SGA seals $5M funding injection from EU bank - PFS “imminent”

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,535,003 SGA shares and 1,466,250 SGA Options and the Company’s staff own 10,000 SGA shares and 2,500 SGA Options at the time of publishing this article. The Company has been engaged by SGA to share our commentary on the progress of our Investment in SGA over time.

An European bank just invested $5M into Sarytogan Graphite (ASX:SGA).

This was done at 16c - a premium to SGA’s last close of 14.5c.

The bank is the European Bank for Reconstruction and Development - EBRD for short.

In total, EBRD will end up with a 17.36% stake in the company.

The EBRD operates in over 30 countries and to date has invested more than €200 billion through ~7,000 projects.

Now we can add SGA to that list of projects backed by the EBRD.

SGA has a giant graphite resource in Kazakhstan, central Asia.

The company spent the last few months successfully testing its graphite product for various market use cases, while working on its PFS.

That PFS is due ‘imminently’ according to today’s SGA announcement.

Previously SGA has signalled the PFS will be due ‘no later than September 2024’.

The PFS is expected to deliver a first look at the economics of the project, and how SGA can bring its graphite to market.

We are looking forward to what the initial project economics look like for SGA, relative to its $21M market cap.

But for now, back to SGA’s new EU backer.

Securing a $5M funding round from a deep pocketed, institutional backed bank is a big achievement for a company like SGA.

It provides external validation of the project and the company’s governance, higher prospects of future support and (we hope) a network of funding opportunities for SGA to tap into.

Now a substantial shareholder of SGA, the EBRD has the financial muscle to support SGA over the long term as it moves toward production, with the ability to fund those bigger later stage CAPEX funding rounds that are inevitably required.

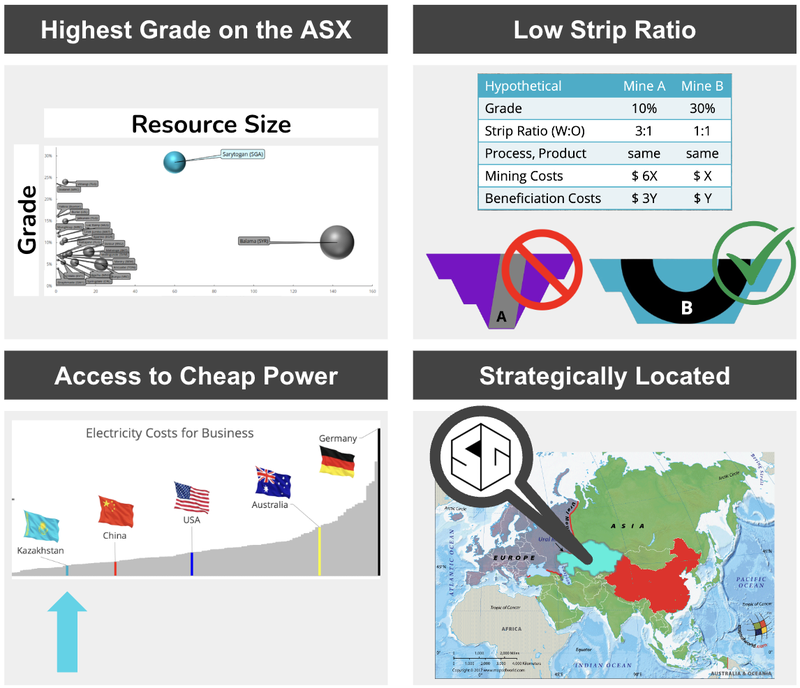

SGA has the second largest contained graphite, and the highest grade resource on the ASX.

SGA’s deposit is already giant, so no more exploration or resource definition is required - the focus is on moving through the feasibility stages and into development.

With this investment from the EBRD and with the PFS to be published imminently, it appears that SGA is in a prime position to advance its project towards development.

Why is the EBRD investing in graphite in Kazakhstan?

The EBRD is owned by 73 countries, as well as the EU and the EIB (European Investment Bank).

