SLM to drill new Brazil lithium project in 4 weeks

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 2,863,637 SLM shares. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time. Some shares may be subject to shareholder approval.

We backed Solis Minerals (ASX:SLM) as our 2023 Small Cap Pick of the Year to deliver success in lithium exploration in Brazil.

- SLM has the same team behind Latin Resources and it’s Brazilian lithium success

- SLM is chasing more Brazil lithium success

- SLM has a good share structure

- Latin Resources is a major shareholder of SLM

Today SLM have announced an option on a NEW lithium exploration tenement in Brazil, and will be drilling it in 4 weeks.

This option could be part of a much larger pre-existing set of 24 tenements at a second lithium project in Brazil.

The project is called “Mina Vermelha”

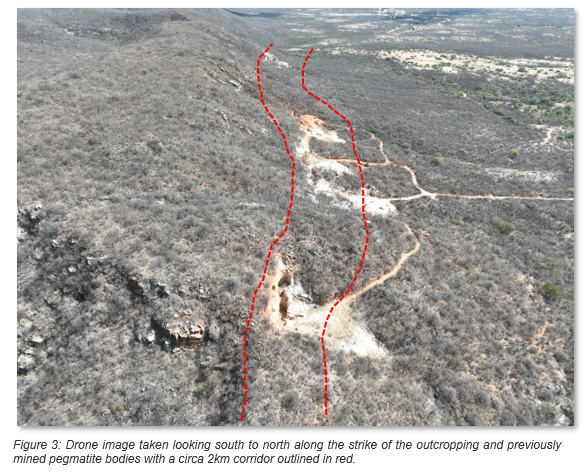

Mina Vermelha has already produced grab samples with grades of 3.45% and 3.07% lithium from a 2km long stretch of pegmatite outcropping.

SLM is drilling it in four weeks...

SLM has secured an initial drilling rig for an upcoming 1,300m 8-hole program and is currently looking to secure a second rig to pepper the 2km pegmatite outcropping with drill holes, and hopefully declare a lithium discovery at Mina Vermelha :

Today we will cover SLM’s new Mina Vermelha tenement.

We have already seen that the SLM share price wants to run on potential of a Brazilian lithium discovery by the now “small cap famous” Chris Gale and the Latin Resources team.

We believe the first SLM run was off the back of interest from cashed up Latin Resources investors who wanted to chase “LRS 2.0”, combined with a tight cap structure and the Brazil lithium thematic.

Again, SLM is drilling its newly acquired lithium project in 4 weeks time.

In June, SLM ran from 16c to $1.34 on the back of SLM’s original lithium exploration project.

The company raised ~$8.1M at 55c (we took a decent swing at that cap raise).

Then a couple of disappointing initial drill results and delays on drilling saw the share price come back down to ~27c where it sits today.

We haven’t sold any SLM shares because we think SLM is eventually going to be the vehicle for the same LRS team to deliver LRS 2.0 - a new lithium discovery in Brazil.

Here is what our SLM Investment ride has looked like so far:

But now SLM has acquired a new project, its lithium in Brazil, it looks big and we will be seeing drilling commence in 4 weeks time.

With its tight cap structure, we already have seen that the SLM share price likes to respond to SLM drilling for lithium in Brazil. We just need a discovery this time to cement in the share price rise.

SLM’s original Jaguar project from June (which we named the (“Pegmatite Grand Canyon”) was an option for SLM to acquire the Jaguar project after 90 days of drilling and due diligence.

Again, a couple of disappointing initial drill results and delays on drilling meant that SLM had not been able to gather the drilling info they wanted to pay the $3.6M (plus 3M SLM shares) to acquire the project.

The Jaguar project owner refused to extend the option due diligence period for SLM to unlock the secrets of the pegmatite grand canyon before buying...

And SLM made the prudent decision NOT to stump up the cash to acquire the project that looked great on the surface, but didn’t deliver amazing initial drill results underneath.

So SLM has protected its $8.1M in the bank from the raise and today announced a new Brazil lithium project, “Mina Vermelha” where drilling will commence in 4 weeks.

Small cap exploration is rarely a linear progression towards an economic resource that takes a stock up the charts in a predictable fashion.

