State of Arkansas to remove sales tax on lithium? $6M capped PFE the only ASX listed player, surrounded by giants

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 11,853,770 PFE Shares and 3,460,950 PFE Options at the time of publishing this article. The Company has been engaged by PFE to share our commentary on the progress of our Investment in PFE over time.

Energy supermajors AND the US government itself share a clear goal to build up a large lithium industry in the USA.

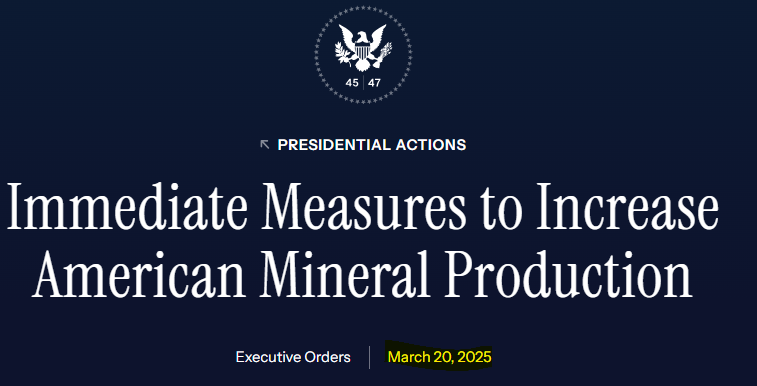

Trump recently signed an Executive Order seeking to stimulate the USA’s local critical minerals supply chain.

The US Department of Energy is handing out grants worth hundreds of millions of dollars to lithium companies...

China is threatening to ban the export of lithium processing technology.

And we haven't even started talking about the escalating tariff related trade wars between China and the USA...

The USA lithium industry is mainly focussed on one part of the country - the Smackover region in the state of Arkansas.

The Smackover is teeming with investments from global energy giants seeking to use Direct Lithium Extraction to produce the battery metal from its high grade lithium brines...

We are Invested in the only micro cap ASX listed company with acreage in the Smackover in Arkansas - ~$6.6M capped Pantera Lithium (ASX:PFE).

And now just in - BREAKING NEWS:

The Arkansas Senate just introduced a bill (SB568) to remove sales and use taxes for the lithium industry - a big signal Arkansas is backing the industry and seeking to create an attractive environment for capital.

While it still needs to go through some legislative hurdles, this is definitely a good sign for PFE & the petrochemical giants active in Arkansas.

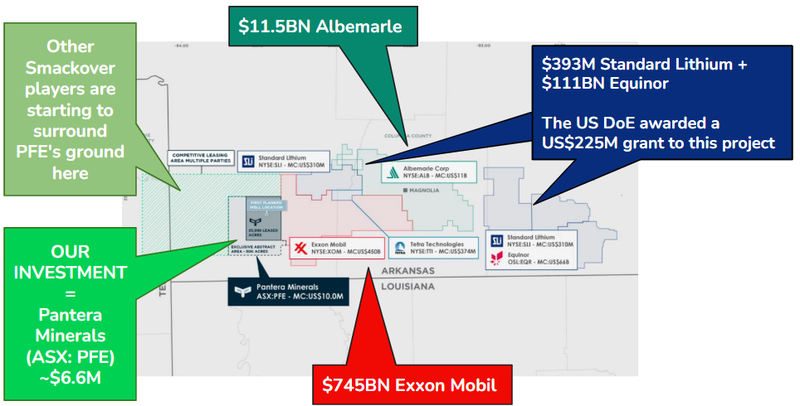

$745BN ExxonMobil and the Norwegian state backed $111BN Equinor are both building lithium businesses near tiny PFE’s +26,000 acres.

(PFE actually has an exclusive leasing area of up to 50,000 acres.)

Inside that 50,000 acres, PFE has established an exploration target of 436Kt to 2.96Mt of Lithium Carbonate Equivalent (LCE).

Exxon has at least ~120,000 acres directly next door to PFE.

Exxon has been spotted drilling near PFE’s acreage, a potential leading indicator of the prospectivity within PFE’s ground...

Exxon’s plan is to be producing lithium in the Smackover by 2027.

