Microcap explorer Solis Minerals (SLM) setting stage for Peru copper drilling

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 363,637 SLM shares and 1,750,000 SLM Options at the time of publishing this article. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time. Shares, options and Initial Entry Price have been updated in accordance with contract amendment announcement

The copper price is threatening a breakout to all time highs...

AND our micro cap exploration Investment Solis Minerals (ASX:SLM) is getting ready to drill some of its Peruvian copper assets this year.

SLM has steadily amassed a 43,500 ha landholding on the coastal Peru belt, which holds potential for a large copper porphyry discovery.

Porphyries are giant, low grade discoveries that can prove extremely valuable. Peru is dotted with them - the country produces 10% of global copper output.

Slightly away from the coast, SLM has another asset called Cinto, that sits 15km away from the major Toquepala copper porphyry deposit - which is now a mine 2.5km wide and 700m deep.

It’s at Cinto that SLM has found high-grade copper including up to 7.14% Cu from surface grab samples:

A “surface” sample means they literally grabbed this rock off the ground.

This is a good starting point for more copper exploration - and the big question will be if SLM can find more mineralisation deeper - which drilling will test.

Today SLM confirmed it now has an access agreement at its Cinto asset and can get started again collecting more samples and doing some all important mapping work in the lead up to drilling.

Permitting for drilling is underway.

It’s very early days for SLM here, and aside from the high grade samples, the geochemical signature and base metal concentration ratios SLM is getting at Cinto are in very similar ranges to the metals content in that giant Toquepala deposit nearby - indicating porphyry style mineralisation.

So we are now looking forward to an exploration “roll of the dice” on drilling for a new copper discovery...

Hopefully into an all time high copper price.

Before today’s news, SLM was capped at ~$7.6M and held $5.6M cash at the end of last quarter.

We are anticipating increased interest in SLM in the lead up to planned drilling next quarter, and hopefully SLM’s market cap starts to increase as drill targets firm up and drilling draws closer.

Further down we have published our new Investment Memo for SLM - refreshing our Investment thesis for the company given how it's positioned now.

We will be tracking SLM as it moves toward what should be some promising drilling events in the coming months.

We originally got behind SLM to discover lithium in Brazil and become “the next Latin Resources”... but that project didn’t work out (as often happens in exploration).

So like any explorer, SLM has gone back to the drawing board and is allocating capital to another project - the current focus is copper exploration in Peru.

(we like that because the copper price has restarted its run over the last couple of weeks)

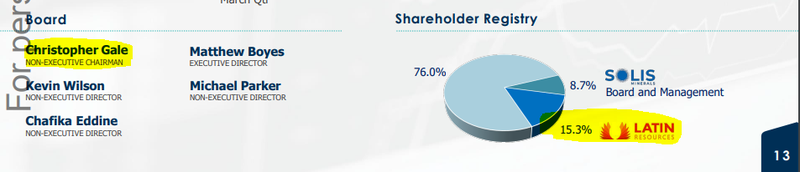

SLM still maintains a very tight cap structure, and it still has the Latin Resources team behind it, who have strong experience doing deals and making discoveries in South America.

SLM’s Chairman is Latin Resources Managing Director, Chris Gale. The $450M capped Latin Resources owns 15.3% of SLM.

Peru is a good place to be looking for copper.

As we noted above, the country is one of the world's biggest copper producers - 10% of global output.

It's home to some of the world’s biggest copper mines, think the Cerro Verde mine, owned by $110BN capped Freeport McMoran.

SLM has held copper exploration ground in Peru ever since its IPO back in 2021.

Since then the company has been progressively adding to its landholding...

As we noted above, SLM now holds over ~43,500 hectares of ground, this is a big increase from the ~14,200 hectares held in December 2021.

Today, SLM locked in Land Access Agreements on one of its copper targets AND put out some rock chip sampling results.

As we mentioned before, SLM has rock chip sampling results with copper grades up to 7.14% at its Cinto project.

These are good grades for rock chip samples - and their proximity to a major copper project is a big bonus.

SLM is seeing and sampling copper in outcroppings - exposed rock - drilling will determine the amount of mineralisation beneath the surface.

But to drill, SLM needs drill permits, and some refined drill targets - which it is working on.