With SLM we are backing the same team that delivered Brazilian lithium success in LRS.

Remember... it took SLM’s big brother, the Chris Gale helmed Latin Resources, years of having a crack at various projects until it finally acquired and unlocked the Colina deposit’s value for LRS.

Eventually the drill bit, and a lot of trial and error, helped send LRS into the big leagues, maybe permanently - Latin Resources is now capped at $750M.

And a sustained Latin Resources share price run from 2c to ~30c today.

It was a combination of exquisite timing, a bit of luck and sound leadership that made Latin a great home for the big funds’ capital that it eventually attracted.

We think the same team at SLM is capable of achieving a similar feat, or as we dubbed it in our initiation note, SLM becoming an “LRS 2.0”.

This is why we still hold our full SLM position.

Now armed with new tenements to drill for lithium in Brazil, we are hoping that SLM can deliver on this expectation.

Through their success at LRS, the SLM team is now well known in Brazilian exploration and investment circles, which we think gives them access to the best early stage projects in Brazil.

Here is a bit more on SLMs newly acquired project.

We note that SLM has applied what it learned from the 90 day due diligence period on their original Jaguar project which is reflected in the deal terms for the new option on Mina Vermelha.

Basically SLM are paying just $155k to secure a 12 months option to drill out the 2km of pegmatite outcrops on Mina Vermelha and assay the results.

IF SLM make a hugely valuable discovery within that time, they can then acquire the project for ~$7.9M of staged payments.

In our view, this is a much better structure than the last deal and gives SLM a lot of time and spare cash to aggressively drill out this new project.

More on SLM’s new lithium drill program in Brazil...

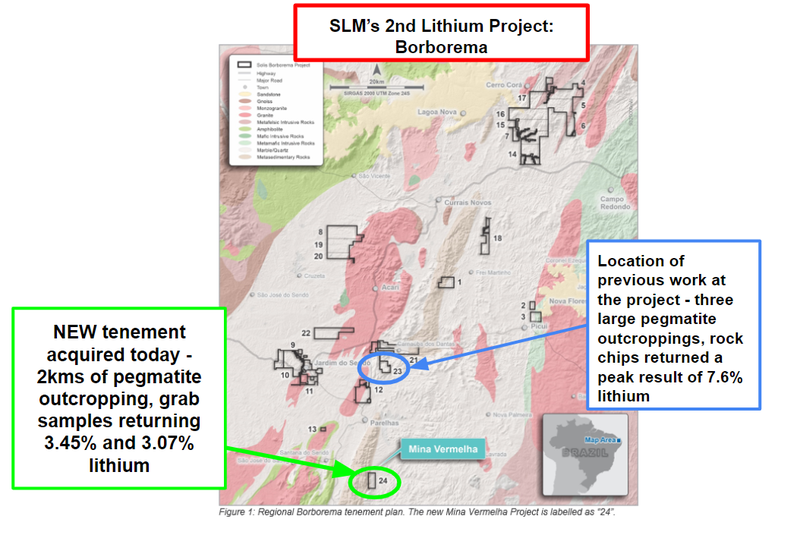

Today’s SLM announced the acquisition of a new tenement in the larger Borborema project.

Here, SLM intends to conduct a 1300m, 8 hole diamond drill program with one rig secured and another potentially to come - drilling is set to start in 4 weeks.