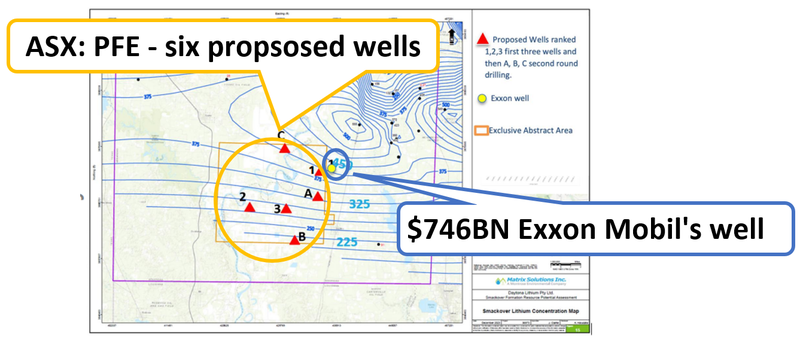

Here’s where PFE is on the map in relation to the other major players:

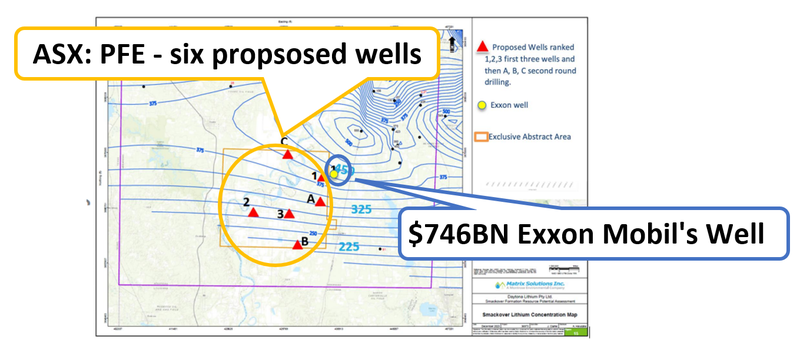

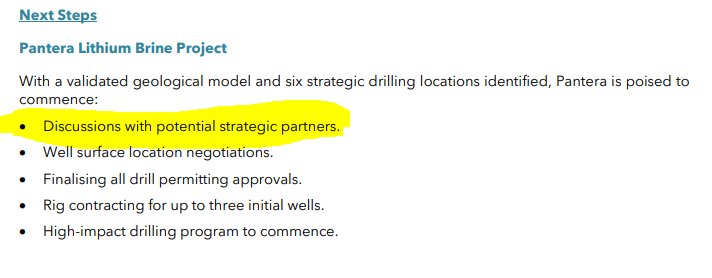

Last week, PFE released a plan to drill three wells across six potentially “lithium rich” targets with the goal to definitively show that PFE does indeed have some of the best Smackover ground.

(of course actually drilling will be the only way to do this)

We think that given the calibre of players already in the Smackover, and the new tax incentives being mooted by the Arkansas legislature, PFE could attract potential interest from a funding partner to drill those wells...

In fact, PFE mentioned last week and re-iterated in this afternoon’s ASX announcement, that ‘discussions with potential strategic partners’ is commencing...

With the lithium macro environment where it is today, external validation of the assets via a non-dilutive funding deal with a strategic partner could be what triggers a swift re-rate in PFE’s market cap.

In today’s note, we will cover:

