Shifting Geopolitics and the Future of Critical Metals

Published 14-SEP-2024 14:54 P.M.

|

17 minute read

- Commentary: Global tensions usher in more “weaponised” export bans. The highs and lows of mining - lithium bottom in? Big night for precious metals - Gold hits all time highs... silver price surges overnight.

- Quick Takes: PFE, NTI, EIQ, SS1, GTR

- This week in our Portfolios: SS1, EXR, AL3, EIQ

Gold and silver both surged overnight.

A sign of rising global tension?

This week we saw even more new threats of export restrictions on critical metals.

Russia is now threatening to restrict uranium exports.

...messing with energy supply again, after they drastically reduced gas supplies to put pressure on Europe in 2022.

Lithium is a critical metal in achieving energy independence from fossil fuels.

And lithium stocks popped up this week on a potential lithium comeback as two “high cost” lithium mines in China were rumoured to be shutting down.

It’s all about energy independence...

Back in 2022 we set out our prediction for how energy and critical material supply may be weaponized as global tensions escalate.

(and we had positioned our Portfolio accordingly)

Around that time the Ukraine war set off a chain reaction of geopolitical events centred around energy.

Guess what also happened in 2022?

This is roughly when the small cap bear market kicked in.

Meaning that small cap critical metals companies share prices came down.

And they struggled to raise capital to develop their projects.

We had positioned our Portfolio around that time to benefit from growing geopolitical friction feeding into rising commodity prices.

It’s been a painful time for critical metals stocks.

But with a rise in critical metal export bans we’re increasingly getting the feeling that the next leg up of the long mooted critical minerals boom is getting closer by the day.

Every new export restriction we hear about is another step closer to urgency in funding new supply.

Right now, governments just can’t seem to stop messing with each other using critical metals supply as leverage.

If anything, it's getting more aggressive.

At some point, the “worm must turn” and new critical metals supply must be developed.

And the capital markets will have a major role to play.

i.e BOTH governments and markets must actually get serious about securing supply of critical minerals.

Securing supply chains requires not just government support, but the market to start re-allocating capital to putting projects into production.

Right now, there seems to be a bit of a disconnect between certain critical mineral prices, government manoeuvres and stock prices.

Here’s an example.

The uranium spot price is still trading at a circa 14 year high around US$80/lb.

We know the US has had virtually no domestic uranium production for a decade.

We’ve recently seen the US ban Russian uranium imports.

And yet, small uranium stocks are yet to get market attention.

Maybe that’s about to change.

The latest news this week in the uranium market is this:

(Source)

Surely, at some point soon the triad of prices, government restrictions and stock prices needs to align to incentivise increased exploration for and production of critical minerals like uranium.

Also on the agenda in Russia are restrictions on titanium and nickel.

Titanium is used in tanks and other military hardware.

And last we checked, the EU still gets ~16% of its nickel from Russia. (Source)

Point is...

We’ve seen commodities “weaponised” before - traditionally they are tied to the production (oil, gas, uranium) or discharge of energy (battery materials).

But increasingly now, also military supply chains.

Is this the last domino to fall, triggering a new and concerted push to secure critical minerals?

China’s new restrictions on antimony exports kicked in yesterday.

Antimony is a key material in munitions (bullets) as well as a range of other high tech military applications.

Speaking of China...

Rumours of the closure of two “high cost” Chinese lepidolite lithium mines sparked big rallies in the big ASX lithium stocks:

All of these headlines were a prelude to another geopolitical power play from China:

(Source)

The EU has been pushing for major tariffs on Chinese EVs - so it looks like there is a big EV fight brewing.

But let’s zoom out a bit here and once more cast our minds BACK to 2022...