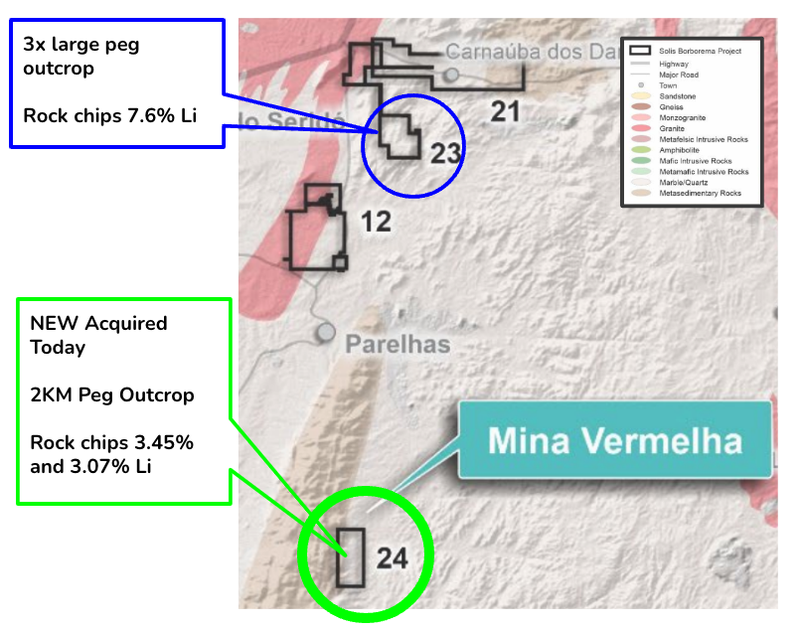

Below is a map of the key tenements at SLM owns at Borborema (including the newly acquired option on Mina Vermelha) which comprise ~25,000 hectares of ground:

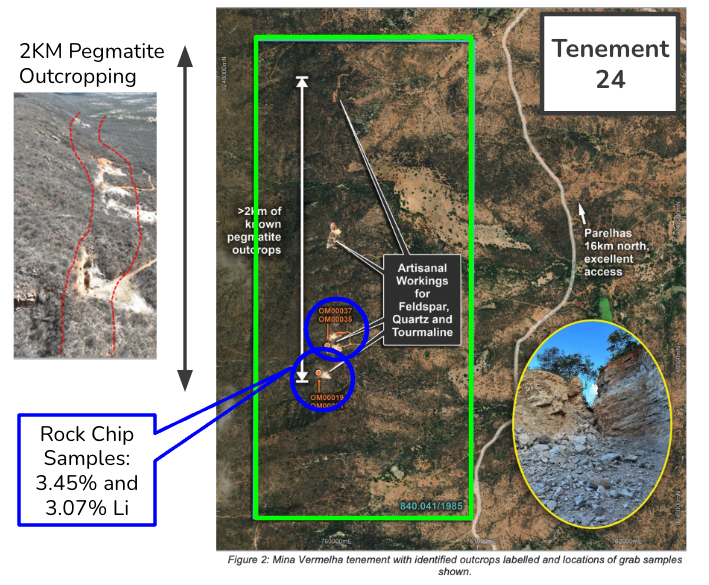

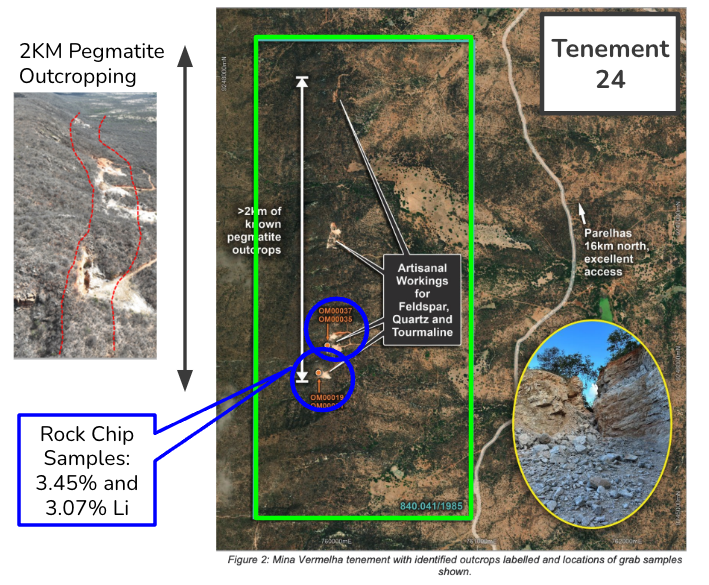

It’s all about projects 23 (blue circle) and 24 (green circle).

