SLM: Micro cap copper explorer about to drill… AusQuest up 700% on copper hit.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 363,637 SLM shares and 1,750,000 SLM Options at the time of publishing this article. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time.

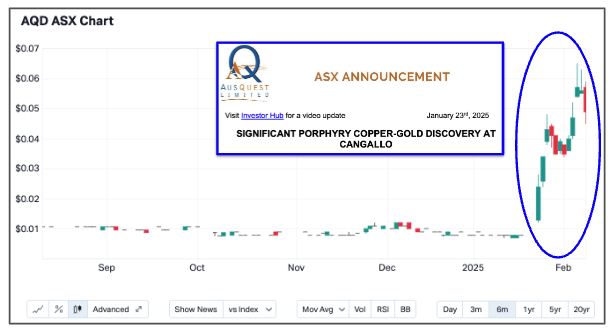

Two weeks ago a micro cap ASX stock made a copper discovery in Peru that delivered a ~700% return.

Our very own micro cap copper explorer Solis Minerals (ASX:SLM) is aiming to drill for a discovery in Peru this quarter.

Same country, similar geology, targeting the same metal, valued at a similar level pre drill...

SLM’s Peruvian copper exploration peer is a company called AusQuest.

Two weeks ago, it was a tiny micro cap stock just like SLM...

... until it drilled and made a "porphyry copper-gold discovery” in Peru.

Copper porphyries are big, shallow deposits that can be highly valuable due to the sheer amount of metals they can contain - the type of deposits that are really attractive to the +$100BN mining majors in this part of the world.

Just like SLM is now, Ausquest went into drilling with a tiny market cap - Ausquest’s was ~$6M at an ~.7c share price.

At its peak only a few days ago AusQuest’s market cap hit ~$78M at ~6.5c.

That’s a >700% return in only a few weeks - the kind of ‘high risk, high reward’ return that attracts investors to ASX micro cap explorers.

Of course - the past performance is not a guarantee of success - for every Ausquest there are dozens of other stocks that drill unsuccessfully despite doing all the pre-drill preparation work they can to ensure the best possible chance of success.

Here is what happened to AusQuest post discovery...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

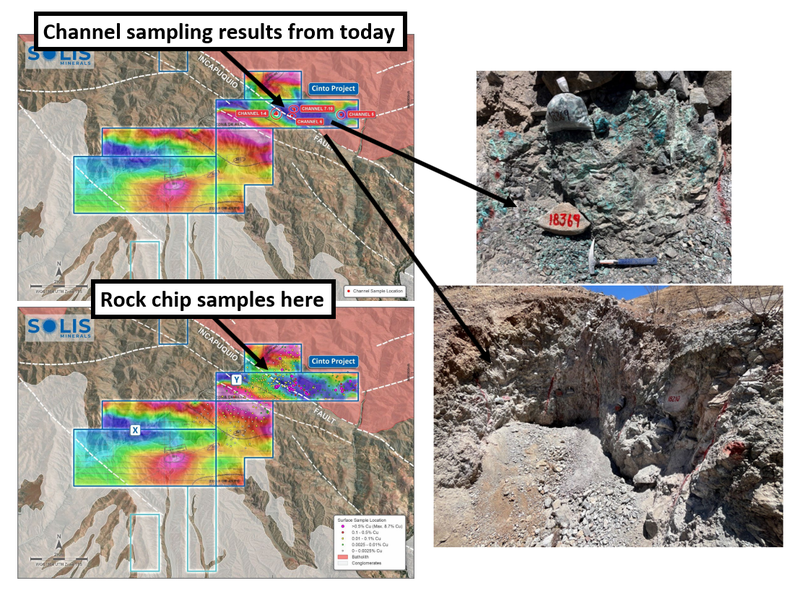

SLM has been doing all the right pre-drill work, adding to that today with news that channel samples and rock chips have demonstrated it has “extensive copper porphyry mineralisation” at its project in Peru.