- The US push to increase mineral production and how it impacts PFE

- The M&A happening for other lithium brine assets

- And the latest news coming out of Exxon and Equinor in the Smackover

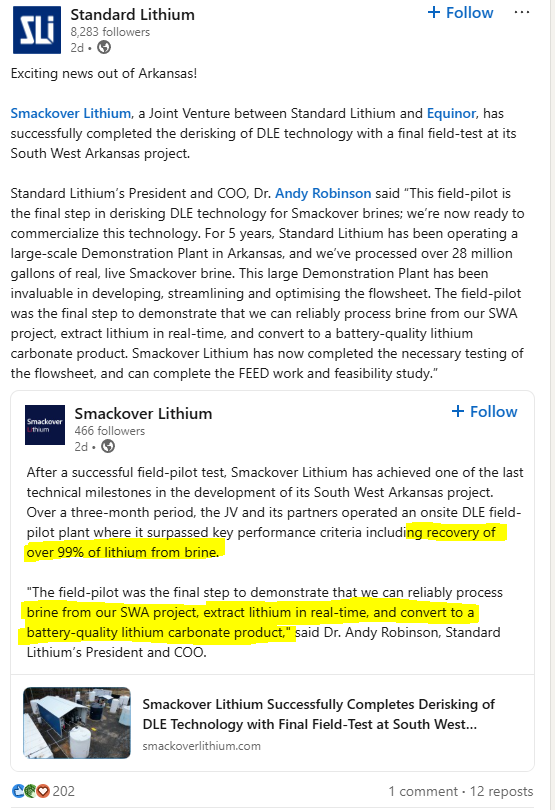

Just a few weeks ago, Equinor produced battery-grade lithium carbonate from its in field demonstration plant (in conjunction with TSX-listed Standard Lithium) in the Smackover.

Proving that, yes, Smackover brines, like what PFE is sitting on top of, can be converted to battery-grade lithium carbonate.

As we hinted at above, the US government is also backing this specific region and stumping up serious coin to support it.

Late last year, the US Department of Energy gave a US$225M grant to Equinor and Standard Lithium...

In exchange for no equity... and it was not a loan - just a ‘grant’ to stimulate the industry.

And now Arkansas has just introduced a bill with its own tax incentives for lithium development activities.

We think that under Trump’s various new Executive Orders and directives, large institutional US money could start chasing ASX listed resource projects - especially projects in the USA (read our full comments on that here).

As we mentioned above, Exxon has already drilled a well right next door to PFE’s ground - a good signal PFE’s ground might be in the sweet spot of the Smackover.

As you can see on the map higher up, PFE is effectively being surrounded by ExxonMobil and others.

We think the fact that acreage is being snapped up all around PFE’s ground implies that the big players think PFE could well have some of the best ground in the area.

However PFE has yet to bring a brine sample to surface, so no one knows for sure.

PFE’s plan is to drill and prove up a maiden JORC lithium resource for its project in H2 2025.

(building off last year’s declaration of a 436Kt to 2.96Mt of lithium carbonate exploration target)

AND as we just mentioned, according to an announcement last week, PFE is about to commence “discussions with potential strategic partners” which could accelerate drilling progress significantly...

Again - we think that under President Trump, various types of US money will start flowing into US based resources projects which is good for any “discussions” PFE may be having.

The US under Trump is trying to boost domestic lithium production.

Just last month, US President Donald Trump signed the following Executive Order (specifically mentioning critical minerals which includes lithium):

(Source)

This Executive Order was designed to create urgency in the domestic mining industry, with clearly defined timeframes for agencies to report back with solutions to the problem.

Trump’s main goal here is to reduce reliance on imports for critical raw materials - this is a key piece of leverage that China has in ongoing friction between the two global powers.

Underscoring this is Trump’s move today to pause the wide sweeping global tariff on every country... except China...

On China, he increased tariffs to 124%.

~77% of raw lithium supply comes out of Australia and South America. (Source)

65% of processed lithium comes out of China. (Source)

But, and this is crucial, the US currently has negligible representation across the entire supply chain.

First step to increase domestic production and by using DLE technologies also own the downstream, processing the raw material into final battery grade products.

We think the big push from the petrochemicals giants will mean Smackover will become the capital for the USA’s lithium brine industry.

PFE is a first mover (and we think “only” mover for now) out of all the companies on the ASX and now holds ground right in the middle of the Smackover region.

PFE is yet to drill its project, but last week it put out an announcement showing six drill ready targets which could form the basis for PFE defining a maiden JORC resource on its ground.

Six of those targets are right next to that well we mentioned earlier from Exxon:

PFE’s target is to drill its project in the second half of this year.

To drill PFE will need to lock in some funding for the wells which is where we think the macro environment is increasingly moving in PFE’s favour.

And as mentioned earlier, PFE has mentioned that “discussions with potential strategic partners” were about to begin...

Competitive tension is increasing for brine assets...

Lithium valuations are currently bombed out on the ASX.

(Which is a big reason why PFE is trading where it is today - capped at $6.6M)

As the market almost always does with emerging resource markets like lithium, it overshoots to the upside and undershoots in a big way on the downside.

We think the market has definitely overshot it now with lithium names...

