Introducing our new Investment: Solis Minerals (ASX: SLM)

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 2,500,000 SLM shares. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time.

It’s been almost 12 months since we added a new Investment to the Next Investors Portfolio.

Our two best Investments across all our Portfolios in the last 3 years have been in lithium.

Today’s new Investment is exploring for lithium in Brazil, and is the same team that has delivered on one of our most successful lithium investments.

Our new Investment and first addition to the Next Investors Portfolio for 2023 is:

Solis Minerals

ASX:SLM 🇦🇺

(TSXV: SLMN 🇨🇦 OTCQB: SLMFF 🇺🇸 FSE: 08W 🇩🇪)

Our Initial Entry Price into SLM is 20c.

We will be holding 100% of our Initial Investment for the next two years.

Regular readers will remember our Investment in lithium company Vulcan Energy Resources in 2019. This Investment went from an Initial Entry Price of 20c to a high of ~$16, and is now hovering around the ~$3.70 mark.

We’ve had success in Brazilian lithium in the past, from our best performing Catalyst Hunter Portfolio company, Latin Resources.

We first Invested in Latin Resources in November 2020 at 1.8c, and then we Invested again at 3c.

After making a lithium discovery in Brazil, now Latin Resources trades at ~18.5c per share.

~10x from our Initial Entry Price.

We Invest for 1,000% gains like this. It doesn't happen often, and many Investments fail or move sideways - success in one company is no guarantee of success in another.

However on this occasion, our Investment in Latin Resources was a great example of everything coming together.

SLM has the Latin Resources team behind it.

SLM was IPO’d by the Latin Resources team, with the original assets from Latin Resources.

Latin Resources currently owns 14% of SLM shares.

After delivering a 10x return as MD of Latin Resources during a broadly bad market, SLM Chairman Chris Gale is somewhat of a small cap rockstar right now.

At Latin Resources, Chris Gale showed he can move a project along quickly and raise big amounts of capital to accelerate progress, and managed to pick the right jurisdiction in Brazil.

We want to see him apply his Latin Resources “Brazilian lithium formula” again on our new Investment SLM.

SLM Managing Director Matt Boyes also holds a country manager role at Latin Resources. He has also had previous success in early stage lithium - overseeing Red Dirt Mining as it grew from a $15M market cap to $200M.

We are hoping SLM can become a “Latin Resources 2.0”.

We have had success in the past backing previously successful teams into their new ventures, like the Vulcan Energy Resources spin out Kuniko.

When a management team has delivered success (like Latin Resources and Vulcan) we have observed that the new spinout company can leverage all the key learnings and networks that have been built in the sector, including potential partners, offtakers, financiers, investors and advisors.

However, we also need to be clear from the outset that the past performance of one company is not an indicator that another company will perform well. Early stage exploration stocks are risky investments and many things can and do go wrong, even with a previously successful management team.

We will cover some of the key near term risks we see later on in this note.

Today SLM added a new project to its Brazilian lithium portfolio.

SLM now has a 90 day option to acquire a “drill ready” hard rock lithium project on a mining lease in Brazil.

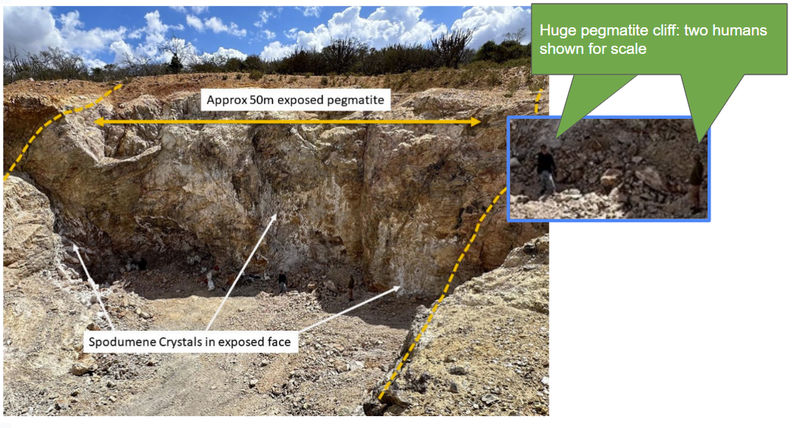

SLM’s project has rock chip samples grading up to 4.95% lithium, and a 50m exposed pegmatite cliff waiting to be drilled under.