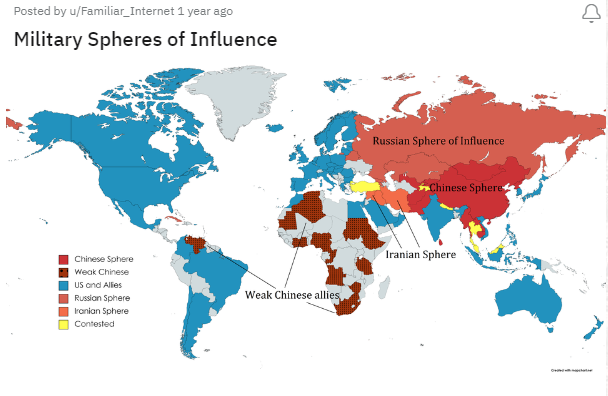

In October 2022 we put forward a map showing how the energy and critical metals supply “battle lines” may be drawn.

The map below shows a rough approximation of the USA-led world order in blue, and the “challengers” in red.

Grey are neutral countries that can swing either way:

(Source)

We said:

A key strategy of the West to defend their “achilles heel” of dependence on oil & gas is to switch to electric vehicles and renewable energy.

It’s Team Red vs Team Blue in the ultimate showdown for energy independence...

“Now that tensions between the red gang and blue gang are escalating, and access to critical resources is being rolled out as a strategic weapon to attack energy independence, we look at a very basic equation to work out where to Invest:

“If you are a blue country and any of your critical resources come from a red country, you need to find and replace that with supply from a blue country.”

Otherwise, increasingly hostile red countries will use your dependence on them against you.”

Those tensions have been escalating over the last few weeks...

Again, it’s all about energy.

And it was oil that originally got us thinking about this emerging “Red vs Blue” battle way back in October 2022.

Read the full article here:

(Source)

Lithium comeback?

The mining industry is often referred to as “cyclical”...

And rightly so... we think the mining industry is structurally at the mercy of supply/demand curves in the long run.

When demand is high and supply is low - commodity prices eventually rally.

When demand is lower than supply - prices tank.

For mature markets like copper, iron ore and oil & gas, the supply/demand curve has been delicately built out over decades (in some cases even longer) making them less vulnerable to major price swings.

Supply is fairly resilient - in the mature markets producers and downstream operators are fairly diversified from a geographic point of view.

On the demand side - fluctuations are minor and easier to predict/react to.

A good example is oil.

No single country produces more than 20% of the world’s oil supply and there is an organisation called OPEC which responds to periods of low demand by cutting supply to keep prices in check.

The lithium market is nothing like these mature markets...

The lithium market is still in its infancy.

Which means the supply/demand curve hasn’t been built out just yet.

Demand is still growing extremely fast.

And supply comes online (and offline) in chaotic waves from knee jerk responses to high/low lithium prices.

In early stage markets like this prices can quickly go parabolic as the market sends a signal to the mining industry that more supply is needed ASAP.

That’s what we saw in 2017-18 and then again in 2021-2022.

In 2017-18 we saw the old tantalum mines that were producing lithium as a by-product crank up lithium production.

Think Pilbara’s project and Greenbushes in WA.

Then during the 2021-2022 bull run we saw new greenfields discoveries get to market (Mt Catlin, Liontown’s project, Sigma’s project in Brazil).

We also saw a new set of producers emerge with different cost profiles...

Lower along the cost curve we saw brine operations get ramped up and put into development.

Higher along the cost curve we saw lepidolite mines get switched on. Lepidolite is often lower grade and harder to process so it became what the industry referred to as “the marginal supply” in the lithium market.

With lithium prices well above even the highest cost producers breakeven prices all of this supply was rushed into the market and created a situation where supply is higher than demand.

For the past ~6-9 months we have been watching the higher marginal cost producers shut up operations and put their mines into care and maintenance.

- NT lithium producer Core Lithium switched its mine off earlier this year

- World’s third biggest lithium company Arcadium Lithium said it would phase down its Mt Cattlin mine in WA

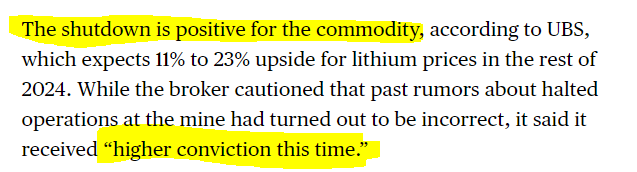

And then this week we saw rumours of CATL (Chinese EV battery maker) switching its mines offline in China.

