Graphite is Back. SGA preps more samples to repeat 99.99% battery grade test success.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,354,500 SGA shares and 1,466,250 SGA options, the Company’s staff own 30,000 SGA shares and 7,500 options at the time of publishing this article. The Company has been engaged by SGA to share our commentary on the progress of our Investment in SGA over time.

Like most battery materials, graphite sentiment has taken a breather this year.

But some global developments over the last couple of weeks have seen a renewed interest in graphite and graphite stocks.

First...a big investment bank called the bottom on graphite.

Then increased energy prices made synthetic graphite too expensive.

And finally China introduced graphite export curbs.

Suddenly, graphite was back in vogue, taking share prices of graphite stocks up with it.

Until the last couple of weeks, the interest in graphite had been low during 2023. It meant for much of the year, graphite stocks were making progress but not being rewarded with share price rerates.

Our Investment Sarytogan Graphite (ASX:SGA) is no exception.

SGA is developing a giant (second largest on the ASX), high grade (highest on the ASX) graphite resource in Kazakhstan, a country in between Europe and China.

SGA has confirmed its resource can be produced to 99.99% purity, which is a requirement to sell into the battery anode markets.

SGA IPO’d back in July 2022. After spending most of its first year on the ASX above 35c and touching as high as 55c, it has gradually found its way back to around the 20c IPO price as sentiment in graphite worsened.

SGA has been making solid progress during 2023, but has not been rewarded by the market during a period of low graphite sentiment.

SGA is currently trading around 20c - its mid-2022 IPO price. It had $6.5M cash in the bank at the end of September.

Since its IPO, it has delivered:

- A big resource upgrade - SGA added ~10% to its already large resource and upgraded ~55% into a higher confidence interval (indicated). The result was well above our bull case expectation of wanting to see SGA upgrade ~20%.

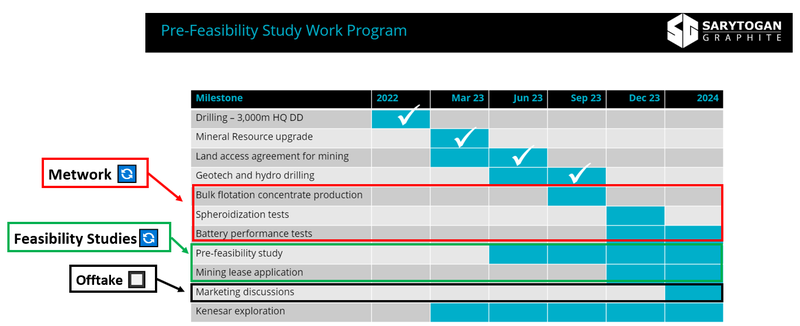

- Kicked off its Pre Feasibility Study - SGA kicked off its PFS in June and has already managed to finalise a lot of the typical inputs that go into a PFS (i.e flowsheet tweaks, resource sizes etc).

- 99.99% Ultra high purity graphite produced - SGA far exceeded battery grade graphite purity, achieving this through flotation, alkaline roasting and thermal purification.

This was a major catalyst for SGA but the market seemingly shrugged it off.

This morning SGA announced that bulk graphite concentrate samples had been sent off to testing labs for “spheroidization, purification and battery testing”.

The testing is the final stage where SGA checks to see how its graphite would perform when used in actual batteries - usually an important bit of technical information buyers/potential offtake partners want to see.

Graphite is one of the most important inputs in an EV battery.

Graphite makes up ~50% of the raw materials in every lithium-ion battery and over 95% of every battery anode.

Without graphite, the EV battery supply chain just doesn't function.

SGA could have an outsized role in the EV battery supply chain, by virtue of the sheer scale of its resource and strategic position in Kazakhstan.

SGA has:

- The highest grade graphite resource on the ASX - Higher grades typically lead to lower costs of processing a resource into a final saleable product.

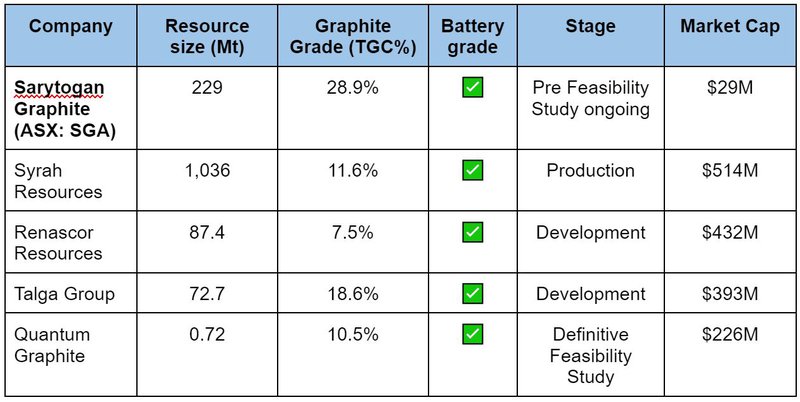

- The second largest graphite resource on the ASX in terms of contained graphite. Second only to Syrah Resources, which is capped at $514M.

