TEE just quadrupled its acreage in NT - natural hydrogen and helium

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,631,250 TEE shares and 1,850,000 TEE options at the time of publishing this article. The Company has been engaged by TEE to share our commentary on the progress of our Investment in TEE over time.

Top End Energy (ASX:TEE) has just quadrupled its granted licence tenure in the NT.

TEE picked up 27,885km^2 of acreage from Gina Rinehart’s Hancock Energy.

The new acreage is prospective for natural hydrogen and helium.

...TEE’s new ground is also prospective for conventional and unconventional hydrocarbons.

TEE is effectively acquiring an option over this ground - there is no upfront consideration payable to Hancock Energy.

Hancock is maintaining exposure to the assets by holding a royalty over any future production revenues.

As they are granted licences, it means TEE can start exploration work right away - avoiding the regulatory delays that have hampered progress on its other assets.

We are particularly interested in the natural hydrogen and helium angle for the new assets.

We have been watching another company Gold Hydrogen go from 19c to $1.45 over 14 weeks on a hydrogen and helium discovery in South Australia - it's now capped at $231M.

That’s as strong a market signal as any for TEE to focus some efforts on exploring the natural hydrogen and helium potential of its own ground...

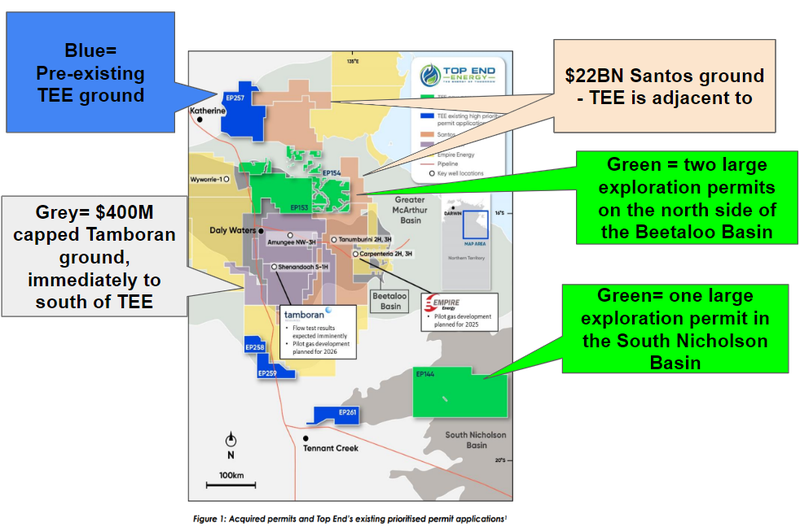

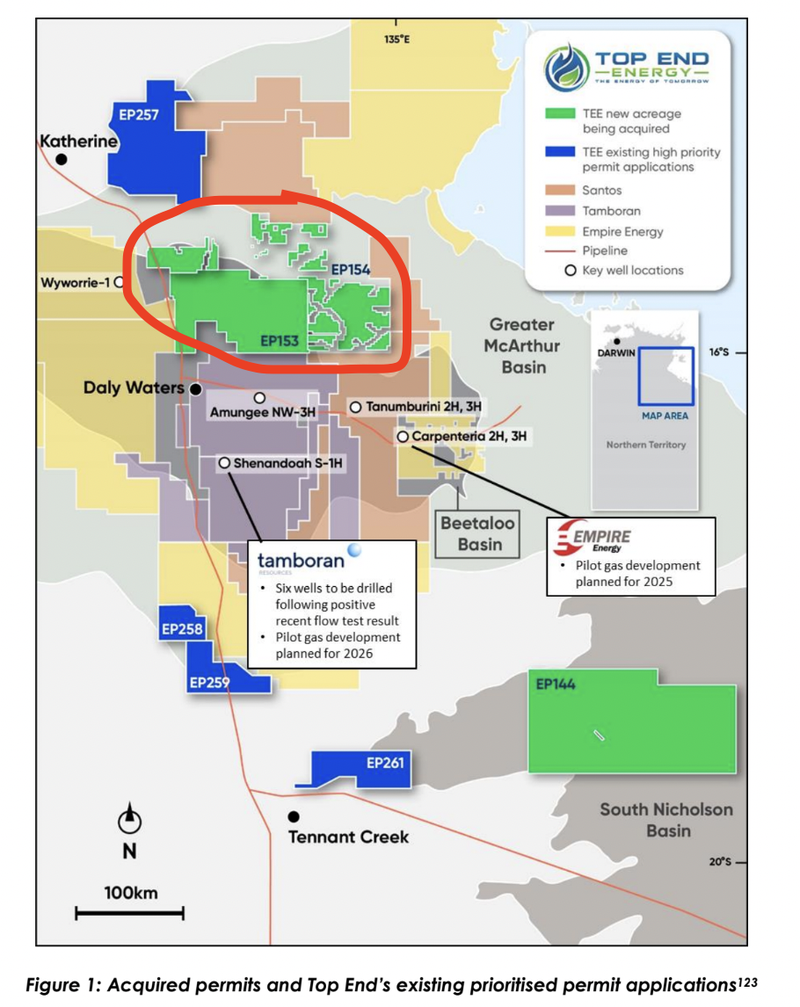

Below is TEE’s acreage on a map - green is the new TEE ground, blue is TEE’s existing ground.

Directly below TEE is the $400M capped Tamboran Resources which is in the middle of an extended flow test on its acreage. Tamboran is the most active player in the region and is backed by US oil and gas billionaire Bryan Sheffield.

(Source)

To go with today's deal TEE also raised $2.1M at 12c. Those new shares will come to market around 8th March.

