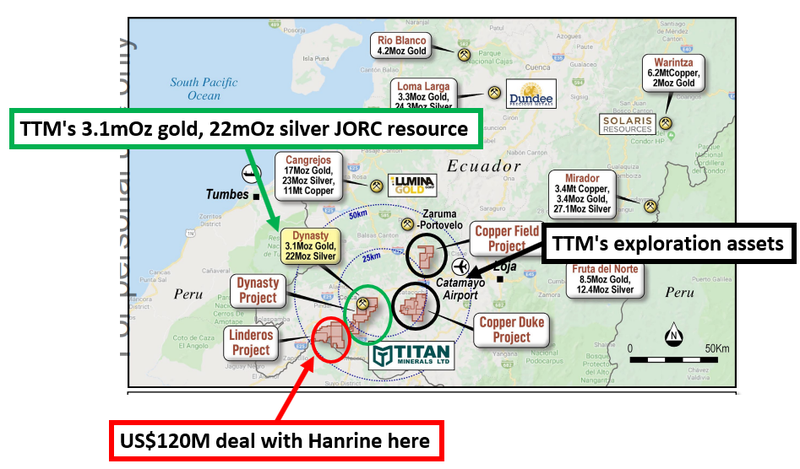

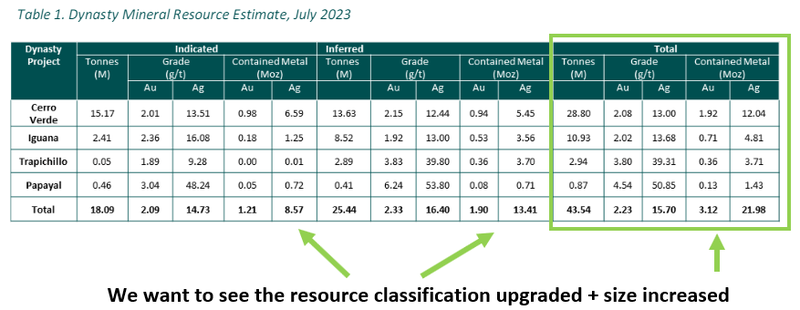

We have been Invested in TTM since July 2020. Since then, TTM converted its large foreign resource into a JORC compliant 3.1M ounce gold and 22M ounce silver resource at its Dynasty project.

We think that the silver resource was largely overlooked by the market at the time, when silver wasn't as in favour as it is now.

This might be changing given the recent run on the silver price...

Last month, TTM surprised us by announcing a proposed US$120M joint venture earn in agreement for an 80% interest in one of its copper exploration projects called Linderos.

The deal was with a subsidiary of Gina Rinehart’s Hancock Prospecting, called Hanrine.

As part of the deal, US$2M gets paid to TTM when the deal becomes binding, the remainder of the US$118M gets spent on exploration and development.

That deal was for only one of TTM’s four projects, a large copper porphyry target.

The deal excludes TTM’s Dynasty project - where the company has that huge 3.1M ounces of gold and 22M ounces of silver.

We think that the copper deal with Gina and the company’s recent capital raise for ~$3.4M at 3c could be a turning point for the company.

The commodity price runs are also working in its favour...

The key things we are watching for next with TTM is confirmation of JV earn in to become binding (triggering the $2M upfront payment to TTM) and for copper, gold and silver prices to keep running.

Following a recent capital raise to drill its gold-silver project and a cashed-up partner funding drilling on its copper porphyry target, we are looking forward to seeing what TTM can get up to over the next 12-18 months.

In today’s note we will publish our new TTM Investment Memo, detailing:

- What TTM does

- The macro theme for TTM

- Our TTM Big Bet

- What we want to see TTM achieve

- Why we are Invested in TTM

- The key risks to our Investment Thesis

- Our Investment Plan

But first, a quick look at TTM and why we think now could be the turning point.

TTM has a portfolio of precious and base metals exploration projects in Ecuador.