The image below shows the 50m cliff of exposed pegmatites at the project.

If you look closely you can get an idea of the scale by spotting two people standing at the foot of the cliff.

SLM has said in today's announcement they plan to start drilling in June (in a few weeks). SLM has to move fast given the timeline for the option expiry isn't far away.

SLM is capped at $8.5M (at a 14c share price) and had $1.8M cash in the bank at 31 March 2023.

As always, early stage exploration investments like this are high risk. The company is in the ‘pre-discovery’ phase and not making any money - so it's reliant on capital markets to fund its exploration efforts, and there’s no guarantee it will make a large discovery.

With $1.8M in the bank at the end of March, we expect SLM is going to need to raise cash at some stage in the near term to fund drilling and the exercise of its option to acquire this new project, assuming the due diligence period is successful.

Today we will share a high level summary of why we Invested in SLM and also any potential near term risks. Once a drilling plan for the newly acquired project is revealed over the coming weeks, we will be sharing our Investment Memo for SLM.

Our SLM ‘Big Bet’

“SLM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - some of which we refer to earlier in today’s note. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

We look forward to following SLM’s journey over the next few years and sharing our opinions and commentary on SLM’s progress as long term Investors.

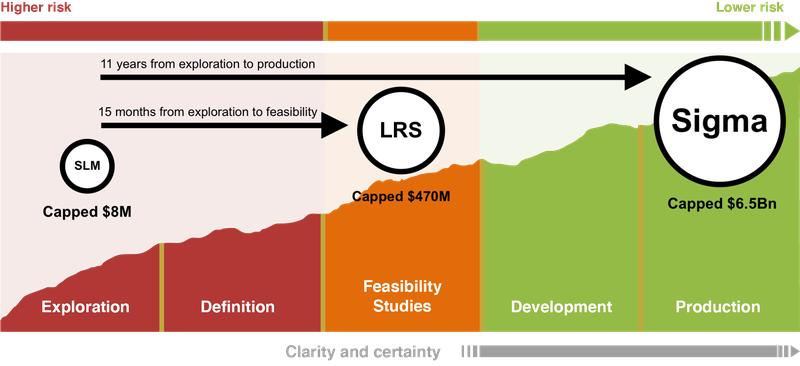

Brazil enters the lithium production game with Sigma. Latin next? ... then SLM?

Brazil is a mining powerhouse, and a stable mining jurisdiction to do business in. You might have heard about Brazil mining iron ore with Vale, which goes head to head with the Aussie iron ore miners.

As the battery metals theme continues to play out globally, we think Brazil is positioning itself to become a major player in the lithium sector - just like it has done in the iron ore space as the world’s second largest producer.

Brazil’s first ever large-scale lithium mine began production a few weeks ago.

The owner of that mine is the $6.5BN capped Sigma Lithium.

Once at full capacity, it will be operating one of the world’s biggest lithium mines.

The $470M capped Latin Resources is following in the footsteps of Sigma Lithium after its own lithium discovery and production ambitions.

Both Latin Resources and Sigma were in New York a few weeks ago ringing the bell at NASDAQ for the launch of Brazil’s “Lithium Valley” (more on that below):

The video above is from a great interview with the Sigma and Latin Resources leaders discussing the growth potential of the Brazilian lithium industry - great news for SLM Investors too.

The formation of Brazil’s “Lithium Valley” is a big sign of Brazil’s intent on attracting foreign investment capital into its lithium sector. The project aims to streamline investments in the lithium battery value chain, via collaboration with government and corporate partners.

In the last ~15 months Latin has managed to move from exploration, to definition, to feasibility studies stage 🎓 To learn more about the mining company lifecycle read: The mining company lifecycle explained.