Once the capital raise is settled, TEE will be capped at ~$12M and should have around ~$3.5M in cash (Dec 31st cash on hand plus the new $2.1M).

That means TEE trades with an EV of ~$8.5M.

With very few shares on issue, we think the current valuation leaves plenty of room to re-rate the stock higher should the company deliver any material catalysts from its projects.

We have been holding TEE since 2021, and have held onto our entire position since then. We also participated in the 12c TEE placement.

It’s been a while since we wrote about TEE, so given the new assets and fresh round of funding, it's time we caught up to speed.

We have been invested in TEE for almost 3 years now, participating in pre IPO rounds during 2021. We have held our entire position for this whole time.

Given TEE’s new assets, we are hoping that 2024 is the year things start really moving.

TEE gives us exposure to three different macro thematics:

- East coast gas: TEE now holds ~198,000km^2 of ground across the NT, QLD and WA. We are primarily Invested in the NT projects surrounding the Beetaloo Basin.

- Natural hydrogen: TEE is looking at the natural hydrogen potential of its NT/WA assets. Hydrogen is an emerging fuel crucial to decarbonisation.

- Helium: TEE is also looking at the helium potential for its NT/WA assets. Helium is a critical input in the semiconductor manufacturing industry and sells for multiples the price of natural gas.

Our Investment Strategy is straightforward when it comes to TEE.

We plan to hold onto most of our Investment as TEE works up its projects and then will look to de-risk (hopefully at much higher prices) as the company gets closer to a big drill program.

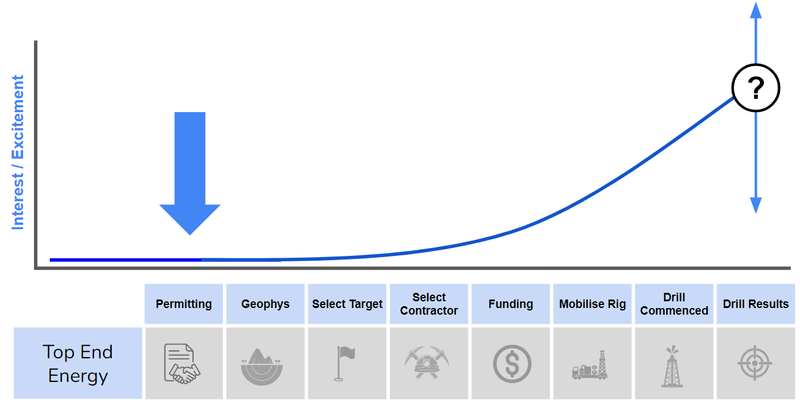

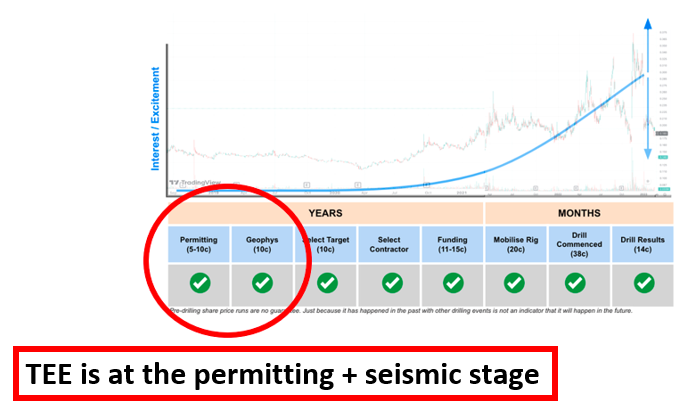

Here’s a very basic chart that shows how energy companies gain shareholder interest over time as they progress toward drilling:

Today TEE took another step toward its first drill program by acquiring a large chunk of granted tenure in and around the Beetaloo Basin in the NT.