There are three separate plays for TTM:

- Dynasty Project (Gold-Silver) - which has a 3.1M ounce gold, 22M ounce silver JORC resource.

- Linderos project (Copper-Gold) - TTM recently announced a proposed earn in joint venture with a Gina Rinehart controlled subsidiary for US$120M for a 80% stake in the project.

- Copper Duke and Copper Field - at Copper Duke, TTM is working with a similar exploration theory as Linderos, looking for a big porphyry target. Copper Field is TTM’s earliest stage asset.

Although TTM has a gold and silver JORC resource at Dynasty and a deal with a Gina Rinehart subsidiary, we think TTM still trades at a relatively small market cap of just $45M.

TTM had US$1.9M in cash (A$2.9M) at March 31st.

Until now, TTM’s share price has been trading lower whereas the underlying commodities that TTM is exposed to has been trending up (gold, silver, copper).

Our view is that as sentiment becomes more and more positive on the underlying commodities, companies like TTM, with in ground resources and strong exploration upside, will be re-rated higher.

We think TTM has the right exposures at the perfect time...

Macro theme can be the strongest influence on a share price

We have said it in the past...

Sometimes, the biggest influence on a company’s share price can be the strength of a macro thematic, which is usually determined by the price of commodities.

When commodity prices are running, investor, corporate and public interest in a sector increases.

Money then flows towards companies with projects in that commodity.

(Source: Why do share prices go up?)

That money flow can be in the form of buying on the market or through capital raises, which leads to increased demand for shares.

The interest from the markets also means shareholders are more apprehensive to sell...

Investors think the share price will go up so they hold off any plans to sell.

That leads to a situation where there is strong buying and limited selling - demand overpowers supply and usually share prices go up.

What it means for the companies is that they have higher share prices, more cash and find it easier to raise money to bring new projects online or to drill out discoveries.

We saw this play out in lithium stocks between 2020 and 2022.

Our view is that IF the gold and silver prices continue running then we could see a similar situation in the gold/silver stocks.

The TTM share price has been on a downward trend since we first invested in 2020:

Unfortunately for the company, the key time that it was developing its asset, between 2021 and 2023 was when the sentiment for the commodities was at its lowest.

The challenge for TTM was balancing spending dollars to drill and develop a JORC Resource while also raising capital at lower valuations due to commodity sentiment.

The hardest thing to do is commit to big and expensive drill programs when the market isn't interested in the results, even if they are really good...

Over that period TTM raised money at lower and lower prices, first at 10c then 6.5c then 5c then 3.3c.

This causes stale holders to sit on the register and likely sell.

But things change quickly, with sentiment for the commodities on the up - new holders coming into the shares now will enjoy the fruits of all of the previous development work while taking on a lower risk at a lower share price.

Ultimately, that is the game of the commodities cycle, and we think that TTM is about to turn the corner.

(Its been a long wait for us with TTM’s commodities to start a price run)

Key catalysts we are looking out for with TTM

Two other factors that can re-rate a company’s share price are an “imminent catalyst” and a “strong result”.

The perfect timing to deliver strong results from a material catalyst is when the two other factors (market sentiment and capital inflows) are working in a company’s favour.

Below are the 4 key catalysts we have to look forward to with TTM:

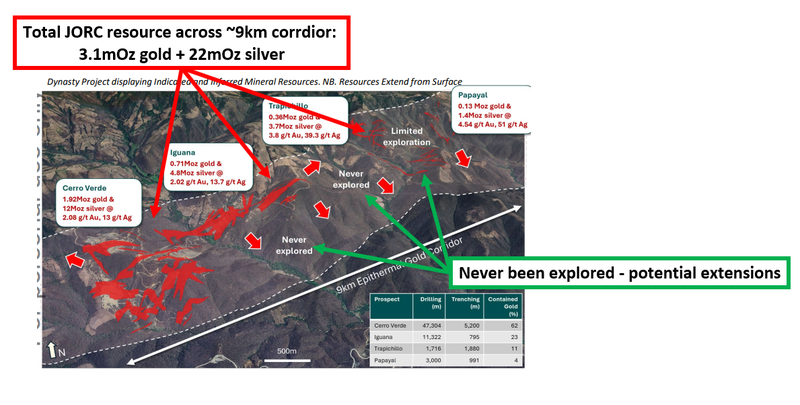

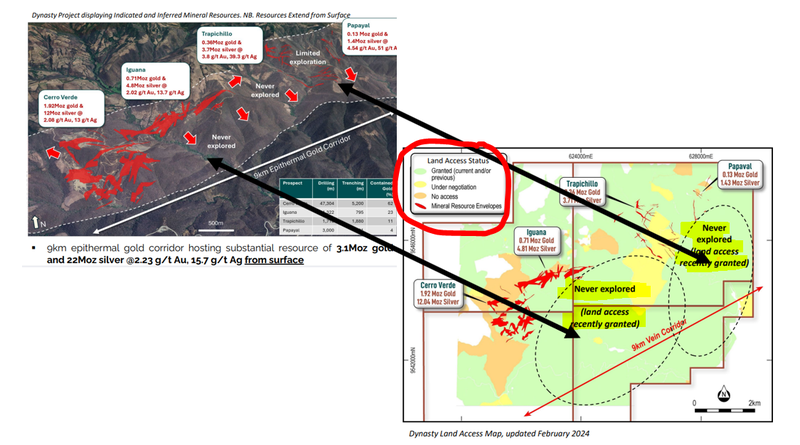

1. Resource upgrade/update at Dynasty 🔄

TTM has spent the last few months running new geological models for the project and expects to put out a resource update next month.

2. Scoping study preliminary results

We expect this news to come after the resource upgrade. TTM has previously said that it should be delivered in Q3 2024 - which is next quarter.

We think this work will give the market a better idea of project economics for TTM’s already very big gold-silver JORC resources.

3. Drilling to upgrade the Dynasty JORC resource again 🔲

TTM expects to start drilling at Dynasty in July.

We want to see TTM drill out the parts of its project that have seen very little exploration - TTM was recently granted land access to these parts. Any new discoveries could add large resources to TTM’s existing resource base.

Below are two images that give a pretty good idea of the exploration potential across the project:

4. Drilling at Linderos (Gina JV) 🔲

We also want to see TTM close the deal with Gina Rinehart’s subsidiary at its Linderos copper project and start drilling.

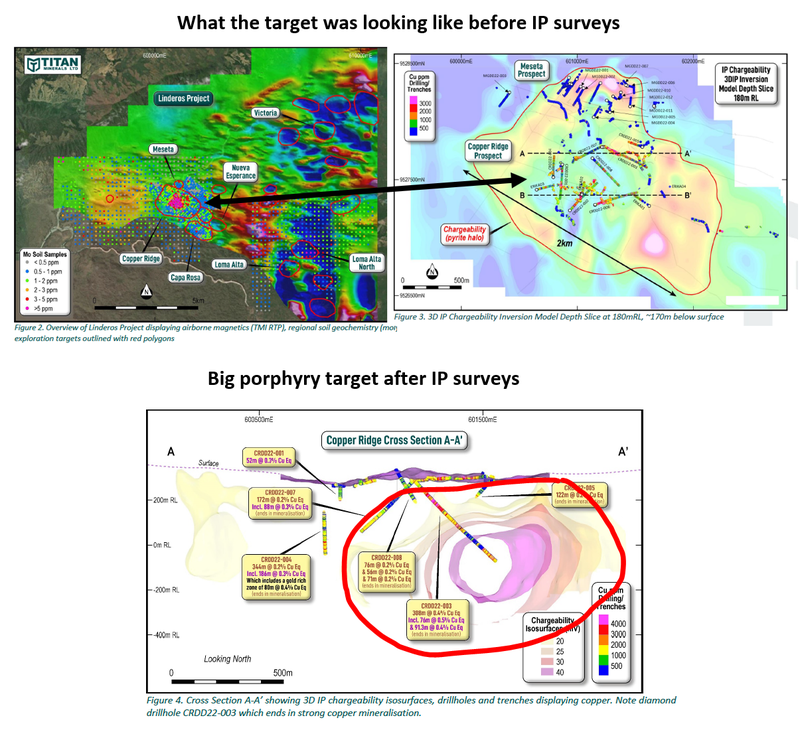

At Linderos we want to see TTM and its JV partner follow up the 308m hits from 2022 where grades returned ~0.4% copper equivalent.