The 11 reasons we are invested in SLM

We will share our SLM Investment Memo in the coming weeks that will include what we want to see SLM deliver over the coming period.

In the meantime here is a quick summary of the 11 reasons we Invested in SLM.

1. Lithium hot, lithium in Brazil even hotter

We have written excessively about the broader lithium market and the decade long investment thematic we are in.

Once it gets to full capacity, Sigma Lithium will be one of the world’s largest lithium producers.

Off the back of this, Brazil launched the “Lithium Valley” in the State of Minas Gerais with the ultimate view of promoting foreign investment in Brazilian lithium projects.

We think a tidal wave of capital is going to come into Brazilian lithium projects. SLM is an early stage Investment in this sector.

2. Junior explorers have had success in Brazil

Sigma has gone from a junior developer with a market cap of <$200M to now trade at $6.5BN. Latin Resources has also gone from <$40M to now trade at $470M. Exploration success in Brazil is typically rewarded with a re-rate in a company’s market cap.

3. Latin Resources success

We have had success Investing in our other Portfolio Company Latin Resources which made a hard rock lithium discovery in March 2022 and has since gone from a share price of ~3.5c to 18.5c per share. Latin is now being called “Sigma 2.0”.

In a similar way, we hope to see SLM become a “Latin 2.0” (while remembering that just because Latin performed well doesn’t mean that SLM will do the same).

4. Same team as Latin Resources (Latin 2.0?)

SLM is backed by the same team that delivered Latin Resources discovery last year.

Latin’s Managing Director Chris Gale is SLM’s non-executive Chairman.

Chris Gale has taken Latin Resources from pre-discovery to a maiden JORC resource in <12 months and managed to raise $72M along the way.

SLM Managing Director Matt Boyes also holds a country manager role at Latin Resources. He has also had previous success in early stage lithium - overseeing Red Dirt Mining as it grew from a $15M market cap to $200M.

5. Backed by Latin Resources (14% shareholder)

Latin Resources hold 14% of SLM shares - which means they are incentivised to see SLM succeed. We hope that SLM can leverage its Latin Resources connection to deliver success in Brazil for itself.

6. Original asset spinout from a well supported, successful bigger company

The SLM to Latin Resources structure has some similarities to how Kuniko was spun out of Vulcan Energy Resources. KNI had an outrageous run from 20c to touch $3.60 in the peak of the bull market, and has now settled at 40c.

We like to back a successful management team in sectors with strong momentum. We certainly aren’t expecting anything like this again, but note that the management team does play a role in the market's interest in a company.

We also have a view that a lot of the interest in Kuniko initially came from investors that had success with Vulcan, wanting to follow the Vulcan team’s new venture.

7. SLM Managing Director built a $200m+ lithium company before

SLM’s MD Matthew Boyes has been there and done it before.

Boyes was the Managing Director at Red Dirt Metals where he oversaw early development of the Mt Ida lithium project - which took Red Dirt’s market cap from ~$15M to in excess of $200M.

If he can elevate SLM to a similar market cap over the next two years we will consider that a very successful result.

8. Low EV and tight capital structure

SLM has only ~60.5 million shares on issue and traded with a market cap of $8.5M at last close. SLM had $1.8M in cash at 31 March 2023, which equates to a tiny Enterprise Value (EV) of $6.7M.

SLM has plenty of room to re-rate if it makes a successful discovery. We note there are ~27 million options on issue too, with the majority having an exercise price of 30c.

9. Latin Resources has a big investor following

SLM should benefit from the crowd of investors that follow (and have made money from) Latin Resources (Latin Resources has ~12,300 shareholders).

SLM is following a similar style exploration process and so investors who have had success with Latin Resources may look to buy into SLM with the hope SLM becomes “Latin 2.0”.