Those are the lepidolite mines we talked about earlier, the high cost marginal supply.

Investment Bank UBS also came out with a pretty bullish take on the lithium market going forward...

Mining is cyclical and when you take a step back from the day to day noise of the industry it really is just an endless cycle of highs and lows as supply comes on/offline and demand increases/decreases.

Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

No one knows when a rebound may happen - it could take a few more months/years for excess inventories to be spent and for the impacts of mine closures to feed into lithium prices (look at that 2019-2021 period).

OR with demand increasing a lot faster nowadays (relative to the last cycle) prices could bounce back a lot sooner than anyone expects it to.

Our experience watching these cycles for decades across different markets is that the equities tend to put in their bottom’s well before the underlying commodity does.

And oftentimes, they are rallying pretty hard before the next cycle is fully in gear.

The lesson to be learned - it's impossible to time it to perfection, but more about picking companies that will be able to make the most of the next cycle when it does come around.

We have averaged down (Invested more at a lower share price) into most of our lithium Investments and added a new one to the Portfolio:

- Mandrake Resources (ASX:MAN) at 3.3c

- Pantera Minerals (ASX:PFE) at 5c

- Pursuit Minerals (ASX:PUR) at 0.35c

- Lightning Minerals (ASX:L1M) - new Portfolio addition at 7c - lithium exploration while lithium is hated...

Now we just wait for the lithium bounce back...

Speaking of a commodity where we think supply/demand could create a bull run - Silver...

The silver price has surged over 10% this week.

Most of that run over the last two days.

From a technical perspective the chart is looking pretty solid.

Silver tends to lag gold and with gold trading at all time highs we think silver could be about to breakout into its own rally.

Gold continues to hit new all time highs:

The long term silver chart is looking very good:

Our thesis isn't just based on short term price predictions.

For a long time we believed the price of silver had traded at unsustainable lows.

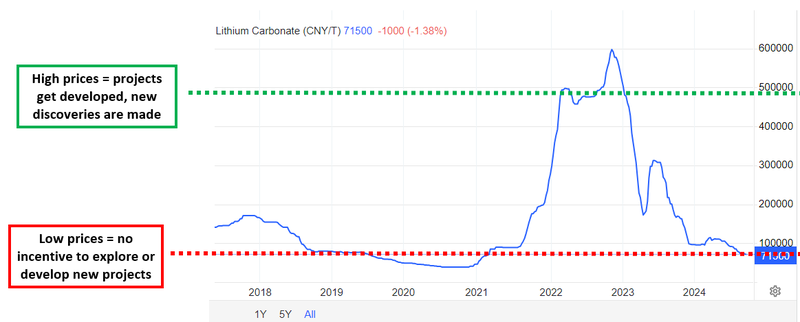

Just as we talked about with lithium earlier, the best way to gauge IF a commodity is likely to rally hard is to try and plot what is called “incentive prices” against the chart for that particular commodity.

That is to establish where prices need to be where new discoveries need to be made and new projects need to be developed.

And where prices need to be for supply to be taken offline and exploration/development to stop.

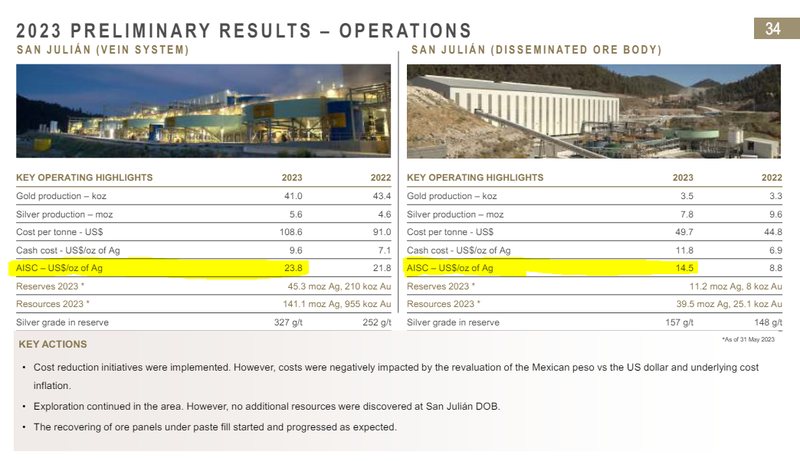

For silver the best way to establish this is to look at the world’s biggest silver producer.