(Note* that monster 308m hit ended in mineralisation and has barely crossed halfway mark of that giant target)

The drilling in 2022 managed to confirm a big copper porphyry system but the market seemed to overlook the results and TTM had to go slow on exploration due to funding shortfalls.

TTM instead went back and ran an IP geophysical survey and found what it thinks could be “a much larger porphyry system than previously recognised in surface mapping, geochemistry, and drilling”.

Here’s what it looks like in “colourful blob” form:

Ultimately, the work completed to date was enticing enough to bring the Hancock Prospecting subsidiary to do a deal.

We want to see TTM get back in and drill out this target while the market is showing an interest in copper explorers - and the best part is TTM won't have to spend any money to do that drilling

TTM expects the drilling to start next quarter.

The latest from TTM’s CEO Melanie Leighton:

Below is a good video presentation of where TTM is at and what to look out for, from TTM’s CEO Melanie Leighton:

(Source)

Our New TTM Investment Memo

Now that TTM has agreed to terms with a Hancock Prospecting subsidiary on one of its copper assets, and recently locked away a capital raise, we thought it would be a good time to reset our TTM Investment Memo.

Below is our new TTM Investment Memo where you can find:

- What TTM does

- The macro theme for TTM

- Our TTM Big Bet

- What we want to see TTM achieve

- Why we are Invested in TTM

- The key risks to our Investment Thesis

- Our Investment Plan

Investment Memo 2: Titan Minerals (ASX:TTM)

Opened: May 28th 2024

Shares Held at Open: 12,152,769

What does TTM do?

Titan Minerals Ltd (ASX:TTM) is an exploration and development company on the hunt for world class gold, silver and copper assets in Ecuador.

What is the macro theme behind TTM?

As of writing this memo gold, silver and copper price are moving upwards.

Gold and silver are both precious metals that are thought of as hedges against currency inflation.

Silver also has industrial use cases including in the manufacture of solar panels. Demand for silver from solar panels is forecast to go exponential and as such can be considered important to the energy transition.

Meanwhile copper is predominantly used for electricity transmission. Renewable energy projects require A LOT of copper to link them up to the grid from remote areas.

Copper is also used in data centres for AI and in electric vehicles (EVs) - there are roughly 80kgs of copper in an average EV.

What is our TTM Big Bet?

“We want to see TTM prove up a $1BN plus copper or gold discovery in Ecuador which is so attractive that a mining major acquires the company.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our TTM Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

7 key reasons why we are Invested in TTM:

- Advanced stage asset with giant JORC resource - TTM’s primary asset (Dynasty) has an existing 3.1M ounce gold, 22M Ounce silver JORC resource. We think the resource at Dynasty underpins TTM’s valuation.

- TTM has agreed to terms on a US$120M farm-in deal with Hancock Prospecting subsidiary - TTM has agreed to terms on a JV / earn in for its earlier stage copper project. Once binding, we think the deal validates the potential for a seriously big copper discovery, given the deal was signed at such an early stage and for such a large amount.

- TTM essentially has a free carried option at giant copper porphyry discovery - We think the proposed deal with Hanrine (Gina’s subsidiary) gives TTM a free option at being a 20% holder in a giant copper porphyry discovery in a deal that is worth more than TTM’s current market cap on its own.

- Right commodities at the right time - TTM gives us exposure to gold, silver and copper. All three commodities are currently running with gold and copper both trading at all time highs and silver breaking out into decade highs.