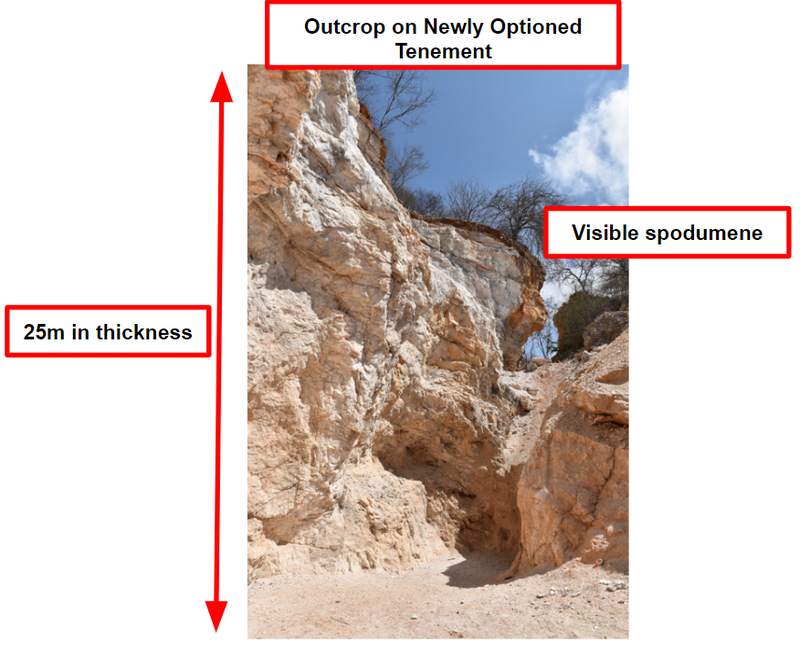

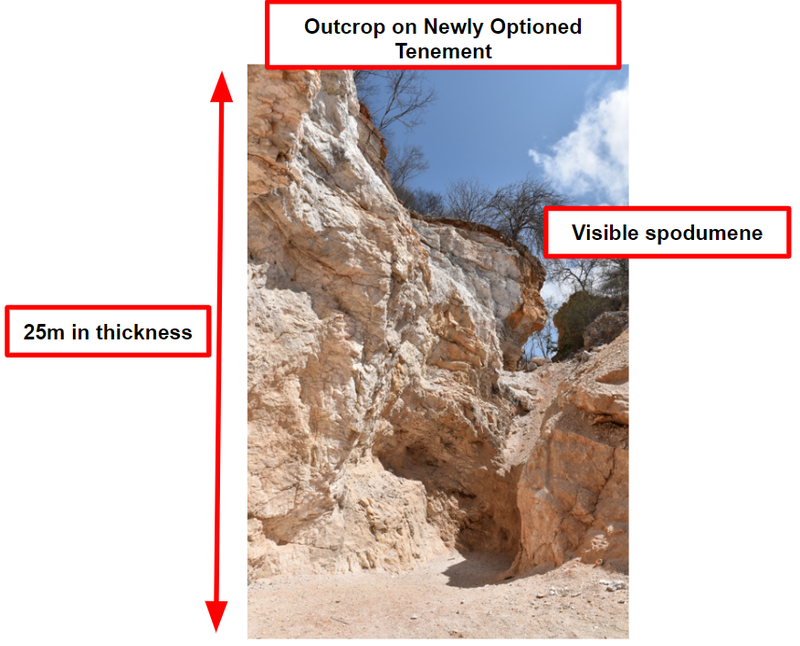

The new tenement is home to a 2km pegmatite outcropping, a promising sign:

That 2kms gets more interesting - with grab samples returning 3.45% and 3.07% lithium from this outcropping, part of which can below:

Putting it all together - this is what SLM is working with at the newly optioned tenement:

All up we see SLM’s second lithium project at Borborema as providing more than enough drill targets for this initial program, which we are hoping helps SLM re-rate once more, this time for good.

Finally, to give a sense for how big SLM’s package of tenements at Borborema is, below are all 24 tenements laid out in one map:

What will SLM pay for the new lithium tenement announced today?

We like that SLM is applying what it learned from its experience at the “Pegmatite Grand Canyon” project.

Perhaps foremost is to secure a longer due diligence period to allow maximum time to assess a potential acquisition (this time they have 12 months instead of 90 days).