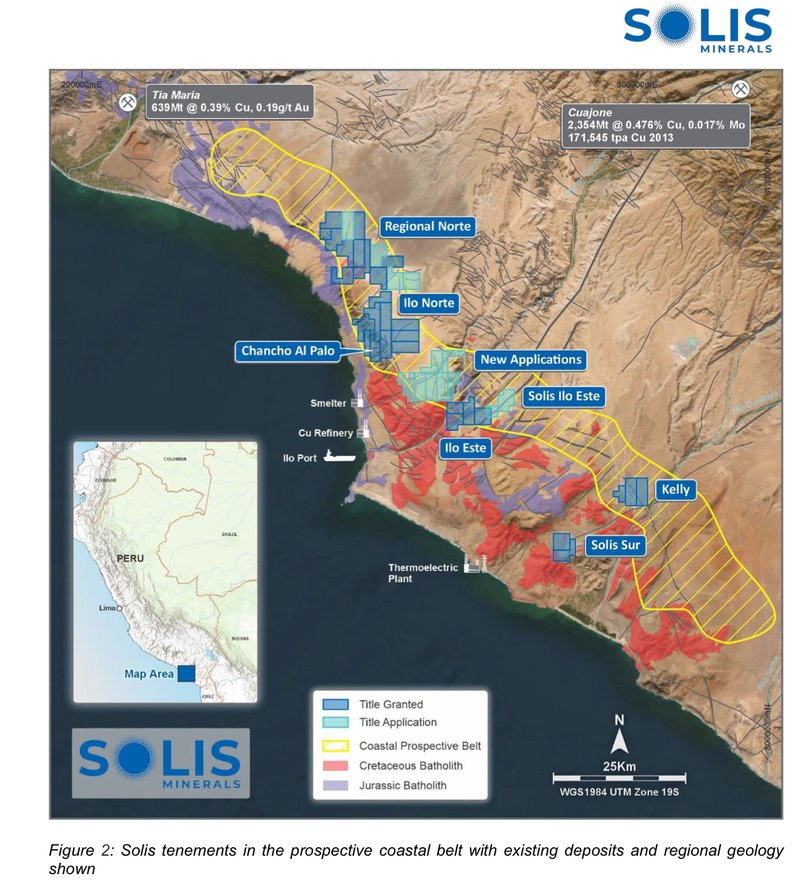

SLM’s Cinto project sits on similar geology to the Toquepala porphyry system.

The Toquepala porphyry system is roughly 15km away from SLM’s project and has a 3377M tonne resource. It’s a massive open pit mine that can be seen from space.

You can see how close it is to SLM’s project in the image here:

So far, SLM’s project hasn't had any geophysics done on it, which is what SLM will focus on next...

SLM’s plan is to first run some drone surveys and then follow it up with IP surveys over the ground.

The IP survey is where we hope to see some big colourful EM blobs around which SLM can plan drill programs.

At the same time SLM is working through drill permitting on its other copper targets in Peru.

SLM’s first drill program at one of its copper projects is targeted for “late 2024”.

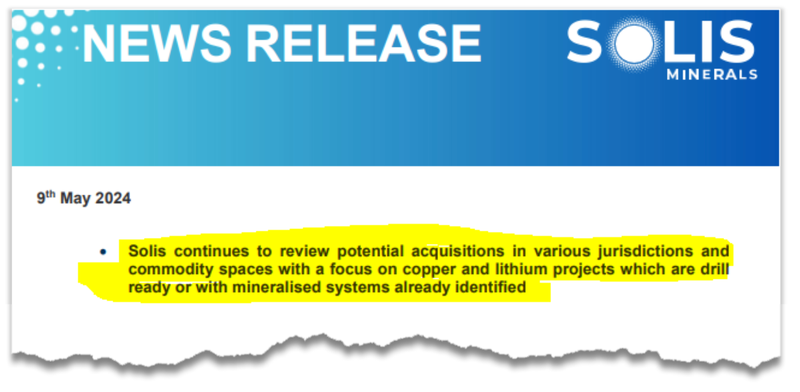

In the background, SLM is still looking at bringing new projects into its portfolio...

We actually caught up with SLM at the Brazilian Lithium Summit 2024 in Minas Gerais last month, so Brazil is clearly still a focus area for the company, given its close association to Latin Resources.

However judging by the above announcement wording, it also looks like SLM are open to deals anywhere.

See our write up on that conference here: Reporting from on site in Brazil...

At yesterday's close SLM traded with a market cap of ~$7.6M and had ~$5.6M cash in the bank at 31st of March, which translates to an Enterprise Value of circa $2M.

Given we are now in July, we would expect that cash balance to reduce somewhat after the June quarterly spend is released later this month.

Tax loss selling over for SLM?

