Gina Rinehart Hancock Subsidiary to earn into TTM Copper Asset

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 12,152,769 TTM shares at the time of publishing this article. The Company has been engaged by TTM to share our commentary on the progress of our Investment in TTM over time.

Here comes Gina...

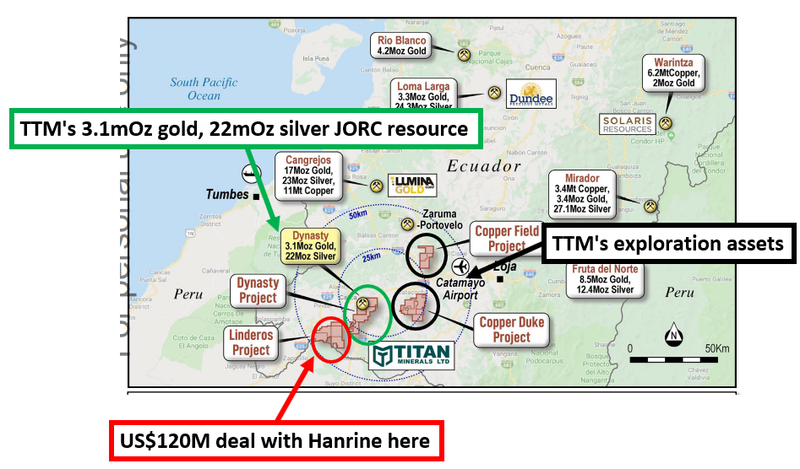

Our gold-copper Investment Titan Minerals (ASX:TTM) has just agreed to terms with a subsidiary of Hancock Prospecting - owned by Australia’s richest person, Gina Rinehart.

The deal will see the Hancock subsidiary pay US$120M to earn up to 80% of just one of TTM’s Ecuadorian copper projects.

TTM still has 100% of a 3 million ounce gold project - and the gold price is hitting new all time records each week.

Today’s deal ascribes a read through value of US$150M on the one copper asset alone (and it's not even TTM’s main asset).

TTM was capped at less than A$60M before today’s news.

We didn't see this deal coming, that's for sure.

TTM’s share price had been coming down quite a bit over the past 12 months - but as so often happens with cyclical markets, things are suddenly looking up for TTM.

Copper prices are rallying, gold prices are at all time highs and even the silver price has started breaking out...

Meaning it’s a great time for TTM’s copper exploration to progress - and it appears that Hancock agrees.

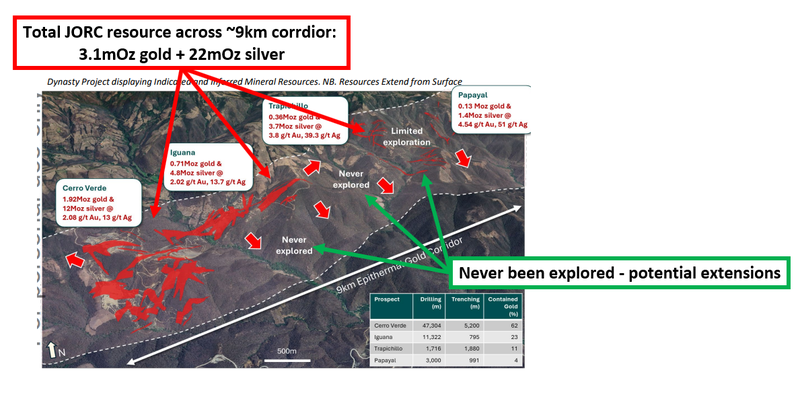

While Hancock spends tens of millions of dollars on TTM’s Linderos asset, TTM can work up its Dynasty project - which already has a 3.1 mOz gold, 22 mOz silver JORC resource.

And we that resource is due to be updated this quarter.

Via her controlling entities, Gina has been on a buying spree lately - before announcing the A$1.7BN takeover of Azure Minerals, she was buying shares on market in that company pretty aggressively.

More recently she picked up a substantial shareholding in Lynas Rare Earths - on market...

Azure and Lynas have multi billion dollar valuations - which is to be expected with Gina rumoured to have a $20BN cash warchest at her disposal.