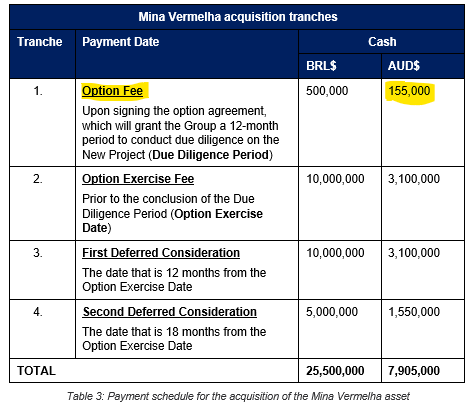

Below is how the deal for the new tenement at the 2nd Brazilian lithium project is structured:

A modest upfront option fee of $155K to secure a nice, long due diligence period of 12 months.

A further $3.1M to exercise the option and acquire the tenement - which we think is a fair price for the tenement’s potential, and SLM only have to pay it if they manage to make some big lithium discoveries on the project in the next 12 months

In 12 months time after that, if the option is exercised, a further $3.1M, and six months later another $1.55M.

If the first 12 months of drilling delivers above expectations, this may actually turn out to be pretty cheap.

If drilling DOES NOT deliver to expectations in the first 12 months, then SLM can walk away from the project and not make any more payments.

In addition to these terms, the vendor gets a 1.5% net smelter royalty (NSR) that SLM has the right to purchase for an amount determined by an independent third party evaluation of the Mina Vermelha asset.

Again, what stands out here compared to the old project is the 12 month due diligence period - and we think that there may be more diversity of targets on the project along an ample 2km stretch of pegmatite outcrop at just the newly optioned tenement alone.

Not to mention the 23 other tenements in the overall project area.

This brings us to our Big Bet for SLM:

Our SLM ‘Big Bet’

“SLM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - some of which we refer to in our SLM Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Introducing our new SLM Investment Memo

Now that SLM has a new project to drill, and has decided not to exercise the option over the first project, we have decided to launch our new SLM Investment Memo.

Almost nothing has changed in our Investment memo for SLM.

Only one of the key reasons is different, which the specific project SLM is targeting to deliver a lithium discovery in Brazil

In summary we like the vehicle, the management team and Brazil lithium macro theme.

We are backing this team to find and deliver a successful Brazilian lithium project.

Investment Memo 2: Solis Mineras (ASX:SLM)

Opened: 12-October-2023

Shares Held: 2,863,637

What does SLM do?

Solis Minerals (ASX:SLM) is a lithium explorer focused on hard rock lithium exploration in Brazil.

What is the macro theme?

Lithium is a critical material used in Electric Vehicle (EV) battery cathodes.

We believe battery metals are the most compelling investment theme of this decade. A lithium supply deficit is anticipated between 2024-2030.

SLM will be looking to replicate some of the success of Brazilian lithium companies Sigma Lithium and Latin Resources.

Brazil is already the world’s second largest producer of iron ore (second to Australia), now the Brazilian government is looking to grow its lithium production.

Our SLM Big Bet:

“SLM discovers and defines a large spodumene hosted lithium resource, leading to a re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SLM Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

Why do we continue to hold SLM?

1. Lithium hot, lithium in Brazil even hotter

We have written extensively about the broader lithium market and the decade long investment thematic we are in.

Once it gets to full capacity, Sigma Lithium will be one of the world’s largest lithium producers.

Off the back of this, “Lithium Valley” was launched in the State of Minas Gerais with the ultimate view of promoting foreign investment in Brazilian lithium projects.

We think a tidal wave of capital is going to come into Brazilian lithium projects. SLM is an early stage Investment in this sector.

2. Junior explorers have had success in Brazil

Sigma has gone from a junior developer with a market cap of <$200M to now trade at $6.5BN. Latin Resources has also gone from <$40M to now trade at $470M. Exploration success in Brazil is typically rewarded with a re-rate in a company’s market cap.

3. Latin Resources success

We have had success Investing in our other Portfolio Company Latin Resources which made a hard rock lithium discovery in March 2022 and has since gone from a share price of ~3.5c to 18.5c per share. Latin is now being called “Sigma 2.0”.