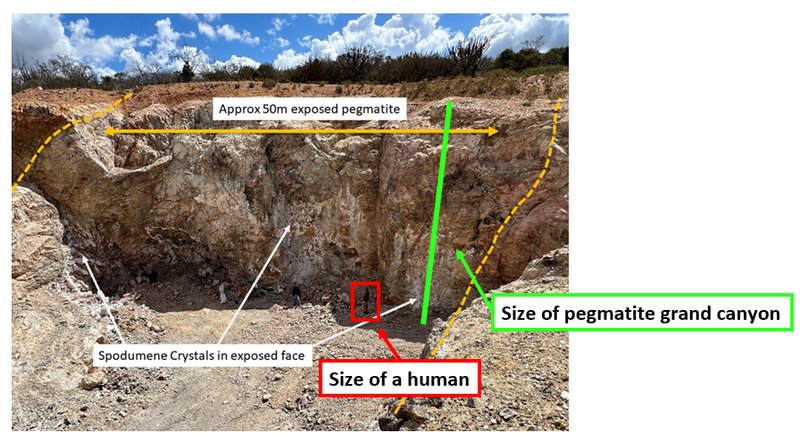

10. SLM about to drill what we are calling ‘Pegmatite Grand Canyon’

In the photo below you can see the exposed spodumene crystals on SLM’s project.

SLM is going to drill test this area and see what kind of high grade intersections it can deliver.

Drilling is in June so we don’t have to wait long for a result here.

11. SLM is already listed in the US, Canada and Germany

“SLM” is the ASX stock code and the primary listing, but we also note that SLM is also already listed on the following other global small cap exchanges: TSXV: SLMN 🇨🇦 OTCQB: SLMFF 🇺🇸 FSE: 08W 🇩🇪.

This means that the potential investor pool that can invest in SLM is not just limited to Australian investors, but also much larger pools of investors in the USA, Canada and Germany.

Many companies will look to do an overseas listing as their project progresses, but we like that SLM has covered all the major small cap exchanges BEFORE they start delivering on their Brazil project.

The short term risks

First ever drilling in a few weeks

SLM will be running the first ever drill campaign on the new project next month. It is possible that the company finds less than what the market is hoping for OR worst case the project is deemed not worth acquiring.

Due diligence period of 90 days

SLM still needs to run the due diligence process. It is possible that the acquisition does not get completed for whatever reason.

Funding risk

SLM will need up to US$1M to complete the acquisition of the new project and likely more funds to run its drill campaign.

With ~$1.8M in cash at 31 March 2023 the company may be cutting it close for funding and may need to raise some capital in the near term.

As is typical with companies when the market is anticipating a near term capital raise, this could weigh on the company’s share price in the near term.

Solis Minerals

ASX:SLM 🇦🇺

(TSXV: SLMN 🇨🇦 OTCQB: SLMFF 🇺🇸 FSE: 08W 🇩🇪)

Latin Resources: Stroll down memory lane

Long time subscribers to our Catalyst Hunter portfolio might be aware that we Invested in Latin Resources before the company went on to make its lithium discovery in Brazil last year.

We watched as our Investment gathered some high grade rock chips, mapped its pegmatites and then drilled its first discovery hole of 4.31m with 2.22% lithium grades.

Within months of the discovery Latin’s share price went from ~3.5c to ~20.5c per share.

Off the back of the discovery the company raised over $70M in capital (first, $35M at 16c in 2022 and then another $37M at 10.5c in 2023).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Latin Resources is now being labelled “Sigma 2.0” - a reference to Latin’s $6.5BN neighbour which set the precedent for a successful lithium company in Brazil.

Just like Latin, only a few years ago Sigma was a fledgling junior explorer on the TSX-V.

Now the NASDAQ listed Sigma Lithium has entered production and opened the floodgates to capital seeking exposure to the Brazilian lithium industry.

Such is the interest in Brazilian lithium projects, Rio Tinto has even been pegging ground around Latin Resources...

Why does this matter for Solis Minerals (ASX:SLM)?

Latin ended up being a great Investment for us - the company has now gone onto become a beast of its own - capped at $470M.

We think our Investment edge is backing junior company’s capped at less than $100M, that we think can eventually become the next Latin Resources or (even better) the next Sigma.