That's an excellent sign ahead of drilling.

SLM is capped at just $5.5M and has plans to drill two different targets this quarter, and a total of 4 by the end of this year.

Across all four projects, SLM is going for similar discoveries to the one made by AusQuest.

Here is where SLM’s copper projects sit relative to Ausquest (AQD)’s copper discovery:

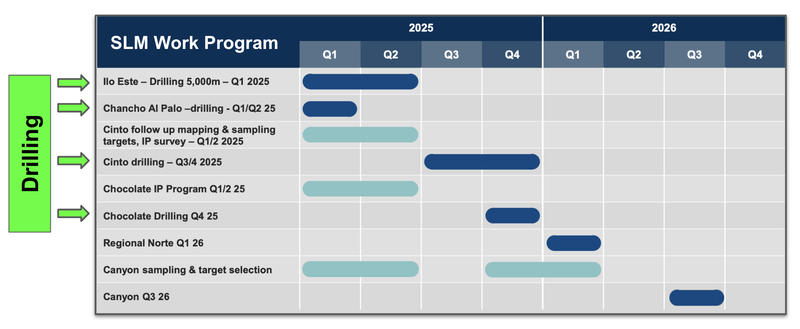

Two of SLM’s four targets are drill ready (Ilo Esto and Chancho Al Palo) - one of the major final hurdles to drilling is drill permits.

SLM expects to be drilling both of those this quarter - i.e. before the end of next month.

SLM held $1.58M in cash at November 30th, so may need to raise additional capital to fund drilling and working capital ahead of the main drilling events.

SLM currently has a market cap of ~$5M which is a level where we think there is plenty of upside to re-rate higher off the back of any good exploration news, given the size of the potential prize.

When it comes to the pre-discovery exploration space we like to Invest in companies where the risks and rewards are high in the hope that they make a discovery.

We tend to have a small portion of our Portfolio Invested in these types of stocks so that if the drilling is unsuccessful it doesn't hurt our Portfolio too much.

BUT if the drilling comes in then it's still a meaningful win for the Portfolio overall.

Next - we want to see SLM get its drill permits and kick off drilling.

Confirmed porphyry gold-copper at one SLM’s four targets

As we mentioned earlier, it was a copper-gold porphyry that re-rated AusQuest by over 700%.

Today, SLM confirmed copper-gold porphyry mineralisation at its Cinto prospect after a channel sampling program (trenching).

Cinto is the target SLM is planning to drill in Q3 of this year.

SLM returned 23.4m at 0.88% copper and 16.83m at 0.52% copper from two different parts of the project in channel sampling.

Importantly, the channel sampling seems to line up with the parts of the project where SLM has previously picked up rock chips with copper grades of ~7.14%.

We are looking forward to seeing SLM drill out that north/eastern part of its project.

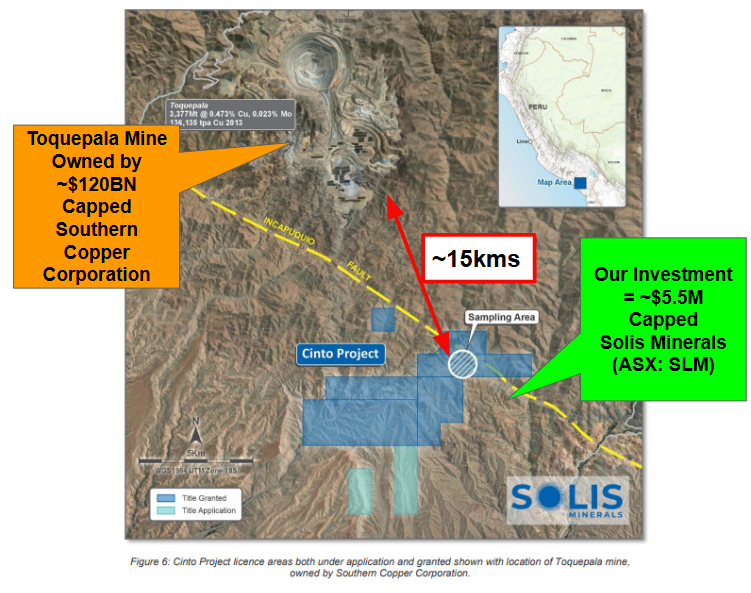

We are especially looking forward to the drilling at Cinto because of its location.