- Battery grade product - A graphite resource that can be processed to a high enough purity to be sold into high value battery anode markets (99.99% purity).

SGA’s project is now in the feasibility stage, with its Pre-Feasibility Study (PFS) due to be completed no later than Q3 next year.

Despite the size and scale of SGA’s project its market cap is well below its ASX graphite peers.

SGA is capped at ~$29M, whereas its graphite peers are capped at many multiples higher:

Our view is that once SGA releases its PFS and puts out financials around its giant JORC resource, the company’s market cap could re-rate in line with its ASX peers.

We are hoping that news coincides with strength across the whole graphite macro thematic.

Graphite macro theme about to go exponential?

Earlier in the year, we said that we thought graphite could be “the next lithium” in 2023.

Our view was that as demand for electric vehicles (EVs) increased, demand for graphite would increase with it, and graphite projects would be bid up the same way lithium explorers & developers were over the last few years.

Our view has not changed, but so far in the short term it hasn't entirely played out that way...

Graphite prices are down for the year (the same way lithium prices are), AND sentiment across the sector was at rock bottom.

Mainly because low energy prices in the first half of the year meant heaps of low-cost synthetic (lab-produced) graphite could be produced out of China, reducing demand for natural (mined) graphite.

The overwhelming narrative in the market was that the world couldn't compete with low cost synthetic graphite out of China...

Over the last few weeks, everything may have changed, though...

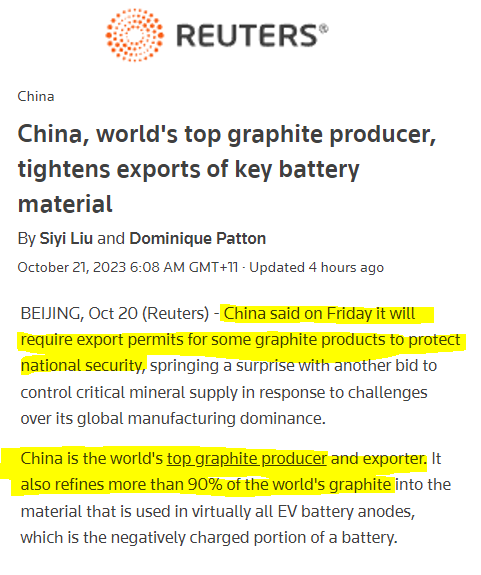

The Chinese government announced export restrictions on some graphite products to “protect national security” potentially putting most of the world's graphite supply at risk.

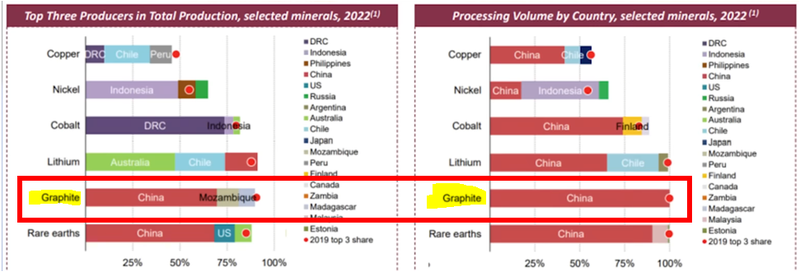

For some context - over 80% of graphite and almost 100% of graphite battery anodes are produced in China.

(Source)

A few weeks ago, UBS also put out a report saying that they think graphite is going to have its moment in the sun...

(Source)

Graphite stocks have already started responding, with most up 10-20% on the first day of trading after that news.

Since the news came out, Syrah Resources which is seen as the ASX’s indicator for health in the graphite sector added a peak of ~$358M to its market cap and was up over ~120%.

In the weeks before the news Syrah’s share price was ~42c (a 52 week low), it peaked around ~95c before cooling off to its current share price.

Why we think SGA stands to benefit the most from the macro

We think countries looking to bullet proof their battery metals supply chain will be forced to look for alternate supply routes outside of China.

The projects closest to development (feasibility stage/development ready) will be the ones to benefit the most from the flow of capital into the sector.

Projects in jurisdictions favourable to mining and a clear pathway to getting into production will also benefit.

We think SGA fits that bill with its:

✅ High grade, large scale and currently in feasibility stage - SGA’s project has:

- The second largest graphite resource in terms of contained graphite.

- The highest grade resource on the ASX.