The projects were acquired from the Hancock Energy - one of the privately held vehicles for Australia’s richest person Gina Rinehart.

Gina is no stranger to the oil and gas space having spent $450M to takeover Warrego Energy in the Perth Basin last year.

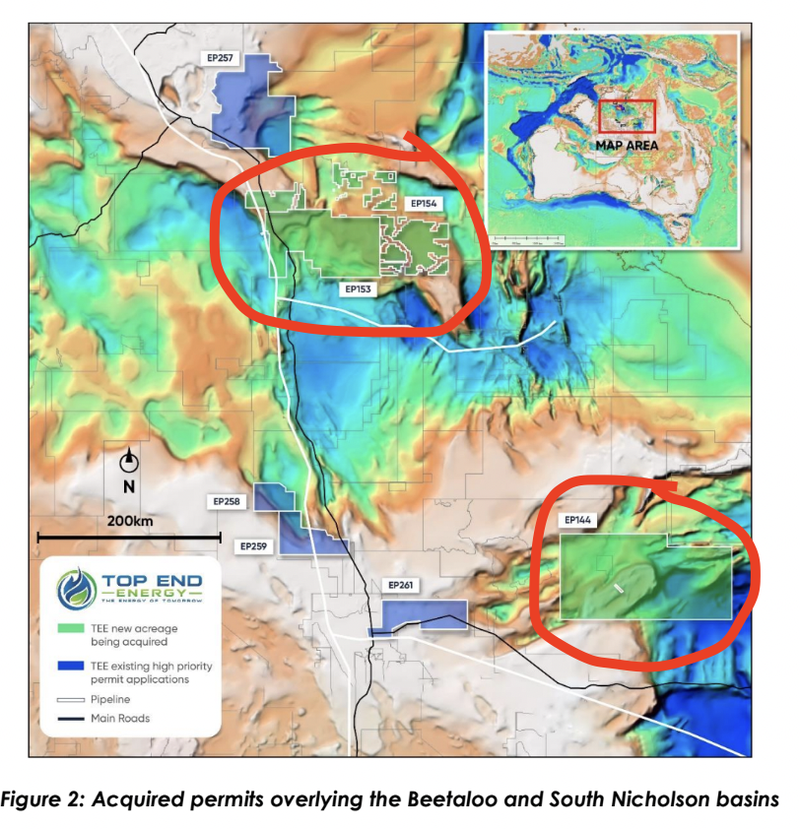

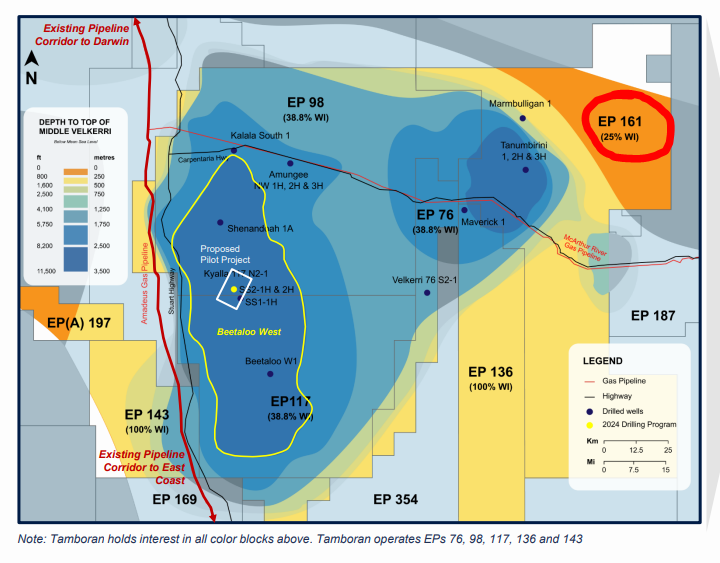

TEE’s new ground comprises a total of 27,885km2 across the northern flank of the Beetaloo and South Nicholson Basins:

(Source)

The key difference between TEE’s existing permits and the newly acquired ones is that the new ones are already granted, and have pre-existing native title agreements in place.