Her latest deal is with our TTM - which was capped at just $58M before today.

For such a small company, TTM already has some impressive funds on its share register including Tribeca, Nero Resources Fund, Bacchus Capital, and Thorney.

Now TTM is partnering with a subsidiary of the Hancock Group.

As we noted above, the deal will see Gina’s private company Hanrine progressively take an 80% interest in the project in exchange for US$120M in funding.

The deal is still subject to the execution of formal binding documents, and the completion of Hanrine’s due diligence investigations. We expect that TTM will be updating shareholders on this process over time.

The first payment will be US$2M to TTM within 30 days of execution of a formal binding agreement, then there will be a progressive earn in over exploration expenditure over future years (more details below on the deal structure)

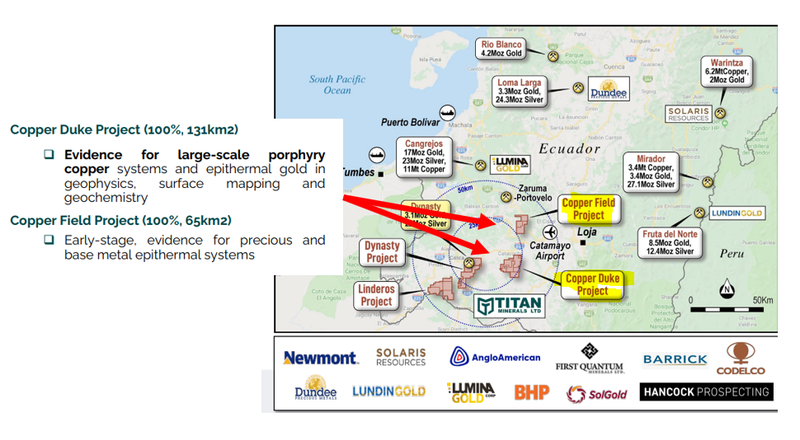

As we noted above, this deal with Hancock covers only one of TTM’s four projects in Ecuador...

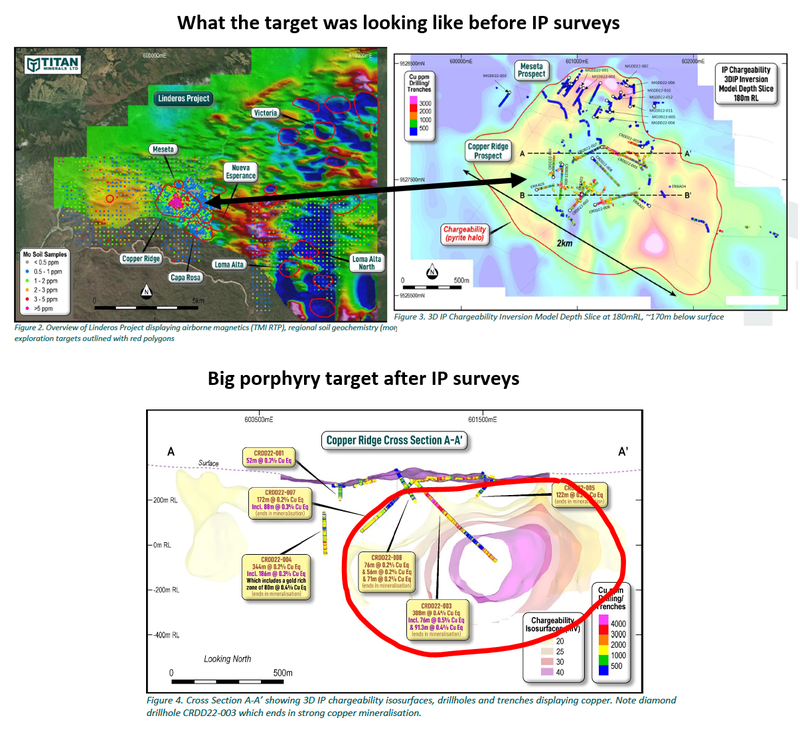

Linderos - the one Hancock is buying into - is actually one of TTM’s earlier stage exploration projects - albeit there have been some monster hits here where TTM hit ~308m at 0.4% copper equivalent back in 2022.