Cinto sits just 10km away from the massive Toquepala mine owned by ~$120BN Southern Copper Corporation.

Southern Copper Corporation is one of the top 10 copper producing companies in the world. (Source)

That mine produces around 180,000 tonnes of copper each year, and has been in operation since 1964:

(Source)

Being so close to an existing mine will mean that any discovery could be a lot more valuable than if it were to be made in an isolated area.

We think South Copper Corporation would surely start to get interested in whatever SLM finds if a discovery is made and the proximity to all of the processing/mine infrastructure could make it a nice way of extending the life of mine for its project.

Giant porphyry discoveries usually end up in the hands of companies with market caps in the hundreds of billions anyway, so any interest from Southern Copper Corporation wouldn’t be a complete surprise to us.

(Of course none of this matters unless SLM can make a discovery...)

We have seen deep pocketed partners get interested in copper porphyry stocks in our Portfolio before - with another South American resources company Titan Minerals (ASX: TTM).

Titan’s copper porphyry project attracted interest from a subsidiary of Gina Rinehart’s Hancock Prospecting - the two signed a US$120M farm-in deal.

So we have seen it happen before, from a porphyry discovery to a farm-in deal from a major mining company.

The challenge with porphyry discoveries is that they can take a lot of capital and a longer period of time to define - which is why the bigger companies tend to invest in them.

BUT the rewards can be great for small cap exploration companies because they can be very attractive to the mining majors.

(like for example, SLM’s neighbour, the $120BN capped Southern Cross Copper)

After AusQuest’s recent sharp share price rise we think that there will be more interest in the region, and in SLM’s upcoming drilling campaigns.

And we think that any copper discovery by SLM could be transformative for the company.

But SLM has to drill the project first.

Copper IS the one thing that all of the big players are looking for.

But they are generally happy to let the small cap companies do the target generation work, permitting and early greenfields exploration before swooping in and drilling it out.

With four promising projects, SLM will be drilling four different projects - giving it plenty of opportunities to replicate the success of AusQuest.

Or potentially, even improve on it...

Here’s more on SLM’s four projects.

SLM’s four “shots on goal” for 2025.

SLM has four different projects, with different styles of targets that it plans to drill all before the end of 2025.

Here is our rapid fire take on all of those targets:

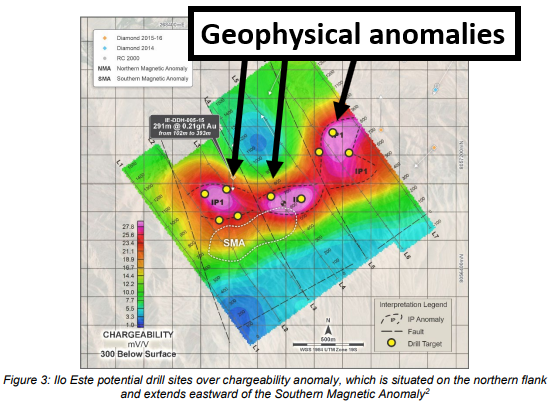

Project 1: Ilo Este

Stage: Drill Ready

Why it is interesting: Nice juicy target ready to drill for copper & gold. SLM has plenty of geophysical anomalies firmed up and previous drilling around the project has shown there is gold mineralisation...

What’s next: Drill Permit

When does SLM expect to drill: Q1 2025

The Ilo Este project has multiple drill targets ready to be tested.

SLM will look to do a 5,000m drilling program over the project in the first quarter of 2025.