- Rare copper exposure with tier 1 discovery potential - we think it is hard to find small cap stocks on the ASX that have genuine tier 1 copper discovery potential. Especially not one with funding secured to drill out a potential discovery. TTM has both at its Linderos project.

- TTM has institutional backing - For such a small company, TTM already has some impressive funds on its share register including Tribeca, Nero Resources Fund, Bacchus Capital, and Thorney.

- Ecuador is a mining hot spot - All of TTM’s assets are in Ecuador. The country is well known for being home to big discoveries and blue chip mining companies like Anglo American, Newmont, BHP, Barrick, Lundin. Large cheques are being written for Ecuadorian mining projects. We think TTM’s assets could be of increased interest over the coming months.

What do we want to see TTM deliver?

Objective 1: Upgrade Mineral Resource Estimate at Dynasty

- We want to see TTM grow its existing 3.1M ounce gold and 22M ounce silver JORC resource at its Dynasty project.

Milestones

🔄 JORC resource upgrade #1

✅ Drilling Results 1

🔲 Drilling Results 2

🔲 JORC resource upgrade #2

Objective #2: Economic assessment of the Dynasty project

- We want to see TTM move the Dynasty project into the feasibility study stage. TTM’s first target for this stage is a pre-scoping study which should give a high level overview of the project's economics.

Milestones

🔲 Metallurgical Testwork Results

🔲 Pre-Scoping Study results

Objective #3: Progress Linderos Project through to MRE

- We want to see TTM complete the deal with Hanrine and start drilling out the Linderos project all the way through to a maiden JORC resource estimate.

Milestones

🔄 Complete JV deal with Hanrine (Gina Rinehart subsidiary)

🔲 Drill program #1

🔲 Drill program #2

🔲 Confirmation of copper Porphyry discovery

🔲 Maiden JORC resource estimateMineral Resource Estimate published

Objective #4: Sign JV/strategic partnership on earlier stage projects

- We want to see TTM progress its earlier stage assets (Copper Duke and Copper Field) through a farm out deal similar to the one signed on Linderos.

Milestones

🔲Joint venture or farm-in partner announced

🔲Drilling exploration program commences

🔲Drilling exploration program results

What are the risks?

Exploration / Drilling risk

There is no guarantee that TTM’s extensional drilling programs will be successful and TTM may fail to uncover enough economic mineralisation to justify the expense.

Funding risk/dilution risk

As a small cap company, TTM is reliant on capital markets to advance its projects if it cannot do strategic deals with partners.

If something negative happens at a macro or company level, TTM could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Commodity price risk

At the time of writing this memo all three of the base metals that TTM’s projects are leveraged to are running hot.

Should the price of these commodities fall, it could hurt the TTM share price and the look-through value of its assets in any takeover scenario.

Deal risk

Specific for the Linderos Project, the deal with Hanrine is subject to conditions including a formal earn-in and JV agreement being signed.

It is possible that the deal falls through for whatever reason, in which case we think the market would react negatively and lead to a fall in TTM’s share price.

Sovereign risk.

TTM’s prospects are all located in the developing nation of Ecuador.

There is no guarantee that local authorities and/or communities will favour development of TTM’s prospects, and so could hinder advancement.

We also note a recent surge in violence could have a dampening effect on investments.

What is our investment plan?

We plan to hold the majority of our position in TTM for the next 12 months (and beyond) as it progresses through both its Dynasty project as well as completing its deal with Hanrine for the Linderos Project.

However we may de-risk a portion of our Investment if the share price appreciates materially in line with our standard de-risking plan.

=TTM Retro=

Investment Memo: Titan Minerals (ASX:TTM)

Opened: Mar 2022

Closed: 28 May 2024

Shares Held at Open: 4,249,250

Shares held at Close: 12,152,769

What does TTM do?

Titan Minerals Ltd (ASX:TTM) is an exploration and development company on the hunt for world class gold and copper assets in the emerging global minerals hotspot, Ecuador.

What is the macro theme behind TTM?