The deal with Hancock doesn't include TTM’s 100% owned 3.1moz gold + 22moz silver JORC resource at Dynasty or its 100% owned Copper Duke and Copper Field exploration assets.

So for ONE of its FOUR assets - TTM is getting a look through valuation for its 20% free carried interest of ~US$30M (A$45M).

Given TTM’s market cap is ~A$61M we think the market is putting an extremely low valuation on its existing JORC resource at Dynasty, and exploration upside on its other projects.

There will be an investor webinar with TTM CEO Melanie Leighton to talk through the deal tomorrow (Friday 19 April 2024 at 11:30am AEST):

Click here to register for the webinar

Why Gina might be interested in TTM...

Higher up we mentioned TTM’s monster hits back in 2022 at the Linderos Project - the 308m at ~0.4% copper equivalent. Since that round of drilling, TTM has been working up the project.

At the time of drilling, TTM managed to confirm big zones of copper porphyry mineralisation - but the market seemed to overlook the results...

We covered those drill results in December 2022, read: TTM honing in on potential copper-gold porphyry discovery

In 2023 the company ran an IP geophysical survey and found what it thinks could be “a much larger porphyry system than previously recognised in surface mapping, geochemistry, and drilling”.

Here’s what it looks like in “colourful blob” form:

(Note* that monster 308m hit ended in mineralisation and has barely crossed halfway mark of that giant target)

Drilling out a target of this size isn't something we normally see small $58M capped companies do - usually it's the bigger companies like BHP and Rio Tinto that come in and take the projects on.

That's because whilst they can be extremely valuable they also require a lot of expensive exploration drilling to prove out.

TTM now has that deep pocketed funding partner, and the joint venture can go back and drill out what could (with a bit of luck) turn out to be a monster copper deposit.

The deal is also structured in a way where the majority of the US$120M gets spent on the project, meaning the deal will force capital into the ground if Hanrine likes what they see.

(Drilling this asset is something we have wanted to see from when we first Invested in the company back in July 2020)

Below are the key terms for the deal:

- US$2M cash upfront to TTM for a 5% interest in the project (within 30 days of executing a binding agreement).

- 10,000m of drilling (or US$8M spent) for a further 25%.

- 15,000m of drilling (or US$12M spent) for a further 21%.

- The final 29% transfers over once Hanrine declares a “decision to mine” or reaches US$120M in expenditure on the project.

So TTM add’s US$2M to its cash balance and is basically free carried through to a decision to mine for what could be ~US$120M in exploration spend by the time the project is ready to be developed (assuming it gets there).

That means cash and other resources are freed up for TTM to focus on its other assets...

TTM’s three other projects

As mentioned earlier, the deal announced today doesn't include TTM’s three other projects which we think the market could be mispricing - especially given the run of gold and silver prices of late.

Dynasty Project (3.1moz gold, 22moz silver JORC resource)

At Dynasty, TTM is fairly well advanced having already defined a large JORC resource.

TTM could technically take the asset through the development feasibility stages OR it can go back and drill out the project and expand its resource.

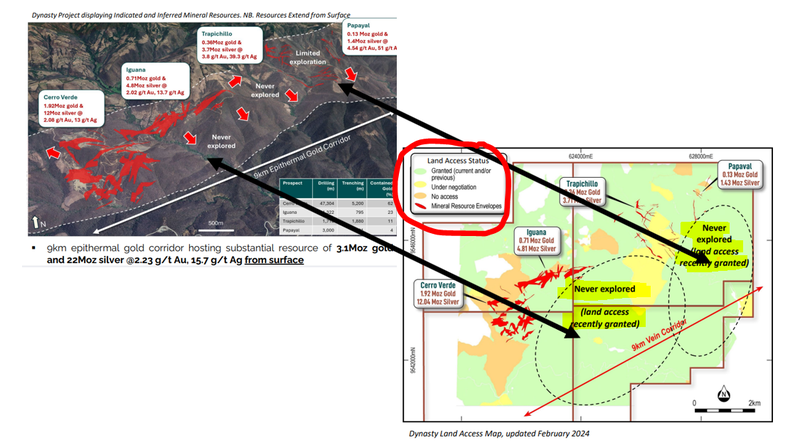

A big part of the reason we Invested in TTM was for the big JORC resource upside at the project from sections in between its multiple deposits.