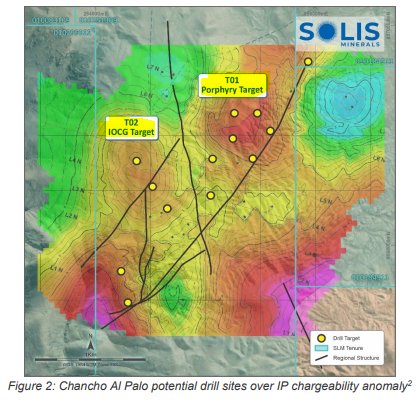

Project 2: Chancho Al Palo

Stage: Drill Ready

Why it is interesting: Here SLM has several geophysical anomalies it can drill. The difference with this project is that SLM will be drilling for two different styles of mineralisation. IOCG (Iron oxide copper gold) style mineralisation in the west and porphyry potential to the east.

What is next: Drill Permitting

When does SLM expect to drill: Q1 2025

Project 3: Cinto Project

This was the project that SLM published news about today.

Stage: Permitting / Target Generation

Why it is interesting: It is just 10km away from the Toquepala mine that produces 180,000 tonnes of copper each year. Importantly, channel and rock chip sampling results seem to line up in the North Eastern part of SLM’s project...

News Today: SLM published results from a channel sampling program that highlighted the potential for a porphyry system

What is next: IP survey this quarter & drill permitting

When does SLM expect to drill: Q3/4 2025

Project 4: Chocolate (previously Guaneros)

Stage: Drill Ready

Why it is interesting: This one is the target SLM plans to drill last. The Chocolate project sits between SLM’s two other main projects Chancho Al Palo and Ilo Este which explains the timing preference. IF SLM has success at those prospects, then drilling Chocolate would probably become more of a priority for the company.

When does SLM expect to drill: Q4 2025

What’s Next for SLM?

🔄 Additional exploration work to firm up drill targets

SLM plans to conduct further induced polarization (IP) surveys at Cinto to refine drill targets, with a first-pass drill program anticipated for 2025.

It will then start drilling across the four projects during 2025, noting that the order of the projects drilled could change depending on which projects have the best targets following this exploration work.

Previously, SLM released an outline of completed works at SLM’s copper projects in Peru with a timeline for drilling at each project on the right:

What are the risks?

The three main risks we are most conscious of for SLM right now are funding risk, exploration risk and permitting risk.

The first and most important risk is funding risk.

SLM had $1.58M in the bank at the end of November which we don't consider is enough to drill all four of its targets this year, especially given working capital needs.

As a result we expect to see SLM go to the market to raise some cash to fund drilling programs at some point.

With SLM planning 2x 5,000m drill programs inside this current quarter, the capital raise may need to happen before OR just after drilling starts this quarter.

Funding risk

SLM is a very early stage exploration company with zero revenue and is reliant on capital raises (or attracting a farm in partner) so it can undertake high-risk / high reward exploration programs. There is a risk that market conditions deteriorate and investors shun high-risk explorers like SLM, and SLM is unable to raise capital without significant dilution of existing shareholders.

Source: 9 July 2024 SLM Investment Memo

Second is permit delay risk.

SLM is waiting on a number of key permits to drill out its project.

Any delays to these permits and the expectations that SLM has set for when to expect them, may negatively impact the company’s share price.

Finally, exploration risk.

This risk will become more apparent as SLM starts to drill out its project.

Drilling may not deliver mineralisation, or any mineralisation found may not be economic.

Exploration risk

SLM’s projects are all considered early stage prospects. This means SLM is yet to make a discovery on the projects. Inherently there is a risk that drilling programs return results with no mineralisation and the projects are not considered valuable.

Source: 9 July 2024 SLM Investment Memo

Our SLM Investment Memo

In our SLM Investment Memo, you can find the following:

- What does SLM do?

- The macro theme for SLM

- Our SLM Big Bet

- What we want to see SLM achieve

- Why we are Invested in SLM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.