- The project is currently in the pre-feasibility study (PFS) stage.

✅ Project is in an established mining jurisdiction (Kazakhstan) -

SGA’s project is located in Kazakhstan - the world’s largest producer of uranium.

Interestingly, Kazakhstan’s mining legislation has been brought into line with Western Australia’s Mining Code (Standard Subsoil-Use Code in 2018), which is well understood by the global investment community.

It also has a lower corporate tax rate than Australia at 20%; mineral royalty of 3.5%; and other taxes of 1.5%.

Importantly SGA’s project is located to service large battery manufacturing hubs in both Europe and in China and is close to infrastructure on China’s One Belt, One Road Initiative.

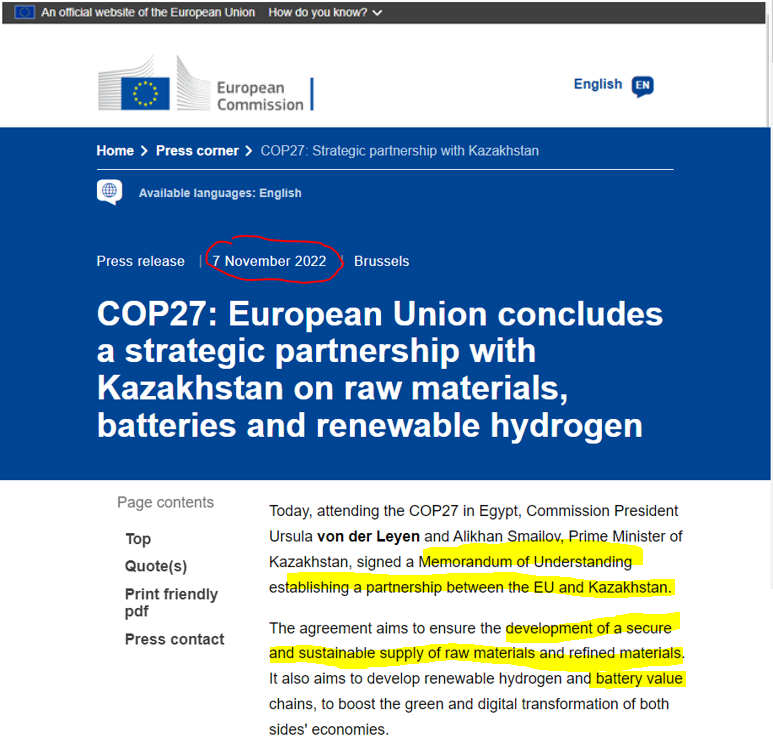

✅ Kazakhstan signed an MOU with the European Union -

In November 2022 the European Union (EU) signed an MoU with Kazakhstan to establish a partnership on battery materials supply, specifically to:

“...allow both sides to advance trade and investments into a secure, sustainable and resilient raw materials value chain, which is key to achieving the transition to climate-neutral and digitalised economies.”

Interestingly, the European Union currently gets 98% of its natural graphite from imports.

We think the MOU strengthens the potential strategic value SGA’s project might have in the future.

Ultimately, we are long term SGA holders and want to see the company take its project through the feasibility study stage and into a position where the company achieves our “Big Bet”.

Our SGA “Big Bet”

“Given this graphite project’s strategic location in between China and Europe, we hope that if SGA proves out the size and economic extractability of the resource, it will generate interest from major mining companies, leading to a takeover of SGA for $1 billion+.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Sarytogan Graphite

ASX:SGA

Our take on the Graphite macro thematic:

In the rest of today’s note, we will touch on:

- Why sentiment in the graphite sector hit rock bottom

- How the outlook is now changing for the better

- How we are Investing in the graphite space right now

Why was the graphite sector so hated?

The primary factors for the slowdown:

- Graphite prices down for the year - Low energy prices made synthetic (lab produced) graphite out of China more competitive versus natural (mined) graphite.

- EV demand lower for the year - demand for electric vehicles was lower in the first half of the year because of temporary changes to Chinese EV subsidies.

So, the graphite market was hit with a perfect storm of lower demand for graphite from battery anode producers and cheaper supply from synthetic graphite producers in China.

Things looked dicey for the first three quarters of 2023, with graphite prices down and sentiment in the sector at rock bottom.

Sentiment and prices were so low that Syrah Resources stopped production at its project in Mozambique, choosing to stockpile graphite instead of selling it into the market.

Syrah owns the world's biggest mine OUTSIDE of China, which is a good indicator of strength/weakness in the graphite market.

Why is the outlook for graphite much stronger now?

It boils down to the same reasons that led the market to lower in the first three quarters of this year.