We also like to back teams that have delivered for us in the past.

Latin’s 14% shareholding in SLM and the company’s specific focus on Brazilian lithium projects, combined with its low market cap and tight capital structure, mean SLM fits into the specific criteria we look for when searching for these companies.

Just like Latin did, we are Invested in SLM to see it take its early stage lithium prospect and make a potentially economic discovery.

SLM drilling next month - what's below the 50m wide pegmatite outcrop?

SLM’s new project is a “drill ready” lithium prospect - this means all of the pre-drilling qualification work has already been done, and investors don't have to wait months before drilling begins.

The project has already been mapped and sampled - the only thing left is to drill test it, looking for high grade lithium mineralisation.

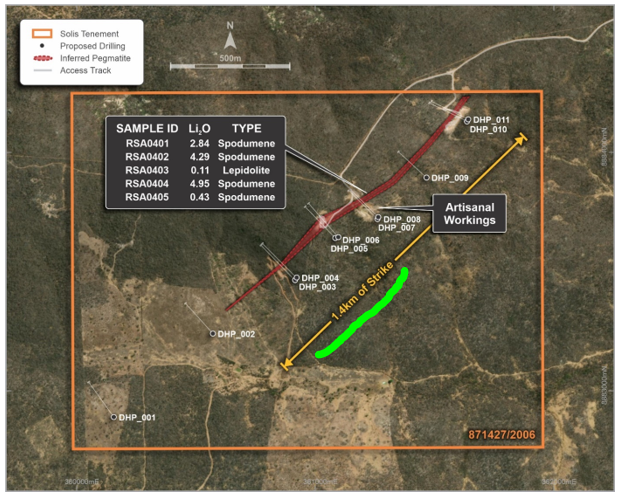

SLM’s outcropping pegmatite measures ~50m in width and is mapped along a ~1km long strike length.

If you squint really hard at the photo below, you can just make out a tiny figure in the middle - that's a geologist, standing there for scale.

Here you can see the rock chip sample locations on a map, along with artisanal workings, and proposed drill hole locations:

For context, SLM’s Brazilian peer Sigma Lithium’s Xuxa deposit initially sat on a strike of ~1.7km with a thickness of ~12-13m.

That deposit had a ~21mt lithium resource - we are hoping that in time, SLM can one day define a resource similar in size.

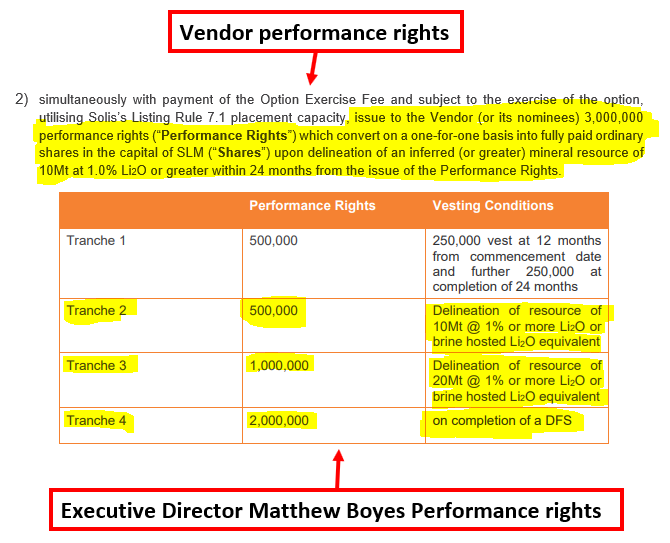

Interestingly, all of the performance shares associated with SLM’s deal (and MD Matt Boyes’ performance shares) are also structured to reward a 10mt+ lithium resource.

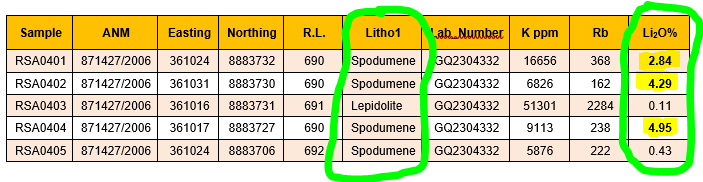

Of the 5 rock chip samples taken from SLM’s project, the peak lithium grade was 4.95%.