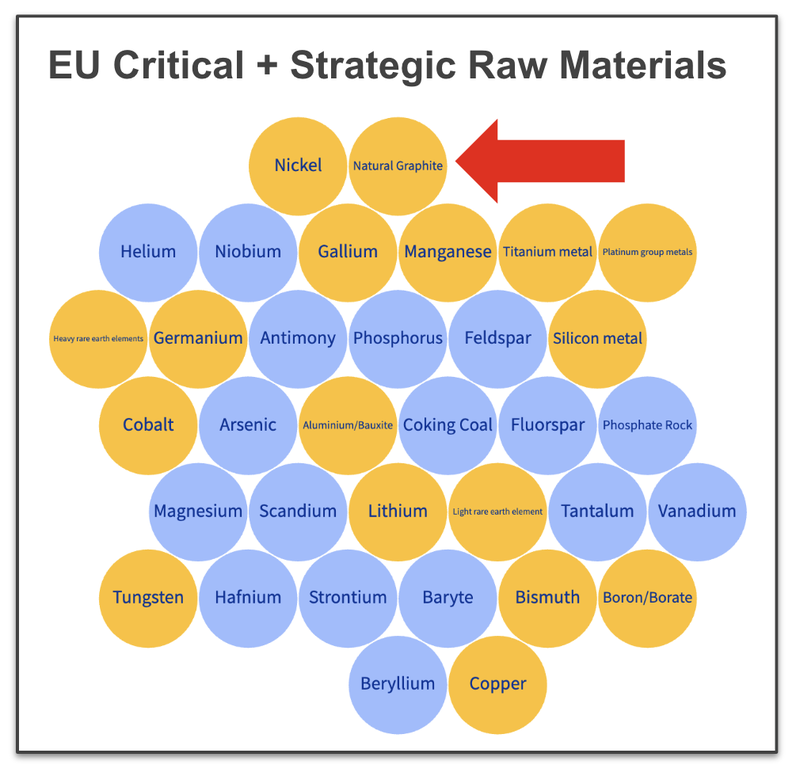

The EU is looking to grow its access to a range of raw materials to address the anticipated growing demand driven by the green transition.

The EU expects this demand to be built off the back of local production of batteries, solar panels, permanent magnets and other clean, future facing technologies.

There is a genuine scarcity surrounding critical minerals in Europe, as much of its clean technology supply chain is tied to China.

And within Europe, a huge industrial sector relies on these materials...

That’s why, in March this year, the European Critical Raw Materials Act was adopted by the European Council.

Natural graphite is considered both a “strategic” and “critical” raw material as part of the Act.

The EU’s critical raw materials act shows that the EU imports ~99% of its natural graphite consumption.

Right now China is the world’s biggest producer of graphite and controls almost ~90% of processing into finished graphite products that go into things like EV batteries.

In addition, there are not that many development ready assets with genuine scale inside the EU...

And although Kazakhstan is technically in Central Asia, back in 2022 the EU government signed an MOU with the Kazakh government to cooperate on critical minerals.

Kazakhstan sits right in the middle of China and the EU, so we think that one big reason for the EBRD investment could be because of its importance for European battery supply chains.

The European Bank for Reconstruction and Development (EBRD) was initially established to aid the development of the private sectors of formerly communist and Eastern Bloc countries, but has since expanded its scope and now works in 38 economies from central Europe to Central Asia.

The EBRD clearly wants to support the economic development of Kazakhstan and promote closer ties between the mineral rich country and the EU, and is making SGA a key part of that broader effort.

The EBRD has a rigorous due diligence process, so we think their stake in SGA is strong validation of the work SGA has done up to this point.

As SGA firms up the economics of its project, we’d be looking for the EBRD to maintain its stake in SGA in subsequent raisings as well.

Here’s what we are looking for next from SGA...

A look at SGA’s project economics are “imminent”

SGA already has a giant, high-grade JORC resource, but right now the focus is on delivering a Pre-Feasibility Study.