The deposits sit along ~9km of strike but the bits in between have not been tested until now primarily because of land access issues.

TTM recently managed to get that access sorted and can drill out those parts of the project where we think there is potential to multiply TTM’s already giant resource.

TTM has flagged a Mineral Resource upgrade as soon as this quarter, so that will be one to look out for.

Copper Duke and Copper Field Projects (Exploration assets)

TTM’s other two assets are both relatively early stage.

At Copper Duke TTM has a similar exploration theory to the one that brought about the monster porphyry copper hits at Linderos.

There TTM is at a similar stage where Linderos was before that 2022 drill program.

Copper Field is TTM’s earliest stage asset.

Gold-Copper macro heating up - and TTM just restructured its balance sheet - good timing

For a long time, TTM has been one of those companies in our Portfolio that suffered from a lack of market interest in its macro investment thematic, no matter how good the newsflow it was putting out.

TTM defined a giant 3.1m ounce gold, 22m ounce silver JORC resource and the market didn't really react.

It produced those big copper porphyry hits from Linderos and the market’s reaction was still muted.

That meant TTM had to tighten up shop and run the company as lean as possible - obviously limiting how much work the company could do (and how much newsflow it could generate).

As a result we have seen TTM’s share price come down quite a bit over the past 12 months.

BUT just as often happens in markets, things are suddenly looking up for TTM.

Copper prices are rallying, gold prices are at all time highs and even the silver price has started breaking out...

Meaning it's a great time for TTM’s copper exploration to progress - and Gina agrees.

This is the copper chart over the last 12 months:

(Source)

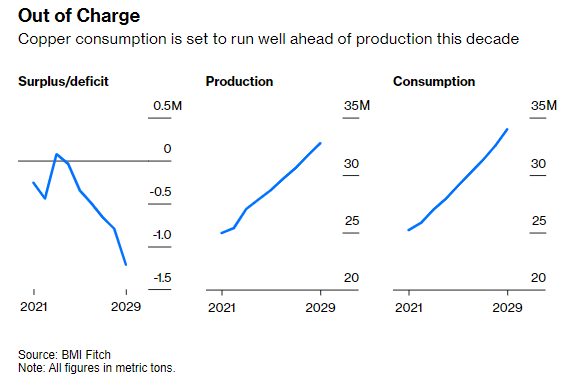

This is what’s happening with copper demand with a long term copper supply deficit forecasted:

(Source)

Grades are getting lower, mining is going deeper and deeper - copper is the lifeblood of the electrification thematic.

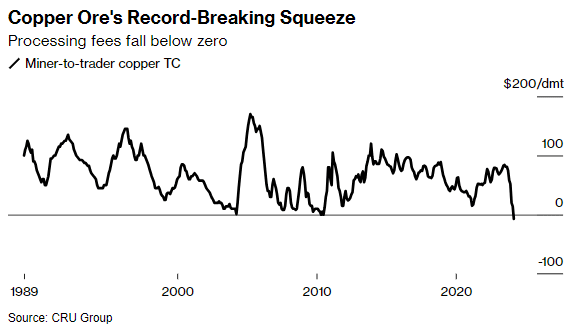

Meanwhile, something is brewing amongst China copper smelters (the factories that extract copper from ores):

(Source)

The above is actually a really important chart, here are the key takeaways:

- Smelters can’t get any supply so are subsidising processing instead of charging for it.

- Tightness in the copper market is down to unexpected closures and downgrades in production from key mines, record-low discounts for copper ore, and a planned increase in copper smelting capacity, which may not fully offset production constraints, potentially leading to further price increases in the future.

- “Copper has been coiled up like a spring,” says one analyst at CRU Group

- Another analyst says - “We believe copper’s second secular bull market this century is taking hold.”

So that’s the copper story, what about gold?

Gold continues to press up to all time highs:

(Source)

(it is the REASONS for the increased demand OR lack of supply where people have different views).