Gold remains a safe haven investment and hedge against inflation, and has historically outperformed in times of volatility (e.g market bubble crash, armed conflicts...).

Bullish gold market conditions persist, particularly with the go-to response to the pandemic being unprecedented worldwide monetary and fiscal stimulus (i.e. ripe conditions for sustained inflation).

Copper demand is set to grow from its already robust position on the back of unprecedented stimulus spending on infrastructure and construction projects globally.

Sentiment: Strong

For a while market sentiment for gold, silver and copper was all relatively weak.

However, in recent months the price of gold, silver and copper have all started rallying and sentiment has started to pick up again.

We are marking the sentiment for TTM’s macro theme as “strong” but we are conscious of the sentiment having been low at points during our first Investment Memo

Why we continue to hold in 2022

Prime Gold-Copper real estate

TTM is an early mover in securing prime real estate within one of the world’s latest exploration and mining hotspots - Ecuador.

TTM owns several exploration and development assets in the country.

Ecuador has only recently become an attractive exploration and mining jurisdiction through improved and stable legislation.

With Ecuador mirroring the geology of several of its mining-rich neighbouring nations, there is a good opportunity for big discoveries still to be made here.

TTM could appeal to larger mining groups now seeking to attain or grow a significant land position within this hotspot.

[Grade = B]

While the overall prospectivity of this part of Ecuador has only improved as TTM has gone about its exploration efforts - the current political situation in Ecuador is markedly more tense.

In a positive for TTM, we note that recently elected President Noboa attended PDAC in Toronto to re-emphasise Ecuador’s attractiveness as a home for mining investment.

Additionally, a number of mining majors have invested heavily in the region of Ecuador that TTM operates in.

However, since our initial TTM Investment Memo was published, we note that a surge in violence in Ecuador may have a dampening effect on potential investment.

Friction between the Ecuadorian federal government and local stakeholders could be a source of risk for TTM, along with the potentially volatile political environment in the country.

Flagship project already with a big resource base

TTM’s Dynasty gold project has a “foreign resource estimate” of 14.5Mt @ 4.53 g/gold + 36g/t silver for a total contained resource of 2.1Moz gold + 16.8Moz silver.

TTM is drilling in order to re-classify the resource to JORC standards, with potential upside of further growing the deposit. This could form the basis of a possible local mining operation down the track.

[Grade = B]

Although TTM managed to deliver an upgrade to the Foreign Resource Estimate, it took much longer than expected.

This caused investor sentiment to wane in the project and the JORC upgrade wasn’t enough to offset the delays in the project.

Copper side bets

TTM has two highly prospective copper projects in their pipeline, not far from where several major copper discoveries have been made of late.

These provide blue-sky potential upside, should a discovery be made.

[Grade = A]

TTM managed to sign a Joint Venture agreement for one of its copper side-bets “Linderos” with a subsidiary of Gina Rienhart’s Hancock Prospecting.

For TTM to extract some value from these “side-bets” is a big win in our eyes.

What do we expect the company to deliver in 2022?

Objective #1: Resource conversion to JORC standards at Dynasty

- We would like to see TTM convert their existing ‘foreign estimate’ resource into a maiden JORC resource estimate this year.

- We also want to see extensional drilling produce an expanded exploration target that highlights the potential to grow the current resource base.

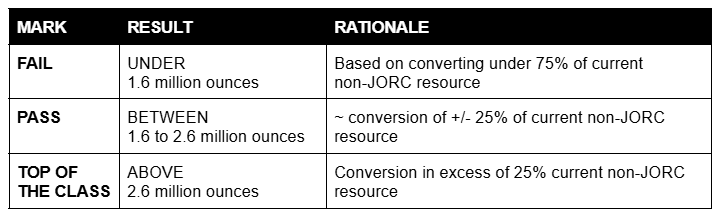

- Here is how we will rank the JORC resource estimate result (our opinion only):

[Grade = A]

TTM managed to publish an upgraded JORC resource of 3.1M ounces of gold and 22M ounces of silver. This beat our “Bull Case” scenario for the project.