Four of the five samples also confirmed the presence of spodumene - spodumene is critical because it is typically the host rock for lithium.

Most of the world's lithium is produced from spodumene hosted lithium projects - so if you are assessing a lithium project, you want to see evidence of spodumene.

🎓 To learn more about the different types of lithium projects and the benefits of a spodumene hosted lithium project check out our educational article here: The different types of lithium projects explained.

Here’s a photo of SLM’s large white weathered spodumene crystals within artisanal workings.

And a pick for scale... again, you might have to look closely around the bright white spodumene crystals.

Now, the company is ready for its planned maiden drilling program which it expects to commence next month.

SLM will be following the same tried and tested playbook that has led to the discoveries of some of the world's biggest lithium deposits that have delivered billions of dollars in value.

The early stage lithium exploration process playbook goes like this:

- Map outcropping pegmatites - SLM has already mapped its outcropping pegmatite over a ~1km strike with widths in excess of 50m. ✅

- Sample the outcrop to see if there is lithium - SLM has taken ~5 rock chip samples returning a peak lithium grade of ~4.95%. ✅

- Confirm the presence of spodumene - spodumene is the source rock for the majority of the world’s lithium supply. SLM has confirmed mineralised spodumene structures. ✅

- Drill below the outcrop to see how much high grade lithium is there - SLM already has a drill rig and is preparing to drill in June 2023. 🔃

For Latin Resources it was the maiden drill program and subsequent development that took the company to a market cap of ~$470M.

We are hoping $8.5M capped SLM can deliver something similar with its first drilling campaign next month - noting of course this is high risk, early stage exploration, things can and will go wrong. Past performance of another company is no guarantee of performance in another company, especially in exploration.

Again, here is a quick reminder of the potential risks:

First ever drilling in a few weeks - SLM will be running the first ever drill campaign on the project next month. It is possible that the company finds less than what the market is hoping for OR worst case the project is deemed not worth acquiring.

Due diligence period of 90 days - SLM still needs to run the due diligence process. It is possible that the acquisition does not get completed for whatever reason.

Funding risk - SLM will need up to US$1M to complete the acquisition of the new project and likely more funds to run its drill campaign.

With ~$1.8M in cash at 31 March 2023 the company may be cutting it close for funding and may need to raise some capital in the near term.

As is typical with companies when the market is anticipating a near term capital raise, this could weigh on the company’s share price in the near term.

What will SLM be paying for the new project?

A breakdown of the payment structure for SLM to acquire the project looks like this:

- Upfront payment of US$100k.

- US$700k after the acquisition is completed.

- 3 million performance rights which would convert into SLM shares if a lithium resource of 10mt with a 1% lithium grade or larger is defined within 24 months.

- US$2.9M cash in 12 months time.

Our take on the deal

We especially like that SLM has given itself 90 days to run due diligence.

With a drill rig already secured and drilling set for June, the company will know relatively quickly whether it is onto a new discovery or not.

This COULD mean the company has the option to walk away from the project should nothing be found.

Alternatively the company’s initial outlay for the project will only be US$800K.

The rest of the consideration comes due in 12+ months time or if the company defines a 10mt + lithium resource.

IF SLM does manage to define a resource this large we would hope SLM’s market cap is multiples of where it is now and the company has no issues raising capital to pay the vendors, especially with chairman Chris Gale’s contact list of Latin Resources investors that have had wins backing him before.

Our SLM Investment Memo - coming soon...

In the lead up to the drill program in June and once a drilling plan is released by SLM, we will be looking to launch our SLM Investment Memo.

In our Memo we will detail:

- Why we Invested in SLM

- Our long term bet - what we think the upside Investment case for SLM is.

- The key objectives we want to see SLM achieve over the next 12 months

- The key risks to our Investment thesis

- Our Investment Plan

Be on the lookout for this over the coming weeks.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.