In a similar way, we hope to see SLM become a “Latin 2.0” (while remembering that just because Latin performed well doesn’t mean that SLM will do the same).

4. Same team as Latin Resources (Latin 2.0?)

SLM is backed by the same team that delivered Latin Resources discovery last year.

Latin’s Managing Director Chris Gale is SLM’s non-executive Chairman.

Chris Gale has taken Latin Resources from pre-discovery to a maiden JORC resource in <12 months and managed to raise $72M along the way.

SLM Managing Director Matt Boyes also holds a country manager role at Latin Resources. He has also had previous success in early stage lithium - overseeing Red Dirt Mining as it grew from a $15M market cap to $200M.

5. Backed by Latin Resources (more than ~15% shareholder, August 2023)

As of the 8th September, Latin Resources holds 15.25% of SLM shares - which means they are incentivised to see SLM succeed. We hope that SLM can leverage its Latin Resources connection to deliver success in Brazil for itself.

6. Original asset spinout from a well supported, successful bigger company

The SLM to Latin Resources structure has some similarities to how Kuniko was spun out of Vulcan Energy Resources. KNI had an outrageous run from 20c to touch $3.60 in the peak of the bull market, and has now settled at 40c.

We like to back a successful management team in sectors with strong momentum. We certainly aren’t expecting anything like this again, but note that the management team does play a role in the market's interest in a company.

We also have a view that a lot of the interest in Kuniko initially came from investors that had success with Vulcan, wanting to follow the Vulcan team’s new venture.

7. SLM Managing Director built a $200M+ lithium company before

SLM’s MD Matthew Boyes has been there and done it before.

Boyes was the Managing Director at Red Dirt Metals where he oversaw early development of the Mt Ida lithium project - which took Red Dirt’s market cap from ~$15M to in excess of $200M.

8. Tight capital structure

SLM has only ~87 million shares on issue with the largest position held by Latin Resources.

As of 22 August 2023, Latin Resources held 15.25% of SLM shares and participated in the 55c placement. Latin Resources potentially hold more than 15.25% given the recent share price action on SLM - we expect LRS is continuing to back SLM.

We note there are a relatively low ~9 million options on issue too, with the majority having an exercise price of 30c.

SLM has plenty of room to re-rate if it makes a successful discovery.

9. Latin Resources has a big investor following

SLM should benefit from the crowd of investors that follow (and have made money from) Latin Resources (Latin Resources has ~12,300 shareholders).

SLM is following a similar style exploration process and so investors who have had success with Latin Resources may look to buy into SLM with the hope SLM becomes “Latin 2.0”.

10. SLM about to drill a new pegmatite rich project

SLM has an extensive package of tenements across ~25,000 hectares at the Borborema Project which is home to a 2km of known stretch pegmatite outcropping, as well as a minimum of 9 known pegmatite outcroppings across just two of the 24 tenements within the project.

The project has already turned up rock chip samples from a spodumene bearing pegmatite with lithium grades of up to 7.6%.

Adding to that, are grab samples which returned grades of 3.45% and 3.07% lithium from outcropping pegmatites.

We think there are plenty of opportunities for a lithium discovery on the two tenements which SLM is initially focussed on, with optionality to drill other tenements as well.

NOTE: This reason #10 is the only change in our Investment thesis for SLM from our previous Memo

11. SLM is already listed in the US, Canada and Germany

“SLM” is the ASX stock code and the primary listing, but we also note that SLM is also already listed on the following other global small cap exchanges: TSXV: SLMN 🇨🇦 OTCQB: SLMFF 🇺🇸 FSE: 08W 🇩🇪.

This means that the potential investor pool that can invest in SLM is not just limited to Australian investors, but also much larger pools of investors in the USA, Canada and Germany.

What do we expect SLM to deliver?

Objective #1: Drilling at the company’s Borborema lithium project, in Brazil.

We want to see SLM drill out its Borborema lithium project quickly.

Milestones:

🔲 Drilling commencement

🔲 Assay results

Once drilling starts we will be watching for the following:

- During drilling - We want to see visual spodumene in the drillcores. Spodumene is generally the host rock for high grade lithium, visual spodumene will be a positive first indication of potential economic lithium mineralisation.