Objective #2: Follow-up drilling at Linderos

- With promising early exploration results late last year, it shouldn’t take too long for TTM to prioritise the prospects at Linderos, and generate numerous drill targets.

- Follow-up drilling at the targets is already underway, and we anticipate assays in 2Q22.

[Grade = B]

Assays from TTM’s follow up drilling came back strong, with 308m at 0.4% copper equivalent. TTM did not follow up this program with more drilling but did conduct IP surveys for more target generation.

From this work, TTM was able to sign a Joint Venture worth up to US$120M to develop the project (in exchange for 80%).

Objective #3: Commence drilling at Copper Duke

- Following the recent recon-drilling program alongside ongoing geophysical surveys and geochemical soil sampling, TTM should be in a position to define drill targets for 2H22.

- We want to see an extensive drilling program later this year, with initial assay results before year-end. This will shed light on the potential for Copper Duke.

[Grade = D]

TTM was able to define drill targets for Copper Duke but no drill program was done. This was due to financial constraints and resources allocated to the Dynasty project.

What could go wrong?

Capital requirements

TTM is not a producer, remaining an explorer, and so requires continuous funding as it continues to advance its assets.

As such, the company will be required to raise capital for survival when the current cash at bank drains. However, there is no guarantee that capital markets will be conducive at that point.

We note that they have a substantial cash balance at present, which minimises this risk for 2022.

[Risk = Materialised]

Through this TTM Investment Memo the company has raised $5.5M at 5 cents per share, $4.1M at 3.3 cents per share.

Each of TTM’s last four capital raises has been done at a lower and lower valuations, which has been painful for existing investors.

Underlying commodity risk

TTM is exposed to commodity price risk, which depends on macroeconomic factors and demand and supply dynamics of the underlying commodities, i.e. gold and copper.

Market sentiment closely correlates with commodity prices, and hence TTM’s valuation will be impacted by commodity prices as well.

There is no guarantee that gold and/or copper sentiment will trend positively this year.

[Risk = Materialised]

Although the sentiment for copper, gold and silver is strong, in 2023 when TTM was raising capital, the sentiment for these commodities was relatively weak.

This has meant that TTM has needed to raise capital at depressed valuations, diluting existing shareholders.

Geological risk

The resource for the flagship project is an estimate only, and there is no guarantee that the current “Foreign resource estimates” is substantially converted into JORC resources.

Even if the JORC reclassification occurs, it could be at a much lower grade, size or level of confidence, which would impact its value.

[Risk = Decreased]

TTM was able to publish a JORC resource and de-risk the project from a geological perspective.

Sovereign risk

TTM’s prospects are all located in the developing nation of Ecuador. There is no guarantee that local authorities and/or communities will favour development of TTM’s prospects, and so could hinder advancement.

[Risk = Unchanged]

What is our investment plan?

We first invested in TTM at 6.67c and increased our position again at 10c in anticipation of the JORC resource estimate on its Dynasty gold project.

We intend to de-risk our investment keeping 80% of our position in the lead up to the JORC resource definition.

We plan to sell up to 50% of our investment in TTM if the share price increases 4-fold from our initial investment price in the lead up to the JORC resource.

Depending on the outcome of the JORC resource estimate, our investment strategy for TTM will change:

- TOP OF CLASS OUTCOME - We will de-risk our position if the share price increases 4-fold from our initial investment price.

- PASS OUTCOME - we will likely hold on to our TTM position and evaluate the project's merits going forward based on the gold price at the time.

- FAIL OUTCOME - we will need to evaluate the merits of TTM’s other projects at the time, either buying back into the stock at a lower price or selling a portion of our holding to de-risk.

[Grade = D]

TTM’s share price did not materially appreciate during the life of the memo and we did sell down a portion of our holdings at a loss.

Although the “Top of class outcome” was beat by TTM’s results, the JORC resource was delayed and the commodity price risk materialised.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.