With valuations where they are across the sector, we think the likelihood of M&A deals, strategic partnerships and farm-in deals becomes more and more likely.

Deals activity usually only ever happens when markets are stable - that can mean stable in a bad way (at the bottom of a bear market) OR stable in a good way (at the top of a bull market).

Those dynamics means deals happen at the peaks and troughs of the market.

Last week we saw evidence of valuation dislocations and appetite for M&A when ASX listed lithium brine developer Galan got a bid at 3x its market value...

More proof of the dislocation in valuations... the board rejected a 3x premium to its market price...

(Source)

Prior to that, there was Rio’s acquisition of Arcadium Lithium for $6.7BN.

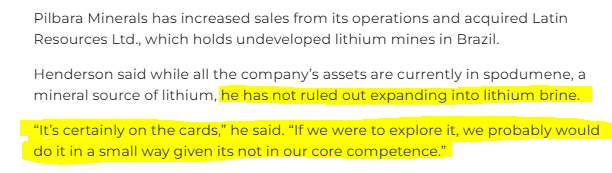

Even Pilbara Minerals, one of the biggest pureplay hard rock miners is rumored to be looking at brine assets...

(Source)

Brine projects have the potential to be lower OPEX in the long run which is why we think corporates are attracted to them.

And now that deals in the brine space are being made public, we think this is starting to ratchet up the competitive tension from the players who were sitting and waiting to pull the trigger on deals.

This could also mean urgency increases to do deals on assets like PFE’s, which may be on corporate watchlists.

In the short term, with the lithium macro environment where it is today, we think the market needs external validation and non-dilutive funding to trigger a re-rate in PFE’s market cap.

So as the macro environment improves for PFE, this should only increase the likelihood of a deal happening.

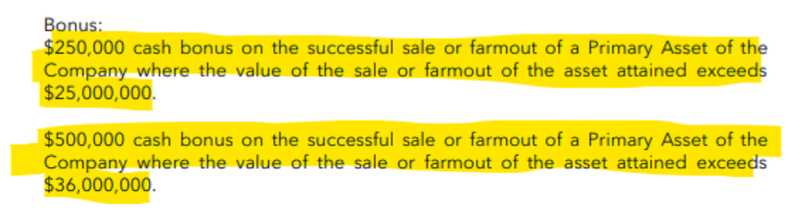

In fact, PFE’s Executive Chairman and CEO Barnaby Egerton-Warburton, is specifically incentivised to secure a sale or farm out on PFE assets.

A few months ago we noticed incentives for Egerton-Warburton set by the board to deliver a “sale or farmout” at a $25M to $36M valuation:

(Source)

PFE’s current market cap is ~$6.6M.

We are backing Barnaby and his team to deliver something that re-rates PFE’s cap to something in line (fingers crossed) higher than those deal values...

Our PFE Big Bet:

“PFE to return 10x by making a discovery and defining a deposit significant enough to move into development studies”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PFE Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

The latest out of the Smackover

Other than today’s news of Arkansas’ proposed lithium development tax incentives, last month we saw some pretty big news out of $393M Standard Lithium and $111BN Equinor in the Smackover region.

Standard said that the Joint Venture (JV) was able to take brines from its ground in the Smackover and then convert it to a battery grade lithium carbonate product in real time.

The news said that the JV had managed to achieve “99% lithium recoveries”.

(Source)

This was a “field pilot” which means Standard and Equinor managed to produce battery grade lithium carbonates using its DLE tech in an environment that is as close to real life conditions as possible.

Usually DLE tech is tested off site in lab environments.

Standard and Equinor showed they can replicate strong recoveries on the ground as if the project was in production.

Now they can take all of their learnings and scale it up with an engineering/feasibility study.

Standard and Equinor are at the stage where they know they can make their project work - they just need to spend the capital to get it into commercial production.

Seeing giant oil & gas players like Equinor technically de-risk its project is good for everyone with projects in the region...

Especially for a company like PFE.

We think PFE can reap the benefits of these developments in the Smackover, and let the bigger players draw more capital to the area which increases the look through valuation of its project...