Below is a slide taken from the Fresnillo 2023 results presentation which shows the All in sustaining cost (AISC) for two of its silver mines.

One is at US$21 per ounce and the other at US$14.5 per ounce.

(they must be a lot happier with silver at ~US$30 per ounce)

Naturally, their assets are in the lowest cost quartile for silver producers.

So, US$14.50 to US$21 is as good as it gets when it comes to the cost of mining silver.

( Source )

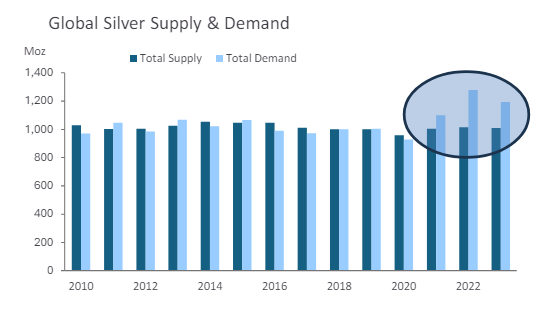

Now looking at the silver price...

The above numbers show us roughly how much it costs to mine silver.

The next thing to think about is how much a miner can sell its silver for.

For over a decade the silver price traded between ~US$13 per ounce and ~US$22 per ounce.

Those prices were nowhere near high enough to justify bringing new silver mines online, and they were especially not high enough to incentivise new exploration.

For over a decade silver prices have been trading at what we think are well below incentive prices.

It's no surprise that silver production has been in decline for the past 3 years and the market is now in a structural supply/demand deficit.

( Source )

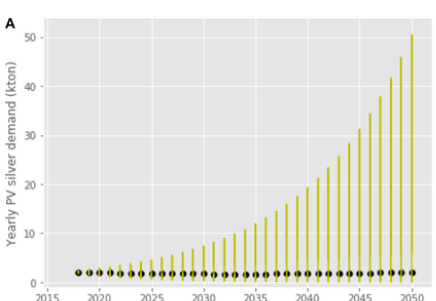

Now, we think the silver market is currently in a position where no new supply has come online for ages all while demand could be about to go exponential.

By 2050 - 50% of silver demand is expected to come from the solar panel manufacturing market. This is a relatively recent development in the silver market.

The chart below shows how demand for silver is expected to rise by over 250% by 2050 due to solar alone:

(Source)

Our view is that over the next 5-10 years, the silver price will need to go a lot higher then where it is today, to incentivise new exploration and new mine supply.

For the lithium market to incentivise new supply to come online, prices rallied over 10x in 2021...

The silver market is a lot more mature than lithium - but even if we got a 2-3x move in the silver price, we think it will bode extremely well for silver stocks.

The only difference between lithium and silver is that there are far fewer silver stocks that are positioned to take advantage of a silver bull market, especially here on the ASX.

We also noticed a mega-deal over on the US exchange with First Majestic taking out Gatos Silver for US$970M.

Could it be that the bigger players in the silver game are making a move ahead of a big silver price run?

We have two silver Investments in our portfolio at the moment.

Apart from the silver exposure they give us, both have their own unique reasons for being in our Portfolio:

- Sun Silver (ASX:SS1) - the biggest primary silver deposit on the ASX and in a part of Nevada, USA home to some of the world’s biggest silver deposits. We are Invested in this one because it could become a de-facto silver ETF on the ASX as the best way to get leveraged exposure to silver prices. (Read our SS1 Investment Memo)

- Mithril Resources (ASX: MTH) - silver and gold in Mexico (a similar part of the world to that First Majestic deal we mentioned earlier). MTH is led by John Skeet who was involved in the Bolnisi story which was taken over for US$1.1BN in Mexico back in 2008. We are hoping he can repeat that success with MTH. (Read our MTH Investment Memo)

What we wrote about this week

Sun Silver (ASX:SS1)

The US needs antimony, fast.