- After drilling - This will be all about waiting for the assay result — we’ll be looking for lithium grades above a level that is considered typically economic.

We have set up expectations for the assays as follows:

- Bull case (exceptional result) = Lithium grades >1.5%.

- Base case (good result) = Lithium grades 1-1.5%.

- Bear case (poor result) = Lithium grades <1%.

Objective #2: Complete due diligence on new tenement at Borborema lithium project (option) in Brazil

SLM has a 12 month due diligence period within which it can acquire its new Brazilian lithium tenement.

We want to see the company run its first drill program and do enough work to justify acquiring its project.

Milestones:

🔄 Due Diligence

🔲 Acquisition completed

Objective #3: Acquire new projects in South America/Brazil.

SLM said in its 31 May 2023 announcement that ”Solis’s primary objective is to quickly position itself by acquiring highly prospective underexplored projects in the northeast of Brazil”.

We want to see the company continue to leverage its in-country experience and acquire new projects in South America/Brazil. We expect SLM to continue to acquire promising projects.

Milestones:

🔲 Acquire/apply for new ground across South America/Brazil.

What could go wrong?

Exploration risk

SLM will be drilling a second lithium project and there is always a risk that after drilling the company doesn't find any economic lithium mineralisation.

As a result exploration risk is one of the primary risks going into the upcoming drill programs. Even if SLM does hit lithium, if the result is below market expectation the share price might react negatively.

Funding risk

Like most small cap exploration stocks, SLM is not generating any revenue, and is reliant on capital markets to fuel its growth plans.

SLM raised $8M (8th June 2023) and should be funded for at least the next few quarters but at some point the company would look to raise more funds to cover the development of its projects. This might be at a lower share price if this round of drilling results do not meet market expectations.

Sovereign risk

Whilst Brazil is a mining friendly country, it is a developing nation, and there is always some risk with regards to investing here.

Market risk

While lithium is a popular investment theme at the moment, lithium prices have pulled back before and its possible supply/demand dynamics change and in turn impact market sentiment for junior lithium explorers like SLM.

Investment Plan

Our Initial Investment is escrowed for the next two years, so we will be holding 100% of this position until June 2025.

Prior to this memo we have not sold any SLM shares and while we participated in the June 2023 placement at 55c and this stock is freely tradable, our plan is to hold until the company has had a chance to deliver some material progress.

If the company materially re-rates from the placement price on the back of positive news we may look to Top Slice some of the placement shares to try and claim back our Initial Investment and be Free Carried on the position.

This is our standard plan across all early stage exploration Investments.

The rest of the Investment plan depends on the outcomes of the company’s drill campaign and will be updated accordingly, and be governed by the 3 to 5 year holding periods as defined in our trading and hold policy disclosure.

A quick word on SLM’s first project - Jaguar

SLM finished drilling the “Pegmatite Grand Canyon” (Jaguar) project in September, with 12 holes completed and three holes sent for assays.

We had visual spodumene in the drill cores, but we suspect both SLM and the market knew it wasn’t quite up to expectations (read our Quick Take).

SLM tried to negotiate an extension to the due diligence period on the option for the project, but this was not able to be negotiated on satisfactory terms with the vendor of the project.

SLM clearly came to the conclusion that the money and effort that might have been needed to unlock the project was a prudent use of capital.

In today’s announcement SLM said that the company has ultimately abandoned this project, which would have been a tough decision, but we think it is the right thing for the company to do, given the large potential US$3.7M ($5.77M) payment to exercise the option.

We’ve experienced this before as Investors in small-cap exploration companies.

Sometimes vendors ask for too much, are unreasonable, there are operational difficulties and ultimately the project just doesn’t satisfy a cost benefit analysis for a company.

Although we were disappointed that SLM walked away from the project, we think that management made the right call to preserve shareholder value and direct funds to other prospective opportunities.

Given this decision, and now that SLM has a new project to drill, we have decided to publish a new investment memo for SLM.

To see our full retro for our first SLM Investment Memo click here. Click the “SLM-IM1” tab to see the retro.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.