That means TEE can start working up the projects straight away.

TEE’s is still waiting for the highest priority permits near the Beetaloo to be granted - once granted they will be the first granted in the NT in 9 years.

We see this as a formality - but it's been a long wait, and while TEE has done all it can to get it granted - there’s always a risk it doesn't go through, so we are eager to see this ticked off.

While we wait, we like that via its deal with Hancock Energy, TEE has moved to secure additional ground in regions and play types the company is already very familiar with.

The new permits acquired today cover ~27,885km2 across the northern flank of the Beetaloo and South Nicholson basins - both areas where TEE has existing permit applications.

(Source)

Why we think the deal is a big step forward for TEE...

We especially like today’s deal because it gives TEE some more advanced, already titled ground in and around the Beetaloo.

The timing is also pretty significant...

The Beetaloo has been referenced as the next major gas production hub of Australia with enough gas to power Australia for up to 300 years.

The size & scale for the potential is so big it has already attracted interest from US oil & gas billionaire Bryan Sheffield.

The US billionaire came in and invested in the biggest player in the region Tamboran Resources, which is currently capped at $401M.

(Source)

Sheffield’s investment is especially interesting as it brings fracking experience to a company that is ultimately looking to commercialise unconventional oil and gas reservoirs.

Since he got involved, Tamboran has been gradually increasing the scale of its stimulation programs - with the next one said to be the biggest planned for the basin.

As the $12M capped TEE proves up its own Beetaloo ground, we see the presence of the US billionaires and Tamboran as a significant bonus and evidence that there is significant value to be extracted in the basin.

On top of that, should Tamboran successfully move into production, we would expect TEE’s ground to be valued at multiples of the current valuation on which it trades today.

How today’s acquisition fits into TEE’s NT exploration strategy

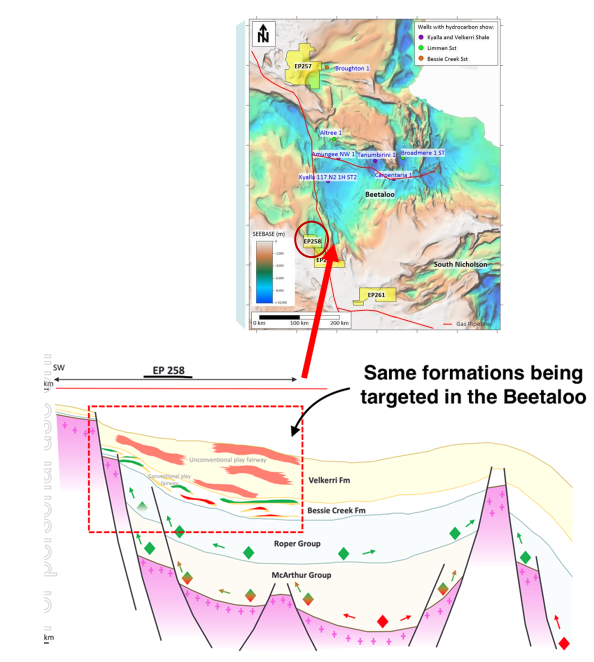

TEE’s exploration strategy from the very beginning has always been to target the same reservoirs Tamboran is going for inside the Beetaloo Basin BUT do it on the basin fringes - what is sometimes called a “Basin Margin Play”.

Today’s acquisition means TEE now has a lot more ground to the northern edges of the Beetaloo.

The new ground sits right next to Tamboran’s ground where most of the capital in the basin is being invested.

(Source)

TEE also has helium/hydrogen optionality

The gas exposure to all the work Tamboran is doing is a main part of our Investment in TEE but we are also interested in the natural hydrogen/helium work the company is doing.

For context - when we first Invested in TEE we mentioned that a key reason for our Investment was because TEE was “Mandated to acquire new projects”, especially in the helium, hydrogen, carbon capture and ammonia space.

Since its IPO the company has done reviews looking at the natural hydrogen/helium potential of its existing projects.