From SGA’s project we know that it has delivered:

- The cost to produce the commodity - usually a company needs to have high grades and a low strip ratio to be able to produce the commodity at a low cost.

- Access to cheap power - power is a big part of the variable cost of running a mine so low power costs should mean low operating costs.

- Proximity to markets (target buyers) - the closer the project to buyers the lower the cost should be to ship the product to customers.

The PFS will give investors a first look at SGA’s project economics including CAPEX, OPEX and NPV figures.

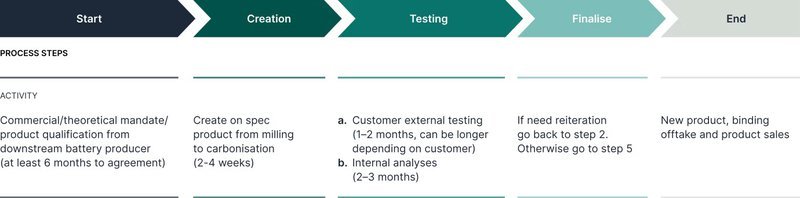

SGA has spent the last ~12 months running through all of the metallurgical testing to see the different types of graphite products that it can produce.

Product testing is important because at the end of the day the more markets SGA can tap into, the higher the prices it can get for its graphite.

And to sell the product to serious buyers, SGA first needs to prove its graphite can perform.

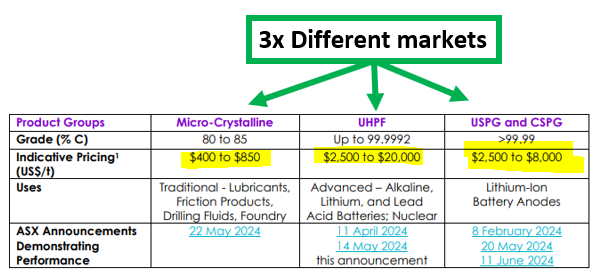

SGA has a product strategy to “place as many units of carbon into as many markets as possible”

This is more refined in the most recent quarterly, with a table showing SGA’s plan to sell to three key markets where prices range from US$400/tonne to US$20,000/tonne.

The three markets are as follows:

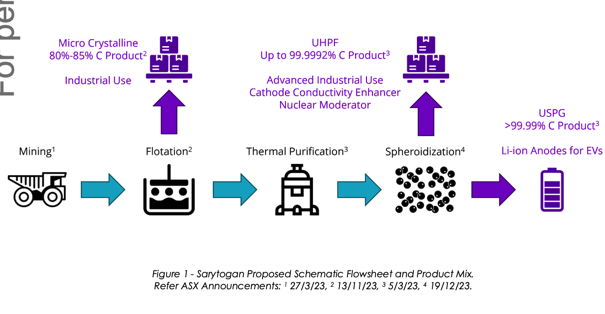

This simple chart shows the proposed flow sheet and where each product can be delivered:

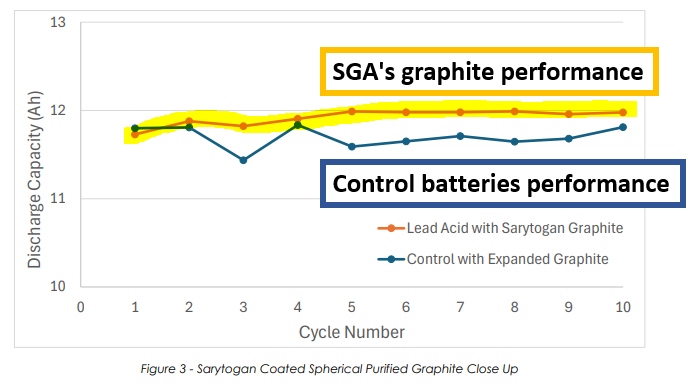

The most recent news from SGA was from testing its graphite in lead acid batteries which fit into the “UHPF” category where prices can be up to US$20,000 per tonne.