- Energy prices have gone up A LOT - oil prices are up ~35% and natural gas prices are also rallying. Tensions in the Middle East are boiling over & the Russia/Ukraine conflict is ongoing. Overall, the pressure is on energy prices to go higher and stay higher...

- A potential Chinese export ban puts ~80% of the market at risk - China produces ~80% of the world’s graphite and controls almost 100% of battery anode production. Without Chinese graphite anodes, the whole EV battery supply chain is at risk.

(Source)

- Alternative supply isn't available - Outside of Syrah’s mine in Mozambique, there are no major mines that can be put into production to diversify supply IF China curbs exports in any major way.

(Source)

How we are Investing in the graphite sector right now

As mentioned, we think the projects most likely to benefit from the macro tailwinds for the sector will be those nearest to development/production or those with size/scale potential.

The graphite sector is a lot more dynamic versus other commodity sectors primarily because mined graphite can be replaced by synthetic, lab produced graphite.

As a result, price runs in the graphite market are typically short lived and unlikely to see the mega runs like we have seen in the lithium space.

As soon as prices get too high, the synthetic graphite producers increase capacity in their plants and supply the market until supply/demand is back into equilibrium.

All that means graphite prices trade in a narrower band where only the highest quality, lowest cost graphite mines can eek out profits.

Our view is that the projects with superior orebody characteristics (flake size differentiation etc.) and those with true size/scale potential (low cost) will be the ones to benefit the most.

Just like the lithium sector is seeing takeover offers being flung around for late-stage, giant projects.

We expect most of the capital that flows into the graphite sector to be focused on a small number of highest-quality projects.

Currently, our focus is less on identifying new opportunities and more on following through our existing investments in follow-up funding rounds as they progress to development.

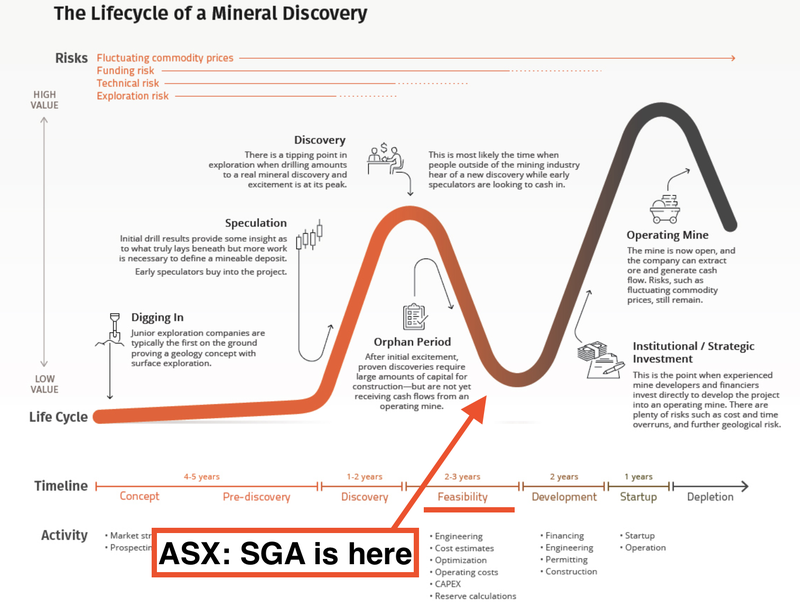

SGA is currently at the bottom of the Lassonde Curve:

What’s Next for SGA?

Ongoing metwork 🔄

Having now surpassed 99.95% TGC purity levels, the next phase of work will be about optimising and scaling up its flowsheet.

SGA mentioned in today’s announcement that bulk flotation tests were already underway, with multiple labs worldwide having received 3-6kg samples for spheroidization, purification and battery testing.

The whole purpose of the current stage of works is to try and test SGA’s flowsheet with larger sample sizes and see if it is scalable.

Read our quick take of the flotation news here: Higher Concentrate Graphite Grades Achieved

Feasibility Studies 🔄

SGA expects to deliver the Pre-Feasibility Study (PFS) in Q3 of 2024.

In today’s announcement, SGA confirmed that the spherodization and battery testing would be the next bit of information plugged into the PFS.

What are the risks?

In the short term, a key risk to SGA’s share price is the graphite price.

While sentiment has started changing after the China news about restricting exports, graphite prices are yet to rally hard off the back of the news.

There is always a risk that prices lag and that companies like SGA are impacted by not being able to raise funds in the short-run.

To see the risks in detail, check out the Memo here, or click on the image below:

Our SGA Investment Memo

Below is our Investment Memo for SGA, where you can find a short, high level summary of our reasons for Investing.

In our SGA Investment Memo, you’ll find:

- Our SGA Big Bet

- Key objectives went want to see SGA achieve

- Why we are Invested in SGA

- What the key risks to our Investment Thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.