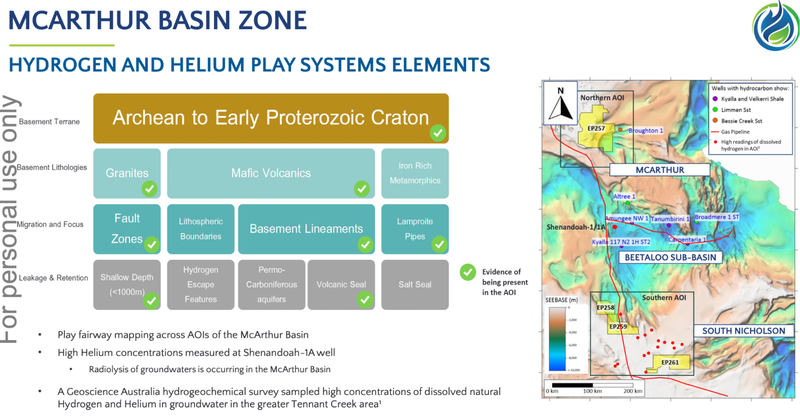

Back in September TEE put out a presentation focusing on the hydrogen/helium potential of its projects.

The presentation was prepared for the South East Asia Australia Offshore & Onshore Conference (SEAAOC) - the largest petroleum conference in Northern Australia.

One of the slides we liked the most was the following which touched on the high helium grades found in a nearby well (Shenandoah-1A):

See the full presentation here.

This is where we see the potential for big unexpected surprises from TEE.

The market knows relatively well what's going on in the Beetaloo from an unconventional gas perspective because of all the news that comes out of Tamboran.

But there is very little newsflow about the hydrogen/helium potential in the region.

We see it as almost a free option on a major hydrogen/helium discovery with the main value in TEE coming from its exposure to the Beetaloo gas story.

AND we have seen what can happen when a company makes a hydrogen/helium discovery in Australia - the Gold Hydrogen discovery in SA for example.

Gold Hydrogen announced a discovery in late October last year and its share price hasn't looked back ever since.

Pre-discovery the company was capped at $26M, now it is capped at $231M - ~10x higher.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

TEE trades at a fraction of Gold Hydrogen’s market cap and whilst it is very early days in TEE’s exploration, we think the market is attributing very little value toward the hydrogen/helium prospectivity of its projects.

Especially considering the high helium/hydrogen grades found in nearby wells (Shenandoah-1A) and (Wyworrie-1).

Obviously it's far too early to know what could come from a hydrogen/helium perspective across TEE’s ground but we will be watching to see any updates from the company on this front.

Our TEE Investment Strategy

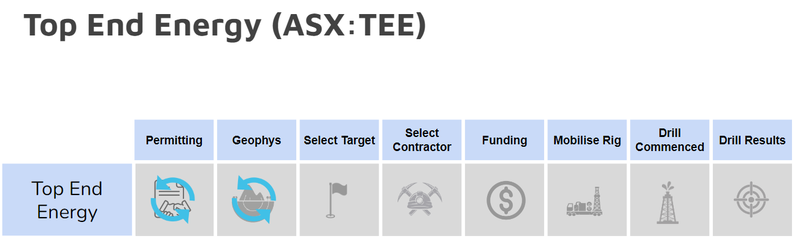

TEE is still relatively early in the exploration process for its projects.

At this stage, most of its projects are in the “analyse data” stage, which is a few steps before any drilling work can start.

Instead of going out and drilling as many wells as possible, the company is doing all the groundwork looking to work up projects to a point where they are attractive enough to either drill OR to find partners for.

We don't mind this strategy considering how low TEE’s market cap is and the current state of the small cap market.

Our view is that as TEE works up its projects and sets clear drill targets the market starts to value its prospects accordingly.

It will also give us an opportunity to execute our oil & gas Investment Strategy which is as follows:

- Invest early, as the company is in the early exploration work stage.

- Increase our Investment, as the company de-risks the project through permitting, geophysics and target generation.

- Top Slice, if the share price runs in anticipation of exploration results

- Free Carry, into results while still maintaining a large position to be leveraged for a discovery

- Evaluate our position post-drilling.

We think we are now in the early stages of phase 2 of our strategy.

We are hoping that when TEE eventually drills its project it can achieve our Big Bet which is as follows:

Our TEE ‘Big Bet’

“TEE makes a new large scale gas discovery in Australia and becomes a takeover target from one of the oil and gas majors at 1,000%+ from our Initial Entry Price.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our TEE Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

The latest from TEE’s NT neighbours

A large part of our Investment approach to TEE has been to Invest and patiently hold as the majors in the NT de-risk the region.