SGA showed that its graphite performed strongly in lead acid batteries with higher and more consistent discharge capacity compared to the batteries in the market right now.

The market didn't really react to the news but from a technical perspective we think that was an important announcement.

Lead acid batteries are the most widely used battery chemistry in the world and the expandable graphite used to produce them can sell for up to US$20,000 per tonne.

SGA’s product performing better than a control battery could be a sign that SGA tries to focus on selling into this market where prices are highest, and margins should be a lot higher.

We think that the higher prices are especially important because they will be what SGA plugs into its Pre Feasibility Study (PFS) and will influence the project's NPV numbers.

We are hoping to see SGA put out relatively strong NPV numbers... especially relative to its current market cap of ~$21M.

Ultimately we expect to see SGA’s share price re-rate in line with the project economics numbers that feasibilities show and we hope that the studies help SGA achieve our Big Bet which is as follows:

Our SGA “Big Bet”

“Given this graphite project’s strategic location in between China and Europe, we hope that if SGA proves out the size and economic extractability of the resource, it will generate interest from major mining companies, leading to a takeover of SGA for $1 billion+.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

How today’s news relates to our SGA Investment Memo

The EBRD investment is strong validation that SGA’s project is critical to the European Critical Minerals strategy.

We forecast this in our “why we invested” in our SGA memo:

Project located in Kazakhstan - an established mining jurisdiction between EU and China

Kazakhstan’s mining legislation is based on Western Australia’s mining code. The country is the biggest producer of uranium in the world producing ~45% of global supply in 2021. Companies like Chevron and Exxon Mobil own and operate projects in-country. Kazakhstan’s unique location also presents itself as a future supplier of battery metals to downstream users in Europe and China.

Source: “Why we Invested” - SGA Investment Memo 22 July 2022

SGA also has a tight cap structure with ~149 million shares on issue prior to the EBRD investment.

Having listed in July 2022, there were around ~65.7 million in shares that came out of escrow last month having been subject to a 24 month escrow condition. (Source: Prospectus, p. 46-47)

The fact that the share price has held up reasonably well in this context, we think shows that the holders are sticky, and looking for SGA to succeed over a longer period of time.

EBRD will take on more than 17% of the SGA share register, but will likely be a long term holder of the shares.

Therefore, with another long term institutional investor on board, the “free float” of the company’s share registry will be maintained.

This means a higher potential for a share price re-rate on positive, unexpected results.

Tight capital structure

There are only 132 million shares currently on issue. 54% of SGA’s shares are escrowed (mostly for two years from the IPO date). This includes the 39% held by founder and Technical Director Dr Waldemar Mueller. There is therefore a limited number of shares available in the event that there is increased demand - we think the SGA capital structure is leveraged to growth.

Source: “Why we Invested” - SGA Investment Memo 22 July 2022

What are the risks?

One of the key risks with any graphite project is “customers”.

Unlike the copper or gold markets, where the commodity can easily be sold into a metals exchange (as a fungible asset), graphite needs a more tailored approach.

If SGA is unable to source enough customers with its graphite project (customers being offtake agreements) then it will be difficult to secure funding for its mine.

One of the challenges in the short term for securing customers is “product qualification risk”.

Over recent months SGA has produced various graphite types including battery grade graphite, and tested the products successfully.

Next it needs to take those products and test results to qualified buyers to see if it can get any early commitments on sales.

This process can take a while to complete (up to 2 years in extreme scenarios) AND there is never a guarantee that SGA gets past the prospective qualification stage.

Securing customers for its graphite is the key risk we see for SGA project going forward given it has ticked all the boxes so far when it comes to the development stages.

To see more risks that we listed as part of our SGA Investment Memo click here.

Our SGA Investment Memo

Below is our Investment Memo for SGA, where you can find a short, high level summary of our reasons for Investing.

In our SGA Investment Memo, you’ll find:

- Our SGA Big Bet

- Key objectives went want to see SGA achieve

- Why we are Invested in SGA

- What the key risks to our Investment Thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.