Our silver explorer and developer Sun Silver (ASX:SS1) has just confirmed the presence of anomalous antimony in a number of areas of of its giant silver resource in Nevada USA.

Antimony is used in infrared missiles, nuclear weapons and night vision goggles, and mostly as a hardening agent for bullets and tanks.

China is the world’s biggest supplier - responsible for ~63% of the world’s antimony needs, and their antimony export restrictions are just a few days away from taking effect.

Read: SS1’s high grade antimony readings - does it run across the whole project?

Elixir Energy (ASX:EXR)

Earlier this week, reports emerged that oil and gas supermajor Shell was flaring gas in the Taroom Trough in Queensland.

Our Investment Elixir Energy (ASX:EXR) has acreage next door to Shell in the Taroom Trough, and they’ve currently got running flow tests on their own well.

Read: Shell flared gas in the Taroom Trough - next door to EXR

AML3D (ASX:AL3)

Remember the first time you used UberEats?

The amount of choice, the speed of delivery, and the convenience?

Our 2024 Tech Pick of the Year AML3D (ASX:AL3) just signed a Manufacturing License Agreement with a US Navy intermediary...

...to increase the library of 3D printed parts that the US Navy can order from AL3.

What does this have to do with the UberEats app?

Stay with us, we explain below.

Read: AL3 Signs Key Agreement For US Navy Submarine Parts

Quick Takes

PFE Signs Rig Agreement For First Well Test

SS1 hits high grade extensions to its existing resource

GTR hits extensions to its US uranium resource

Macro News - What we are reading & listening to

Lithium:

- Hedge funds are covering shorts in lithium stocks after CATL halted production, driving prices up.

- Short-term lithium prices may rise, but a drop is possible if production resumes.

Lithium Stocks Pilbara Minerals, Tianqi Soar on Speculation CATL Suspends Mine (Bloomberg)

- Lithium stocks surged globally after CATL halted production, easing oversupply concerns.

- UBS expects an 8% supply cut and up to 23% price increase for lithium in 2024.

Lithium finds a bottom, but beware Chinese whispers and false dawns (AFR)

- Lithium stocks surged globally after speculation that CATL suspended production, easing supply concerns.

- Despite recent gains, analysts warn of potential volatility as demand remains uncertain and CATL may restart production.

MIN ASX: MinRes eyes bottom on lithium as price pain spreads to China (AFR)

- Lithium stocks surged after reports that China’s CATL suspended lithium production, signalling a potential price recovery.

- MinRes sees this as a sign of market stabilisation, with UBS predicting up to a 23% rise in lithium prices.

PLS ASX: Lithium markets brace for short squeeze as analysts tip rally to extend (AFR)

- CATL’s mine suspension triggered a short squeeze, boosting lithium stocks and carbonate futures.

- Analysts caution the rally could be brief without sustained supply cuts and improved demand.

Battery Metals:

- Major nations, including Australia, are forming a collective marketplace to reduce reliance on China for critical minerals.

- The plan seeks to boost investment and project development while countering China’s market dominance.

China Asks Its Carmakers to Keep Key EV Technology at Home (Bloomberg)

- China advises its automakers to keep advanced EV technology domestically while sending key parts for assembly abroad to avoid tariffs.

- The policy could complicate global expansion for Chinese carmakers and affect their investments in certain countries.

Nickel & Uranium:

- Putin’s suggestion to limit exports of uranium, titanium, and nickel caused prices of these commodities to spike.

- His remarks prompted a rise in shares of uranium miners and a surge in nickel prices, reflecting concerns over potential supply disruptions.

Uranium:

Italy Is in Early Talks for Creation of Nuclear-Power Company (Bloomberg)

- Italy is planning to create a new company to develop small nuclear reactors, in partnership with Ansaldo Nucleare, Enel, and Newcleo.

- This marks a significant shift for Italy, which has banned nuclear power for decades, with legislative measures expected later this year.

What we watched this week:

The Founding of Franco Nevada | Pierre Lassonde & Jimmy Connor

What we listened to this week:

Is the lithium bottom in? - Money of Mine

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.