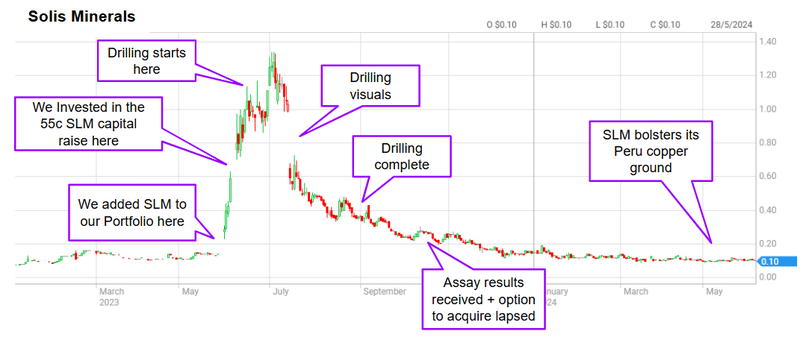

It's now been almost 12 months since SLM hit its share price highs of $1.34 per share.

That was in the first few weeks of July last year (the start of FY24).

Since then the company’s share price has come off a very long way after it opted NOT to proceed with its original Brazil lithium project.

Generally, when shares fall this much within a single financial year they become very susceptible to tax loss selling in June.

This is because almost all of the buying within the last twelve months would have been under water:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

New investors that entered high, who had held for most of the financial year would have been sitting on significant paper losses coming into June.

And the company’s chart seems to agree with what we think...

It's no surprise to us that SLM hit a 52-week low in the last few weeks of June - 7.6c...

However, when a stock is sold down so much during a tax loss season it can have the potential for a stronger bounce back in July, as all the tax loss sellers have left the building (with crystallised losses).

Here is what it looks like on the SLM chart:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The big question is - can SLM sustain this upward trend over the coming months in the lead up to drilling?

One positive move from SLM during that 2023 rally to $1.34 is that the company took the opportunity to raise $8.1M at 55c.

(we put $200k into that placement at 55c and haven't sold any of our shares - hopefully a big copper discovery will get us back above water on this - that’s the small cap exploration game).

The well timed raise means SLM still has $5.6M cash in the bank as of March 2024, while it looks for new assets & works up its Peru copper projects.

Below is a brief timeline of SLM’s share price since we first added the company to our Portfolio:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Catalysts we think could get the SLM share price moving again

Given SLM’s current modest Enterprise Value (EV), we think there are two key catalysts that could get the market interest in SLM again - and hopefully get its share price moving higher again.

- SLM finding copper drill targets in Peru

Once SLM runs geophysical surveys on the Cinto project (today’s announcement) we hope to see some giant colourful blobs (drill targets).

SLM is also working on drill permitting at two of its other copper projects in Peru (Ilo Este and Ilo Norte).

Those two projects have already had geophysical surveys done on them and are “drill ready”.

Those two sit next to an existing smelter, a copper refinery and two existing mines:

- SLM makes the most of the lithium bear market and picks up new lithium ground

We think it's a good time to have cash in the bank and to be on the lookout for new lithium assets.

The lithium market is a long way from its highs in 2020-2022.

The bigger companies are selling off and the ones with exploration ground are being sold off even harder...

The positive for a company looking at new acquisitions is that good projects can now be dealt at reasonable valuations.

Back between 2020-2022 we were seeing some super expensive deals done for very greenfield lithium ground.

Now with things changed and the markets not interested in early stage exploration ground we think the lithium market is very much a buyers market.

A good pick up in the bear market is what changed the fortunes of our other Brazilian lithium success story Latin Resources (ASX:LRS).

For context - LRS picked up its lithium ground during the 2018-2020 lithium bear market and then drilled and made a discovery in 2022.

LRS’s discovery took its share price from ~3c to a high of ~40c+.

Now its market cap is almost half a billion dollars.

SLM is backed by LRS and when we first Invested in the company we said we wanted to see the company go and become our LRS 2.0.

Given enough time, we are hoping SLM can pull it off.

Overall, we are hoping either of the two catalysts we listed above contribute to SLM achieving our Big Bet which is as follows:

Our SLM Big Bet

“SLM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - some of which we refer to in our SLM Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Our new SLM Investment Memo

Now that SLM has had a crack at two of its lithium assets in Brazil without making a discovery, the company is now focusing on its copper projects in Peru.

Given the change in focus, and in the lead up to copper drilling later this year, we think now is a good time to reset our Investment Memo.

Today we will be launching our new SLM investment Memo where you can find:

- What does SLM do?

- The macro theme for SLM

- Our SLM Big Bet

- What we want to see SLM achieve

- Why we are Invested in SLM

- The key risks to our Investment Thesis

- Our Investment Plan

What does this company do?

Solis Minerals (ASX:SLM) is an explorer, focused on making a new metals discovery.

As an early stage explorer, SLM could pivot in various directions towards different commodities, but for now, its current focus is on copper and lithium.

What is the macro theme?

Copper is already the third most widely used metal in the world - and with demand set to increase from things such as electric vehicles and semiconductor wiring — we see it as leverage to the global electrification boom and anticipated commodities supercycle over the coming decade.

Meanwhile, lithium is a critical mineral used in Electric Vehicle (EV) battery cathodes.