After a long period of being out of favour, gold is now in high demand.

And because there was no broad based investment in developing new mines, there isn't enough supply to match the current demand from buyers.

Some of the notable theories as to why the gold price is going up are:

- China’s central bank (PBOC) buying gold?

- Chinese investors (ie the general population) buying up gold as property and stock markets fall?

- The relationship between gold and US debt - as debt increases, gold price increases?

- Geopolitical tensions pushing investors into safe havens like gold?

- De-dollarisation theory? Does the world go to gold as a global reserve currency?

- Investors fleeing other assets looking for safety in gold?

Read our weekend email covering all of this here: So why exactly are gold and silver prices running?

All up, we think it’s a great price environment for TTM’s assets, and one that could get better.

At the same time, TTM has restructured its balance sheet and got its hands on some cash to finally go and do stuff with.

TTM recently raised ~$8.2M at 3c per share and IF today’s deal is completed will get another US$2M from Hanrine.

Post deal completion, TTM should have a pretty strong cash balance giving the company runway to work up its assets.

With cash in the bank, big partner funding its copper porphyry asset and a big JORC resource we are hoping TTM can start delivering strong newsflow into a stronger macro environment for all the commodities it has exposure to.

Ultimately we want to see TTM achieve our Big Bet which is as follows:

Our TTM Big Bet:

“We want to see TTM prove up a $1BN plus copper or gold discovery in Ecuador which is so attractive that a mining major acquires the company”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our TTM Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for TTM?

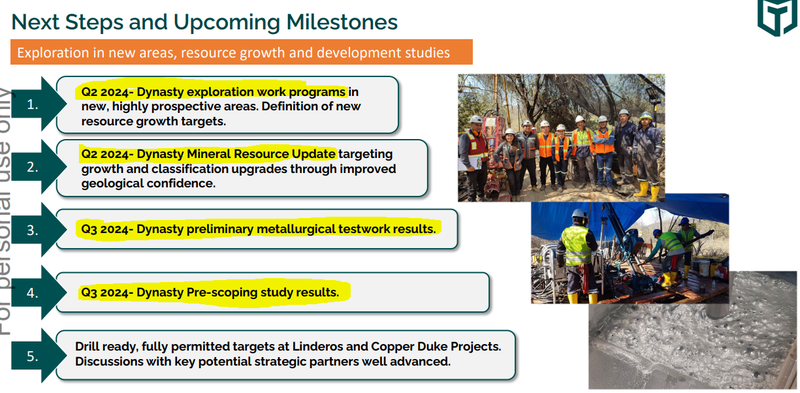

More work at its Dynasty project 🔄

With Linderos now free carried (assuming the deal gets finalised) TTM can focus on its Dynasty asset.

Below are the key catalysts we are looking forward to from Dynasty over the coming quarters:

What are the risks?

In the short term, the key risk for TTM is “Deal Completion Risk”.

The deal with Hanrine is subject to a few conditions including a formal earn-in and JV agreement being signed.

(Source)

It is possible that the deal falls through for whatever reason, in which case we think the market would react negatively and lead to a fall in TTM’s share price.

IF the deal were to fall through it could also bring about “Funding Risk” for TTM.

TTM is pre-revenue and can only really raise smaller amounts of capital to drill out its projects given its size.

If Hanrine were to walk away from Linderos, it would be likely that TTM doesn’t have enough funding available to work up all of its assets all at once, especially considering the size/scale of Linderos.

Again, in that scenario we would expect the market to react negatively and lead to a sell off in TTM shares.

To see more risks as part of our TTM Investment Memo click here.

More recently, political and social events in Ecuador have the potential to impact TTM, which we frame as “Jurisdiction risk”.

Ecuador has recently experienced a crime wave and a tense political environment - this could impact TTM’s operations, now or in the future.

Our TTM Investment Memo

After today’s deal, we think the fundamental thesis for Investing in TTM have changed significantly.

We will be looking to put out a new TTM Investment Memo in the coming weeks to outline what we want to see the company achieve now that it has a big funding partner like Hanrine onboard at Linderos.

Be on the lookout for that note.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.