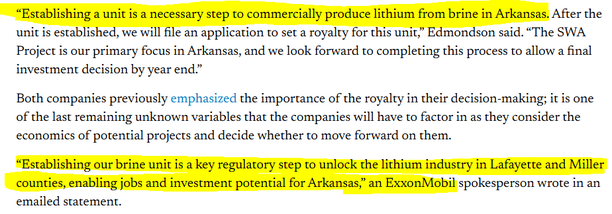

Equinor and Exxon are also working on permitting their projects (unitisation)

We also noticed Equinor and Exxon both recently applied for the unitisation of their lithium projects in the region.

(Source)

Unitisation is a fairly foreign concept for us in Australia, but it's actually a pretty important signal for a company’s intentions with a project in the USA, and it is typically applied to oil & gas projects.

When a company goes to unitise acreage, it is essentially looking to pool all or some portions of multiple leases into one single unit.

The main reason for this is so smaller leases can be combined to cover a larger portion of a reservoir unit that extends over several different leases.

It’s basically a way of taking separate leases and turning them into one single giant lease.

So from a technical perspective, when a company commits to unitisation, it is starting to consider how it would go about developing its acreage.

(Source)

This is where the signalling is important (especially relative to PFE).

That push to unitise by Exxon and Equinor shows us that they are serious about taking their projects into development...

Which is again... positive for PFE’s ground in the Smackover.

What’s next for PFE?

🔄Update on strategic partners

We want to see PFE engage with a strategic partner to help realise the value of its Smackover ground, given these discussions are about to commence.

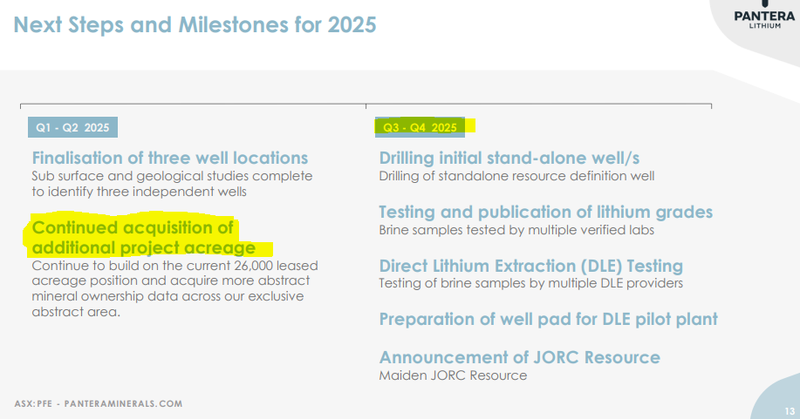

Beyond that, here is what PFE has recently signalled as the next major milestones for the company.

The following slide was from PFE’s most recent investor presentation which you can check out here.

(Source)

- 🔄Continued acreage growth (Q1 - Q2 2025)

- 🔲 Drilling initial stand alone well/s (Q3 - Q4 2025)

- 🔲 DLE (Direct Lithium Extraction) Testing (Q3 - Q4 2025)

- 🔲 Maiden JORC lithium resource (Q3 - Q4 2025)

(We’ve visited the project area ourselves - Read our site visit breakdown here)

Arkansas Lithium Summit - lithium come back?

What are the risks?

The main risk for PFE in the short term is “Funding risk”.

PFE is pre-revenue and to be able to drill its project or expand its acreage it may need to raise more capital.

Capital raises, in the short term may lead to more dilution and may take place at discounts to market prices.

PFE has mentioned that it is going to start discussions with strategic partners which could result in some non-dilutive funding for PFE, however there are no guarantees that these discussions will be successful.

PFE had ~$2.3M in cash at 31 December 2024.

Funding risk

PFE is a micro cap stock and will need to raise more capital to continue expanding its foothold in the Smackover Formation. Capital raises can lead to dilution and may take place at a discount to market prices, reducing the value of PFE shares

Source: “What could go wrong? - PFE Investment Memo 4 March 2024

To see more risks read our PFE Investment Memo here.

Our PFE Investment Memo

Below is our Investment Memo for PFE, which provides a short, high-level summary of our reasons for Investing.

In our PFE Investment Memo, you can find the following:

- What does PFE do?

- The macro theme for PFE

- Our PFE Big Bet

- What we want to see PFE achieve

- Why we are Invested in PFE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.