SLM will be looking to replicate some of the success of Brazilian lithium companies Sigma Lithium and Latin Resources and the Brazilian government is looking to grow its lithium production.

Our SLM Big Bet

“SLM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - some of which we refer to in our SLM Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why do we continue to hold SLM?

- Latin Resources success - We have had success Investing in Latin Resources which made a hard rock lithium discovery in Brazil and re-rated to a peak market cap of ~$1BN. Latin is now being called “Sigma 2.0” due to it following the nearby $1.8BN Brazilian lithium producer Sigma Lithium. In a similar way, we hope to see SLM become a “Latin 2.0”.

- Same team as Latin Resources (Latin 2.0?) - SLM is backed by the same team that delivered Latin Resources discovery last year. Latin’s Managing Director Chris Gale is SLM’s non-executive Chairman. Chris Gale has taken Latin from a ~$5M market cap multi-asset early stage explorer (similar to where SLM is now) to a peak market cap of almost $1BN off its lithium discovery in Brazil. Latin is now fully focused on bringing its Brazilian lithium discovery into production.

- Latin Resources is SLM’s biggest shareholder - Latin Resources holds ~15.3% of the company (as of 3 May 2024) which should mean they are incentivised to see SLM succeed. We hope that SLM can leverage its Latin Resources connection to deliver success in acquiring valuable projects in South America..

- Latin Resources has a big investor following - SLM should benefit from the crowd of investors that follow (and have made money from) Latin Resources (Latin Resources has ~12,900 shareholders).

- Copper price near all-time highs - Copper is trading at US$4.60/lb and could push higher as the electrification and decarbonisation macro themes get stronger.

- Lithium bear market could throw up opportunities - SLM has publicly stated it is looking at making new lithium acquisitions. With the current bear market in lithium stocks, SLM could find interesting exploration ground at a reasonable valuation.

- Tiny enterprise value (EV) means leverage to a discovery - At the time of this memo SLM has an EV of ~$2M, which we think means that the company is highly leveraged to a re-rate in the event of successful drilling results.

What do we expect the company to deliver?

Objective #1: Geophysical surveys across earlier stage copper projects in Peru

We want to see SLM rank more drill targets across its earlier stage copper assets in Peru.

Milestones:

🔲 Geophysical surveys commence

🔲 Geophysical survey results

🔲 NEW drill targets identified

Objective #2: Drilling at least one of its Peruvian copper assets

SLM has two drill ready copper projects and several earlier stage prospects in Peru. We want to see SLM drill at least one of those targets within the next 12 months.

Milestones:

🔲 Drill permitting

🔲 Drill rig contracted

🔲 Drilling commencement

🔲 Drilling results

Objective #3: Acquire a new exploration project

SLM announced on May 9, 2024, that the company “continues to review potential acquisitions in various jurisdictions and commodity spaces with a focus on copper and lithium projects”. We want to see SLM make at least one new acquisition within the next 12 months, to give it another chance of making a discovery.

Milestones:

🔲 New project acquisition #1

🔲 New project acquisition #2

What could go wrong?

- Exploration risk: SLM’s projects are all considered early stage prospects. This means SLM is yet to make a discovery on the projects. Inherently there is a risk that drilling programs return results with no mineralisation and the projects are not considered valuable.

- Commodity pricing: Copper is an industrial metal that is reliant on buoyant economic growth, if there is any significant decline in economic activity globally then copper prices are likely to de-rate.

- Jurisdiction risk/political risk: Despite its abundant resources and established mining industry, Peru has a reputation as having a more complicated permitting process than other countries in South America, despite efforts at reform. If SLM has delays in the drill permitting process this could impact the SLM share price negatively. Or alternatively, changes in the Peruvian political landscape could alter the attractiveness of Peru as a mining jurisdiction.

- Funding risk: SLM is a very early stage exploration company with zero revenue and is reliant on continuous capital raises (or attracting a farm in partner) so it can undertake high-risk / high reward exploration programs. There is a risk that market conditions deteriorate and investors shun high-risk explorers like SLM, and SLM is unable to raise capital without significant dilution of existing shareholders.

- Market risk: SLM is an early stage exploration company chasing new discoveries. There is always a risk that a market wide sell off will hurt SLM’s share price the most, given investors will look to withdraw capital from the high risk high reward investments in their portfolios first.

What is our Investment Plan?

Our updated Initial Entry price for SLM is 55c, so we need the company to deliver a decent discovery and deliver a 5x return from its share price at the time of this Investment Memo before we consider selling.

We have 1,750,000 unlisted 9c options in SLM too which we will exercise if the price runs back towards 50c on a discovery, which will help bring down our average entry price (these shares are escrowed until May 2025).

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.