In the background, TEE would get its permits granted and slowly work them up to being drill-ready prospects.

As a result, we are always tracking the major's activities in the region.

Below is our latest take on the region.

Tamboran Resources (38.75% - capped at $402M), Bryan Sheffield (38.75%) and Falcon Oil and Gas (22.5% - capped at $220M)

What they are doing: Extended flow test running for the Shenandoah South well.

When it is happening: Right now. Tamboran and its partners just announced the results from the first 30 days with an average flow rate of 6.4 MMcf/d. Results from the 90 day mark are expected in April.

(Source)

Santos (75% - capped at $23BN) and Tamboran Resources (25% - capped at $402M):

What they are doing: The Joint Venture just recently submitted Environmental Management Plan’s (EMP) for a 200-240km 2D seismic survey over its permits.

(Source)

When it is happening: Right now.

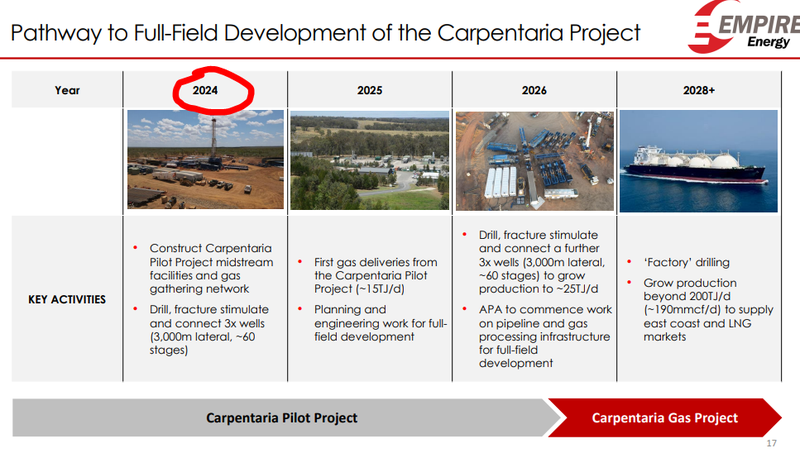

Empire Energy (capped at $140M)

What is it doing: Empire is looking to make a Final Investment Decision (FID) on a pilot plant at its Carpentaria project. The target is to produce up to 25 TJ of gas per day.

When it is happening: Empire expects to be making an FID “in the coming months”.

(Source)

What’s next for TEE?

Issue of placement shares 🔄

To go with today’s acquisition TEE also raised $2.1M at 12c per share.

The shares from the raise are expected to be issued “on or around 8 March 2024”.

Work program for newly acquired projects 🔄

TEE confirmed it would be putting out a work program for the blocks acquired in today’s deal.

These will set out how TEE goes about exploring the projects over the coming years so we are looking forward to that news.

Permitting in the NT 🔄

With the native title approval secured and Section 31 Deed signed, we want to see TEE’s EP 258 application granted.

Once granted, this would mark the first exploration permit (EP) granted in the Northern Territory since 2015.

Once granted TEE’s plan is to run a ~2,500 line kilometre airborne gravity survey as well as look at the potential helium/hydrogen potential of the project.

Farm-down QLD gas project 🔄

TEE confirmed in its recently quarterly report that its plan was to “Initiate a farm-down process for ATP 1069 with the aim of securing a joint venture partner”.

We are hoping to see some newsflow on that front.

What are the risks?

In the short term the key risk to our TEE Investment is “permitting risk”.

TEE isn't doing any high risk exploration as yet across its projects BUT there is still a major hurdle the company faces which is the permitting at its NT applications.

TEE has now been waiting for over 2 years for the permits to be granted and despite making progress with native title holders hasn't managed to get its permits granted as yet.

There is always a chance TEE fails to get the permits and loses a large chunk of its landholding in and around the Beetaloo basin.

If this were to happen we would expect TEE’s share price to re-rate lower.

To see other key risks we have listed, check out our TEE Investment Memo here.

Our TEE Investment Memo

In our TEE Investment Memo, you can find:

- TEE’’s macro thematic

- Why we Invested in TEE

- Our TEE “Big Bet” - what we think the upside Investment case for TEE is

- The key objectives we want to see TEE achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.